The dream of homeownership is a cornerstone of financial aspiration for many, representing stability, a place to build equity, and a personal sanctuary. However, transforming this dream into reality often hinges on securing a home loan – a significant financial undertaking that can feel daunting without proper guidance. Navigating the complex world of mortgage applications, interest rates, and financial jargon requires preparation, insight, and a clear understanding of the process. This comprehensive guide will demystify how to get a home loan, equipping you with the knowledge and confidence to embark on this pivotal financial journey.

Laying the Foundation: Pre-Application Essentials

Before you even begin looking at properties or speaking with lenders, the most critical step is to meticulously assess and strengthen your financial foundation. This preparatory phase is not merely about ticking boxes; it’s about positioning yourself as an attractive borrower and ensuring you secure the best possible terms for your mortgage.

Understanding Your Financial Health

Lenders evaluate your financial health through several key metrics to gauge your reliability as a borrower. Your proactive understanding and improvement of these areas can significantly impact your loan eligibility and interest rates.

- Credit Score: Your credit score is a numerical representation of your creditworthiness, primarily influenced by your payment history, amounts owed, length of credit history, new credit, and credit mix. Lenders use this score (typically FICO or VantageScore) to determine your risk profile. A higher score, generally above 740, unlocks lower interest rates and more favorable loan terms. It’s crucial to obtain your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) well in advance to dispute any errors and understand your standing.

- Debt-to-Income Ratio (DTI): Your DTI is a critical metric that compares your total monthly debt payments to your gross monthly income. Lenders typically prefer a DTI of 36% or lower, though some programs may allow up to 43% or even 50% in certain circumstances. A lower DTI indicates that you have sufficient disposable income to manage your mortgage payments alongside existing obligations. To calculate it, sum all your monthly debt payments (car loans, student loans, credit card minimums, etc.) and divide by your gross monthly income. Reducing debt before applying can significantly improve your DTI.

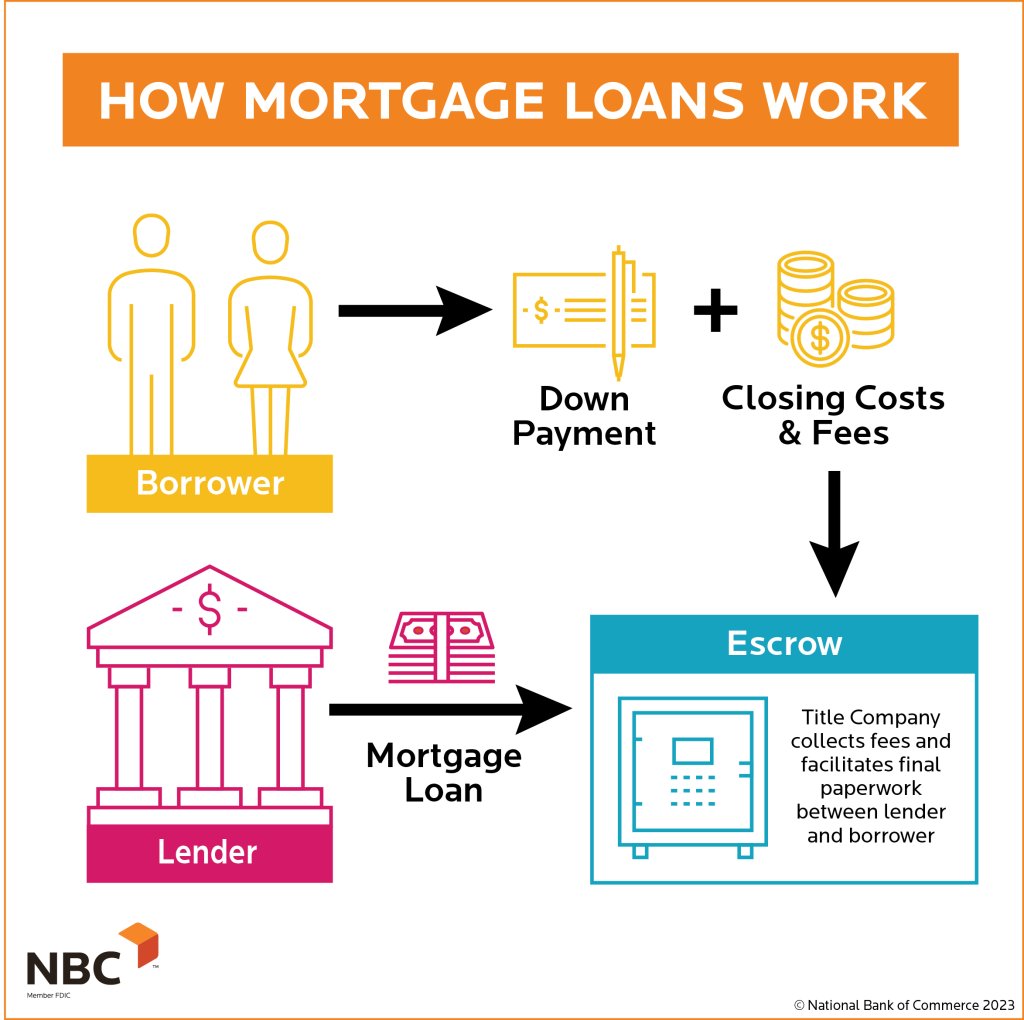

- Savings for Down Payment & Closing Costs: These are two distinct but equally vital components of upfront capital. A down payment is a percentage of the home’s purchase price paid upfront, reducing the amount you need to borrow. While 20% is often recommended for conventional loans to avoid Private Mortgage Insurance (PMI), many programs allow for much lower down payments (e.g., 3-5% for conventional, 3.5% for FHA, 0% for VA/USDA). Closing costs are additional fees charged by lenders and third parties for services related to the loan and property transfer. These typically range from 2% to 5% of the loan amount and include items like appraisal fees, title insurance, legal fees, and origination fees. Having these funds readily available in a secure, verifiable account is essential.

Budgeting and Affordability Assessment

Beyond just qualifying for a loan, it’s paramount to determine what you can truly afford without straining your finances. Homeownership entails more than just a mortgage payment.

- What Can You Truly Afford? Your mortgage payment will likely include principal and interest (P&I), property taxes (T), and homeowner’s insurance (I) – often referred to as PITI. However, you must also factor in potential Homeowner’s Association (HOA) fees, utility costs (which can be higher in a larger home), and an emergency fund for unexpected repairs and maintenance. Create a realistic monthly budget that accounts for all these potential expenses, ensuring your housing costs don’t consume an unmanageable portion of your income.

- Pre-qualification vs. Pre-approval: Understanding the difference between these two initial steps is crucial. Pre-qualification is a quick, informal assessment based on self-reported financial information, giving you an estimate of how much you might be able to borrow. It’s a useful starting point but carries little weight with sellers. Pre-approval, on the other hand, involves a more rigorous review of your actual financial documents, including a credit check. It results in a conditional commitment from a lender for a specific loan amount and provides a strong signal to sellers that you are a serious and qualified buyer. Always aim for a pre-approval before actively house hunting.

Gathering Your Documents

The home loan application process is document-intensive. Being organized and having your paperwork ready beforehand will streamline the entire procedure. Expect to provide:

- Income Verification: Recent pay stubs (30-60 days), W-2 forms (past two years), and federal tax returns (past two years). If self-employed, profit and loss statements and two years of business and personal tax returns are standard.

- Asset Verification: Bank statements (past two-three months) for checking, savings, and investment accounts to show your down payment and reserve funds.

- Credit History Reports: While lenders pull these, it’s wise to review yours beforehand for accuracy.

- Identification: Government-issued photo ID (driver’s license, passport).

Navigating the Loan Landscape: Types and Lenders

With your financial house in order, the next step involves understanding the diverse range of mortgage products available and identifying the right financial institution to partner with. The choice of loan type and lender can significantly impact your monthly payments, upfront costs, and long-term financial commitments.

Exploring Different Loan Types

The mortgage market offers a variety of loan products, each designed to cater to different financial situations and borrower profiles.

- Conventional Loans: These are the most common type of mortgages, not insured or guaranteed by a government agency. They generally require a good credit score and a DTI within traditional limits. While a 20% down payment is ideal to avoid Private Mortgage Insurance (PMI), many conventional loans allow for as little as 3% down, though PMI will be required. They come in both fixed-rate and adjustable-rate varieties.

- FHA Loans: Insured by the Federal Housing Administration (FHA), these loans are popular for first-time homebuyers or those with lower credit scores. They offer more lenient credit requirements and allow down payments as low as 3.5%. However, they require both an upfront mortgage insurance premium (UFMIP) and annual mortgage insurance premiums (MIP), which generally cannot be canceled.

- VA Loans: Backed by the U.S. Department of Veterans Affairs (VA), these loans offer incredible benefits to eligible service members, veterans, and surviving spouses. Key advantages include no down payment requirement, no private mortgage insurance, and competitive interest rates. There is a VA funding fee, but it can often be financed into the loan.

- USDA Loans: Guaranteed by the U.S. Department of Agriculture (USDA), these loans are designed to help low- and moderate-income individuals purchase homes in eligible rural and suburban areas. They often require no down payment and offer favorable terms, but income and property location restrictions apply.

- Jumbo Loans: For properties that exceed the conventional loan limits set by the Federal Housing Finance Agency (FHFA), jumbo loans are necessary. They typically come with stricter underwriting requirements, higher credit score demands, and larger reserve requirements due to the higher loan amounts involved.

- Adjustable-Rate Mortgages (ARMs) vs. Fixed-Rate Mortgages: A fixed-rate mortgage maintains the same interest rate for the entire life of the loan, offering predictability in monthly payments. An adjustable-rate mortgage (ARM) starts with a fixed interest rate for an initial period (e.g., 3, 5, 7, or 10 years), after which the rate adjusts periodically based on market indexes. ARMs can offer lower initial payments but carry the risk of increased payments if rates rise.

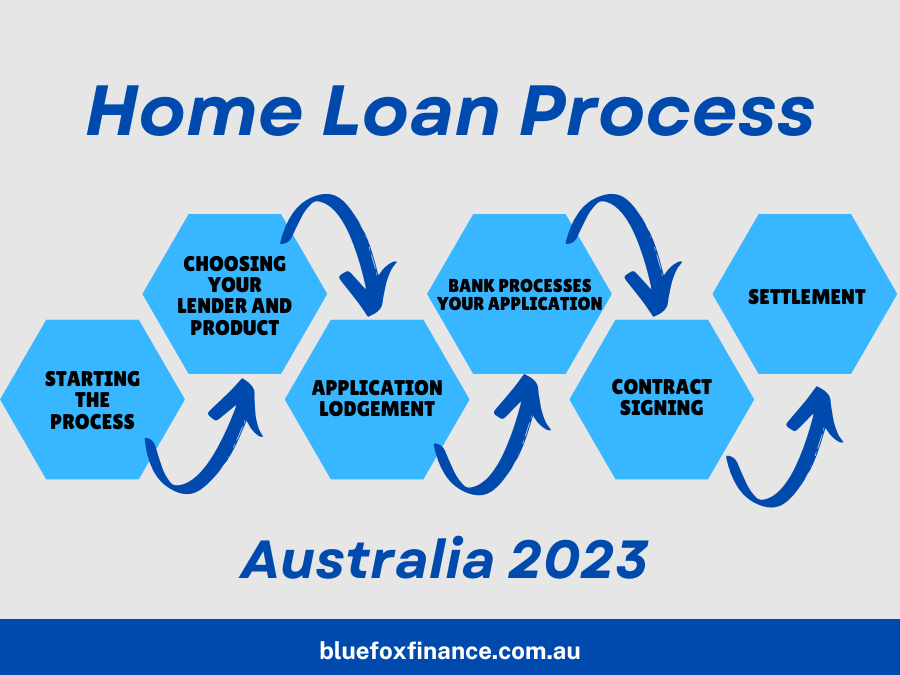

Choosing the Right Lender

The institution you choose to provide your mortgage can significantly impact your experience. It’s wise to shop around and compare offers from multiple lenders.

- Banks (National and Local): Large national banks often offer a wide range of products and convenient online services. Local banks and community banks may provide a more personalized experience and potentially more flexibility.

- Credit Unions: These member-owned financial cooperatives often offer competitive rates and lower fees due to their non-profit status. Membership requirements vary but are typically easy to meet.

- Mortgage Brokers: A mortgage broker acts as an intermediary, working with multiple lenders to find the best loan products and rates for your specific situation. They can save you time and potentially money by comparing offers, but they charge a fee, which can be paid by you or the lender.

- Online Lenders: These lenders operate entirely digitally, often streamlining the application process and sometimes offering highly competitive rates due to lower overheads. However, the personalized service might be less extensive than with traditional brick-and-mortar institutions.

- Factors to Consider: When evaluating lenders, look beyond just the interest rate. Consider all fees (origination fees, application fees, discount points), the lender’s responsiveness and customer service, their reputation, and their willingness to answer your questions thoroughly. Getting a Loan Estimate from multiple lenders is crucial for a direct comparison of costs.

The Application and Underwriting Process

Once you’ve been pre-approved and found a home, the real work of securing your loan begins. This phase involves a detailed examination of your finances and the property’s value to ensure the lender’s investment is sound.

Submitting Your Application

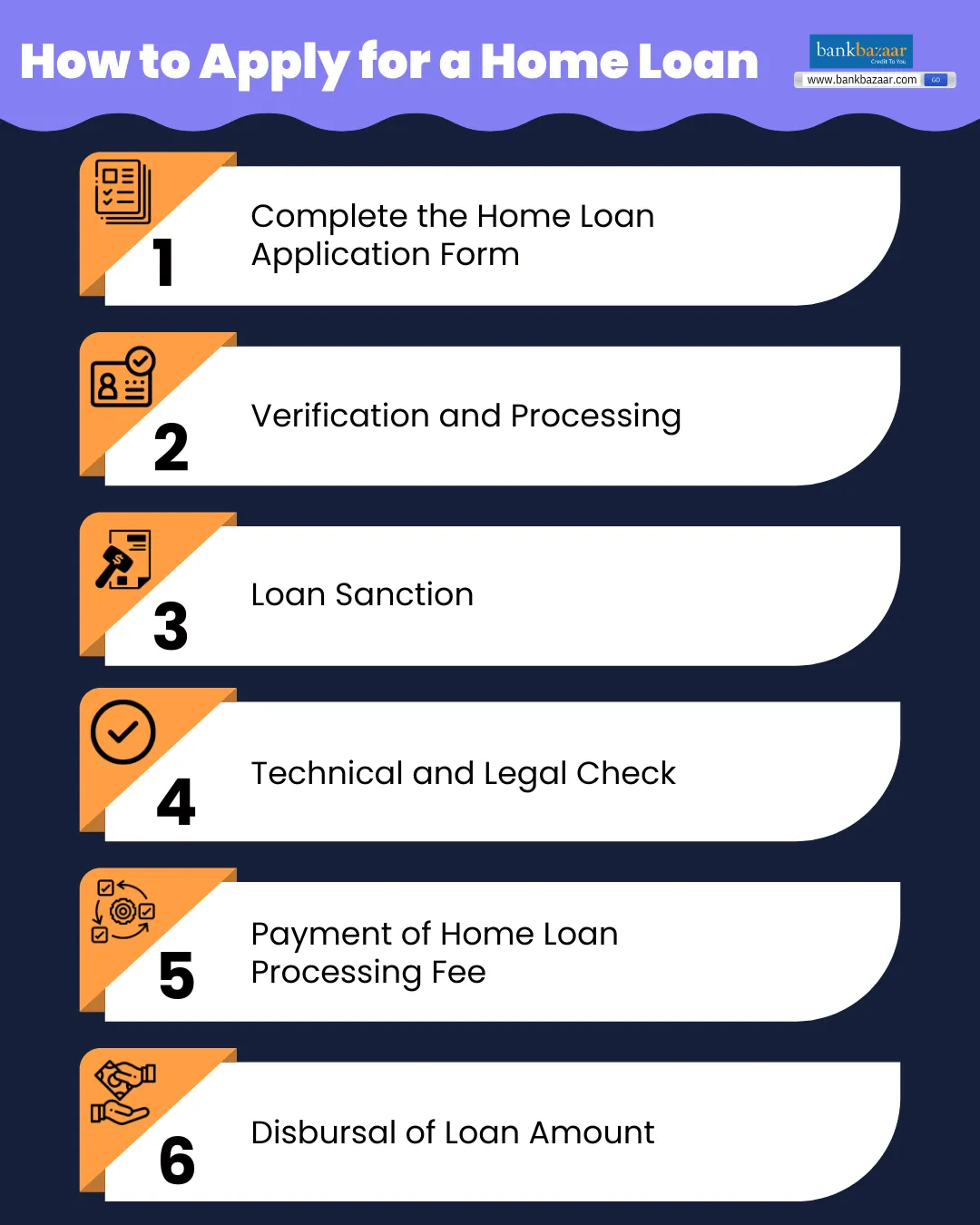

With a chosen home and a pre-approved lender, you’ll formally submit your full loan application.

- The Formal Application Form: This comprehensive document will reiterate your personal and financial information, the details of the property you intend to purchase, and your desired loan terms. Be prepared to provide all the documents you gathered in the pre-application phase.

- Disclosure Forms: You will receive a stack of disclosures outlining the terms, conditions, and risks associated with your loan. It’s imperative to read these carefully and understand what you are signing.

- Locking in Your Interest Rate: After your offer on a home is accepted, you’ll typically have the option to “lock in” your interest rate. This guarantees that your rate won’t change between the time you lock it and the closing date, usually for a period of 30 to 60 days. This protects you from market fluctuations, but be aware of lock-in fees and expiration dates.

Underwriting: The Deep Dive

Underwriting is the lender’s meticulous process of verifying all the information in your application and assessing the risk of lending to you.

- Lender’s Review of All Submitted Documents: The underwriter will pore over every piece of documentation you’ve provided – income, assets, credit reports, employment history – to ensure consistency and accuracy. They are looking for red flags or discrepancies.

- Verifying Income, Assets, Employment, Credit: Expect your employer to be contacted to verify your employment status and salary. Your bank accounts might be reviewed again to ensure no large, unexplained deposits or withdrawals have occurred. Your credit report will be pulled one last time before closing.

- Appraisal: Determining the Home’s Value: The lender will order an independent appraisal of the property to determine its fair market value. This is crucial because the loan amount cannot exceed the appraised value (or the purchase price, whichever is lower). If the appraisal comes in lower than the agreed-upon purchase price, it can cause complications, requiring negotiation with the seller or a larger down payment from you.

- Title Search: Ensuring Clear Ownership: A title company will conduct a thorough search of public records to ensure that the seller has the legal right to sell the property and that there are no liens, encumbrances, or disputes on the title that could affect your ownership. Title insurance is usually required to protect both the lender and you against future claims.

- Potential for Additional Document Requests: It’s common for underwriters to request additional information or clarification during this phase. Respond promptly to avoid delays.

Loan Approval and Conditions

At the end of the underwriting process, your loan will either be approved, denied, or approved with conditions.

- Conditional Approval vs. Full Approval: A conditional approval means the lender is willing to finance your home purchase, provided certain conditions are met. These might include selling your current home, providing additional documentation, or satisfying specific repair requirements on the property. A full approval means all conditions have been satisfied, and the loan is ready to close.

- Clearing Conditions Before Closing: Work diligently with your loan officer to promptly address and clear any outstanding conditions. Delays in providing requested information can push back your closing date.

Closing the Deal: From Approval to Keys

The final stage of the home loan process is the closing, often referred to as settlement. This is where all parties involved finalize the transaction, funds are exchanged, and ownership officially transfers.

The Closing Disclosure (CD)

Three business days before your scheduled closing date, you will receive a mandatory document called the Closing Disclosure (CD). This is a critical document that you must review meticulously.

- Understanding the Final Loan Terms, Fees, and Costs: The CD itemizes all final loan terms, including the interest rate, monthly payment, and a comprehensive breakdown of all closing costs, credits, and prepaid items.

- Comparison with Loan Estimate: Crucially, compare the CD with the Loan Estimate (LE) you received earlier in the process. While some minor fluctuations are normal, significant discrepancies should be questioned immediately with your lender or real estate agent. The CD provides a final, legally binding statement of all costs.

- Your Right to Review it Several Days Before Closing: The three-day review period is mandated by law to give you ample time to understand all aspects of the transaction and ask any clarifying questions before signing. Do not rush this step.

What Happens at Closing

The closing appointment is typically held at the office of a title company, attorney, or escrow agent.

- Signing Stacks of Documents: You will sign numerous legal documents, including the promissory note (your promise to repay the loan), the mortgage or deed of trust (which pledges the home as collateral), and various disclosures and agreements.

- Transferring Funds (Down Payment, Closing Costs): You will be required to provide a certified check or wire transfer for your down payment and any remaining closing costs not covered by the loan. Ensure these funds are accessible and properly transferred as instructed.

- The Role of the Closing Agent/Attorney: The closing agent (or attorney, depending on your state) facilitates the process, ensures all documents are correctly executed, collects and disburses funds, and records the new deed and mortgage with the local government. They act as a neutral third party to ensure a smooth and legal transfer of ownership.

- Receiving the Keys! Once all documents are signed, funds are disbursed, and the transaction is recorded, you will officially receive the keys to your new home. This is the culmination of your efforts.

Post-Closing Responsibilities

Homeownership doesn’t end at closing; it begins. You’ll have ongoing financial responsibilities.

- First Mortgage Payment: Your first mortgage payment is typically due one full month after your closing date. For example, if you close on June 15th, your first payment would likely be due August 1st.

- Escrow Accounts for Taxes and Insurance: Many lenders require an escrow account, where a portion of your monthly mortgage payment is set aside to cover property taxes and homeowner’s insurance premiums. The lender manages these payments on your behalf.

- Budgeting for Ongoing Homeownership Costs: Beyond your mortgage, remember to budget for utilities, routine maintenance, potential repairs, and possibly HOA fees. Building an emergency fund specifically for home-related expenses is a smart financial move.

Expert Tips for a Smooth Journey

Securing a home loan is a marathon, not a sprint. A few key practices can make the journey considerably smoother and more successful.

Maintain Financial Discipline

From the moment you decide to pursue a home loan until after closing, it’s crucial to maintain stable financial behavior. Avoid making any large purchases, opening new credit lines, closing existing credit accounts, or changing jobs. Any significant financial changes can impact your credit score, DTI, or employment verification, potentially jeopardizing your loan approval.

Shop Around for Rates

Never settle for the first loan offer you receive. Contact multiple lenders—banks, credit unions, and mortgage brokers—to compare interest rates, fees, and loan terms. Even a seemingly small difference in interest rate can save you tens of thousands of dollars over the life of a 30-year mortgage. Request a Loan Estimate from each to facilitate an apples-to-apples comparison.

Don’t Be Afraid to Ask Questions

The mortgage process is complex, and there’s a lot of jargon. If you don’t understand something, ask. Ask your loan officer, your real estate agent, or your attorney. A clear understanding of every document you sign and every step of the process empowers you to make informed financial decisions.

Work with a Trusted Team

Assemble a team of reliable professionals. A good real estate agent can guide you through the home search and negotiation, a diligent loan officer can navigate the mortgage process, and a thorough home inspector can uncover potential property issues. Each plays a vital role in ensuring a successful and secure transaction.

Securing a home loan is a significant financial milestone that requires careful planning, thorough preparation, and a clear understanding of the intricate process. By laying a strong financial foundation, exploring the various loan options, diligently navigating the application and underwriting stages, and meticulously managing the closing, you can confidently achieve your dream of homeownership. While complex, this journey is entirely achievable with patience, persistence, and an informed approach, ultimately leading to the rewarding stability of your own home.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.