In the intricate world of finance, where every digit can represent significant value, precision and understanding are paramount. While the question “what is 1 1/3 as a decimal?” might appear to be a simple arithmetic exercise, its implications for personal finance, investing, and business finance are surprisingly profound. This seemingly basic conversion underpins a multitude of financial concepts, from calculating interest rates and understanding growth percentages to analyzing investment returns and managing budgets. Mastering the ability to fluidly navigate between fractions and decimals is not just a mathematical skill; it is a foundational pillar of financial literacy that empowers individuals and businesses to make more informed, strategic decisions.

The answer to the initial question is straightforward: 1 1/3 as a decimal is 1.333… (or 1.33 if rounded to two decimal places). This recurring decimal represents one whole unit and one-third of another. While the numerical conversion itself is quick, the true value lies in exploring why this understanding is critical within the money landscape. This article will delve into how such conversions illuminate various financial scenarios, empowering you to better comprehend and manage your financial health.

The Foundation of Financial Literacy: Understanding Fractions and Decimals

At its core, financial literacy hinges on a strong grasp of numerical concepts, and the ability to work with fractions and decimals interchangeably is non-negotiable. These two formats are simply different ways of expressing parts of a whole, but their applications and interpretations in finance can vary significantly.

Bridging the Gap: Why Conversions Matter in Finance

Imagine trying to compare an investment opportunity that promises a “one-third share” of profits with another offering a “30% return.” Without the ability to convert 1/3 into a decimal (0.333…) or percentage (33.3%), direct comparison becomes cumbersome and prone to misinterpretation. Financial reports, investment prospectuses, and loan agreements often present information in a mix of fractions, decimals, and percentages. A savvy financial consumer or business leader must be able to convert between these forms effortlessly to accurately assess value, risk, and potential returns.

For instance, when dealing with stock splits, dividend yields, or ownership stakes, fractions might initially be used. However, for calculating exact monetary values, averaging performance, or comparing against benchmarks, decimals become the universal language. An investor might own 1/3 of a company’s shares, but when it comes time to calculate the total value of their holding, or their share of a dividend payout, converting that fraction into a decimal (0.333…) and multiplying by the total value is essential. This seamless conversion ensures precision and clarity, preventing errors that could lead to financial losses or missed opportunities.

The Core Concept: Deconstructing 1 1/3

Let’s break down the mechanics of 1 1/3 to 1.333… The mixed number 1 1/3 consists of a whole number (1) and a fraction (1/3).

To convert a mixed number to a decimal:

- Keep the whole number as it is (1).

- Convert the fraction to a decimal. To do this, divide the numerator by the denominator: 1 ÷ 3 = 0.333…

- Add the whole number to the decimal part: 1 + 0.333… = 1.333…

This simple conversion illustrates a fundamental principle: a fraction represents division. Understanding this relationship is key to deciphering various financial metrics. For example, a “debt-to-equity ratio of 1/3” instantly tells a financier that for every three units of equity, there is one unit of debt, or in decimal terms, 0.33 units of debt per unit of equity. This common language of decimals simplifies comparisons across different companies and industries.

Practical Applications of 1 1/3 (or 1.333…) in Personal Finance

Beyond academic exercises, the understanding of how to convert and apply fractions like 1 1/3 extends deeply into everyday personal finance, influencing budgeting, investing, and debt management.

Budgeting and Allocating Funds: Beyond Whole Numbers

When creating a budget, individuals often allocate portions of their income to various categories like housing, savings, and discretionary spending. While percentages (e.g., “30% for housing”) are common, sometimes allocations are thought of in fractional terms. For example, if someone decides to save “one-third” of every bonus check, knowing that 1/3 is approximately 0.33 or 33.3% allows them to accurately calculate the monetary amount to set aside. This precision is vital for effective financial planning, ensuring that savings goals are met and expenses are properly managed, even when income streams are irregular or come with fractional allocations.

Furthermore, budgeting tools and spreadsheet software predominantly work with decimals. If you’re manually calculating how much “1 1/3 times your current spending” would be in a hypothetical scenario, you’d immediately turn to 1.333… to get an accurate numerical result. This avoids errors and provides clear figures for decision-making.

Understanding Investment Returns and Growth Rates

In the world of investing, returns are frequently expressed as percentages, which are essentially decimals multiplied by 100. If an investment grows by “one-third” of its original value, that translates to a 33.3% growth rate. An investment that triples its value in three years is a growth factor of 3.0, but understanding factors like “1 1/3 times your initial investment” is equally crucial. This means your initial capital has grown by 33.3%.

For example, if you invested $10,000 and it grew by 1 1/3, its new value would be $10,000 * 1.333… = $13,333.33. This direct calculation, facilitated by the decimal conversion, allows investors to quickly project future values, assess past performance, and compare different investment vehicles accurately. It also forms the basis for understanding more complex metrics like compound annual growth rate (CAGR) or return on investment (ROI).

Debt Management and Interest Calculations

Debt, especially high-interest debt, can quickly spiral out of control if not properly understood. Interest rates are nearly always expressed as percentages, requiring decimal conversion for calculations. While a loan might not directly state an interest increase of “1 1/3 times the prime rate,” understanding fractional multipliers is crucial for mental flexibility.

More directly, consider a situation where a penalty fee is “1/3 of the monthly payment.” Knowing this translates to 0.333… times the payment allows for immediate calculation of the exact monetary penalty. This precision is vital for budgeting for debt repayment and avoiding unexpected costs. Even when calculating simple interest, knowing that an annual rate of 4% is 0.04 as a decimal for calculations is fundamental. The ease of conversion between fractional concepts and decimal calculations ultimately leads to better control over one’s financial obligations.

Business Finance: Leveraging Decimal Precision for Strategic Decisions

For businesses, the stakes are even higher. Every fraction and decimal carries weight, impacting profitability, valuation, and strategic direction. The ability to precisely work with these numbers is fundamental to sound financial management and competitive advantage.

Sales Growth and Market Share Analysis

When analyzing business performance, metrics like sales growth and market share are frequently discussed. A company might report that its sales increased by “1 1/3 times last quarter’s sales.” Converting this to 1.333… allows for immediate, quantifiable comparison and projection. If last quarter’s sales were $1 million, a 1 1/3 increase means current sales are $1 million * 1.333… = $1.333 million. This decimal conversion makes it straightforward to plot trends, set new targets, and allocate resources effectively.

Similarly, market share figures are often represented as percentages or decimals. If a company holds “one-third of the market,” understanding this as 33.3% or 0.333… allows for precise calculation of potential revenue based on total market size. Such calculations are critical for strategic planning, competitor analysis, and identifying growth opportunities.

Cost Analysis and Profit Margins

Cost management is a relentless pursuit for businesses. Decisions about pricing, production, and supply chains often rely on granular cost data. If the cost of a raw material increases by “1/3,” knowing that this translates to a 33.3% increase allows for immediate recalculation of production costs and adjustments to pricing strategies. A small fractional increase, if not accurately converted and accounted for, can significantly erode profit margins.

Profit margins themselves are often expressed as percentages (e.g., a “gross profit margin of 25%,” meaning 0.25 of every revenue dollar is gross profit). If a target profit margin is set as “at least 1/3,” this immediately translates to needing a 33.3% margin, guiding pricing and cost control efforts. The precision offered by decimals ensures that profit calculations are robust and reliable for both internal reporting and external financial statements.

Financial Ratios and Performance Metrics

Financial analysts and investors rely heavily on financial ratios to assess a company’s health, efficiency, and profitability. Ratios like debt-to-equity, current ratio, quick ratio, and return on assets are almost always presented as decimals. For instance, a debt-to-equity ratio of 0.5 indicates that a company has half as much debt as equity, while a ratio of 1.333… (which is 1 1/3) would suggest more debt relative to equity, potentially signaling higher risk.

Understanding the decimal representation of these ratios allows for direct comparison against industry benchmarks, historical performance, and competitors. It helps identify trends, pinpoint areas of strength or weakness, and ultimately inform investment decisions, lending approvals, and strategic management choices. The ability to quickly interpret these decimal figures, even if they originated from fractional ideas, is a cornerstone of financial acumen.

The Impact of Fractional Thinking on Long-Term Wealth Building

Developing a comfort level with fractions and decimals isn’t just about immediate calculations; it fosters a deeper, more nuanced understanding of how wealth accumulates over time, enabling superior long-term financial planning.

Compound Interest and the Power of Small Increments

Compound interest, often hailed as the “eighth wonder of the world,” relies heavily on the repeated multiplication of initial capital by growth factors, which are essentially 1 plus an interest rate expressed as a decimal. Even seemingly small annual percentage rates, when converted to their decimal equivalents and compounded over decades, can lead to substantial wealth accumulation. Understanding that a 5% annual return means multiplying your principal by 1.05 each year allows for clear projections of future value.

Similarly, an annual growth factor of “1 1/3” (meaning a 33.3% annual return) would indicate extremely rapid wealth growth. Visualizing and calculating this compounding effect requires decimal precision. Missing a fractional point in an interest rate or growth factor, even if small, can lead to vastly different outcomes over extended periods.

Diversification and Asset Allocation Strategies

Diversifying an investment portfolio involves allocating funds across various asset classes, industries, and geographies. These allocations are often expressed as percentages or fractions (e.g., “one-third in stocks, one-third in bonds, one-third in real estate”). Converting these to decimals (0.333…) ensures that the total allocation sums up to 1 (or 100%) and allows for precise monetary allocation.

For instance, if an investor has $150,000 and wants to follow a “1/3 rule,” they would allocate $150,000 * 0.333… = $50,000 to each category. This meticulous approach to asset allocation helps manage risk, optimize returns, and maintain a balanced portfolio aligned with long-term financial goals.

Making Informed Decisions in a Complex Financial World

The financial landscape is filled with complex products, services, and opportunities, many of which present information in varied numerical formats. From calculating loan payments with variable interest rates to understanding the expense ratios of mutual funds or the tax implications of capital gains, a solid grasp of fractions and their decimal equivalents empowers individuals to cut through jargon and make truly informed decisions. It allows for critical evaluation of financial products, comparison of different offers, and the ability to spot potential discrepancies or hidden costs. In essence, it provides the analytical toolkit necessary to navigate a world where financial success often hinges on numerical literacy.

Tools and Techniques for Mastering Financial Conversions

While the conceptual understanding is vital, practical application also benefits from efficient tools and techniques for performing these conversions.

Basic Calculation Methods

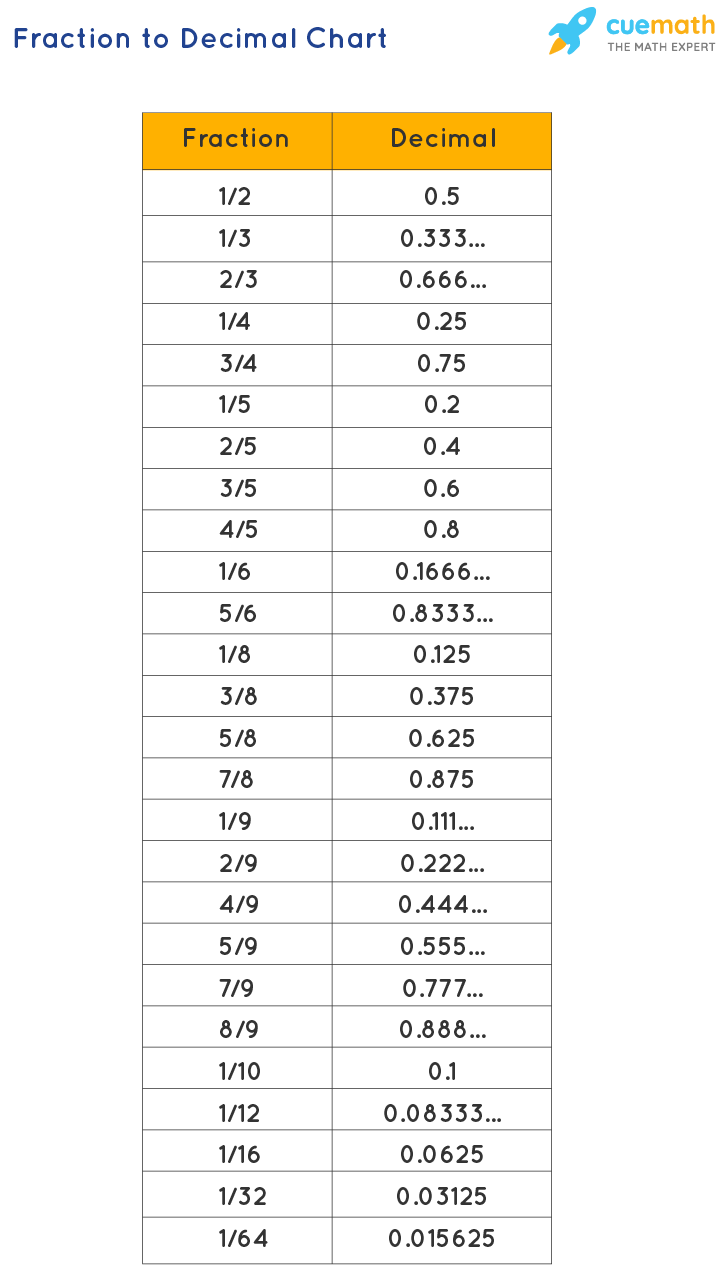

For simple conversions like 1 1/3, mental math or basic pen-and-paper division (1 ÷ 3) is sufficient. For mixed numbers, remember to convert the fractional part to a decimal and then add it to the whole number. Practice with common fractions (1/2, 1/4, 3/4, 1/5, 1/10, 1/3, 2/3) helps build intuition and speed, which are invaluable in fast-paced financial decision-making.

Leveraging Spreadsheets and Financial Calculators

For more complex calculations, especially those involving many figures or recurring decimals, spreadsheets (like Microsoft Excel or Google Sheets) and financial calculators are indispensable. Spreadsheets can instantly convert fractions to decimals using simple division formulas, allowing users to quickly integrate these values into larger financial models for budgeting, investment analysis, and forecasting. Financial calculators, designed for complex computations, similarly streamline the process, ensuring accuracy and saving time. Learning basic functions in these tools significantly enhances one’s financial analytical capabilities.

The Importance of Mental Math in Everyday Finance

While tools are powerful, the ability to perform quick mental conversions for common fractions and decimals (like knowing 1/3 is roughly 0.33) is a powerful asset. It allows for on-the-spot estimations, rapid assessment of deals, and quick checks on calculations. This mental agility is particularly useful when discussing finances verbally or when immediate “back-of-the-envelope” calculations are needed before diving into more detailed analysis. It reinforces a proactive and engaged approach to managing money, rather than passively relying solely on external tools.

In conclusion, the seemingly simple question “what is 1 1/3 as a decimal?” opens the door to a fundamental aspect of financial literacy. The answer, 1.333…, is not just a number, but a gateway to understanding critical financial concepts, from personal budgeting and investment returns to business growth analysis and strategic decision-making. By embracing the fluidity between fractions and decimals, individuals and businesses alike can unlock greater clarity, enhance their analytical capabilities, and ultimately build a more secure and prosperous financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.