Deciding to close a credit card, especially one from a major issuer like Chase, is a financial decision that warrants careful consideration. While it might seem like a straightforward step to simplify your finances or eliminate an unused account, there are several nuances and potential implications for your credit health that you must understand. This comprehensive guide will walk you through the process of closing a Chase credit card, highlighting crucial steps to take before, during, and after the closure, and helping you navigate the potential impact on your personal finances and credit score.

Whether you’re looking to reduce your overall debt, consolidate your credit lines, avoid annual fees, or simply streamline your financial portfolio, approaching the closure of a Chase credit card strategically is key to a smooth transition and maintaining your financial well-being.

Before You Close: Essential Pre-Closure Checklist

Before you pick up the phone to contact Chase, there are several critical steps you must undertake to ensure a smooth closure process and minimize any negative repercussions. Rushing this stage can lead to lost rewards, unexpected fees, or even a hit to your credit score.

Pay Down Your Balance to Zero

This is perhaps the most crucial step. You cannot effectively close a credit card with an outstanding balance. Ensure that your account balance is completely paid off, including any pending charges or interest accruals, before initiating the closure request. It’s often advisable to make your final payment a few days in advance to allow time for the payment to clear and post to your account. Attempting to close a card with a balance will likely result in Chase requiring you to pay it first, prolonging the process. Furthermore, leaving a small balance could lead to interest charges and even collection efforts if forgotten, severely impacting your credit.

Redeem Rewards and Benefits

One of the most common oversights when closing a credit card is forgetting to redeem accumulated rewards. If your Chase card earns Ultimate Rewards points, cashback, airline miles, or any other type of benefit, ensure you redeem them all before closing the account. Once the account is closed, any unredeemed rewards associated with that specific card will generally be forfeited. This can represent a significant loss, especially if you’ve been accumulating points for a large redemption like travel or high-value gift cards. Check your Chase online account or recent statements to determine your current rewards balance and understand the various redemption options available to you.

Transfer Automatic Payments and Subscriptions

In today’s digital age, many people have various subscriptions, utility bills, or recurring payments set up to automatically charge their credit card. Before closing your Chase card, take the time to identify all such automatic payments linked to that account. Update your payment information with each service provider to ensure they are redirected to another active card or bank account. Failing to do so can lead to missed payments, late fees, service interruptions, or even a negative mark on your credit report if a vital payment goes unpaid. Go through your past statements over the last 12-18 months to catch any less frequent recurring charges.

Consider Your Credit Score Impact

Closing a credit card can have an impact on your credit score, both positive and potentially negative. It’s essential to understand these implications beforehand. Your credit score is influenced by several factors, including your credit utilization ratio (how much credit you’re using versus how much is available), the length of your credit history, and your mix of credit accounts. Closing an old, unused card with a high credit limit could increase your credit utilization ratio on your remaining cards, which might negatively affect your score. Similarly, closing your oldest credit account could shorten your average credit history, another factor in your score. We’ll delve deeper into this aspect later, but it’s crucial to acknowledge these possibilities as part of your pre-closure evaluation.

Review Any Annual Fees or Outstanding Charges

Before proceeding, confirm if your Chase card carries an annual fee. If it does, timing your closure just after the fee posts (and you’ve decided not to keep the card) might allow you to get a prorated refund if you call within a certain window, though this varies by issuer and specific card terms. Be aware of any other outstanding charges, such as foreign transaction fees from recent travel or interest charges that might appear after your final payment. Ensure all these are cleared to truly bring your balance to zero.

The Step-by-Step Process to Close Your Chase Credit Card

Once you’ve completed your pre-closure checklist, you’re ready to formally request the closure of your Chase credit card. The process is generally straightforward, but knowing what to expect can make it even smoother.

Gather Necessary Information

Before contacting Chase, have your account number readily available. You might also need your Social Security number or other identifying information to verify your identity. Having this information at hand will speed up the process and demonstrate that you are prepared.

Choose Your Contact Method

While some banks offer online options, the most effective and recommended way to close a Chase credit card is by phone.

- Phone Call (Recommended): This allows for direct communication, immediate confirmation, and the opportunity to ask questions or address any issues in real-time. You can typically find the customer service number on the back of your card, on your monthly statement, or on the official Chase website. When you call, state clearly that you wish to close your credit card account.

- Secure Message (Less Common): Some banking portals allow you to send a secure message. While this can work, it might take longer to get a response and confirmation, and it lacks the immediate interaction of a phone call.

- Written Letter (Least Common): Sending a letter via certified mail can serve as official documentation, but it’s the slowest method and generally unnecessary unless you have specific legal reasons to prefer it.

For speed, clarity, and the ability to handle potential retention offers, a phone call is almost always the best choice.

What to Say During the Call

When you speak to a Chase representative, be clear and direct. Simply state, “I would like to close my credit card account ending in [last four digits of your card number].” The representative will likely ask for your reason for closing the account. You don’t need to elaborate extensively; a simple “I’m consolidating my finances,” “I no longer need this card,” or “I’m trying to reduce the number of credit cards I have” will suffice. Confirm that your balance is zero and that you have redeemed all your rewards. Crucially, ask for a confirmation number for the account closure. This number is your proof that the request was made and processed.

Dealing with Retention Offers

Be prepared for the possibility that the Chase representative might offer you incentives to keep your account open. These “retention offers” could include waived annual fees for a year, bonus points for meeting certain spending thresholds, or a lower interest rate. Chase values its customers, and it’s often more cost-effective for them to retain you than to acquire a new customer. Listen to their offers and genuinely consider if any of them make sense for your financial situation. If you were only closing the card due to an annual fee, for example, a fee waiver might be a compelling reason to stay. However, if your decision is firm, politely decline and reiterate your request to close the account.

Confirming Closure

The process doesn’t end with the phone call. It’s vital to confirm that the account has indeed been closed.

- Check Your Online Account: Within a few days, your Chase online banking portal should reflect the account as closed or show it no longer active.

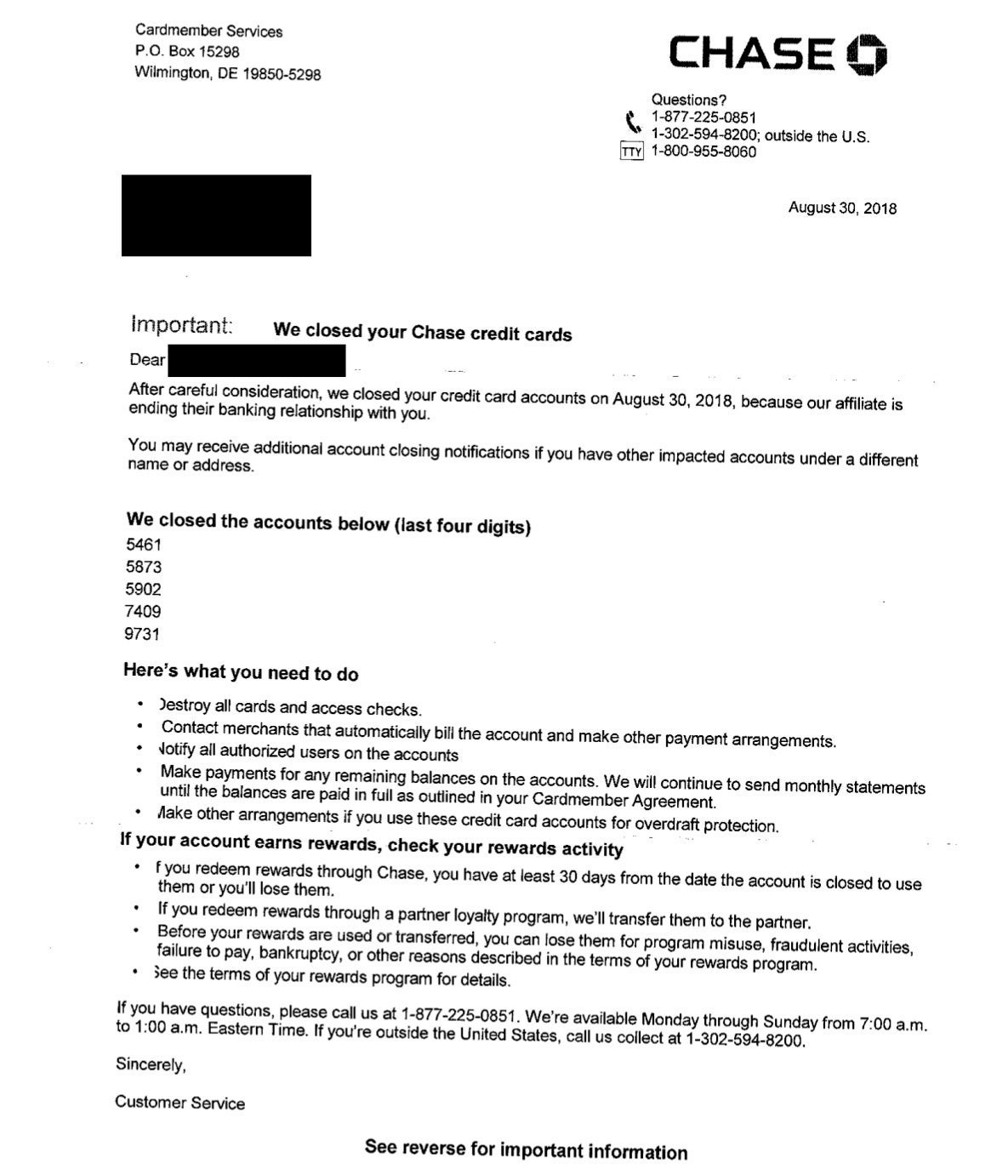

- Look for Official Correspondence: Chase should send you a written confirmation (either via email or postal mail) stating that the account has been closed. Keep this record for your files.

- Review Your Credit Report: Approximately 30-60 days after closure, check your credit report from all three major bureaus (Experian, Equifax, TransUnion) to ensure the account is reported as “closed by grantor” or “closed by consumer” with a zero balance. This confirms that the closure has been accurately reflected in your credit history. You can obtain free copies of your credit report annually from AnnualCreditReport.com.

Understanding the Credit Score Implications

As mentioned earlier, closing a credit card can influence your credit score. It’s not always negative, but it’s essential to understand how various factors might be affected.

Credit Utilization Ratio (CUR)

Your credit utilization ratio is the amount of credit you’re using compared to the total amount of credit available to you across all your accounts. A lower CUR (ideally below 30%) is generally better for your credit score. When you close a credit card, you eliminate that card’s credit limit from your total available credit. If you have balances on other cards, this reduction in available credit could cause your CUR to increase, which could negatively impact your score. For example, if you have $1,000 in debt and $10,000 in available credit (10% CUR), closing a card with a $5,000 limit would leave you with $1,000 in debt and $5,000 in available credit (20% CUR). While still good in this example, a higher balance could push you over the 30% threshold.

Length of Credit History

The age of your credit accounts is another significant factor. Lenders generally prefer to see a longer credit history, as it demonstrates your ability to manage credit responsibly over time. When you close an older account, it doesn’t immediately disappear from your credit report. It will typically remain on your report for up to 7-10 years, continuing to contribute to your average age of accounts during that period. However, once it eventually drops off, it can shorten your average credit history, potentially leading to a slight dip in your score, especially if it was one of your oldest accounts. If the card you’re closing is one of your newest, the impact on your average age of accounts will be minimal.

Mix of Credit

While not as heavily weighted as utilization or payment history, having a healthy mix of different types of credit (e.g., credit cards, installment loans like mortgages or car loans) can positively influence your score. Closing one credit card typically won’t have a major impact on this factor unless it’s your only remaining credit card or a significant portion of your revolving credit.

Strategies to Mitigate Negative Impact

To minimize potential negative impacts, consider these strategies:

- Keep Other Cards Open: If you have other credit cards, keep them active and maintain low balances. This ensures you still have available credit to support a healthy CUR.

- Product Change/Downgrade (see below): If the primary reason for closing is an annual fee, explore product changing the card to a no-annual-fee version instead of outright closing it. This preserves your credit history and credit limit.

- Monitor Your Credit: Regularly check your credit score and report after closing an account to ensure everything is accurately reflected and to spot any unexpected changes.

Alternatives to Closing Your Chase Credit Card

Before making the final decision to close your Chase credit card, consider if there are alternatives that might achieve your goals without potentially impacting your credit score.

Product Change/Downgrade

One of the most effective strategies to avoid the potential negative credit score impacts of closing an account is to request a “product change” or “downgrade.” Many credit card issuers, including Chase, allow you to switch your existing card to another product within their portfolio. For instance, if you have a Chase Sapphire Reserve with a high annual fee but no longer travel extensively, you might be able to downgrade it to a no-annual-fee Chase Freedom Flex or Chase Freedom Unlimited.

The significant advantage of a product change is that your account number typically remains the same, preserving your credit history (length of account) and your credit limit. This means there’s no immediate impact on your average age of accounts or your credit utilization ratio. You also usually get to keep any unredeemed rewards, though it’s always wise to confirm this with Chase beforehand. This is an excellent option if your primary reason for closing is to avoid an annual fee or if the card’s benefits no longer align with your spending habits.

Use it Sparingly (and responsibly)

If the card has no annual fee and you’re simply not using it often, another alternative is to keep it open but use it for a very small, recurring purchase (like a streaming service or a small online subscription) and then immediately pay it off. This keeps the account active and contributing positively to your credit history and utilization, without accumulating debt. Just be sure to set up autopay for the full statement balance to avoid any missed payments. This strategy helps maintain a higher overall credit limit, thus potentially keeping your credit utilization lower on your other cards.

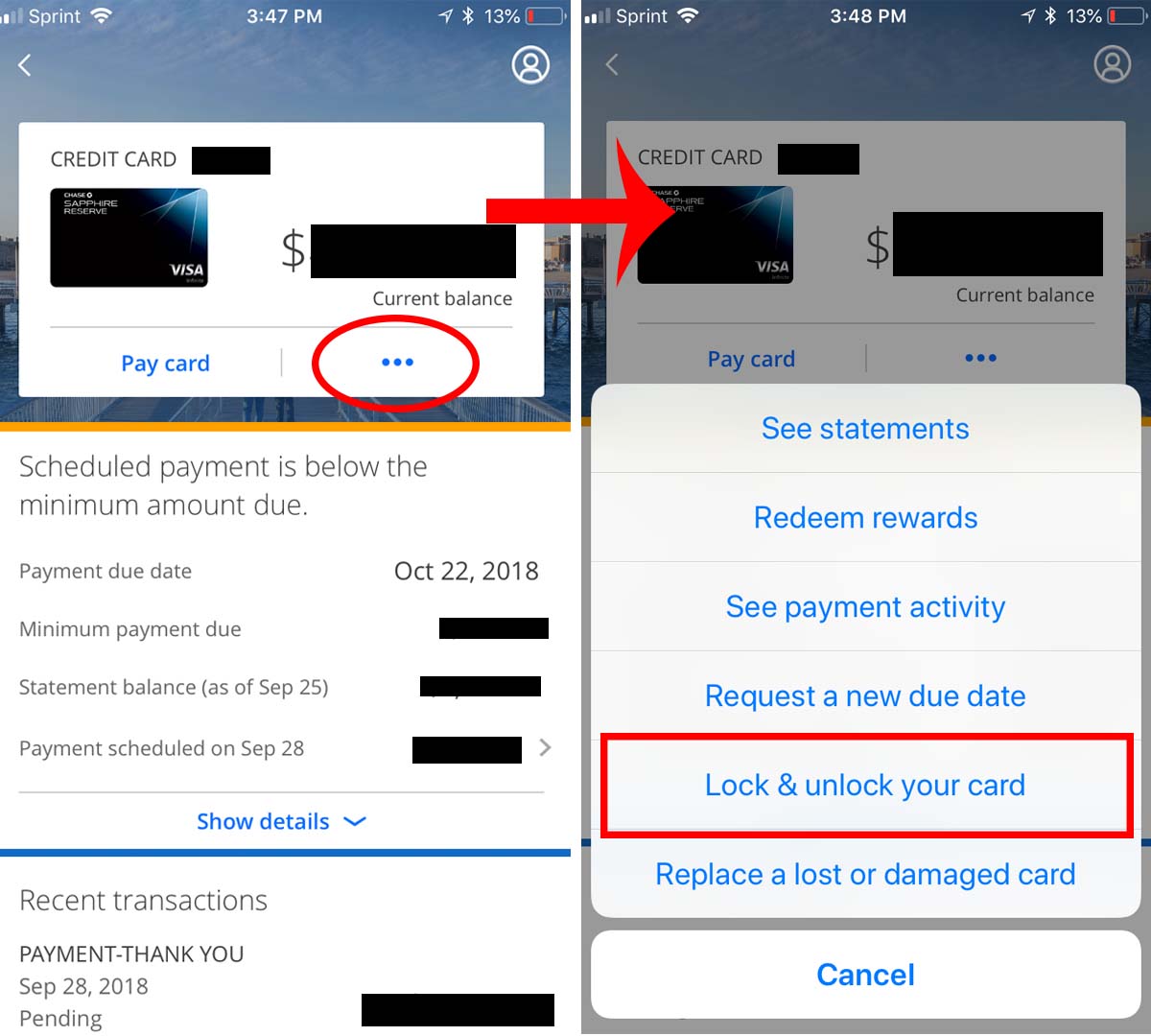

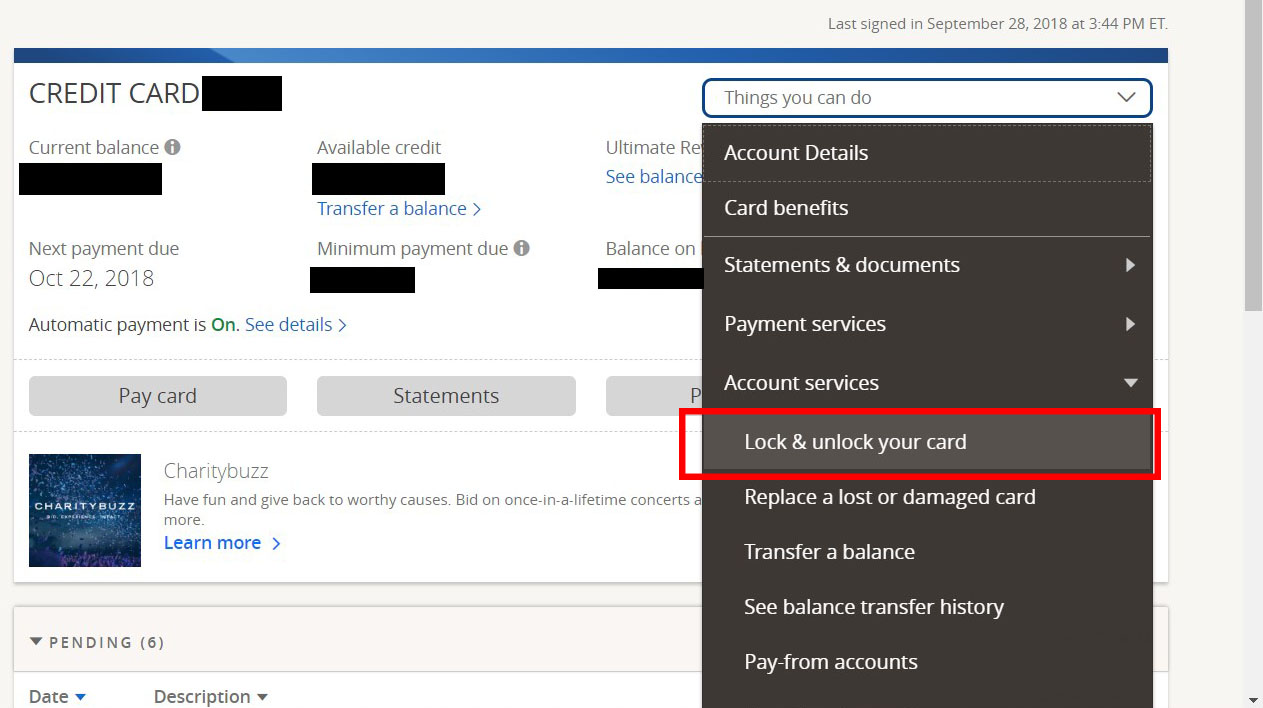

Freezing the Card

If your concern is more about security or preventing impulse spending, consider “freezing” the card instead of closing it. Many banks, including Chase, offer the ability to temporarily freeze your credit card through their mobile app or online portal. This prevents new purchases or cash advances, giving you control without permanently closing the account. You can then unfreeze it if and when you decide to use it again. This is a good temporary solution for managing an inactive card without impacting your credit factors.

Conclusion

Closing a credit card, especially one from a major issuer like Chase, is a financial decision that demands careful thought and strategic execution. While it can be a valuable step towards simplifying your financial life or avoiding unnecessary fees, it’s crucial to understand the implications for your credit score and to take all necessary preparatory steps.

By diligently paying down your balance, redeeming rewards, transferring automatic payments, and understanding how your credit score might be affected, you can ensure a smooth transition. Remember to confirm the closure with Chase and monitor your credit report for accurate reporting. Should you find yourself hesitant to close an account, exploring alternatives like a product change can offer a middle ground, allowing you to adapt your financial tools without compromising your hard-earned credit history. Ultimately, an informed approach ensures that closing a Chase credit card aligns with your broader financial goals and supports your long-term financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.