In the world of personal and business finance, interest is the fundamental “price” of money. Whether you are looking to purchase a home, finance a car, grow a small business, or simply watch your savings account flourish, understanding how interest rates are calculated is essential for making informed financial decisions. Interest is essentially a fee paid by a borrower to a lender for the use of assets. For the borrower, it represents the cost of debt; for the lender or saver, it represents the return on investment.

However, interest is rarely a single, static number. It fluctuates based on economic conditions, mathematical formulas, and risk assessments. To truly master your finances, you must look beyond the percentage sign and understand the mechanics behind the math.

The Fundamentals of Interest Calculation: Simple vs. Compound

At its core, interest calculation follows two primary philosophies: simple and compound. Understanding the difference between these two is the first step in recognizing why some debts disappear quickly while others seem to grow indefinitely.

Simple Interest: The Linear Growth Model

Simple interest is the most straightforward way to calculate the cost of a loan or the growth of an investment. It is calculated solely on the principal amount—the original sum of money borrowed or invested. The formula is universally recognized as:

Interest = Principal × Rate × Time (I = P × r × t)

For example, if you borrow $10,000 at a 5% annual simple interest rate for three years, you would pay $500 in interest each year. By the end of the term, you would have paid a total of $1,500 in interest. Simple interest is commonly used for short-term personal loans and some types of consumer automobile loans. Because it does not “stack,” it is generally more favorable for borrowers than for lenders.

Compound Interest: The Power of Exponential Growth

Compound interest is often referred to as “interest on interest.” Unlike simple interest, compound interest is calculated on the initial principal and also on the accumulated interest of previous periods. This creates an exponential growth curve that can work for you (in savings) or against you (in debt).

The formula for compound interest is more complex:

A = P(1 + r/n)^{nt}

(Where A is the final amount, P is the principal, r is the annual interest rate, n is the number of times interest compounds per year, and t is the time in years.)

The frequency of compounding—whether it’s daily, monthly, or annually—makes a significant difference. The more frequently interest is compounded, the higher the total interest will be. This is why a savings account with monthly compounding will yield more than one with annual compounding, even if the interest rate is identical.

Frequency Matters: Monthly, Quarterly, and Annual Compounding

The “compounding period” is a crucial variable in the interest equation. In the banking world, most savings accounts and credit cards compound interest daily or monthly. For a saver, daily compounding is the “gold standard” because your money begins earning interest on the previous day’s interest almost immediately. Conversely, for a credit card holder, daily compounding is one reason why high-interest debt can become unmanageable so quickly; the balance grows every single day that it remains unpaid.

Understanding APR vs. APY: What Borrowers and Savers Need to Know

When you look at financial products, you will frequently see two acronyms: APR and APY. While they may look similar, they serve different purposes and provide different insights into the actual cost or return of a financial product.

Annual Percentage Rate (APR): The True Cost of Borrowing

The APR is the standard measure used for loans, mortgages, and credit cards. It represents the annual cost of a loan to a borrower, including not just the interest rate, but also any fees or additional costs associated with the transaction (such as origination fees or points in a mortgage).

The APR provides a more “all-in” picture than the nominal interest rate alone. For instance, two lenders might offer the same 4% interest rate on a mortgage, but one might charge $5,000 in closing fees while the other charges $2,000. The lender with higher fees will have a higher APR, signaling to the borrower that the loan is actually more expensive.

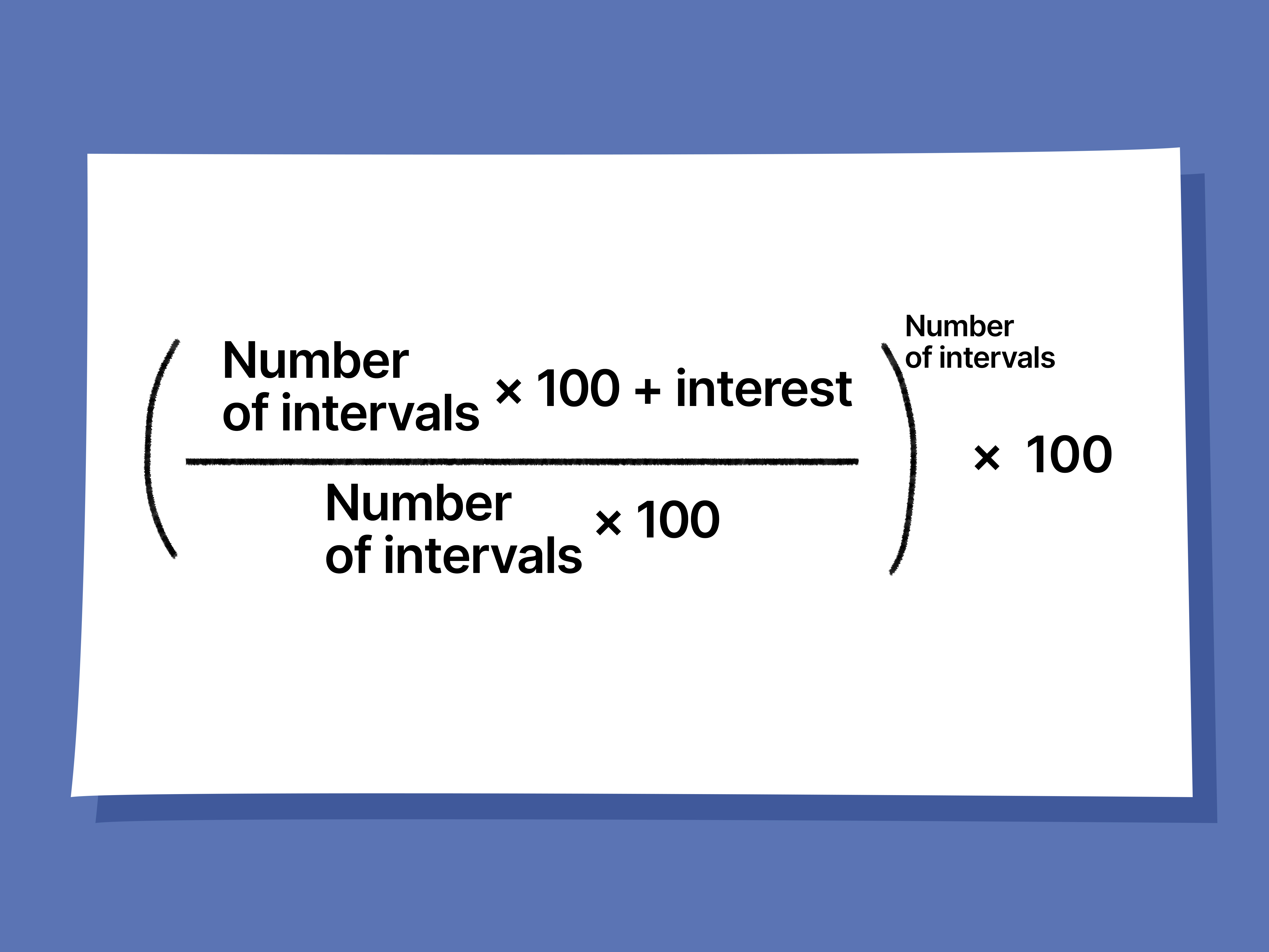

Annual Percentage Yield (APY): Maximizing Your Savings Returns

While APR is for borrowers, APY is for savers. The Annual Percentage Yield reflects the real rate of return on an investment or savings account, taking into account the effect of compound interest. Because APY accounts for compounding, it is always higher than the nominal interest rate (unless interest is compounded only once per year).

For example, a certificate of deposit (CD) with a 5% interest rate compounded monthly will have an APY of approximately 5.11%. When shopping for a high-yield savings account, the APY is the most important number to compare, as it tells you exactly how much your deposit will grow over one year.

How to Compare Offers Using These Metrics

To make the best financial choice, you must compare “apples to apples.” When borrowing, always compare the APR rather than the base interest rate to ensure you aren’t being blindsided by hidden fees. When saving, always look at the APY to see the impact of compounding. Understanding these metrics prevents the common pitfall of choosing a product that looks cheap or profitable on the surface but hides its true nature in the fine print.

Factors That Influence Your Personal Interest Rate

Not everyone is offered the same interest rate. When a bank calculates the rate to offer you, they are essentially performing a risk assessment. Several macro and micro-economic factors dictate the final number you see on a loan application.

Credit Scores and Risk Assessment

Your credit score is perhaps the most significant factor within your control. Lenders use your credit history to determine the likelihood that you will repay a loan. A high credit score (typically 740 and above) signals lower risk, allowing the lender to offer a lower interest rate. Conversely, a lower score suggests higher risk, which the lender offsets by charging a higher interest rate. Over the life of a 30-year mortgage, the difference between a “good” and “excellent” credit score can equate to tens of thousands of dollars in interest savings.

The Role of Central Banks and the Federal Funds Rate

On a broader scale, interest rates are influenced by the monetary policy of central banks, such as the Federal Reserve in the United States. When the “Fed” raises the federal funds rate, it becomes more expensive for banks to borrow money from each other. To maintain their profit margins, banks pass these costs on to consumers by raising interest rates on mortgages, credit cards, and business loans. This is often done to combat inflation. When the economy is sluggish, central banks may lower rates to encourage borrowing and spending.

Loan Term and Inflation Expectations

The duration of a loan also affects the interest rate calculation. Generally, long-term loans (like a 30-year mortgage) carry higher interest rates than short-term loans (like a 15-year mortgage). This is because there is more “uncertainty” over a longer period. Lenders must account for the risk that inflation will rise, eroding the value of the money they are paid back in the future. If inflation is expected to be high, lenders will increase interest rates to ensure their real return remains positive.

Calculating Interest in Real-World Scenarios

To see how these formulas translate into your daily life, it is helpful to look at how different financial products handle the math behind the scenes.

Mortgage Amortization: How Your Monthly Payment is Split

A mortgage is a unique type of installment loan where the interest is calculated monthly based on the remaining principal balance. This process is called amortization. In the early years of a 30-year mortgage, a vast majority of your monthly payment goes toward interest, while only a small fraction reduces the principal. As the principal balance decreases over time, the interest portion of your payment also decreases, and more of your money goes toward building equity. This is why making extra principal payments early in a mortgage can significantly reduce the total interest paid over the life of the loan.

Credit Card Interest: The Daily Balance Method

Credit cards are notoriously expensive because they typically use the “Average Daily Balance” method for interest calculation. The credit card company tracks your balance every single day of the billing cycle. At the end of the month, they average those daily balances and multiply that average by a daily periodic rate (which is your APR divided by 365).

Because interest is calculated based on your balance throughout the month, carrying a high balance for even a few days can increase your interest charges. This is also why “grace periods” are so valuable—if you pay your statement in full every month, the interest calculation is waived entirely.

Personal Loans and Fixed-Rate Installments

Most personal loans use a fixed-rate structure, where the interest is calculated upfront or based on a pre-determined schedule. Unlike credit cards, where the interest can fluctuate based on your spending habits, personal loans provide a predictable monthly payment. This makes them a popular choice for debt consolidation, as the borrower can often secure a lower interest rate than that of a credit card and have a clear “end date” for their debt.

Strategies to Minimize Interest Paid and Maximize Interest Earned

Mastering the calculation of interest allows you to flip the script and make the math work in your favor. Whether you are attacking debt or building a portfolio, strategy is key.

Debt Avalanche vs. Debt Snowball

When managing multiple debts, two popular strategies emerge: the Debt Snowball and the Debt Avalanche. The Debt Avalanche method focuses strictly on the math—you pay off the debt with the highest interest rate first. By eliminating the most “expensive” debt first, you minimize the total interest paid over time. The Debt Snowball focuses on psychological wins by paying off the smallest balances first. From a purely financial calculation standpoint, the Avalanche method is superior for saving money on interest.

Leveraging High-Yield Savings Accounts (HYSA) and CDs

To maximize interest earned, you should look beyond traditional “big bank” savings accounts, which often offer negligible interest rates (sometimes as low as 0.01%). High-Yield Savings Accounts (HYSAs), often offered by online banks, provide significantly higher APYs. Additionally, if you have money you don’t need immediate access to, Certificates of Deposit (CDs) allow you to “lock in” a high interest rate for a set period, protecting you from rate drops if the market changes.

Refinancing: When Does the Math Make Sense?

Refinancing is the process of replacing an existing loan with a new one that has better terms—usually a lower interest rate. To determine if refinancing makes sense, you must calculate the “break-even point.” This is the point at which the interest savings from the new loan outweigh the closing costs and fees of the refinance. For example, if a mortgage refinance costs $4,000 but saves you $200 a month in interest, your break-even point is 20 months. If you plan to stay in the home longer than 20 months, the calculation favors refinancing.

By understanding how interest rates are calculated, you move from being a passive participant in the economy to an active strategist. Whether you are navigating the complexities of a mortgage, managing credit card balances, or seeking the best return on your savings, the ability to calculate and compare interest is the ultimate tool for long-term financial success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.