In an increasingly digital financial world, the humble paper check might seem like an anachronism to some. Yet, for many, it remains a fundamental tool for payments, record-keeping, and financial transactions. Whether you’re paying rent, settling an invoice, or setting up a direct debit, understanding the anatomy of a check – and particularly how to locate the check number – is a crucial piece of financial literacy. This seemingly simple query unlocks deeper insights into financial security, record reconciliation, and the mechanics of the banking system itself.

Far from being a mere decorative digit, the check number serves as a unique identifier, a financial fingerprint that meticulously tracks each transaction. For individuals and businesses alike, knowing where to find this number is not just about filling out a form; it’s about maintaining financial order, preventing fraud, and ensuring smooth operations. This guide will demystify the check number, revealing its location, its significance, and its role in both traditional and evolving payment landscapes.

Understanding the Anatomy of a Check

Before we pinpoint the check number, it’s essential to understand the broader context of a check’s design. A check is more than just a piece of paper; it’s a legally binding instruction to your bank to pay a specified amount of money from your account to another party. Each element on a check serves a distinct purpose, creating a comprehensive financial instrument. Familiarity with these components not only helps in identifying the check number but also in comprehending the entire payment process and bolstering your financial awareness.

Key Components Beyond the Check Number

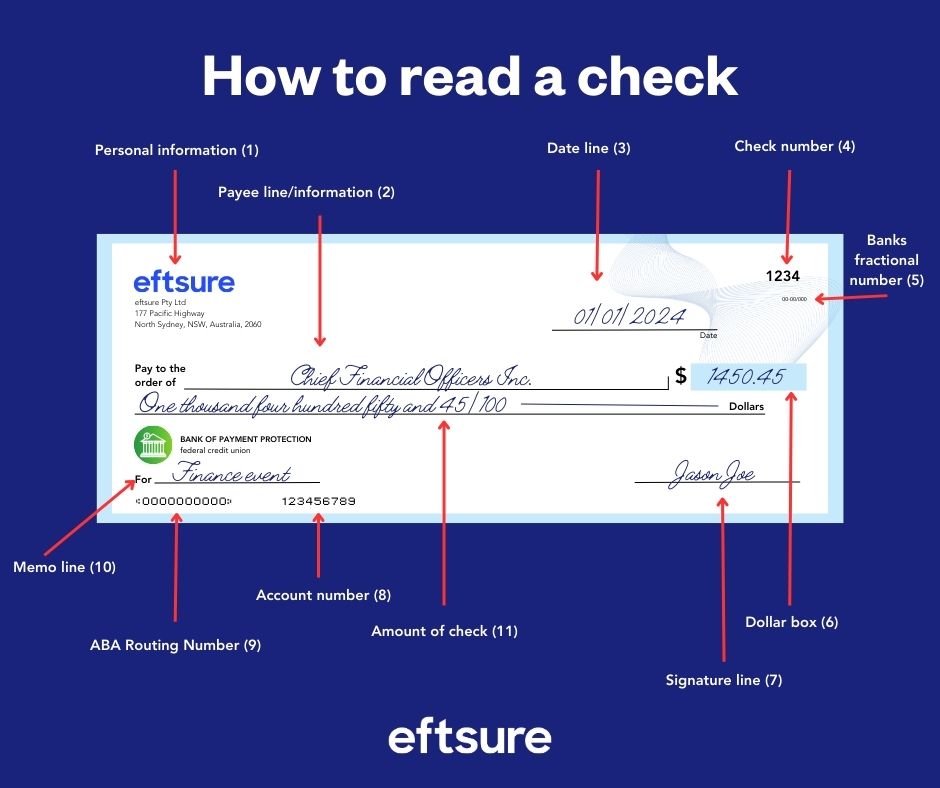

While the check number is our primary focus, it’s surrounded by other vital pieces of information. At the top of the check, you’ll typically find your name and address, ensuring the recipient knows who the payment is coming from. Below this, there’s a date line, indicating when the check was written. The “Pay to the order of” line designates the recipient, and the dollar box, along with the written amount line, specifies the exact sum to be paid. A memo line offers space for a brief description of the payment, useful for personal record-keeping or clarifying the purpose of the transaction to the recipient. Finally, your signature line at the bottom right corner authorizes the payment, making the check legally valid. Each of these components plays a role in the integrity and functionality of the check, but it’s the sequence of numbers at the bottom that holds the key to automated processing and unique identification.

The Routing Number: Your Bank’s Address

Beneath the main body of the check, along the bottom edge, you’ll find a series of numbers printed in a special font known as MICR (Magnetic Ink Character Recognition). The first set of numbers, typically nine digits long, is the routing number. Think of this as your bank’s specific address within the vast financial network. This number identifies the financial institution that holds the account, directing the payment to the correct bank for processing. Different banks have different routing numbers, and sometimes even different branches of the same bank may have distinct routing numbers. When setting up direct deposits, bill payments, or linking external accounts, the routing number is paramount in ensuring funds are transferred to the correct financial institution. It’s the foundational identifier for the banking system itself, making sure your money goes to the right place.

The Account Number: Your Personal Identifier

Immediately following the routing number on the MICR line (or sometimes separated by a symbol), you’ll find your account number. This is your unique identifier within your specific bank, distinguishing your checking account from all others. It tells the bank which specific account the funds should be drawn from. While routing numbers identify the bank, account numbers pinpoint the exact destination or source of funds within that bank. This number is highly sensitive and should be protected, as it provides direct access to your funds. Together, the routing number and account number form the core digital instructions necessary for processing any check or electronic funds transfer. Understanding these two critical pieces of information is foundational to managing your money, setting up recurring payments, and protecting your financial security.

Locating the Check Number: Your Financial Fingerprint

With an understanding of the overall check structure, identifying the check number becomes straightforward. It is specifically designed to be easily accessible yet robustly integrated into the check’s unique identifier system. While checks might appear similar, the check number is the serial code that differentiates one from another, making each payment traceable and distinct. Knowing its typical locations is essential for accurate record-keeping and for providing correct information when asked for it.

The Traditional Spot: Top Right Corner

For most standard personal and business checks, the most common and easily visible location for the check number is in the top right corner of the check. It’s usually a small, standalone number, often starting from 001 and increasing sequentially with each new check in your checkbook. This prominent placement makes it convenient for the check writer to quickly reference and record the number when issuing a payment. When you look at a check, your eye is often drawn to the amount and payee, but glance upwards and to the right, and you’ll almost certainly spot this number. Its simplicity and consistent placement have made it the primary reference point for individuals reconciling their bank statements or tracking individual transactions manually.

The MICR Line: The Digital Read

Beyond its visible location in the corner, the check number also appears as part of the Magnetic Ink Character Recognition (MICR) line at the very bottom of the check. This is the sequence of numbers printed in a distinct, often bold and somewhat blocky font, which is designed to be machine-readable by automated check-processing equipment. The check number is typically the last set of numbers on this MICR line, usually following the account number. Sometimes it might be preceded by a symbol (like ⑈). While the human-readable number in the top right corner serves for manual reference, the MICR line version is critical for the automated clearing system. It ensures that when a check is deposited and processed, the banking system can quickly and accurately identify the specific check, its source account, and its destination, without human intervention. This dual placement underscores its importance both for personal record-keeping and for the modern financial infrastructure.

Variations and Exceptions

While the top right corner and the end of the MICR line are the standard locations, it’s worth noting that some variations can exist, particularly with specialized checks or financial institutions. For instance, some business checks or temporary checks might place the number in a slightly different corner or use a different formatting on the MICR line. Occasionally, starter checks issued directly by a bank might not have pre-printed check numbers in the same sequential order as a full checkbook. Furthermore, checks issued by credit unions or smaller regional banks might have subtle differences in their layout compared to larger national banks. However, even with these minor variations, the principle remains: the check number will always be present, unique, and consistently positioned either in a corner or as part of the machine-readable MICR sequence at the bottom. If you ever have difficulty locating it, referring to an example check provided by your bank or checking your online banking portal for an image of a cleared check can quickly clarify its specific placement.

Why the Check Number Matters: Beyond Just Identification

The check number is far more than just a sequential marker; it’s a vital component of financial security, record-keeping, and the broader payment ecosystem. Its significance extends beyond merely identifying an individual check, playing a crucial role in preventing fraud, simplifying reconciliation, and facilitating essential financial services. Understanding why this small number is so important empowers you to manage your finances more effectively and safeguard your assets.

For Reconciliation and Record-Keeping

One of the primary reasons the check number is indispensable is for financial reconciliation and meticulous record-keeping. Every time you write a check, it’s prudent to record the check number, the payee, the date, and the amount in your checkbook register or personal finance software. When your bank statement arrives, whether physically or digitally, it will list all the checks that have cleared your account, identified by their unique check numbers. By comparing your records with the bank’s statement, you can ensure that all transactions match, that no unauthorized checks have cleared, and that your account balance is accurate. This process of reconciliation is critical for personal budgeting, tax preparation, and quickly identifying discrepancies or errors. Without the check number, tracking specific payments would be a convoluted and error-prone task, making it nearly impossible to maintain a precise financial overview.

Fraud Prevention and Security

The check number also serves as a critical tool in fraud prevention and security. Because each check number is unique and sequential, it helps banks and account holders detect suspicious activity. If multiple checks with the same number appear, or if a check number is out of sequence, it could be an immediate red flag for potential fraud, such as counterfeiting or alteration. When you report a lost or stolen checkbook, providing the range of missing check numbers allows your bank to place alerts on those specific checks, preventing them from being cashed by unauthorized individuals. Furthermore, if you suspect that a check you wrote was altered after you issued it, the check number, combined with your records, provides crucial evidence for investigation. In an era where financial scams are increasingly sophisticated, the simple sequential nature of the check number adds an essential layer of traceability and accountability, safeguarding your funds against illicit activities.

Initiating Payments and Setting Up Services

Beyond internal record-keeping and security, the check number is often required when initiating certain payments or setting up various financial services. For instance, some utility companies, landlords, or subscription services may ask for a check number when you make an initial payment, especially if you are setting up recurring direct debits or electronic fund transfers (EFTs) from your checking account. This is particularly true for “voided checks” – a check written with “VOID” across it, which is used to provide your routing and account numbers to a third party (like an employer for direct deposit) without authorizing a payment. Even in these cases, the check number is still a part of the document being shared, reinforcing the unique identification of that particular financial instrument and the associated account. In essence, the check number is a foundational element that underpins many aspects of personal and business financial administration, demonstrating its enduring relevance in a diverse financial landscape.

Modern Alternatives and Digital Checking

While the paper check and its identifiable number remain a cornerstone for many transactions, the financial world is rapidly evolving. Digital innovation has introduced a plethora of alternative payment methods that offer speed, convenience, and often enhanced security. Understanding these modern alternatives and how they relate to the traditional check number is crucial for navigating the contemporary financial landscape and making informed choices about managing your money.

Virtual Check Numbers and Online Bill Pay

The concept of a “check number” has subtly transitioned into the digital realm with the advent of virtual check numbers and robust online bill pay systems. When you use your bank’s online bill pay service, you’re essentially authorizing your bank to make payments on your behalf. Depending on the payee, your bank might send an electronic payment (ACH transfer) or, in some cases, print and mail a physical check. When a physical check is mailed via online bill pay, it will still have a check number, often generated sequentially by the bank’s system. However, for electronic payments, there isn’t a physical check number in the traditional sense. Instead, transactions are identified by unique transaction IDs or confirmation numbers provided by your bank. These digital identifiers serve the same purpose as a physical check number: they allow for tracking, reconciliation, and verification of payments, offering a digital equivalent for an analog concept. This shift emphasizes that the principle of a unique transaction identifier is more important than the physical format.

The Evolution of Payment Methods

The financial industry has witnessed a dramatic evolution of payment methods, moving from purely cash and checks to a broad spectrum of digital options. Debit cards, credit cards, wire transfers, ACH transfers, mobile payment apps (like Venmo, Zelle, PayPal), and even cryptocurrencies have all emerged as viable alternatives to writing a physical check. Each of these methods comes with its own set of identifiers – transaction IDs, authorization codes, wallet addresses – that fulfill the role of tracking and authentication previously handled solely by the check number. This proliferation of options offers greater flexibility and often faster processing times. While some individuals and businesses still prefer checks for certain transactions due to habit, security concerns, or a need for a physical paper trail, it’s clear that the demand for instant, digital payment solutions is growing, further diversifying how we manage our money and identify transactions.

Best Practices for Digital Financial Management

As digital checking and electronic payments become more prevalent, adopting best practices for digital financial management is paramount. Just as you protect your physical checks, you must safeguard your online banking credentials. This includes using strong, unique passwords, enabling two-factor authentication, and regularly monitoring your online banking statements for any unauthorized activity. Understanding how transaction IDs work for digital payments is the modern equivalent of understanding check numbers for paper checks. Keep detailed digital records of all online payments, including confirmation numbers and recipient details, to facilitate reconciliation. Be cautious of phishing attempts and suspicious links that could compromise your account information. The convenience of digital finance comes with the responsibility of robust cybersecurity. By staying informed about the various payment methods, their unique identifiers, and the associated security measures, individuals and businesses can confidently navigate the future of money, combining the reliability of traditional financial tools with the efficiency of modern technology.

Safeguarding Your Financial Information

Whether dealing with physical checks or digital transactions, protecting your financial information is non-negotiable. The check number, along with your routing and account numbers, represents a gateway to your funds. Understanding how to safeguard these critical identifiers is essential for preventing fraud, identity theft, and unauthorized access to your money. Proactive security measures are your first line of defense in an increasingly complex financial landscape.

Protecting Physical Checks

Despite the rise of digital payments, many individuals and businesses still rely on paper checks. Therefore, protecting your physical checks remains a fundamental security practice. Treat your checkbook like cash or a credit card; do not leave it unattended or in plain sight. Store your checkbook in a secure location at home or in the office. Never sign blank checks, as this makes them easy targets for fraudsters to fill out and cash. When writing a check, always use a pen with indelible ink to prevent alterations, and fill in all lines to leave no room for additional digits or text. If a check is voided, tear it into multiple pieces before discarding to prevent anyone from retrieving your account information. Regularly reconcile your checkbook with your bank statements to quickly identify any missing or fraudulent checks. If you notice any checks missing or believe your checkbook has been compromised, immediately notify your bank and place a stop payment order on the missing checks.

Online Security for Banking Information

In the digital age, online security for banking information is equally, if not more, critical than protecting physical documents. Your routing and account numbers, typically found on checks, are also accessible through your online banking portal and are the keys to setting up electronic transfers. Always ensure you are using a secure, private internet connection when accessing your bank accounts, and never log in from public Wi-Fi networks. Use strong, unique passwords for all your online financial accounts and enable multi-factor authentication (MFA) whenever possible. Be extremely wary of unsolicited emails, texts, or phone calls asking for your banking information, account numbers, or passwords – these are often phishing attempts designed to steal your credentials. Regularly check your bank statements and transaction history online for any suspicious activity. If you identify any unauthorized transactions, report them to your bank immediately. Adopting a vigilant approach to online security is crucial to preventing identity theft and protecting your digital funds.

What to Do if a Check is Lost or Stolen

Even with the best precautions, accidents happen. Knowing what to do if a check is lost or stolen is a crucial part of financial preparedness. If you realize a blank check from your checkbook is missing, or if an issued check never reached its intended recipient and appears lost, contact your bank immediately. Provide them with the check number (if it was an issued check), the date, and the amount, and request a “stop payment” order. This legally prevents the bank from honoring the check if it is presented for payment. Be aware that banks typically charge a fee for stop payment orders. If an entire checkbook or a significant number of blank checks are stolen, it’s vital to notify your bank right away so they can flag your account and advise you on further security measures, which may include closing the compromised account and opening a new one. Additionally, monitor your bank statements closely for several months for any suspicious activity. Taking swift action in such scenarios can significantly mitigate potential financial losses and protect your identity from being exploited.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.