The prime rate stands as a cornerstone of the financial system, a pivotal interest rate that influences everything from the cost of corporate borrowing to the variable rates on consumer credit cards and mortgages. Understanding what the prime rate is, how it’s determined, and its current trajectory is crucial for businesses making investment decisions, individuals managing personal finances, and anyone seeking to grasp the broader economic landscape. Far from an abstract concept, the prime rate directly impacts the financial health of millions, acting as a barometer for monetary policy and economic conditions. In a world where economic indicators constantly shift, staying informed about the prime rate isn’t just prudent; it’s essential for sound financial planning and strategic decision-making.

Understanding the Prime Rate: A Core Financial Indicator

At its core, the prime rate is the interest rate that commercial banks charge their most creditworthy corporate customers on short-term loans. While this definition might sound narrow, its influence ripples through virtually every segment of the economy, making it one of the most closely watched financial benchmarks. Its significance stems from its direct relationship with the central bank’s monetary policy, serving as a foundational element upon which many other lending rates are built.

Defining the Prime Rate

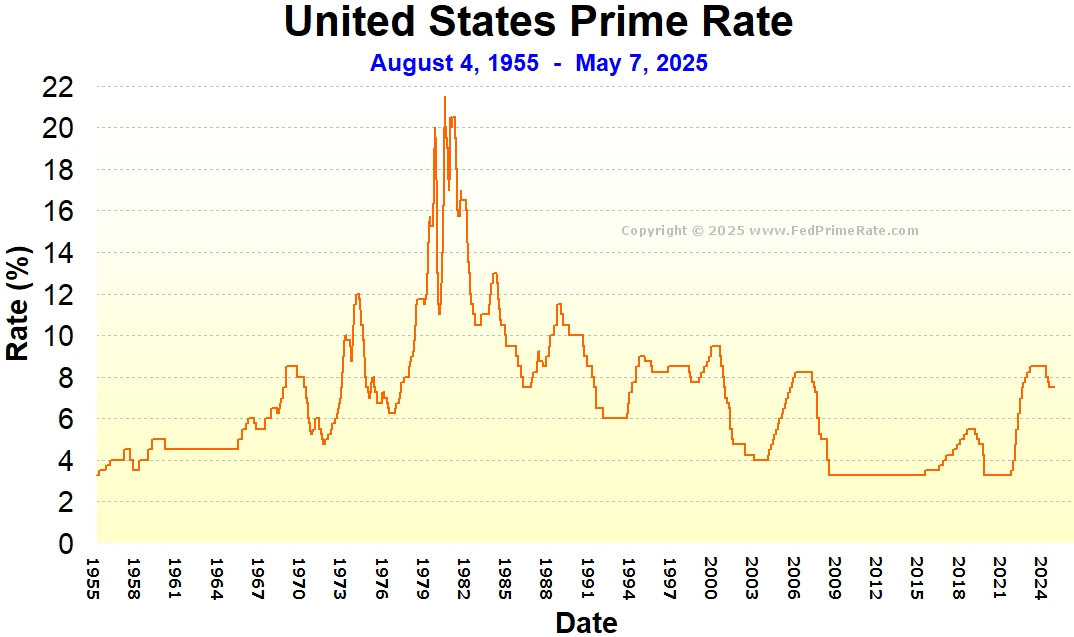

The prime rate isn’t set by a single entity in a vacuum; rather, it’s a reflection of the prevailing economic conditions and, most importantly, the monetary policy enacted by a country’s central bank. In the United States, for instance, the prime rate is closely tied to the Federal Funds Rate, which is the target rate set by the Federal Open Market Committee (FOMC) of the Federal Reserve. The Federal Funds Rate is the rate at which commercial banks lend their excess reserves to other banks overnight. Historically, the U.S. prime rate has been approximately 3 percentage points higher than the upper limit of the federal funds target range. This spread accounts for various factors, including the banks’ operational costs, risk assessment, and desired profit margins. While this spread has been remarkably consistent over decades, minor fluctuations can occur based on market liquidity and competitive pressures among banks. Unlike some other rates that are subject to negotiation, the prime rate is publicly posted by major banks and is largely uniform across the industry, lending it an air of universality and transparency.

How the Prime Rate is Determined

The primary driver of the prime rate is the central bank’s monetary policy, specifically its decisions regarding its benchmark interest rate. For the U.S., this means the Federal Reserve’s FOMC meetings, held eight times a year (or more frequently if economic conditions warrant), are critical events. During these meetings, the FOMC assesses a wide array of economic data—including inflation rates, employment figures, GDP growth, and consumer spending—to determine the appropriate stance for monetary policy. If the Fed believes inflation is too high, it may raise the federal funds rate target to cool down the economy by making borrowing more expensive, which, in turn, leads to an increase in the prime rate. Conversely, during periods of economic slowdown or recession, the Fed might lower the federal funds rate to stimulate borrowing and investment, causing the prime rate to fall. This direct linkage makes the prime rate a powerful tool for the central bank to influence economic activity, guiding inflation, employment, and overall economic stability. Understanding this mechanism is key to anticipating future movements in the prime rate and their potential impact on financial obligations.

The Prime Rate vs. Other Interest Rates

While the prime rate is foundational, it’s crucial to distinguish it from the myriad of other interest rates consumers and businesses encounter. The prime rate serves as a baseline, but most other loan products carry additional premiums based on the borrower’s creditworthiness, the loan’s term, the type of collateral, and the specific market’s risk perception. For example, consumer credit card Annual Percentage Rates (APRs) are almost always significantly higher than the prime rate, often fluctuating with it, but including a substantial risk premium for unsecured debt. Similarly, mortgage rates, while influenced by the broader interest rate environment, also factor in the long-term nature of the loan, the property as collateral, and prevailing bond market yields, which can move independently of short-term central bank actions. Auto loan rates, personal loans, and student loans all follow similar patterns: they are influenced by the prime rate but incorporate additional layers of risk assessment and market dynamics. This hierarchical relationship means that while the prime rate sets a general direction, the specific rate an individual or business receives will depend on their unique financial profile and the specific loan product.

The Current Landscape: What’s Driving the Prime Rate Today?

The prime rate is not static; it is a dynamic indicator constantly responding to shifts in global and domestic economic conditions, as well as the deliberate actions of central banks. To understand “what is prime rate right now,” one must delve into the immediate context of monetary policy and the most pressing economic factors at play.

Federal Reserve’s Stance and Recent Actions

In recent times, central banks globally, including the Federal Reserve, have been navigating a complex economic environment characterized by persistent inflation pressures, robust labor markets, and geopolitical uncertainties. The Fed’s primary mandate revolves around achieving maximum employment and stable prices (i.e., controlling inflation). Over the past couple of years, in response to elevated inflation rates, the Federal Reserve embarked on an aggressive campaign of interest rate hikes, significantly increasing the federal funds rate target. This tightening monetary policy directly translated into a higher prime rate.

As of the current period (early 2024), the Fed has indicated a more cautious, data-dependent approach. Following a series of significant hikes, the FOMC has paused its rate increases, signaling a period of assessment. The focus has shifted from aggressive tightening to determining if the current restrictive stance is sufficient to bring inflation back to the 2% target without causing an undue economic slowdown or recession. Future movements in the prime rate will hinge on whether the Fed decides to maintain current rates for an extended period, or if improving inflation data and/or a weakening labor market prompt them to consider rate cuts later in the year. The messaging from the Fed consistently emphasizes flexibility and responsiveness to incoming economic data.

Influential Economic Factors

Beyond direct central bank actions, several key economic factors are constantly shaping the environment in which prime rate decisions are made:

- Inflation Data: Core inflation metrics, such as the Consumer Price Index (CPI) and Personal Consumption Expenditures (PCE) price index, are paramount. If inflation remains stubbornly above the Fed’s 2% target, it could lead to the prime rate remaining elevated or even rising further. Conversely, a clear and sustained downward trend in inflation could pave the way for future rate reductions.

- Labor Market Strength: The unemployment rate, job creation figures (e.g., non-farm payrolls), and wage growth are critical indicators. A strong labor market typically gives the Fed more leeway to keep rates higher, as it suggests the economy can withstand restrictive monetary policy. A significant weakening in employment, however, would likely prompt the Fed to consider lowering rates to prevent a severe downturn.

- Economic Growth (GDP): Gross Domestic Product (GDP) reports offer a broad measure of economic health. Sustained robust growth might suggest the economy can handle higher rates, while signs of stagnation or contraction could push the Fed towards easing policy.

- Consumer Spending and Business Investment: These indicators reflect confidence and demand within the economy. Healthy spending and investment support higher rates, while a slowdown could signal the need for policy adjustments.

- Geopolitical Events and Global Economy: External factors, such as international conflicts, supply chain disruptions, and economic performance of major trading partners, can also indirectly influence the domestic economic outlook and, consequently, the Fed’s decisions regarding the prime rate.

What “Right Now” Implies for Borrowers and Lenders

In the current environment of elevated, albeit potentially peaking, interest rates, the implications for borrowers and lenders are significant. For borrowers, particularly those with variable-rate debt (like many credit cards, HELOCs, and ARMs), “right now” means higher monthly payments and increased borrowing costs compared to a few years ago. Businesses seeking short-term capital or lines of credit also face higher financing expenses, which can impact profitability and investment decisions. This high-rate environment can act as a natural brake on spending and economic expansion.

For lenders, “right now” presents opportunities for higher interest income on loans and a potentially more attractive environment for attracting deposits with better savings rates. However, it also brings increased risk, as higher borrowing costs can lead to higher default rates among less creditworthy borrowers. The current situation demands a careful balancing act for both sides of the financial equation, with a strong emphasis on managing debt wisely and strategically deploying capital.

Who is Affected by Changes in the Prime Rate?

The prime rate’s influence extends far beyond the financial institutions that set it, permeating every corner of the economy. From multinational corporations to individual households, changes in this benchmark rate can trigger significant financial adjustments. Its impact is multifaceted, affecting borrowing costs, investment returns, and overall economic behavior.

Businesses and Corporate Borrowers

Businesses, regardless of size, are acutely sensitive to prime rate fluctuations. Larger corporations often use lines of credit tied to the prime rate to manage their day-to-day operations, cover short-term cash flow needs, and finance working capital. When the prime rate rises, the cost of these essential financing tools increases, directly impacting their operational expenses and potentially reducing profit margins. This can force companies to reassess their inventory levels, accounts receivable management, and overall liquidity strategies.

For businesses contemplating expansion, new equipment purchases, or significant capital investments, a higher prime rate translates into more expensive loan financing. This increased cost of capital can lead to delayed projects, scaled-back ambitions, or even the abandonment of otherwise viable ventures, thereby slowing economic growth. Small businesses, in particular, are often more vulnerable to prime rate changes as they may have less access to diverse funding sources and tighter margins than larger enterprises. Their ability to secure affordable credit directly influences their capacity to grow, create jobs, and innovate. Conversely, a falling prime rate can stimulate business activity by reducing borrowing costs, encouraging investment, and freeing up capital for growth.

Individual Consumers

Perhaps no group feels the direct and immediate impact of prime rate changes more acutely than individual consumers, especially those carrying variable-rate debt.

- Adjustable-Rate Mortgages (ARMs) and Home Equity Lines of Credit (HELOCs): These loan products are often directly indexed to the prime rate plus a margin. When the prime rate rises, borrowers with ARMs typically see their monthly mortgage payments increase after the initial fixed-rate period. Similarly, HELOC payments, which are almost universally variable, will rise, adding a significant burden to household budgets. This can affect homeowners’ disposable income and their ability to spend on other goods and services.

- Credit Cards: The vast majority of credit cards in the U.S. have variable Annual Percentage Rates (APRs) that are tied to the prime rate. As the prime rate increases, so does the interest charged on credit card balances, making it more expensive to carry debt. This can lead to higher minimum payments and a longer time to pay off balances, further straining personal finances.

- Personal Loans and Student Loans: While many personal loans are fixed-rate, a significant portion of private student loans and some personal loans have variable rates linked to the prime rate. Borrowers with these loans will experience changes in their monthly payments in sync with prime rate movements.

On the other hand, a high prime rate environment can also incentivize consumers to save more, as deposit rates (for savings accounts and Certificates of Deposit) often track the prime rate, offering better returns than in a low-rate environment.

Savers and Investors

Changes in the prime rate also have substantial implications for savers and investors, influencing where they choose to allocate their capital.

- Savers: When the prime rate rises, banks typically offer higher interest rates on savings accounts, money market accounts, and Certificates of Deposit (CDs). This is a welcome development for savers, as their cash holdings can earn a more substantial return, helping to combat inflation and grow their wealth more effectively. Conversely, a low prime rate environment means meager returns on traditional savings, prompting savers to seek alternative investment avenues.

- Investors: The impact on investors is more complex. Higher prime rates generally lead to higher bond yields, making fixed-income investments more attractive. However, this can also negatively impact the stock market, as higher borrowing costs for companies can depress earnings, and higher bond yields provide a competitive alternative to equity investments. Investors might shift their portfolios from growth stocks to more value-oriented or dividend-paying stocks, or increase their allocation to bonds and cash. Real estate investors, particularly those relying on financing, will face higher costs, potentially affecting property values and rental yields. Understanding the prime rate’s trajectory is crucial for making informed decisions about asset allocation and portfolio strategy.

Strategies for Navigating a Dynamic Prime Rate Environment

Given the pervasive influence of the prime rate, developing proactive strategies is essential for individuals and businesses alike. A dynamic prime rate environment, characterized by fluctuating interest rates, demands thoughtful financial planning and adaptable approaches to both borrowing and saving.

For Borrowers

In an environment where the prime rate can shift, borrowers must be particularly vigilant and strategic:

- Understand Loan Terms (Fixed vs. Variable): The first step is to thoroughly understand the terms of existing and new loans. For variable-rate debts like credit cards, HELOCs, and ARMs, recognize that payments will change with the prime rate. If rates are rising, consider locking in a fixed rate where possible, especially for larger debts like mortgages, to gain payment predictability. This might involve refinancing an ARM into a fixed-rate mortgage or consolidating credit card debt into a fixed-rate personal loan.

- Refinancing Opportunities: When the prime rate is on a downward trend, refinancing can be a powerful tool. Continuously monitor market rates for mortgages and other significant loans. Even a small reduction in interest rates can lead to substantial savings over the life of a loan. However, always factor in closing costs and fees when evaluating whether refinancing is truly beneficial.

- Manage Credit Card Debt Effectively: With credit card APRs often tied directly to the prime rate, rising rates make carrying a balance significantly more expensive. Prioritize paying down high-interest credit card debt aggressively. Consider strategies like the “debt snowball” or “debt avalanche” methods, or explore balance transfer cards with introductory 0% APRs (but be mindful of transfer fees and the expiry of the introductory period).

- Build an Emergency Fund: A robust emergency fund, ideally covering 3-6 months of living expenses, becomes even more critical in a rising interest rate environment. It provides a buffer against unexpected expenses or income disruptions, reducing the need to take on high-interest debt when borrowing costs are elevated.

For Savers and Investors

While higher rates can be challenging for borrowers, they often present opportunities for savers and investors:

- Maximizing Returns on Savings: In a high prime rate environment, cash is no longer trash. Explore high-yield savings accounts, money market accounts, and Certificates of Deposit (CDs) offered by banks and credit unions. These accounts often offer significantly better returns than traditional checking or low-yield savings accounts. Compare rates from different institutions to ensure you are getting the best possible return on your liquid cash. Laddering CDs (investing in CDs with staggered maturity dates) can be a strategy to both capture higher rates and maintain liquidity.

- Considering Fixed-Income Investments: Higher prime rates typically lead to higher yields on bonds and other fixed-income securities. This can make government bonds, corporate bonds, and bond funds more attractive for investors seeking stable income and capital preservation. However, it’s important to remember that bond prices move inversely to interest rates; as rates rise, existing bond prices tend to fall. For long-term investors, staggered investments in fixed income can help average out returns.

- Diversification Strategies: A dynamic interest rate environment underscores the importance of a well-diversified investment portfolio. Don’t put all your eggs in one basket. Diversify across different asset classes (stocks, bonds, real estate, commodities) and within asset classes (e.g., different sectors, market caps, and geographies for stocks). This helps cushion the impact of rate changes on any single part of your portfolio.

- Consulting with Financial Advisors: Given the complexity of navigating interest rate cycles, particularly for long-term financial planning, consulting with a qualified financial advisor is highly recommended. An advisor can help assess your individual financial situation, risk tolerance, and goals, and then tailor a strategy that aligns with the prevailing economic conditions and potential future prime rate movements. They can provide insights into tax implications, retirement planning, and investment adjustments that you might overlook.

Conclusion

The prime rate is far more than an obscure financial term; it is a fundamental pillar of the global economy, acting as a direct reflection of monetary policy and broader economic health. Understanding “what is prime rate right now” provides crucial insights into the current cost of borrowing for businesses and individuals, the potential returns for savers, and the overall direction of the economic winds. Its close relationship with central bank actions, driven by factors like inflation and employment, underscores its role as a powerful tool for economic management.

For businesses, the prime rate dictates the cost of capital, influencing everything from daily operations to long-term expansion plans. For individual consumers, it directly impacts the affordability of mortgages, credit card debt, and personal loans, shaping household budgets and spending power. And for savers and investors, it helps determine the attractiveness of various financial instruments, guiding decisions on where to park capital for growth or income.

In an ever-evolving financial landscape, staying informed about the prime rate and its trajectory is not just beneficial but imperative. By proactively adapting financial strategies—whether through debt management, strategic saving, or diversified investing—individuals and businesses can better navigate the challenges and capitalize on the opportunities presented by a dynamic interest rate environment. The prime rate serves as a constant reminder that prudent financial planning, informed by a keen awareness of economic indicators, is the cornerstone of lasting financial well-being.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.