Applying for a new credit card can be a significant step in managing your personal finances, offering benefits like rewards, cash back, and improved purchasing power. For many, Chase credit cards are a top choice, known for their competitive offerings and robust rewards programs. However, once the application is submitted, a common question arises: “What happens next?” The waiting period can be filled with anticipation, and knowing how to check your Chase credit card application status efficiently and effectively is crucial for peace of mind and informed financial planning.

This article delves into the various methods available to monitor your application, deciphers the potential outcomes, and provides strategic insights into what steps you might take, whether you’re approved, pending, or denied. Understanding this process empowers you to navigate the world of credit with greater confidence and control, aligning perfectly with sound personal finance management.

Why Monitoring Your Application Status is Essential for Financial Prudence

In the realm of personal finance, proactive management is always preferable to reactive damage control. Tracking your credit card application isn’t merely about curiosity; it’s a fundamental aspect of responsible financial stewardship. Each step of the process holds implications for your credit profile and future financial decisions.

Peace of Mind and Proactive Planning

Submitting a credit card application involves sharing sensitive personal and financial information. The period between application and decision can be nerve-wracking, especially if you’re planning a significant purchase or simply eager to begin earning rewards. Knowing where your application stands alleviates this stress. An approved status allows you to anticipate the arrival of your new card and integrate it into your spending strategy. If the status is pending, it prompts you to consider potential next steps, such as providing additional information. This proactive approach ensures you’re never left in the dark, enabling you to plan your financial moves with greater certainty.

Identifying Potential Issues and Rectification

Sometimes, an application might get stuck or face an unexpected delay. These issues could range from a simple technical glitch to a need for further verification of your identity or financial details. By actively checking your application status, you can quickly identify if it’s lingering in a “pending” state for an unusually long time. This early detection empowers you to reach out to Chase directly to understand the cause and provide any necessary information or clarification, potentially expediting the decision-making process. Without monitoring, these delays could go unnoticed, prolonging your wait and potentially impacting other financial plans.

Timely Decision-Making for Future Applications

A key aspect of responsible credit management involves understanding the impact of multiple credit inquiries. When you apply for a credit card, a “hard inquiry” is typically placed on your credit report, which can temporarily lower your credit score. If your application with Chase is denied, knowing this outcome promptly allows you to adjust your strategy. You might decide to wait a few months to improve your credit score, address specific financial concerns, or apply for a different card better suited to your current credit profile. Conversely, if approved, you can avoid unnecessary applications that would lead to additional hard inquiries and potentially further dips in your score. This judicious approach to credit applications is a hallmark of intelligent personal finance.

The Primary Methods for Checking Your Chase Credit Card Application Status

Chase, a leader in financial services, provides several convenient channels for applicants to check the status of their credit card application. Each method caters to different preferences and situations, ensuring accessibility for all customers.

Online Portal: The Digital Gateway

For most applicants, the quickest and most efficient way to check a Chase credit card application status is through their dedicated online portal. This digital service is available 24/7, offering instant updates from the comfort of your home or on the go.

Step-by-Step Guide for Online Check

- Navigate to the Official Chase Website: Open your web browser and go to the official Chase website (chase.com).

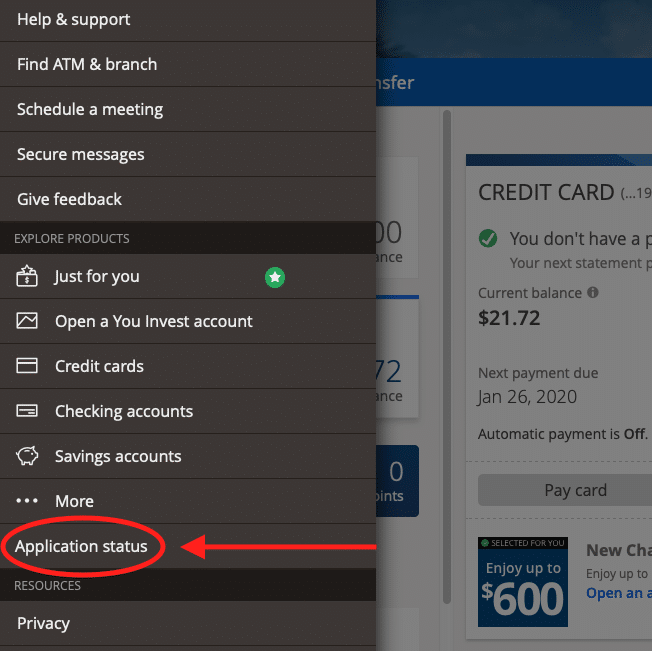

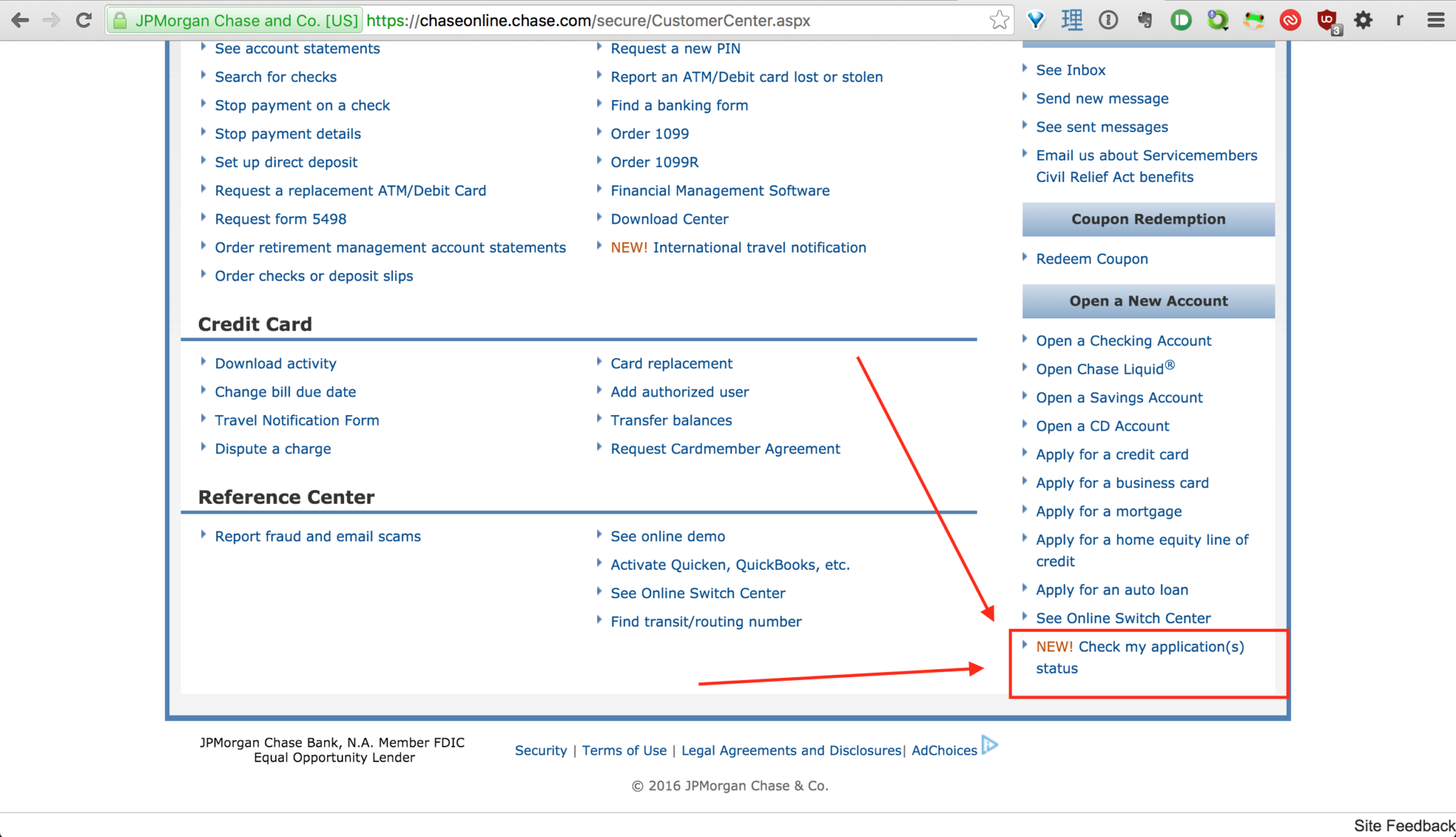

- Locate the Application Status Page: Look for a section related to “Credit Cards” or “Application Status.” Often, there’s a direct link on the main credit card page or within the customer service section. A common direct URL for Chase’s application status checker is chase.com/appstatus.

- Enter Required Information: You will typically need to provide a combination of your application ID (if you received one), your Social Security Number (SSN), and your Zip Code. Ensure this information matches exactly what you submitted on your initial application.

- Review Your Status: Once you submit the required details, the system will display your current application status. This could be “Approved,” “Pending,” or “Denied.”

- Print or Save for Records: It’s always a good idea to take a screenshot or print the status page for your personal records, especially if the decision is still pending or requires further action.

Required Information for Online Access

To successfully use the online portal, you will need:

- Your Social Security Number (SSN): This is the primary identifier.

- Your Zip Code: The one associated with your application.

- Optional: Application ID: While not always strictly necessary if you have your SSN and Zip Code, having your application ID can sometimes speed up the process.

Phone Support: Direct Communication

While the online portal is convenient, sometimes a more personal touch or specific clarification is needed. In such cases, Chase’s phone support is an invaluable resource.

When to Call and What to Expect

You might choose to call Chase if:

- You don’t have internet access or prefer speaking to a human.

- Your online status shows “pending” for an extended period (typically more than 7-10 business days).

- You need to provide additional information that was requested after your initial application.

- You want to understand the reasons behind a denial or discuss a reconsideration (more on this later).

When you call, you’ll typically speak to an automated system first, which may prompt you for your SSN to look up your application. You’ll then have the option to speak with a credit card specialist. Be prepared for potential wait times, especially during peak hours.

Information Needed for Phone Inquiry

When contacting Chase by phone, have the following readily available:

- Your Social Security Number (SSN).

- Your full name and address as provided on the application.

- The specific credit card product you applied for (e.g., Chase Sapphire Preferred, Chase Freedom Unlimited).

- Application ID (if you have it).

Mail Correspondence: Traditional Updates

While less common for real-time status checks, Chase may still communicate decisions or requests for additional information via postal mail. This is often the case if a decision takes longer than usual or if specific documentation is required. An approval or denial letter, complete with terms and conditions or reasons for denial, will generally be sent by mail. While waiting for mail isn’t ideal for urgent updates, it serves as a formal record of Chase’s decision.

Decoding Application Outcomes and Next Steps

Once you check your application status, you’ll typically encounter one of three main outcomes: Approved, Pending, or Denied. Each status has distinct implications and calls for specific actions or considerations from a personal finance perspective.

Approved: Congratulations, What’s Next?

An “Approved” status is, of course, the desired outcome. It signifies that Chase has reviewed your financial profile and deemed you eligible for the credit card.

Understanding Your Welcome Kit

Within 7-10 business days of approval, you should receive a welcome kit in the mail. This kit typically includes:

- Your new credit card.

- The cardholder agreement: This legally binding document outlines your interest rate (APR), fees, payment due dates, and other important terms. Read it carefully.

- Information on how to activate your card and set up online account access.

- Details about your credit limit and any introductory offers.

Activating Your Card and Setting Up Account

As soon as you receive your card, follow the instructions to activate it. This usually involves a quick phone call to an automated service or activation through the Chase website/app. Immediately after activation, set up your online account. This allows you to:

- Monitor your spending and transactions.

- Pay your bills online.

- Access your statements.

- Set up alerts for unusual activity.

- Manage your rewards points.

Proactive account management from day one is crucial for leveraging the benefits of your new card while maintaining financial discipline.

Pending: Patience and Potential Action

A “Pending” status means Chase needs more time or additional information to make a final decision. This is a common interim step and not necessarily a cause for alarm.

Understanding “Pending” Status

Chase might put an application on pending for several reasons:

- Verification: They may need to verify your identity, income, or other details.

- High Volume: During peak application periods, processing times can extend.

- Borderline Credit Profile: Your credit score or financial history might be close to their approval criteria, requiring a manual review by an underwriter.

- Missing Information: Something might have been unclear or omitted from your application.

The Reconsideration Line: A Strategic Option

If your application remains pending for more than a week, or if you’re later denied and wish to appeal, the “reconsideration line” is a powerful tool. This is a specific phone number where you can speak directly with a credit analyst or underwriter. You can find Chase’s reconsideration line numbers easily with a quick online search (often 1-888-270-2127 for personal cards).

When calling the reconsideration line:

- Be polite and professional.

- Clearly state your case: Explain why you believe you’re a good candidate for the card. Highlight positive aspects of your financial situation (e.g., stable income, low debt, existing relationship with Chase, strong payment history).

- Address any potential concerns: If you know of a recent hard inquiry or a slightly lower credit score, briefly explain mitigating factors.

- Be prepared to answer questions about your income, debts, and financial history.

This call can often sway a pending application to approval or, in the case of a denial, lead to a reversal of the decision.

What Information Might Chase Need?

During a pending status, Chase might request:

- Proof of income: Pay stubs, tax returns (W-2s), or bank statements.

- Proof of address: Utility bills or other official documents.

- Identity verification: A copy of your driver’s license or passport.

- Clarification on specific items on your credit report.

Respond to these requests promptly to avoid further delays or a potential denial due to lack of information.

Denied: Learning from the Decision

A denial can be disappointing, but it’s an opportunity for financial learning and improvement. Chase is legally required to provide you with a specific reason for denial (via a denial letter sent by mail within 30 days).

Reasons for Denial

Common reasons for credit card application denial include:

- Low credit score: Not meeting Chase’s minimum credit score requirements for the specific card.

- High debt-to-income ratio: Too much existing debt relative to your income.

- Too many recent credit inquiries or new accounts: This can signal risky behavior to lenders.

- Insufficient income: Not meeting the income threshold.

- Lack of credit history: For new credit users, sometimes called a “thin file.”

- Previous negative relationship with Chase: Defaulted on a prior loan or credit card.

The Value of the Reconsideration Line Post-Denial

Even after a denial, the reconsideration line is worth a call. Sometimes, an automated system might overlook nuances in your application. A human analyst might see your full financial picture differently. Prepare your case as described above, focusing on why the stated reason for denial might be mitigated or why your overall financial health makes you a good candidate despite the issue. Success here isn’t guaranteed, but it costs nothing but time to try.

Improving Your Chances for Future Applications

If a denial stands, use the information provided to improve your financial profile:

- Review your credit report: Get free copies from AnnualCreditReport.com. Dispute any inaccuracies.

- Pay down existing debt: Focus on high-interest debts first.

- Improve your credit score: Make all payments on time, keep credit utilization low (below 30%), and avoid new hard inquiries for a period.

- Build a stronger credit history: Consider a secured credit card or becoming an authorized user on someone else’s well-managed account.

- Reapply strategically: After 6-12 months of improvement, consider reapplying for the same card or a different one better suited to your current credit standing.

Strategic Considerations Before and After Applying

A responsible approach to credit cards extends beyond simply checking an application status; it encompasses careful planning before applying and diligent management after approval. These strategic considerations are cornerstones of sound personal finance.

Pre-Application Due Diligence: Maximizing Your Approval Odds

Before you even hit “submit” on a Chase credit card application, taking a few preparatory steps can significantly enhance your chances of approval and prevent unnecessary hard inquiries.

Credit Score Impact

Your credit score is arguably the most critical factor Chase considers. Each Chase card has different implicit credit score requirements (e.g., generally 700+ for premium cards).

- Check your score: Utilize free credit score services (e.g., from your bank, credit card company, or services like Credit Karma).

- Understand the score: Familiarize yourself with factors influencing your score (payment history, credit utilization, length of credit history, credit mix, new credit).

- Address deficiencies: If your score is low, dedicate time to improving it before applying.

Existing Relationship with Chase

If you already have a banking relationship with Chase (e.g., a checking or savings account), this can sometimes be a positive factor. Chase may view you as a more trusted customer. While not a guarantee, it can occasionally provide a slight edge, especially if your application is borderline.

Income and Debt-to-Income Ratio

Chase, like any lender, wants to ensure you can comfortably manage new debt.

- Stable Income: A consistent and sufficient income is crucial. Be accurate in your stated income on the application.

- Debt-to-Income (DTI) Ratio: This measures how much of your monthly income goes towards debt payments. A lower DTI (ideally below 36%) indicates you have more disposable income to handle new credit obligations, making you a less risky borrower.

Post-Decision Financial Hygiene

Whether approved or denied, the period following a credit card application decision presents opportunities for reinforcing good financial habits.

Managing Your New Card Responsibly

For those approved, the work has just begun. Responsible credit card management is paramount:

- Pay in Full, On Time: This is the golden rule. Paying your balance in full each month avoids interest charges and builds excellent payment history. If you can’t pay in full, always pay at least the minimum on time.

- Keep Credit Utilization Low: Aim to keep your spending below 30% (ideally 10% or less) of your credit limit. High utilization can negatively impact your credit score.

- Monitor Your Account: Regularly check your statements for errors or fraudulent activity.

- Understand Rewards Programs: Maximize your benefits by understanding how to earn and redeem rewards effectively.

Strategies for Rebuilding Credit After Denial

A denial isn’t the end of the road; it’s a redirection.

- Review the Denial Letter: Understand the exact reasons and focus your efforts on those specific areas.

- Obtain Your Credit Report: Scrutinize your report for any errors that could be disputing.

- Focus on Fundamentals: Pay all bills on time, reduce existing debt, and avoid opening new credit accounts for a period to allow your credit profile to stabilize and improve.

- Consider Alternatives: Explore secured credit cards or credit-builder loans, which are designed to help individuals establish or rebuild credit responsibly.

Frequently Asked Questions and Expert Tips

Navigating credit card applications and status checks often brings up common queries. Addressing these, along with some expert advice, can further empower your financial journey.

How Long Does It Usually Take?

Most Chase credit card application decisions are made instantly online. However, if your application requires further review, it can take anywhere from 7 to 10 business days, sometimes extending up to 30 days in complex cases. If you haven’t heard back after 10 business days, it’s a good time to use the online status checker or call the reconsideration line.

Can I Expedite the Process?

Generally, you cannot “expedite” an application decision directly. The best way to encourage a quicker resolution for a pending application is to promptly provide any requested information. If you’re approved and need the card quickly, you can sometimes request expedited shipping, though this is usually for the physical card itself, not the approval decision. Call Chase customer service after approval to inquire about expedited shipping.

What if I Applied for Multiple Cards?

Applying for multiple cards in a short period (known as “credit seeking” or “velocity”) can be a red flag for lenders and may lead to denials. Chase has its own internal rules, famously the “5/24 rule,” which generally means they won’t approve you for most of their credit cards if you’ve opened five or more personal credit cards from any issuer in the last 24 months. If you’ve applied for multiple cards, understand that this could be a reason for denial or a pending status requiring further review. It’s often best to space out credit card applications significantly.

Expert Tips for Credit Card Management

- Don’t Apply Blindly: Research cards thoroughly to ensure they align with your spending habits and financial goals. Chase offers a diverse portfolio; pick one that truly benefits you.

- Understand the “Why”: Why are you getting this card? For rewards? Building credit? Emergency fund? Having a clear purpose helps in responsible usage.

- Regularly Review Your Credit Report: It’s your financial fingerprint. Check it for accuracy and to track your progress.

- Set Up Alerts: Enable spending alerts, payment reminders, and credit score change notifications from Chase or other financial apps.

- Utilize Financial Tools: Leverage budgeting apps, credit score trackers, and other personal finance tools to stay on top of your financial health.

By understanding how to effectively check your Chase credit card application status and what actions to take based on the outcome, you position yourself to make informed financial decisions. This proactive approach not only streamlines the application process but also fosters a stronger foundation for long-term credit health and overall personal financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.