In the world of finance, few acronyms carry as much weight as “S&P.” Whether you are a seasoned institutional investor or a newcomer checking your retirement account for the first time, the S&P 500 is likely the most significant influence on your financial health. Often referred to simply as “the market,” the Standard & Poor’s 500 Index represents the 500 leading publicly traded companies in the United States. It is not merely a list of stocks; it is a complex, living entity that serves as the ultimate barometer for the U.S. economy and, by extension, the global financial landscape.

To understand the S&P 500 is to understand the mechanics of modern capitalism. This article explores the depths of what the S&P 500 is, how it functions, and why it remains the gold standard for investors worldwide.

The Fundamentals of the S&P 500 Index

At its core, an index is a statistical measure of change in a representative group of individual data points. In the case of the S&P 500, those data points are the stock prices of the most influential corporations in America. Unlike other indices that might focus on a specific sector, the S&P 500 is designed to capture the “large-cap” segment of the market, covering approximately 80% of available market capitalization.

Origins and the Role of Standard & Poor’s

The index is maintained by S&P Dow Jones Indices, a joint venture that traces its roots back to 1860. Henry Varnum Poor first published a guide to the financial state of U.S. railroads, and later, in 1923, the Standard Statistics Company created its first stock market index. The modern iteration of the S&P 500 as we know it today—containing 500 companies—was launched on March 4, 1957. Since then, it has become the most followed stock market index in the world, eclipsing the older Dow Jones Industrial Average (DJIA) in terms of its perceived accuracy in reflecting the broader economy.

The Concept of Market Capitalization Weighting

One of the most critical aspects of the S&P 500 is that it is “float-adjusted market-capitalization-weighted.” This means that companies with higher market values have a greater impact on the index’s performance. Market capitalization is calculated by multiplying the share price by the number of outstanding shares. However, the S&P 500 uses “float-adjusted” capitalization, which only counts the shares available to the public, excluding those held by insiders or government agencies.

This weighting methodology is significant because it reflects the actual investment opportunities available in the market. When a trillion-dollar giant like Apple or Microsoft sees a 1% shift in stock price, it moves the entire index much more significantly than a 1% shift in a company at the bottom of the list.

How Companies Are Selected for the Index

A common misconception is that the S&P 500 is simply the 500 largest companies in America. While size is a primary factor, it is not the only one. The index is “curated” rather than strictly rules-based, meaning a committee decides who stays and who goes based on a set of stringent eligibility criteria.

The Eligibility Requirements: More Than Just Size

To be considered for the S&P 500, a company must meet several financial health and liquidity standards. As of recent years, the market cap requirement for entry is typically north of $15 billion. However, size is just the beginning. The company must be a U.S. entity, have a positive sum of earnings over the previous four quarters, and maintain high liquidity—meaning its shares must be easy to buy and sell in large volumes. These rules ensure that the index remains a high-quality representation of the economy rather than a volatile list of “flash-in-the-pan” success stories.

The Role of the Index Committee

The S&P Index Committee meets regularly to review the index’s composition. They look at sector balance to ensure the index isn’t overly skewed toward one industry, though the natural growth of sectors like Technology has historically challenged this balance. When a company no longer meets the criteria—perhaps due to a merger, a decline in market cap, or a sustained period of losses—the committee removes it and selects a replacement. This “survivorship bias” is one reason the S&P 500 tends to perform well over the long term; it systematically removes losers and adds winners.

Why the S&P 500 is the Standard for Measuring Success

For most investors, the S&P 500 isn’t just a number on the news; it is the “benchmark” against which all other investments are measured. If a mutual fund manager claims to be an expert, the first question they are asked is: “Did you beat the S&P 500?”

Passive vs. Active Management

The rise of the S&P 500 has coincided with a massive shift from active to passive investing. Active management involves professional stock pickers trying to outperform the market. Passive management involve buying an index fund that simply tracks the S&P 500. Decades of data, most notably the SPIVA (S&P Indices Versus Active) reports, show that over long periods, the vast majority of active managers fail to beat the S&P 500. This realization has led to trillions of dollars flowing into S&P 500 index funds, making it the bedrock of modern retirement planning.

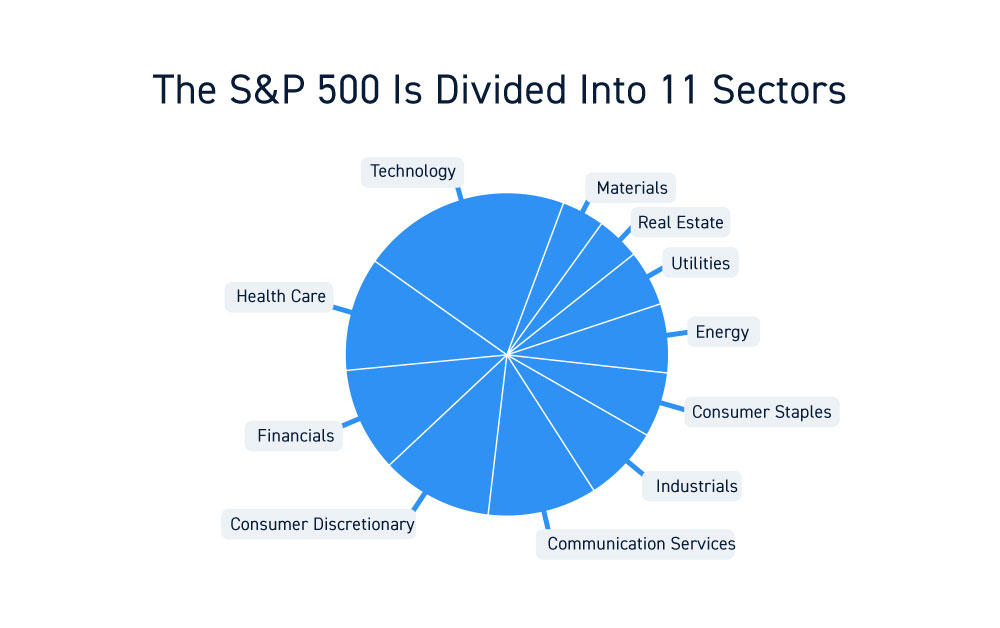

A Reflection of the US Economy and Sector Diversification

The index is divided into 11 Global Industry Classification Standard (GICS) sectors, including Information Technology, Health Care, Financials, Consumer Discretionary, and Energy. Because the index covers such a wide range of industries, it acts as a real-time thermometer for the American economy. When consumer spending is high, the Discretionary sector rises; when interest rates climb, the Financial sector reacts. This diversification provides a level of stability that individual stocks cannot offer, as a downturn in one sector (like Energy) can often be offset by a boom in another (like Technology).

Practical Strategies for Investing in the S&P 500

You cannot “buy” the S&P 500 index itself, as it is just a list of numbers. However, you can buy products that replicate its performance. For the average individual, this is perhaps the most efficient way to build wealth in the history of finance.

Index Funds and ETFs: Low-Cost Entry Points

The most popular way to invest in the S&P 500 is through Exchange-Traded Funds (ETFs) or Mutual Funds. Titans of the industry like Vanguard, BlackRock (iShares), and State Street (SPDR) offer funds that hold all 500 stocks in the exact proportions of the index. The primary advantage here is the “expense ratio.” Many S&P 500 ETFs have fees as low as 0.03%, meaning for every $10,000 invested, you only pay $3 a year in management fees. This low-cost structure allows more of your money to stay in the market, compounding over time.

The Power of Long-Term Compounding

Historically, the S&P 500 has provided an average annual return of approximately 10% before inflation. While the market does not go up every year—some years see significant drops—the long-term trajectory has been consistently upward. Through a strategy known as Dollar-Cost Averaging (investing a set amount regularly regardless of price), investors can harness the power of compounding. Over 30 years, a modest monthly contribution to an S&P 500 fund can grow into a substantial nest egg, thanks to the collective growth and innovation of the 500 largest companies in the U.S.

Navigating the Risks and Limitations

While the S&P 500 is a powerful tool, it is not without risks. Intelligent investing requires an understanding of where the index might be vulnerable.

Market Concentration and the Tech Heavyweight Dilemma

Because the index is market-cap weighted, it has become increasingly “top-heavy.” In recent years, a small group of massive technology companies—often called the “Magnificent Seven”—have come to represent a significant percentage of the entire index’s value. This means that if the tech sector experiences a bubble or a regulatory crackdown, the entire S&P 500 can suffer, even if the other 493 companies are doing well. Diversification within the 500 is high, but the concentration of power at the top is a factor every investor must monitor.

Understanding Systematic Risk and Volatility

Finally, it is essential to remember that the S&P 500 is subject to “systematic risk”—the risk inherent to the entire market. Events like global pandemics, geopolitical conflicts, or sudden changes in Federal Reserve policy can cause the index to drop by 20% or more (a “bear market”). Investing in the S&P 500 requires a high tolerance for volatility and a long-term time horizon. It is a vehicle for wealth creation, but it is not a “safe” asset in the way a savings account is; your principal can and will fluctuate.

In conclusion, the S&P 500 is more than just a financial metric; it is the heartbeat of American corporate success. By understanding its structure, its selection process, and its role as a benchmark, investors can make informed decisions that align with their long-term financial goals. Whether used as a yardstick for performance or as the core of a retirement portfolio, the S&P 500 remains the most vital tool in the world of money.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.