The annual ritual of tax filing can often feel like a labyrinth, with complexities ranging from understanding deductions to deciphering forms. Yet, beyond the calculation and preparation, one fundamental question remains for many taxpayers: “Where do I actually pay my taxes?” This seemingly simple query opens up a vast landscape of options, requirements, and strategic considerations that are crucial for ensuring compliance, avoiding penalties, and maintaining financial peace of mind.

Understanding the “where” of tax payments is more than just knowing an address or a website; it’s about comprehending the diverse channels available, recognizing the specific authority to which you owe money, and leveraging the most efficient and secure methods for your financial situation. From the convenience of online portals to the steadfastness of traditional mail, and from federal obligations to state and local dues, this guide will illuminate the pathways to fulfilling your tax responsibilities effectively and strategically.

Understanding Your Tax Obligations: Who, What, and When

Before you can determine where to send your money, it’s paramount to understand who you’re paying, what kind of taxes you’re paying, and when these payments are due. This foundational knowledge is the bedrock of effective tax management and prevents misdirected payments or missed deadlines that can lead to costly penalties.

Identifying Your Tax Authorities: Federal, State, and Local

The United States operates on a multi-tiered tax system, meaning you typically owe taxes to more than one governmental body.

- Federal Taxes: These are owed to the U.S. government, primarily to the Internal Revenue Service (IRS). This includes federal income tax, self-employment tax, and various excise taxes. Everyone earning above a certain threshold, or engaging in taxable activities, is subject to federal taxation.

- State Taxes: Most states impose their own income tax, sales tax, and property taxes. The rules, rates, and even the existence of certain taxes vary significantly from state to state. For instance, states like Florida, Texas, and Washington do not have a state income tax, while others like California and New York have some of the highest. Understanding your state’s specific tax structure is critical.

- Local Taxes: At the municipal or county level, you might encounter local income taxes, property taxes, or other specialized taxes. These are common in many cities and counties, particularly for property owners, and their collection methods can differ significantly from federal and state processes. For example, some cities levy an occupational privilege tax or a school district income tax.

Accurately identifying all the entities to which you owe taxes is the first step in directing your payments correctly. Each authority will have its own preferred and designated payment channels.

Types of Taxes You Might Owe: Income, Property, Sales, and Payroll

The “what” refers to the specific categories of taxes you are liable for. While the focus often falls on income tax, other types are equally important:

- Income Tax: The most common form, levied on wages, salaries, investment gains, and other forms of income. This is typically paid annually, though many pay throughout the year via withholding or estimated payments.

- Property Tax: Assessed on real estate you own, typically collected by local governments (counties or municipalities). These are often paid in installments, sometimes through an escrow account managed by your mortgage lender.

- Sales Tax: A consumption tax levied on the sale of goods and services, usually paid by the consumer at the point of purchase. Businesses collect and remit these to the relevant state or local authority.

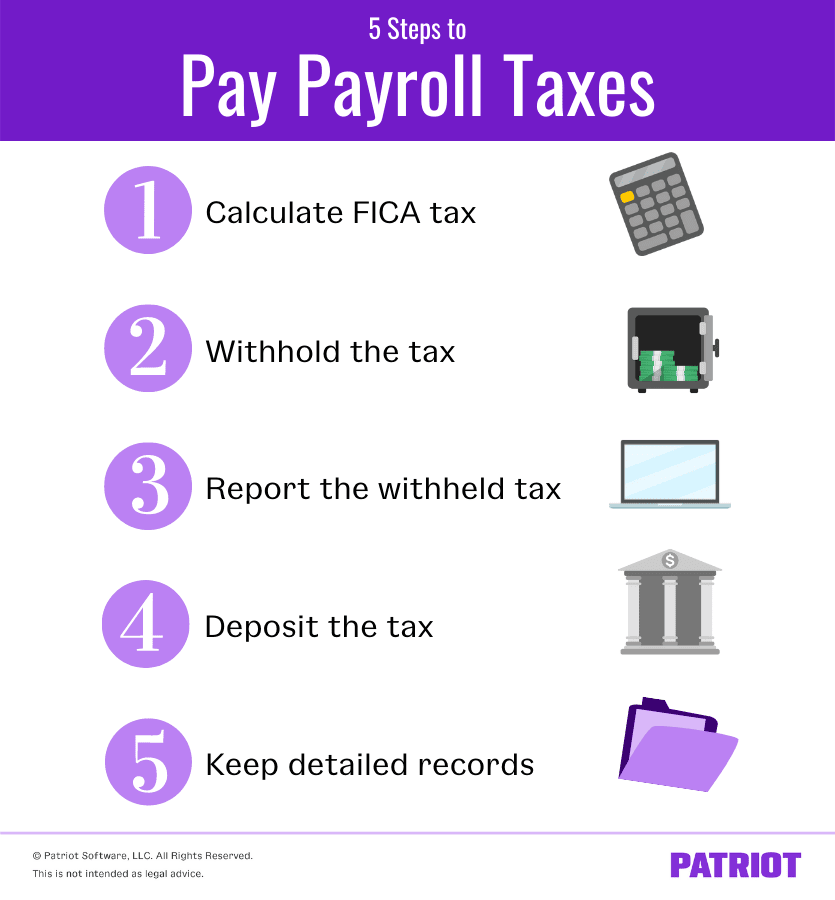

- Payroll Taxes: Include Social Security and Medicare taxes (FICA), paid by both employees and employers. Self-employed individuals pay both halves as self-employment tax. Employers are responsible for withholding and remitting these.

- Other Taxes: This can include excise taxes (on specific goods like fuel or tobacco), estate taxes, gift taxes, and various business taxes.

Each tax type may have unique payment mechanisms and due dates, further emphasizing the need for a comprehensive understanding of your full tax profile.

The Critical Role of Tax Deadlines

Perhaps as important as knowing where to pay is knowing when to pay. Missing a tax deadline can result in penalties, interest charges, and increased scrutiny from tax authorities.

- Annual Income Tax Filing: For most individual taxpayers, the federal income tax deadline is April 15th (or the next business day if April 15th falls on a weekend or holiday). State income tax deadlines often align with federal deadlines but can vary.

- Estimated Tax Payments: If you are self-employed, have significant income not subject to withholding, or are retired, you may need to pay estimated taxes quarterly. These deadlines are typically April 15th, June 15th, September 15th, and January 15th of the following year.

- Property Taxes: These deadlines are highly localized and can vary significantly by county or municipality. Many areas offer discounts for early payment or impose penalties for late payment.

- Extensions: While you can often get an extension to file your tax return (e.g., until October 15th for federal income tax), this is generally not an extension to pay any taxes you owe. If you expect to owe, you should still pay by the original deadline to avoid interest and penalties.

Timely payment is a non-negotiable aspect of tax compliance. Mark your calendars, set reminders, and familiarize yourself with all relevant due dates.

Modern Pathways: Paying Taxes Online

In the digital age, online payment methods have become the most popular, convenient, and often the most secure way to pay taxes. Governments at all levels have invested heavily in robust online portals to streamline the payment process.

Direct Pay Options: IRS.gov and State Portals

The most straightforward way to pay your federal taxes online is directly through the IRS website.

- IRS Direct Pay: This free service allows you to pay your federal income taxes directly from your checking or savings account. You can schedule payments up to 365 days in advance, receive email confirmations, and modify or cancel payments up to two days before the scheduled date. It’s ideal for final tax payments, estimated taxes, and payments for amended returns.

- State Revenue Websites: Similar to the IRS, every state tax authority maintains its own official website with direct pay options. These portals typically offer electronic funds withdrawal (EFW) directly from your bank account, often referred to as ACH debit. You’ll need your bank account and routing numbers, along with relevant tax identification information.

Using official government websites for direct pay offers the highest level of security and avoids any processing fees, making it the preferred method for many.

Utilizing Tax Software and E-File Services

Tax preparation software has revolutionized how millions of Americans file and pay their taxes.

- Integrated Payment: Popular tax software programs like TurboTax, H&R Block Tax Software, and TaxAct allow you to prepare and e-file your federal and state returns. Crucially, they also integrate payment options directly into the filing process. You can authorize an electronic funds withdrawal from your bank account when you submit your e-filed return, ensuring your payment is processed simultaneously.

- Estimated Tax Integration: Many software solutions also help calculate and schedule estimated tax payments, simplifying compliance for self-employed individuals and those with non-wage income.

This method offers unparalleled convenience, as the payment process is seamlessly integrated with the return submission, reducing the chance of errors or missed steps.

Third-Party Payment Processors: Credit Cards, Debit Cards, and Digital Wallets

While direct pay from your bank account is free, you can also pay your taxes using a credit card, debit card, or certain digital wallets through authorized third-party processors.

- Convenience for a Fee: The primary advantage is convenience and the potential to earn credit card rewards. However, these services charge a processing fee, typically a percentage for credit cards (around 1.87% to 2.25%) and a flat fee for debit cards (around $2.50 to $4.00). It’s essential to weigh the fee against any potential rewards or the need for short-term liquidity.

- Authorized Processors: The IRS (and most state tax agencies) only work with a select list of authorized third-party processors (e.g., PayUSAtax, ACI Payments, Official Payments). Always use one of these approved vendors to ensure your payment is secure and correctly remitted.

This option is particularly useful for those who prefer to manage cash flow, utilize credit card benefits, or simply find it more convenient than direct bank transfers.

Estimated Tax Payments for Self-Employed and Gig Workers

For individuals not subject to employer withholding, such as freelancers, small business owners, and gig economy workers, estimated tax payments are crucial. The same online methods apply:

- IRS Direct Pay: Ideal for scheduling quarterly federal estimated payments.

- EFTPS (Electronic Federal Tax Payment System): A free service provided by the U.S. Treasury, specifically designed for business and individual taxpayers to make federal tax payments electronically. It requires enrollment but allows for scheduled payments up to 365 days in advance and offers a detailed payment history. It’s often preferred by businesses and those who make frequent federal tax payments.

- State Estimated Payments: Similar systems exist at the state level. Many states offer their own online portals or require estimated payments to be submitted through their specific electronic systems.

Proactive and timely estimated payments prevent a large, unexpected tax bill and potential underpayment penalties at year-end.

Traditional and Alternative Payment Methods

While online payments dominate, traditional methods remain viable and, in some specific circumstances, even necessary. Additionally, for those facing financial hardship, alternative arrangements can be made with tax authorities.

Paying by Mail: Checks and Money Orders

The classic method of sending a physical check or money order remains an option for both federal and state taxes.

- Federal Mail Payments: If you are paying your federal taxes by mail, you typically include a check or money order (payable to the “U.S. Treasury”) with a Form 1040-V, Payment Voucher. It’s crucial to mail it to the correct IRS address, which varies based on your location and whether you are sending a payment with your return or separately. Always consult the IRS website or your tax instructions for the most current mailing address.

- State and Local Mail Payments: State and local tax agencies also accept payments by mail. Similar to federal payments, you’ll need to include a payment voucher or the relevant form and send it to the designated address for your specific state or locality.

- Important Considerations: Always use certified mail with a return receipt for proof of mailing and delivery. Ensure your check or money order is correctly filled out with your name, address, phone number, Social Security number (or EIN), and the tax year/form being paid. Never send cash through the mail.

While less instant, mail payments provide a tangible record of submission (especially with certified mail) and are suitable for those who prefer not to conduct financial transactions online.

In-Person Payments: When and Where It’s an Option

For those who prefer a face-to-face transaction or need immediate assistance, limited in-person payment options exist.

- IRS Taxpayer Assistance Centers (TACs): Some IRS TACs accept cash payments, but it’s essential to check their specific services and availability beforehand, as not all TACs offer this. Appointments are often required. They may also be able to process payments via check or money order.

- Retail Partners (for federal cash payments): The IRS has partnered with certain retail chains (e.g., 7-Eleven, Family Dollar, CVS Pharmacy) to allow taxpayers to make federal cash tax payments. You must first generate a payment barcode online (through IRS.gov or one of the third-party processors) and then present it to the retailer. This is a convenient option for those who deal primarily in cash.

- State and Local Offices: Many state and local tax offices also offer in-person payment options, particularly for property taxes or local income taxes. Always verify the office hours, required documentation, and accepted payment methods before visiting.

These options cater to specific needs, such as those without bank accounts, or individuals seeking direct interaction for their tax payments.

Addressing Underpayments: Payment Plans and Offers in Compromise

What happens if you can’t pay your taxes by the deadline? Ignoring the problem is the worst approach. The IRS and state tax agencies offer solutions for taxpayers facing financial hardship.

- Payment Plans (Installment Agreements): If you owe federal taxes and cannot pay the full amount immediately, you can request an installment agreement with the IRS. This allows you to make monthly payments for up to 72 months. You will still incur interest and penalties, but it prevents more aggressive collection actions. Short-term payment plans (up to 180 days) are also available. Similar options exist at the state level.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to settle their tax liability with the IRS for a lower amount than what they originally owed. This is typically an option for individuals experiencing extreme financial difficulty where paying the full amount would cause significant hardship. The IRS considers your ability to pay, income, expenses, and asset equity. OICs are complex and often require professional tax assistance.

- Penalty Abatement: In certain situations, the IRS may waive penalties if you have a reasonable cause for failure to file or pay on time (e.g., natural disaster, serious illness). Interest generally cannot be abated.

These relief options underscore the importance of communicating with tax authorities if you anticipate or experience payment difficulties, rather than simply failing to pay.

Strategic Tax Payment Planning: Beyond Just Sending Money

Paying taxes effectively involves more than just selecting a payment method; it’s about incorporating tax obligations into your broader financial strategy. Proactive planning can minimize surprises, manage cash flow, and ensure long-term financial health.

Proactive Withholding and Estimated Tax Adjustments

Don’t wait until tax season to think about paying.

- W-4 Adjustments: For employees, regularly reviewing and adjusting your W-4 form with your employer can ensure the correct amount of federal income tax is withheld from each paycheck. This prevents under-withholding (leading to a large tax bill) or over-withholding (tying up funds that could be earning interest or used for other financial goals).

- Estimated Tax Review: Self-employed individuals should regularly review their income and expenses throughout the year to adjust their estimated tax payments. Using tools like the IRS Tax Withholding Estimator can help project your tax liability and adjust payments accordingly, avoiding penalties for underpayment.

Aligning your withholding or estimated payments with your actual tax liability is a key strategy for smooth tax management.

Leveraging Financial Tools for Tax Management

A variety of financial tools and services can simplify the process of tracking income, expenses, and tax payments.

- Budgeting Software/Apps: Tools like Mint, YNAB (You Need A Budget), or even simple spreadsheets can help you allocate funds specifically for tax payments, ensuring you have the necessary cash readily available when due.

- Accounting Software: For small businesses and freelancers, accounting software like QuickBooks, FreshBooks, or Xero can automate expense tracking, invoice generation, and financial reporting, making tax calculations and payment preparation much more efficient. Many even offer direct integrations for tax payments.

- Dedicated Savings Accounts: Setting aside a percentage of each income payment into a separate, interest-bearing savings account earmarked specifically for taxes can prevent scrambling for funds when tax deadlines approach.

These tools transform tax payment from a dreaded annual event into an integrated part of your ongoing financial routine.

The Cost of Procrastination: Penalties and Interest

Delaying or avoiding tax payments comes with significant financial repercussions.

- Failure-to-Pay Penalty: The IRS imposes a penalty for failing to pay on time, typically 0.5% of the unpaid taxes for each month or part of a month that taxes remain unpaid, capped at 25% of your unpaid tax bill.

- Failure-to-File Penalty: If you don’t file your return on time, the penalty is much steeper: 5% of the unpaid taxes for each month or part of a month that a tax return is late, capped at 25% of your unpaid tax. If both apply, the failure-to-file penalty reduces the failure-to-pay penalty.

- Interest: In addition to penalties, the IRS charges interest on underpayments and unpaid balances. This interest rate can change quarterly and typically compounds daily, making the total amount owed grow rapidly over time. State and local tax agencies have similar penalty and interest structures.

The financial burden of procrastination far outweighs any perceived convenience, making timely payment a financially prudent decision.

Seeking Professional Guidance

When in doubt, or when dealing with complex financial situations, consulting with a qualified tax professional is always a wise investment.

- Tax Preparers/CPAs: These professionals can not only prepare your returns but also advise on optimal payment strategies, help navigate payment plans, and represent you in dealings with tax authorities.

- Financial Advisors: A comprehensive financial advisor can integrate your tax planning into your broader investment, retirement, and estate planning goals, offering a holistic approach to managing your wealth, including your tax obligations.

Their expertise can help ensure accuracy, compliance, and strategic financial decision-making when it comes to the “where” and “how” of paying your taxes.

In conclusion, understanding where to pay your taxes is a crucial component of sound financial management. By familiarizing yourself with the various tax authorities, available payment methods, critical deadlines, and strategic planning tools, you can transform a potentially stressful obligation into a manageable and integrated aspect of your financial life. Whether you choose the convenience of online payments, the reliability of mail, or require the flexibility of payment plans, an informed approach is your best defense against errors and penalties, ensuring you fulfill your civic duty efficiently and confidently.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.