For millions of Americans, Social Security isn’t just a government program; it’s a foundational pillar of their financial security, especially in retirement. Yet, despite its critical role, many individuals find themselves asking a seemingly simple question with a complex answer: “How much is my Social Security benefit?” The amount isn’t a fixed sum; it’s a personalized calculation influenced by a multitude of factors, from your earning history to the age you decide to claim. Understanding these variables is not merely an academic exercise; it’s essential for effective retirement planning, helping you project your future income and make informed decisions about your financial future.

This comprehensive guide aims to demystify the Social Security benefit calculation process. We will delve into the core mechanics of how your benefits are determined, explore the key factors that can significantly alter your monthly payout, touch upon the various types of benefits available, and offer actionable strategies to help you maximize this vital income stream. Whether you’re decades away from retirement or approaching your claiming age, gaining clarity on your Social Security benefits is a crucial step toward securing a comfortable and predictable financial future.

Understanding the Foundation: How Benefits Are Calculated

The journey to determining your Social Security benefit begins with a formula that considers your lifetime earnings. The Social Security Administration (SSA) doesn’t just look at your current income; it takes a holistic view of your contributions over your working life.

The Role of Your Earnings Record: Average Indexed Monthly Earnings (AIME)

The first critical component is your Average Indexed Monthly Earnings (AIME). Social Security benefits are based on your average earnings over your working career. However, these earnings are not simply averaged in their nominal value. To account for changes in general wage levels over time, the SSA “indexes” your past earnings. This process adjusts your earnings from earlier years to reflect the approximate wage levels of the year you turn 60. For example, earnings from 1980 will be adjusted upward to be comparable to earnings in the early 2000s, ensuring that your earliest contributions aren’t undervalued due to inflation and wage growth.

Specifically, the SSA identifies your 35 highest-earning years (after indexing) and then calculates the average monthly earnings from those years. If you have fewer than 35 years of work with earnings, the non-earning years will be counted as zero, which can significantly lower your AIME and, consequently, your benefit. This emphasizes the importance of a long and consistent work history.

Primary Insurance Amount (PIA): Your Baseline Benefit

Once your AIME is calculated, the next step is to determine your Primary Insurance Amount (PIA). Your PIA is the benefit you would receive if you start collecting Social Security benefits at your Full Retirement Age (FRA). The PIA is derived from your AIME using a progressive formula involving “bend points.”

Bend points are specific dollar amounts in the AIME formula that create segments, each with a different percentage multiplier. For instance, a certain percentage (e.g., 90%) of the first segment of your AIME is counted, a lower percentage (e.g., 32%) of the next segment, and an even lower percentage (e.g., 15%) of any AIME above that. This progressive structure means that lower earners receive a higher percentage return on their contributions compared to higher earners, although higher earners still receive a larger absolute benefit. The bend points themselves are updated annually to reflect changes in the national average wage index. Your PIA is the core figure from which all other benefit amounts (early, delayed, spousal, survivor) are derived.

Maximum Taxable Earnings: Impact on Contributions and Benefits

Each year, there’s a maximum amount of earnings subject to Social Security taxes. In 2024, for example, this limit is $168,600. This means that any earnings above this threshold are not subject to Social Security taxes, and they also don’t count towards your future Social Security benefits. While this might seem like a disadvantage for high earners, it’s a fundamental aspect of the system designed to balance contributions and benefits across different income levels. It also means there’s an upper limit to the maximum possible Social Security benefit, regardless of how high one’s income rises above the taxable maximum.

Key Factors Influencing Your Benefit Amount

While the AIME and PIA form the foundation, several critical factors can significantly alter the actual monthly benefit check you receive. Understanding these levers is crucial for strategic planning.

Your Earning History and Duration of Work

As mentioned, the SSA uses your 35 highest-earning years (after indexing) to calculate your AIME. This means:

- A longer work history is generally better: Working more than 35 years can replace lower-earning years from your past with higher-earning recent years, increasing your average.

- Higher earnings lead to higher benefits: Up to the maximum taxable earnings limit, earning more throughout your career directly translates to a higher AIME and thus a higher PIA. Missing years of work, or having periods of very low earnings, will result in zeros being averaged into your 35-year calculation, substantially reducing your overall benefit.

Your Age When You Claim Benefits

This is arguably the most impactful decision you’ll make regarding your Social Security benefit.

- Full Retirement Age (FRA): This is the age at which you are entitled to receive 100% of your PIA. FRA varies based on your birth year. For those born in 1960 or later, it is age 67.

- Claiming Early (as early as age 62): You can start receiving benefits as early as age 62, but doing so will permanently reduce your monthly benefit. The reduction is approximately 5/9 of 1% for each month before your FRA, up to 36 months, and 5/12 of 1% for each month beyond 36 months. For someone with an FRA of 67, claiming at age 62 results in a permanent 30% reduction in benefits.

- Delaying Benefits (up to age 70): If you delay claiming benefits past your FRA, you can earn Delayed Retirement Credits (DRCs). For each year you delay, your benefit increases by a certain percentage (currently 8% per year for those born 1943 or later) until age 70. This means that someone with an FRA of 67 who delays until age 70 could receive an additional 24% on top of their PIA. There is no additional benefit for delaying past age 70.

Cost-of-Living Adjustments (COLAs)

Social Security benefits are designed to maintain their purchasing power over time. To achieve this, the SSA implements Cost-of-Living Adjustments (COLAs). These annual adjustments are based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If the CPI-W increases, benefits are increased proportionally, typically announced in the fall and effective the following January. While not a factor in the initial calculation of your PIA, COLAs are crucial for ensuring your benefit keeps pace with inflation throughout your retirement.

Taxation of Benefits

While not affecting the amount of your benefit, it’s important to be aware that your Social Security benefits may be subject to federal income tax. Whether or not your benefits are taxed, and to what extent, depends on your “provisional income,” which includes your adjusted gross income, tax-exempt interest, and 50% of your Social Security benefits.

- Up to 50% of your benefits may be taxable if your provisional income is between $25,000 and $34,000 for an individual, or between $32,000 and $44,000 for a married couple filing jointly.

- Up to 85% of your benefits may be taxable if your provisional income is above $34,000 for an individual, or above $44,000 for a married couple filing jointly.

Some states also tax Social Security benefits, so it’s wise to check your state’s specific regulations.

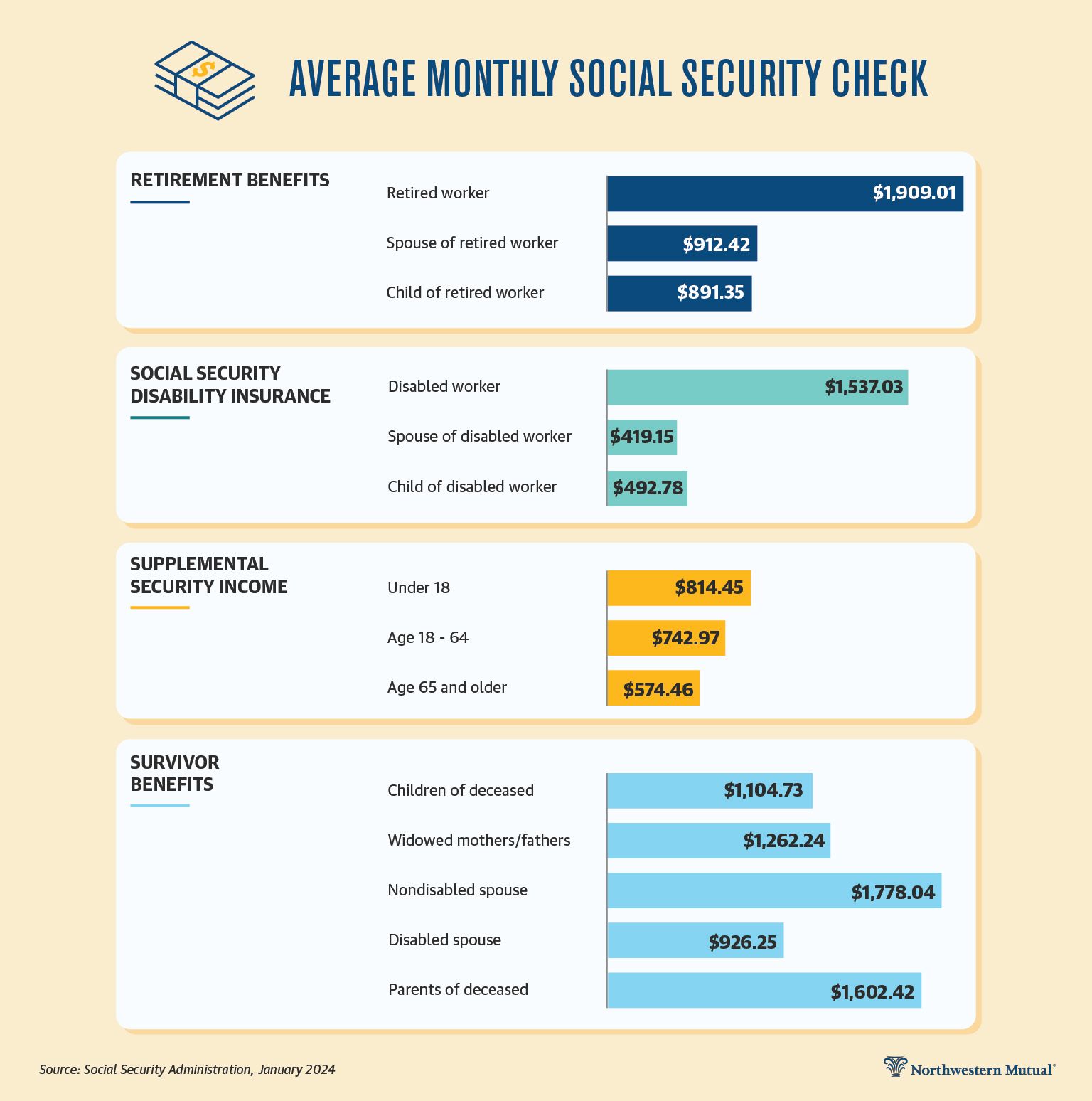

Types of Social Security Benefits Beyond Retirement

Social Security is more than just a retirement program. It provides a safety net for various life circumstances, offering benefits to family members of workers who have paid into the system.

Spousal Benefits

If you’re married, you might be eligible for spousal benefits based on your spouse’s work record. Generally, a spouse can receive up to 50% of the working spouse’s PIA. This is particularly beneficial if one spouse has a significantly lower (or no) work history. To claim spousal benefits, the working spouse must have already filed for their own benefits, and the claiming spouse must be at least 62 years old, or caring for a child under age 16 or disabled. If you are eligible for both your own benefits and spousal benefits, you will generally receive the higher of the two amounts.

Survivor Benefits

Social Security also provides crucial financial support to the family members of a deceased worker. These are known as survivor benefits. Eligible recipients can include:

- Widows and Widowers: A surviving spouse can receive up to 100% of the deceased worker’s benefit if they claim at their own FRA, or a reduced amount if claimed earlier. Benefits can start as early as age 60 (or age 50 if disabled).

- Children: Unmarried children under age 18 (or 19 if still in high school) can receive benefits. Disabled children can receive benefits at any age if their disability began before age 22.

- Dependent Parents: In some cases, dependent parents aged 62 or older may also be eligible.

Disability Benefits (SSDI)

If you become severely disabled and are unable to work, Social Security Disability Insurance (SSDI) can provide a vital income stream. To qualify, you must have worked long enough and recently enough to have earned sufficient “work credits.” The amount of your disability benefit is generally equivalent to your PIA, as if you had reached your FRA. The SSA’s definition of disability is strict: you must be unable to do substantial gainful activity due to a medical condition that is expected to last at least a year or result in death.

Family Maximum Benefit

It’s important to note that there’s a limit to the total amount of benefits that can be paid to a family on one worker’s record. This is known as the family maximum benefit. While individual family members may be eligible for certain percentages of the worker’s PIA, the total combined benefit paid to a family usually cannot exceed between 150% and 188% of the worker’s PIA. If the sum of individual benefits exceeds this family maximum, each individual benefit (except the worker’s) will be proportionately reduced until the total equals the maximum.

Strategies for Maximizing Your Social Security Benefits

Given the personalized nature of Social Security benefits, strategic planning can significantly impact the total amount you receive over your lifetime.

Work Longer and Earn More

This is perhaps the most straightforward strategy. By working for at least 35 years and consistently earning at or above the maximum taxable earnings limit, you ensure that no zero-earning years dilute your AIME. Additionally, continuing to work in your later years, especially if those years are among your highest earning, can replace lower-earning years from earlier in your career, thereby boosting your overall average.

Delay Claiming if Possible

As detailed earlier, delaying your claim past your Full Retirement Age (FRA) up to age 70 results in a substantial increase in your monthly benefit due to Delayed Retirement Credits (DRCs). This 8% annual increase is a guaranteed, inflation-adjusted return that is hard to beat elsewhere. For individuals in good health and with other sources of income to cover expenses in their early retirement years, delaying can be one of the most powerful strategies to maximize lifetime benefits.

Coordinate with Your Spouse

Married couples have more complex, but also more powerful, claiming strategies. Spouses can coordinate their claiming decisions to maximize their combined lifetime benefits. For example, one spouse might claim early to provide immediate income while the other delays claiming until age 70 to maximize their individual benefit (and potentially, the survivor benefit for the surviving spouse). There are also “file and suspend” and “restricted application” strategies (though some have been phased out for certain birth cohorts) that financial advisors specializing in Social Security can help navigate. The key is to analyze both spouses’ earning records, health, and financial needs to create an optimal strategy.

Monitor Your Earnings Record

It’s critical to regularly check your Social Security earnings record. The SSA provides an annual Social Security Statement (available online via your “my Social Security” account) that details your reported earnings year by year and provides estimates of your future benefits. Reviewing this statement allows you to identify any discrepancies or missing earnings that could negatively impact your benefit calculation. Correcting errors early can prevent significant headaches down the line.

Tools and Resources to Estimate Your Benefit

The good news is that you don’t have to guess your potential Social Security benefits. The SSA provides excellent tools and resources to help you estimate and plan.

Your Social Security Statement

This is your go-to document. It summarizes your earnings history, provides estimates of your future retirement benefits at different claiming ages (62, FRA, and 70), and also includes estimates for disability and survivor benefits. You can access it online by creating a free “my Social Security” account on the SSA website. Reviewing this statement annually is a fundamental step in your retirement planning.

Online Calculators (SSA Website)

The official Social Security Administration website (ssa.gov) offers several free and user-friendly online calculators. These tools allow you to input different scenarios (e.g., claiming age, future earnings projections) to see how various decisions might affect your benefit amount. They are invaluable for modeling different claiming strategies and understanding the financial implications.

Financial Advisors

For more complex situations, especially for married couples, high earners, or those with unique financial circumstances, consulting a qualified financial advisor specializing in retirement planning and Social Security can be highly beneficial. They can help you analyze your specific situation, navigate intricate claiming rules, and integrate Social Security into your broader financial plan. They can also help you understand the impact of other income sources and taxes on your benefits.

Conclusion

Understanding “how much is Social Security benefit” is far from a simple question; it’s a deep dive into your personal earning history, strategic timing, and a complex yet robust government program. Your Social Security benefit is a dynamic figure, shaped by your contributions, the age you choose to claim, and the annual cost-of-living adjustments that help it keep pace with inflation.

By grasping the fundamental calculation methods, recognizing the critical factors that influence your payout, and exploring the various types of benefits available, you empower yourself to make more informed decisions. Leveraging resources like your annual Social Security statement, online calculators, and professional financial advice can transform uncertainty into clarity, allowing you to strategically plan for a retirement where Social Security plays its intended role as a reliable and vital source of income. Proactive engagement with your Social Security planning is not just an option; it’s a necessity for a financially secure future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.