Purchasing a home is often the largest financial commitment an individual or family will make in their lifetime. For most, this monumental step is facilitated by a mortgage loan – a complex yet essential financial product that allows aspiring homeowners to finance their dreams. Navigating the world of mortgages can seem daunting, filled with unfamiliar terminology, rigorous requirements, and a labyrinth of options. However, with a clear understanding of the process, meticulous preparation, and strategic decision-making, obtaining a mortgage loan becomes an achievable and even empowering journey.

This comprehensive guide aims to demystify the mortgage loan process, providing you with the insights and tools needed to confidently secure the financing for your future home. From understanding the basics of lending to navigating the closing table, we’ll break down each critical step, empowering you to make informed decisions and achieve homeownership.

Understanding the Mortgage Landscape

Before embarking on the application process, it’s crucial to grasp the fundamental concepts of mortgages, the various types available, and the key players involved. This foundational knowledge will serve as your compass through the often intricate financial terrain.

What is a Mortgage and Why is it Important?

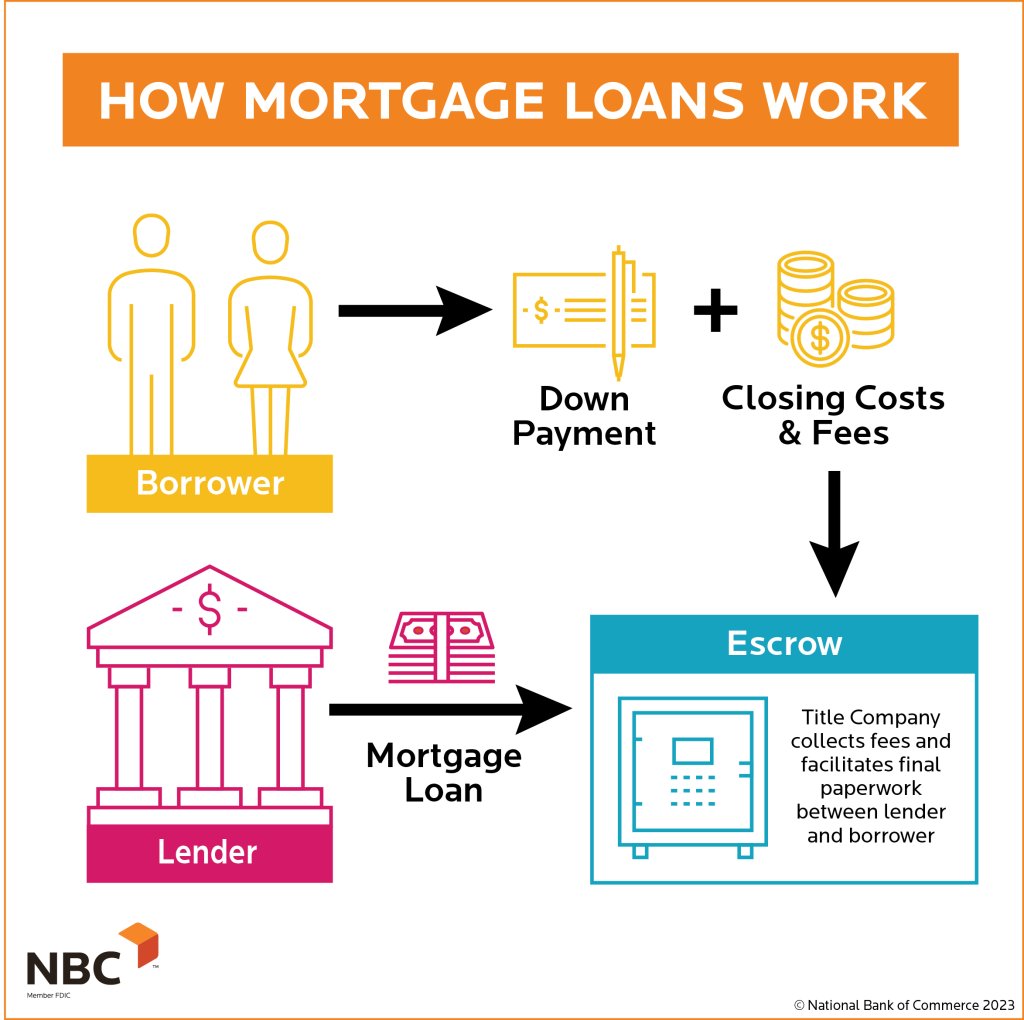

At its core, a mortgage is a loan specifically used to purchase real estate. It’s a secured loan, meaning the property itself serves as collateral. If the borrower defaults on the loan, the lender has the right to repossess the property through a process called foreclosure. In exchange for the loan, you, the borrower, agree to repay the principal amount plus interest over a predetermined period, typically 15 or 30 years, through regular monthly payments.

Mortgages are important because they make homeownership accessible to a vast majority of the population who might not have the upfront capital to buy a property outright. They bridge the gap between aspirational homeownership and financial reality, enabling individuals to build equity, benefit from potential property appreciation, and enjoy the stability and personal satisfaction of owning their own home.

Types of Mortgage Loans

The mortgage market offers a variety of loan products, each designed to cater to different financial situations and needs. Understanding these distinctions is vital for choosing the loan that best suits you.

- Conventional Loans: These are not insured or guaranteed by the government. They are often backed by private lenders and require borrowers to meet specific credit and financial criteria set by government-sponsored enterprises like Fannie Mae and Freddie Mac. If your down payment is less than 20%, you’ll typically be required to pay Private Mortgage Insurance (PMI).

- Fixed-Rate Mortgages (FRM): With a fixed-rate mortgage, the interest rate remains constant for the entire duration of the loan. This provides stability and predictability in monthly payments, making budgeting easier and protecting borrowers from potential interest rate hikes.

- Adjustable-Rate Mortgages (ARM): ARMs feature an interest rate that can change periodically after an initial fixed-rate period (e.g., 5/1 ARM means fixed for 5 years, then adjusts annually). While ARMs often start with lower interest rates than FRMs, the variability introduces a risk of increased monthly payments if rates rise. They can be attractive for those planning to sell or refinance before the adjustable period begins.

- Government-Insured Loans:

- FHA Loans: Insured by the Federal Housing Administration, these loans are popular with first-time homebuyers or those with less-than-perfect credit and lower down payments (as low as 3.5%). They have specific property requirements and require Mortgage Insurance Premiums (MIP) for the life of the loan or until specific conditions are met.

- VA Loans: Guaranteed by the U.S. Department of Veterans Affairs, VA loans offer exceptional benefits to eligible service members, veterans, and surviving spouses, including no down payment requirement and no private mortgage insurance.

- USDA Loans: Backed by the U.S. Department of Agriculture, these loans aim to promote homeownership in rural and suburban areas. They offer 100% financing for eligible low- to moderate-income borrowers who purchase homes in designated rural areas.

Key Players in the Mortgage Process

Navigating a mortgage involves interacting with several professionals, each playing a critical role.

- Lenders: These are the financial institutions (banks, credit unions, online lenders) that originate and fund mortgage loans. They set the terms, rates, and approval criteria.

- Mortgage Brokers: Brokers act as intermediaries between borrowers and multiple lenders. They can shop around for different loan products and rates on your behalf, often simplifying the comparison process. They earn a commission from either the borrower or the lender (or both).

- Loan Officers: These are representatives of a specific lender, guiding you through their institution’s loan products, application process, and requirements.

- Underwriters: These professionals evaluate your loan application, assessing your creditworthiness, income, assets, and the property’s value to determine if you qualify for the loan and at what terms.

- Appraisers: Licensed professionals who provide an objective estimate of a property’s market value. This ensures the loan amount is justified by the property’s worth.

- Title Company/Escrow Officer: They ensure a clear title to the property, handle the transfer of funds, and manage all necessary documents at closing.

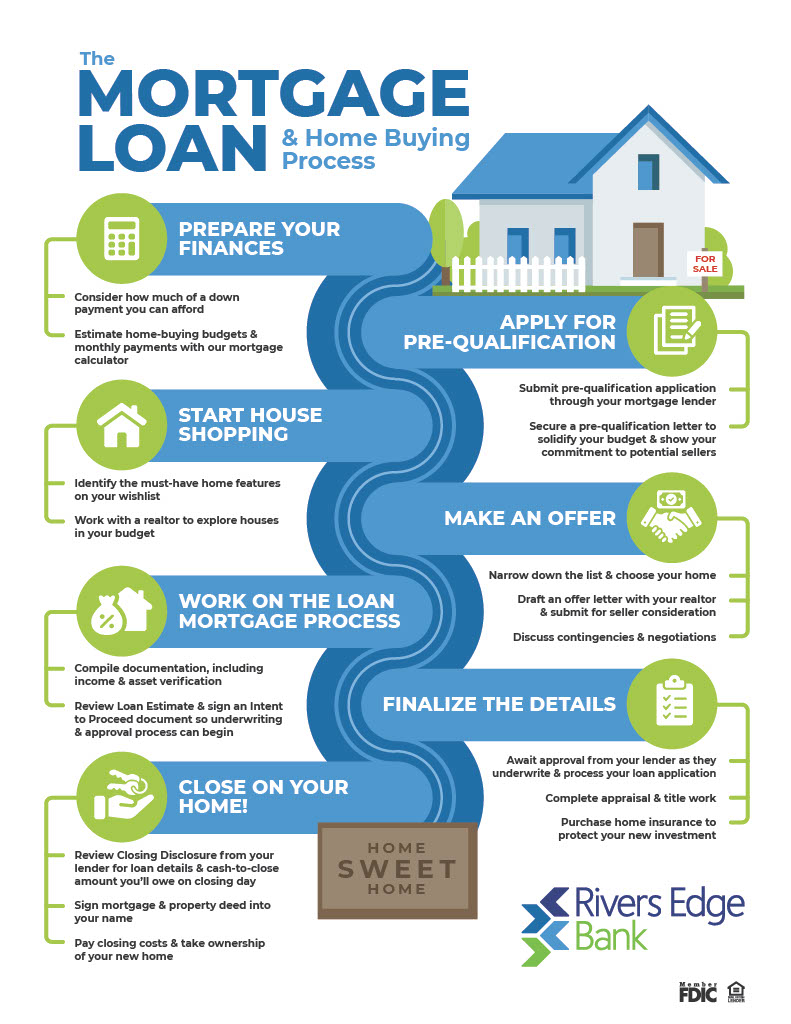

Preparing for Mortgage Application Success

The key to a smooth and successful mortgage application lies in thorough preparation. Lenders scrutinize your financial history and current standing to assess your ability to repay the loan. Being well-prepared significantly increases your chances of approval and securing favorable terms.

Assessing Your Financial Health

Before even speaking to a lender, take an honest look at your financial situation. This self-assessment will help you understand your strengths and weaknesses from a lender’s perspective.

- Credit Score: Your credit score (e.g., FICO score) is paramount. It’s a numerical representation of your creditworthiness, reflecting your payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders typically look for scores in the mid-600s for FHA loans, and often 700+ for the best conventional rates. Obtain your credit reports from all three major bureaus (Equifax, Experian, TransUnion) and dispute any errors. Start improving your score by paying bills on time, reducing debt, and avoiding new credit inquiries.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments (including the proposed mortgage payment, credit cards, car loans, student loans) to your gross monthly income. Lenders typically prefer a DTI ratio of 43% or lower, though some programs allow higher. A lower DTI indicates you have more disposable income to manage your mortgage payments.

- Savings and Down Payment: The more you can put down as a down payment, the better. A larger down payment reduces the loan amount, decreases your monthly payments, and can help you avoid PMI on conventional loans (with 20% down). Lenders also want to see that you have cash reserves (liquid savings) to cover several months of mortgage payments after closing, demonstrating financial stability.

- Employment Stability: Lenders prefer borrowers with a stable employment history, typically two years or more in the same job or industry. Consistent income demonstrates your ability to make regular payments.

Gathering Essential Documentation

Once you’ve assessed your financial health, begin compiling the documents lenders will inevitably request. Having these ready will streamline the application process.

- Income Verification:

- Pay stubs (most recent 30-60 days)

- W-2 forms (past two years)

- Tax returns (past two years, especially if self-employed or with complex income)

- Proof of other income (alimony, child support, social security, pension statements)

- Asset Verification:

- Bank statements (checking and savings accounts, past 60 days to 3 months)

- Investment account statements (brokerage, retirement accounts)

- Gift letters (if a portion of your down payment is a gift from a relative)

- Employment Verification:

- Employer contact information for verification

- Letters of explanation for any employment gaps

- Credit History:

- Statements for all existing debts (credit cards, student loans, auto loans)

- Explanation letters for any derogatory credit events (e.g., bankruptcies, foreclosures, late payments)

Getting Pre-Approved vs. Pre-Qualified

These terms are often used interchangeably, but there’s a significant difference.

- Pre-Qualification: This is an informal estimate of how much you might be able to borrow based on a brief review of your finances (often self-reported) without verifying documents or pulling a hard credit check. It’s a good starting point for understanding affordability but holds little weight with sellers.

- Pre-Approval: This is a much more thorough process. A lender will review your financial documents, pull a hard credit report, and verify your income and assets. If approved, you’ll receive a pre-approval letter stating the maximum loan amount you qualify for. This letter shows sellers you’re a serious and qualified buyer, giving you a competitive edge in a hot housing market. Always opt for pre-approval before seriously house hunting.

Navigating the Application and Approval Process

With your financial house in order and a pre-approval in hand, you’re ready to dive into the core of the mortgage journey: selecting a lender, formally applying, and moving through the underwriting phase.

Shopping for the Best Rates and Terms

Do not settle for the first offer you receive. Mortgage rates and terms can vary significantly between lenders, impacting your monthly payments and the total cost of your loan over its lifetime.

- Compare Lenders: Research at least 3-5 different lenders, including national banks, local credit unions, and online mortgage providers. Look beyond just the interest rate; compare closing costs, lender fees (origination fees, application fees), and customer service reviews.

- Understand the Loan Estimate: Once you apply, lenders are required to provide a Loan Estimate form within three business days. This standardized document clearly outlines the interest rate, monthly payments, estimated closing costs, and other loan terms. Use it to compare offers side-by-side. Pay close attention to the “Cash to Close” section and the “Comparisons” section, which details projected payments and costs.

- Negotiate: Don’t be afraid to negotiate. If you receive a better offer from one lender, see if another is willing to match or beat it. Timing is key; aim to gather all your Loan Estimates within a 14-45 day window to minimize the impact of multiple credit inquiries on your credit score.

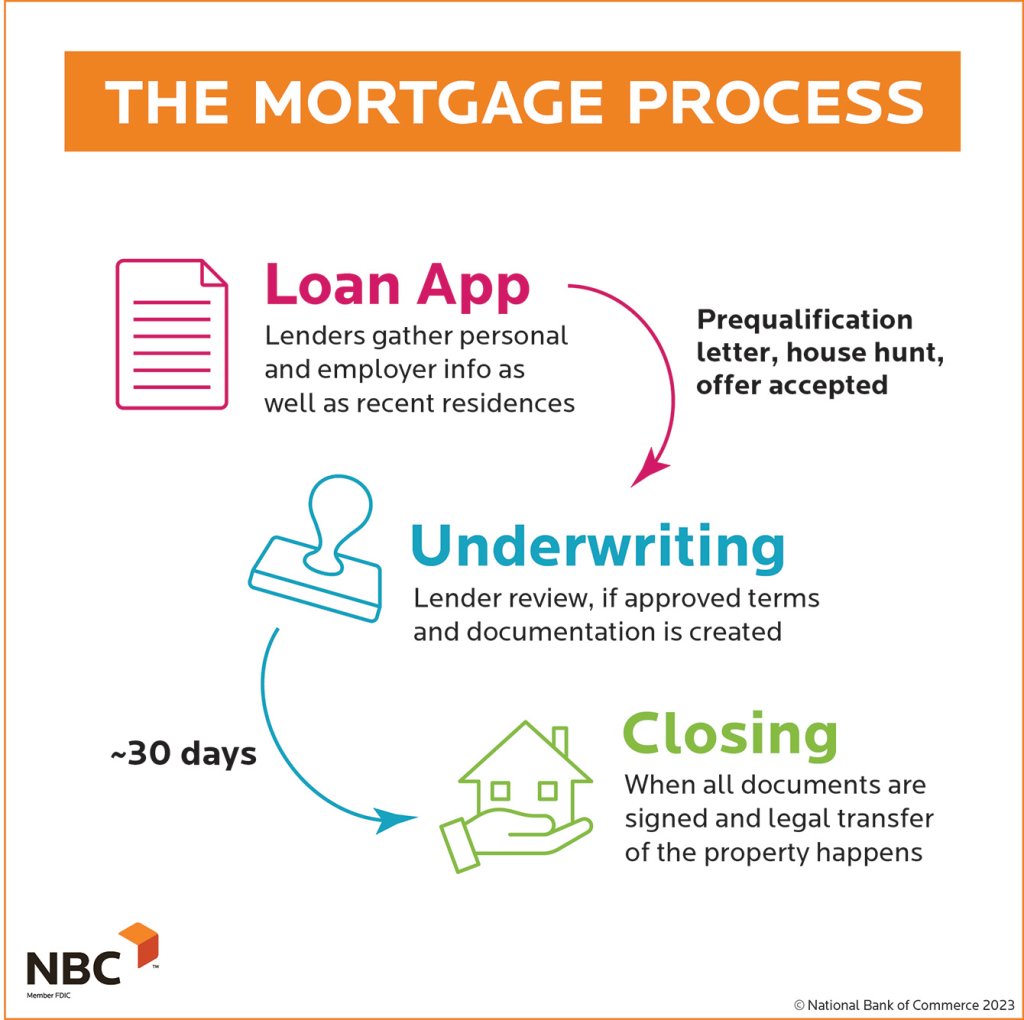

Submitting Your Application and Underwriting

Once you’ve chosen a lender, you’ll submit your formal mortgage application. This involves providing all the documentation you’ve meticulously gathered.

- Formal Application: You’ll fill out a detailed application (often online) and upload or provide all requested documents. Your loan officer will then submit your complete package to the underwriting department.

- Underwriting: This is the most critical phase where the lender thoroughly verifies all the information you’ve provided. Underwriters meticulously review your credit history, income, assets, employment stability, and the property’s value to assess the risk involved. They may request additional documents or clarifications (e.g., “conditions” for approval). Be responsive and provide requested information promptly to avoid delays.

- Conditional Approval: If the underwriter finds everything in order, you’ll receive a conditional approval, meaning your loan is approved pending the satisfaction of certain conditions (e.g., a satisfactory appraisal, clear title report, final employment verification).

The Importance of a Home Appraisal and Inspection

Parallel to the underwriting process, two vital assessments of the property itself will take place.

- Home Appraisal: The lender will order an appraisal to determine the fair market value of the property. This protects the lender by ensuring the loan amount does not exceed the home’s value. If the appraisal comes in lower than the agreed-upon purchase price, it can necessitate renegotiation with the seller, you making up the difference in cash, or even rescinding the offer.

- Home Inspection: While not mandatory for the loan itself, a home inspection is highly recommended for your protection. A professional inspector will thoroughly examine the property for any structural issues, maintenance problems, or potential hazards. This helps you understand the condition of the home you’re buying and can uncover costly repairs before closing. Depending on your purchase agreement, you may be able to negotiate repairs or a price reduction based on inspection findings.

Closing the Deal and Beyond

The closing is the culmination of your efforts, where ownership of the home is officially transferred. However, the responsibilities of homeownership extend well beyond signing the final papers.

Understanding the Closing Process and Costs

“Closing” is the legal process where the property title is transferred from the seller to the buyer, and the loan documents are signed.

- Closing Disclosure (CD): At least three business days before closing, you’ll receive a Closing Disclosure from your lender. This document provides a final, detailed breakdown of all loan terms, fees, and costs associated with the transaction. Compare it carefully with your initial Loan Estimate to ensure no unexpected changes.

- Closing Costs: These are fees and expenses incurred during the home buying and selling process, typically ranging from 2% to 5% of the loan amount. They include lender fees (origination, underwriting), third-party fees (appraisal, title insurance, attorney fees), prepaid items (property taxes, homeowner’s insurance premiums), and escrow fees. Be prepared for these upfront costs.

What to Expect at Closing

Closing day typically involves signing a significant stack of legal documents. You’ll sign the promissory note (your promise to repay the loan), the mortgage or deed of trust (pledging the property as collateral), and various disclosures. You’ll also need to bring a cashier’s check or arrange for a wire transfer for your down payment and closing costs, minus any earnest money already paid. The title company or escrow officer will facilitate the signing and ensure all funds are properly disbursed.

Post-Closing Responsibilities and Mortgage Management

Once you’ve received the keys, your journey as a homeowner begins.

- First Mortgage Payment: Understand when your first mortgage payment is due. It often falls within 30-60 days after closing.

- Escrow Account: Many mortgages include an escrow account for property taxes and homeowner’s insurance premiums. A portion of your monthly payment goes into this account, and the lender pays these bills on your behalf when they are due.

- Mortgage Servicer: Your lender may sell your loan to a mortgage servicer. This company will be your primary contact for all payment-related inquiries, statements, and escrow management. Understand who your servicer is and how to contact them.

- Refinancing: As interest rates change or your financial situation evolves, you may consider refinancing your mortgage to obtain a lower rate, change loan terms, or tap into your home equity.

Common Pitfalls and Expert Tips

While the mortgage process is well-defined, certain missteps can derail your application or lead to less favorable outcomes. Being aware of these and following expert advice can save you time, money, and stress.

Avoiding Common Mortgage Mistakes

- Making New Major Purchases: Avoid buying a new car, furniture on credit, or opening new credit cards between pre-approval and closing. This can significantly alter your DTI ratio and credit score, potentially jeopardizing your loan approval.

- Changing Jobs: A sudden job change, especially to a different industry or a lower-paying role, can raise red flags for underwriters and delay or even cancel your loan.

- Ignoring Your Credit Report: Don’t wait until the last minute to check your credit. Errors can take time to correct.

- Not Comparing Lenders: Settling for the first offer without shopping around can cost you thousands over the life of the loan.

- Failing to Understand All Costs: Be prepared for closing costs and other expenses beyond just the down payment.

Tips for First-Time Homebuyers

- Start Early: Begin saving for a down payment and improving your credit score well in advance of your desired purchase date.

- Utilize First-Time Homebuyer Programs: Many states and local governments offer special programs, grants, or tax credits specifically for first-time buyers. Research these opportunities.

- Don’t Overextend Yourself: Just because a lender approves you for a certain amount doesn’t mean you should borrow that much. Create a realistic budget, including maintenance and utility costs, and stick to it.

- Build a Strong Support Team: Work with a trusted real estate agent, mortgage loan officer, and potentially a financial advisor.

The Role of a Financial Advisor

While a loan officer guides you through the mortgage application, a financial advisor offers a broader perspective on your overall financial health. They can help you:

- Determine True Affordability: Beyond the lender’s limits, an advisor can help you understand how a mortgage fits into your long-term financial goals, savings plans, and retirement strategy.

- Optimize Down Payment Strategy: Advise on whether to put down more to avoid PMI or save cash for other investments.

- Plan for Closing Costs and Reserves: Help integrate these significant expenses into your overall financial plan.

- Evaluate Refinancing Opportunities: Provide objective advice on when refinancing makes financial sense.

Obtaining a mortgage loan is a significant financial undertaking, but it is also a gateway to achieving the dream of homeownership. By understanding the process, preparing diligently, and making informed decisions at each stage, you can confidently navigate the complexities and secure the right loan that paves the way for your future home. Remember, patience, persistence, and proactive communication with your mortgage team are your greatest assets on this rewarding journey.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.