The year 1929 conjures images of economic despair and financial ruin, largely due to the infamous stock market crash that served as a dramatic prelude to the Great Depression. While often referred to in singular terms, the “crash” was not a single event but rather a series of precipitous declines that collectively shattered investor confidence and revealed deep-seated vulnerabilities within the global financial system. Pinpointing its exact timing requires examining key dates in October 1929 that saw fortunes vanish and economic stability unravel. Understanding these events is not merely a historical exercise; it offers invaluable insights into market dynamics, regulatory necessity, and the enduring human element of fear and greed in finance.

The Unraveling of Prosperity: A Timeline of Disaster

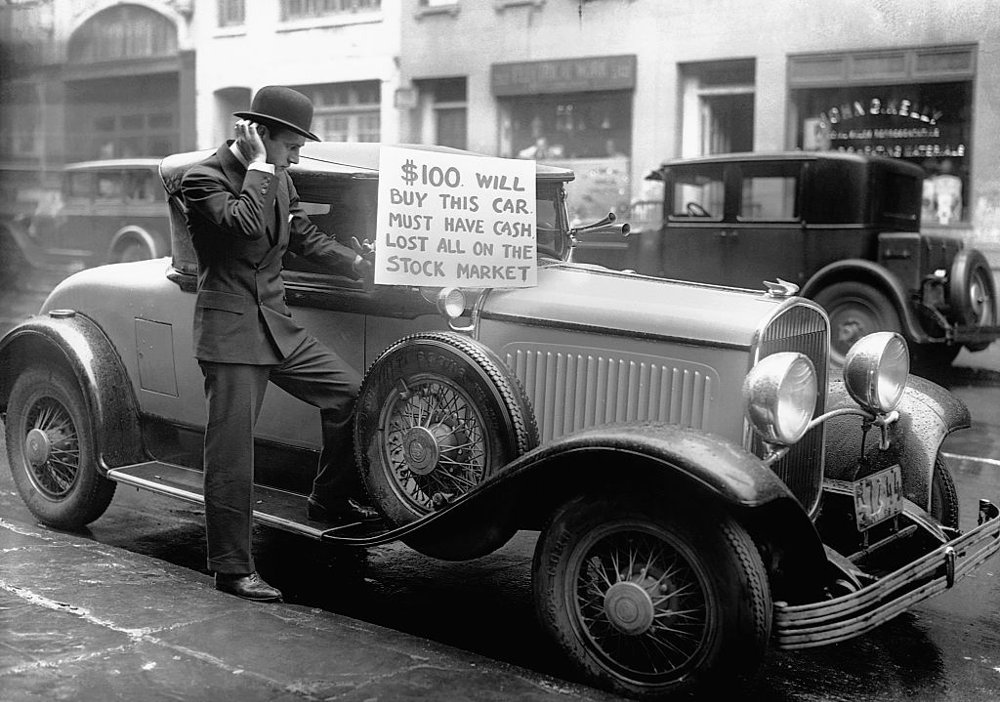

The Roaring Twenties had been characterized by unprecedented economic growth, technological innovation, and a widespread belief in perpetual prosperity. The stock market became a playground for both seasoned investors and speculative newcomers, driving valuations to unsustainable heights. However, beneath this glittering surface, cracks were forming, and the grand edifice of prosperity began to tremble in the autumn of 1929.

Black Thursday: October 24, 1929

The initial tremor struck on Thursday, October 24, 1929. On this day, the New York Stock Exchange (NYSE) experienced an unprecedented wave of selling. The market opened with a sharp decline, and within hours, panic selling erupted. Over 12.8 million shares were traded, more than double the normal volume, as investors scrambled to unload their holdings. Prices plummeted, and ticker tapes ran hours behind, creating an atmosphere of widespread uncertainty and fear. Leading bankers, including J.P. Morgan & Co.’s Thomas W. Lamont and Charles E. Mitchell of National City Bank, attempted to stem the tide by pooling resources and buying large blocks of shares to restore confidence. This intervention provided a temporary reprieve, causing the market to recover some of its losses by the end of the day. Many believed the worst was over, but this was merely the calm before a far greater storm.

Black Monday: October 28, 1929

The illusion of recovery was brutally shattered on Monday, October 28. Following the slight rebound on Black Thursday, Friday and Saturday trading sessions were relatively quiet. However, when the markets reopened on Monday, the previous week’s efforts proved insufficient to counteract the overwhelming bearish sentiment. Panic returned with a vengeance, but this time, there was no coordinated effort to intervene. The Dow Jones Industrial Average (DJIA) plunged nearly 13% in a single day, recording one of its largest percentage drops in history. This day marked a profound shift in market psychology, as hope gave way to desperation. The widespread selling indicated a lack of conviction, and many investors who had held onto their stocks through Black Thursday now capitulated, eager to salvage whatever remained of their investments.

Black Tuesday: October 29, 1929

Black Tuesday, October 29, 1929, is widely regarded as the most devastating day of the crash. The events of Monday had set the stage for outright chaos. The market opened to a deluge of sell orders that overwhelmed the trading system. A staggering 16.4 million shares were traded, a record that would not be broken for nearly 40 years. The DJIA plummeted another 12%, wiping out billions of dollars in market value. This was not merely a correction; it was a full-blown financial catastrophe. Brokers desperately tried to contact margin call clients, many of whom were already bankrupt. The collective wealth of millions of Americans evaporated in a matter of hours, signaling the definitive end of the speculative bubble and the beginning of a prolonged economic downturn. The image of frantic traders, bewildered investors, and desperate individuals became synonymous with this fateful day.

The Aftermath: A Prolonged Decline

While Black Tuesday marked the peak of the immediate panic, the market did not suddenly stabilize. The declines continued intermittently throughout November 1929, and indeed for several years afterward. The initial shockwave of the crash wiped out approximately $30 billion in market value by mid-November, an amount greater than the total cost of World War I for the United States. This staggering loss of capital, coupled with the erosion of consumer and business confidence, played a pivotal role in transforming what might have been a severe recession into the protracted suffering of the Great Depression. The market continued its downward trajectory, reaching its lowest point in July 1932, having lost nearly 90% of its value from its 1929 peak.

Beneath the Surface: Underlying Causes of the Catastrophe

The 1929 crash was not an isolated event but rather the culmination of several interlocking economic and structural weaknesses that had been developing throughout the 1920s. The immediate panic selling was merely the trigger that exposed these vulnerabilities, leading to a catastrophic collapse.

Speculative Mania and Overvalued Stocks

The “Roaring Twenties” fostered an environment of exuberant speculation. Stock prices soared far beyond their intrinsic value, driven by optimism and the belief that the market would always go up. Many companies saw their stock prices double or triple in a short period without a corresponding increase in their earnings or assets. This created a massive speculative bubble, where people bought stocks not for their long-term value, but with the expectation of selling them quickly for a higher price to another, even more optimistic, buyer.

Easy Credit and Margin Buying

A significant fuel for this speculation was the widespread availability of easy credit. Investors could purchase stocks “on margin,” meaning they paid only a small percentage (often as little as 10%) of the stock’s price and borrowed the rest from their brokers. When stock prices began to fall, brokers issued “margin calls,” demanding that investors deposit more money to cover their loans. Unable to do so, investors were forced to sell their holdings, further driving down prices and creating a vicious cycle of selling, falling prices, and more margin calls.

Economic Imbalances and Wealth Inequality

Despite the general prosperity, the economic benefits of the 1920s were not evenly distributed. A significant portion of the nation’s wealth was concentrated in the hands of a few, while many Americans struggled with stagnant wages and agricultural distress. This imbalance limited overall consumer demand, making the economy overly reliant on investment and exports. When these pillars faltered, there wasn’t enough domestic consumer spending power to cushion the blow. Additionally, industries like agriculture had been in recession for years, and coal mining and textiles faced declines even before 1929.

Weak Regulatory Framework

In the 1920s, financial markets operated with minimal government oversight. There was no Securities and Exchange Commission (SEC) to regulate stock exchanges, no federal deposit insurance to protect bank accounts, and very limited transparency regarding corporate financial reporting. This lack of regulation allowed for widespread manipulation, insider trading, and unchecked speculative practices, all of which contributed to the market’s fragility. The absence of a strong central banking response mechanism also exacerbated the crisis when it hit.

The Devastating Ripple Effect: Impact on the Economy and Society

The stock market crash of 1929 was not confined to Wall Street; its tremors reverberated throughout the entire U.S. and global economies, leading to widespread hardship and fundamentally altering the landscape of finance and government.

Bank Failures and Credit Crunch

One of the most immediate and devastating consequences of the crash was a wave of bank failures. Many banks had invested heavily in the stock market themselves or had lent money to individuals and businesses for speculative purposes. As stock prices plummeted and loans went unpaid, banks faced massive losses. Fearing for their savings, people rushed to withdraw their money, leading to “bank runs.” With no federal deposit insurance at the time, countless individuals lost their life savings, further eroding confidence and paralyzing the credit system. Businesses, unable to secure loans, were forced to scale back operations or close entirely.

Business Closures and Mass Unemployment

The collapse of the stock market and the subsequent banking crisis triggered a severe contraction in economic activity. Businesses, facing diminished consumer demand and an inability to access credit, cut production, reduced wages, and laid off workers. Factories stood idle, and storefronts were shuttered. The unemployment rate skyrocketed from around 3% in 1929 to an agonizing 25% by 1933, leaving millions of Americans without income or prospects. This widespread joblessness led to poverty, homelessness, and immense social distress across the nation.

Global Economic Contagion

The U.S. economy was deeply interconnected with the rest of the world, particularly Europe, which was still recovering from World War I. American banks had lent heavily to European nations, and the crash led to a sharp reduction in these loans and a demand for repayment. This triggered a cascade of financial crises across Europe, further deepening the global economic downturn. Protectionist trade policies, such as the Smoot-Hawley Tariff Act of 1930, exacerbated the problem by stifling international trade and deepening the global depression.

Psychological Trauma and Loss of Trust

Beyond the quantifiable economic losses, the crash inflicted deep psychological trauma on the American populace. The sudden evaporation of wealth, the widespread unemployment, and the loss of faith in financial institutions fostered a pervasive sense of insecurity and cynicism. For many, the American Dream seemed shattered, and trust in the capitalist system was severely shaken. This psychological impact endured for generations, influencing saving habits, investment decisions, and political attitudes for decades to come.

Lessons Learned: Shaping Modern Financial Systems

The catastrophe of 1929 and the ensuing Great Depression served as a harsh but invaluable teacher, prompting fundamental reforms that reshaped the U.S. financial system and laid the groundwork for greater stability and investor protection.

Regulatory Reforms: SEC and Glass-Steagall

In response to the crash, the U.S. government enacted landmark legislation aimed at preventing a recurrence. The Securities Act of 1933 and the Securities Exchange Act of 1934 established the Securities and Exchange Commission (SEC), an independent agency tasked with regulating the stock market, preventing fraud, and ensuring transparency. The Glass-Steagall Act of 1933 (officially the Banking Act of 1933) created the Federal Deposit Insurance Corporation (FDIC) to insure bank deposits, restoring public confidence in the banking system, and separated commercial banking from investment banking, aimed at curbing speculative activities by deposit-taking institutions.

Central Bank’s Role: Lender of Last Resort

The Federal Reserve’s failure to act decisively during the early stages of the crisis was a critical error. Prior to 1929, the Fed lacked a clear understanding or mandate for its role in preventing financial panics. Post-crash analysis highlighted the necessity for a central bank to act as a “lender of last resort,” providing liquidity to solvent banks during crises to prevent widespread failures. This understanding profoundly influenced subsequent monetary policy and central bank interventions in future financial turmoil.

Investor Protection and Education

The crash underscored the need for greater investor protection and public education about the risks of financial markets. Regulations were put in place to mandate disclosure of financial information by corporations, prohibit manipulative practices, and ensure that brokers acted in the best interest of their clients. While not perfect, these measures aimed to create a fairer and more transparent market where investors could make informed decisions, reducing the likelihood of being swept up in speculative bubbles fueled by misinformation.

The Importance of Diversification and Prudent Investing

For individual investors, the crash provided a painful lesson in risk management. The perils of putting all eggs in one basket, engaging in excessive margin buying, and chasing speculative gains became starkly apparent. The importance of diversification across different asset classes, long-term investing strategies, and thorough research became fundamental principles of sound financial planning, moving away from the speculative frenzy that characterized the 1920s.

Avoiding a Repeat: Contemporary Safeguards and Future Challenges

While the financial system of today is vastly different from that of 1929, the memory of the crash continues to inform policy decisions and risk management strategies. Modern safeguards are designed to prevent such a catastrophic collapse, though new challenges constantly emerge.

Stress Tests and Capital Requirements

Following the 2008 financial crisis, which echoed some themes of 1929 (though with different root causes), regulatory bodies significantly strengthened capital requirements for banks and introduced rigorous stress tests. These tests assess how financial institutions would fare under various adverse economic scenarios, ensuring they hold sufficient capital buffers to absorb losses and prevent systemic collapse. This proactive approach aims to build resilience into the financial system.

Early Warning Systems and Market Surveillance

Regulators now employ sophisticated data analytics and surveillance tools to monitor market activity for signs of excessive speculation, manipulation, or emerging systemic risks. International cooperation between regulatory bodies has also improved, recognizing the global interconnectedness of financial markets. The goal is to identify and address potential problems before they escalate into full-blown crises.

Addressing New Forms of Speculation

While the direct causes of the 1929 crash involved traditional stock market speculation, modern financial markets present new avenues for risk. The rise of complex derivatives, high-frequency trading, and highly leveraged hedge funds introduces new forms of speculative behavior and interconnectedness. Regulators face the ongoing challenge of understanding and appropriately regulating these evolving financial instruments and practices to prevent new bubbles from forming.

The Ongoing Quest for Financial Stability

The events of 1929 serve as a permanent reminder that financial markets are inherently prone to cycles of boom and bust, often driven by human psychology. Despite advancements in regulation and economic understanding, the quest for absolute financial stability remains an ongoing challenge. Vigilance, adaptability, and a commitment to prudent oversight are essential to mitigate risks and ensure that the lessons learned from the darkest days of the stock market’s history continue to guide future financial policies, protecting investors and the broader economy from similar catastrophic events.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.