Mortgage rates are a cornerstone of the housing market, directly impacting affordability, buying power, and the overall financial health of homeowners and prospective buyers. For anyone considering purchasing a home, refinancing an existing mortgage, or simply trying to understand the broader economic picture, comprehending “what mortgage rates are today” is not merely an exercise in curiosity; it’s a critical financial imperative. These rates are dynamic, influenced by a complex interplay of economic indicators, central bank policies, and global market forces, making their daily fluctuations a constant topic of discussion and analysis.

Understanding current mortgage rates goes beyond just knowing a number. It involves grasping the underlying mechanisms that drive these rates, the factors that cause them to rise or fall, and how a borrower’s individual circumstances can shape the rate they ultimately secure. In today’s economic environment, where inflation, interest rate hikes, and geopolitical events frequently dominate headlines, staying informed about mortgage rate trends is more important than ever. This comprehensive guide aims to demystify mortgage rates, offering insights into their behavior, practical advice for tracking them, and strategies for securing the most favorable terms for your financial future.

Understanding the Fundamentals of Mortgage Rates

Before diving into the daily ebb and flow of rates, it’s essential to establish a foundational understanding of what mortgage rates truly represent and the different forms they can take. This basic knowledge empowers borrowers to make more informed decisions and to better interpret the financial news related to home lending.

What is a Mortgage Rate?

At its core, a mortgage rate is the interest rate you pay on the money you borrow to purchase or refinance a home. It is expressed as a percentage of the principal loan amount and determines the cost of borrowing over the life of the loan. This rate is a primary driver of your monthly mortgage payment, influencing how much of your payment goes towards interest versus the principal balance. A lower interest rate means lower monthly payments and less money paid over the loan term, while a higher rate leads to higher payments and a greater overall cost.

Fixed vs. Adjustable-Rate Mortgages (ARMs)

Mortgages primarily come in two types when it comes to how their rates behave:

- Fixed-Rate Mortgages: As the name suggests, the interest rate on a fixed-rate mortgage remains constant for the entire duration of the loan, typically 15 or 30 years. This offers predictability and stability, as your principal and interest payment will never change, regardless of market fluctuations. Borrowers often prefer fixed rates for long-term budgeting and peace of mind, especially in periods of low interest rates or expected rate increases.

- Adjustable-Rate Mortgages (ARMs): ARMs feature an initial fixed-rate period (e.g., 5, 7, or 10 years), after which the interest rate adjusts periodically based on a predetermined index (like SOFR – Secured Overnight Financing Rate) plus a margin. While ARMs often start with lower interest rates than fixed-rate mortgages, the uncertainty of future rate adjustments can be a significant risk. They might be attractive to borrowers who plan to sell or refinance before the fixed-rate period ends, or who expect their income to increase significantly.

The Impact of Annual Percentage Rate (APR)

While the interest rate tells you the cost of borrowing, the Annual Percentage Rate (APR) provides a more comprehensive measure of the total cost of a mortgage over its life. APR includes the interest rate plus other costs associated with the loan, such as origination fees, discount points, mortgage insurance, and other lender charges. Because APR encompasses more fees, it is typically higher than the nominal interest rate. Comparing APRs across different lenders gives a more accurate picture of the true cost of each loan offer, allowing for a better apples-to-apples comparison.

Key Factors Influencing Current Mortgage Rates

Mortgage rates are not set in a vacuum. They are highly responsive to a myriad of economic and financial indicators, making their daily movements a subject of intense scrutiny by economists, analysts, and borrowers alike. Understanding these influences is crucial for anticipating trends and making timely decisions.

Federal Reserve Policy and Interest Rates

Perhaps the most significant influencer of mortgage rates, albeit indirectly, is the Federal Reserve. While the Fed does not directly set mortgage rates, its monetary policy decisions, particularly changes to the federal funds rate, have a profound ripple effect. When the Fed raises its benchmark rate to combat inflation, it generally makes borrowing more expensive across the board, pushing up rates on other types of loans, including mortgages. Conversely, a reduction in the federal funds rate typically aims to stimulate economic activity by making borrowing cheaper.

Inflation and Economic Indicators

Inflation is a primary concern for lenders and bond investors. When inflation is high, the purchasing power of money erodes over time. Lenders demand higher interest rates to compensate for this loss of value, ensuring that the returns on their investments maintain their real worth. Key economic reports such as the Consumer Price Index (CPI), employment data, GDP growth, and manufacturing indices provide snapshots of the economy’s health and inflationary pressures, all of which directly or indirectly feed into mortgage rate calculations. A strong economy often correlates with higher inflation and, subsequently, higher rates, as the Fed may act to cool down an overheating market.

The Bond Market (Specifically 10-Year Treasury Yields)

Long-term mortgage rates, especially for 30-year fixed mortgages, are closely tied to the yields on the 10-year U.S. Treasury bond. Mortgage-backed securities (MBS), which are bundles of mortgages sold to investors, compete with Treasury bonds for investor capital. When 10-year Treasury yields rise, investors demand higher yields on MBS, which translates into higher mortgage rates for consumers. Conversely, falling Treasury yields often signal a flight to safety during economic uncertainty or an anticipation of lower inflation, pushing mortgage rates down. Monitoring the 10-year Treasury yield is often a good predictor of the general direction of fixed mortgage rates.

Lender Competition and Overhead

While macroeconomic factors set the baseline, individual lenders also play a role in the rates they offer. Competition among banks, credit unions, and non-bank lenders can lead to slightly better rates or more favorable terms for borrowers. A lender’s operational costs, risk assessment models, and profit margins are all factored into the rates they quote. This is why shopping around multiple lenders is always recommended, as rates can vary, sometimes significantly, from one institution to another even on the same day.

Your Personal Financial Profile

Finally, and crucially, your individual financial situation heavily influences the mortgage rate you qualify for. Lenders assess risk based on several personal factors:

- Credit Score: A higher credit score (generally above 740-760) indicates a lower risk to lenders, often resulting in access to the most competitive rates.

- Down Payment: A larger down payment reduces the loan amount and the lender’s risk exposure, which can translate into a better interest rate.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (typically below 43%) signals that you can comfortably manage your new mortgage payments.

- Loan-to-Value (LTV) Ratio: This is the loan amount divided by the home’s value. A lower LTV (higher down payment) usually leads to better rates.

How to Interpret and Track Mortgage Rates

Given their dynamic nature, knowing where to find reliable rate information and how to interpret it is essential for any serious borrower.

Where to Find Daily Rate Updates

Several reputable financial websites, mortgage lenders, and industry publications provide daily updates on average mortgage rates. These often include rates for 30-year fixed, 15-year fixed, and various ARM products. Examples include Freddie Mac’s Primary Mortgage Market Survey, Bankrate, Zillow, and NerdWallet. While these sources provide national averages, remember that the rate you personally receive may differ based on your specific financial profile and location.

Understanding Rate Trends and Volatility

Don’t just look at today’s rate in isolation. Pay attention to trends over weeks and months. Are rates steadily climbing, falling, or experiencing high volatility? Understanding the trend can help you decide if it’s a good time to lock in a rate or if waiting might be beneficial. Volatility can be a double-edged sword; it can present opportunities for lower rates but also carries the risk of rates jumping up quickly.

The Importance of Rate Locks

Once you apply for a mortgage, you’ll have the option to “lock in” your interest rate. A rate lock guarantees the interest rate for a specific period (e.g., 30, 45, or 60 days) while your loan is being processed. This protects you from rate increases if market rates rise before your loan closes. However, if rates fall during your lock period, you might miss out on a lower rate unless your lender offers a “float down” option, which often comes with a fee. Timing your rate lock strategically is a key decision in the mortgage process.

Strategies for Securing the Best Mortgage Rate

While some factors influencing mortgage rates are beyond a borrower’s control, there are proactive steps individuals can take to improve their chances of securing the most favorable terms.

Improving Your Credit Score

Your credit score is paramount. Before applying for a mortgage, obtain copies of your credit reports from all three major bureaus (Equifax, Experian, TransUnion) and dispute any errors. Pay down high-interest debt, avoid opening new credit lines, and make all payments on time. A higher credit score signals responsibility and lower risk to lenders, leading to better rate offers.

Increasing Your Down Payment

A larger down payment reduces the amount you need to borrow and signals greater financial stability. This decreases the lender’s risk, often resulting in a lower interest rate and potentially avoiding the need for private mortgage insurance (PMI). Aiming for at least 20% down is ideal, but even going slightly above the minimum required can make a difference.

Shopping Around for Lenders

Never settle for the first offer you receive. Contact multiple lenders—including large banks, local credit unions, and online mortgage brokers—to compare their rates, fees, and overall loan terms. Subtle differences in APRs and closing costs can add up to significant savings over the life of the loan. Leverage competitive offers from one lender to negotiate with another.

Considering Points and Fees

Lenders often offer borrowers the option to pay “points” (also known as discount points) at closing to reduce the interest rate. One point typically equals 1% of the loan amount. While paying points can lower your monthly payments, it increases your upfront closing costs. You’ll need to calculate the “break-even point” – how long it takes for the monthly savings to offset the cost of the points – to determine if it’s a worthwhile investment for your situation. Understand all associated fees, not just the interest rate, to get a full picture of the loan’s cost.

The Long-Term Implications of Today’s Mortgage Rates

Current mortgage rates don’t just affect immediate monthly payments; they have profound long-term implications for financial planning, housing market dynamics, and wealth accumulation.

Impact on Affordability and Monthly Payments

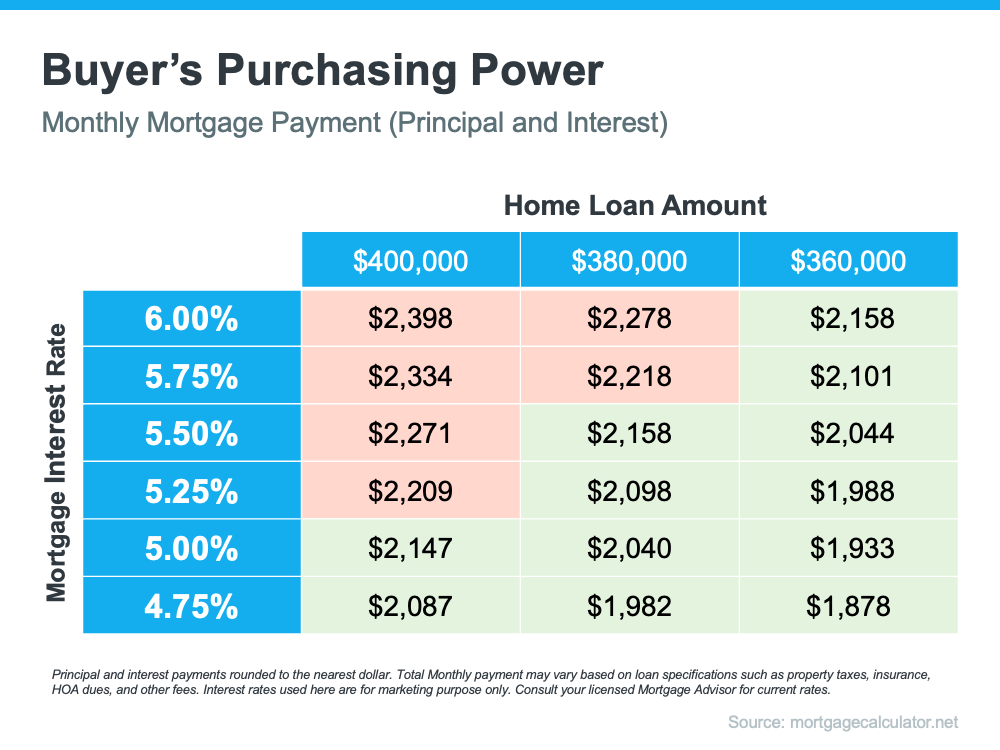

Higher mortgage rates directly translate to higher monthly principal and interest payments for the same loan amount. This can significantly reduce purchasing power and make homeownership less accessible for some buyers, particularly in high-cost areas. Conversely, lower rates enhance affordability, allowing buyers to qualify for larger loans or enjoy lower monthly expenses. For many, understanding what is mortgage rates today is about understanding what kind of home, if any, they can afford.

Refinancing Opportunities and Considerations

Existing homeowners pay close attention to mortgage rates as well, especially for refinancing opportunities. If current rates drop significantly below their existing mortgage rate, refinancing can lead to substantial savings on monthly payments, a shorter loan term, or the ability to tap into home equity. However, refinancing involves new closing costs, so a careful cost-benefit analysis is always necessary to determine if the savings outweigh the expenses.

Housing Market Dynamics

Mortgage rates are a critical determinant of housing market health. High rates can cool down an overheated market by reducing buyer demand and slowing sales, potentially leading to price stabilization or even decreases. Low rates, on the other hand, often fuel demand, leading to bidding wars and home price appreciation. Therefore, monitoring “what is mortgage rates today” also provides valuable insight into the broader trajectory of the real estate market.

In conclusion, mortgage rates are far more than just numbers; they are powerful economic indicators with tangible effects on individuals and the economy at large. By diligently tracking rates, understanding their underlying influences, and implementing smart financial strategies, prospective homebuyers and existing homeowners can navigate the complex mortgage landscape with greater confidence and make decisions that align with their long-term financial goals. Staying informed about current market conditions and seeking expert advice from trusted financial professionals are invaluable steps in securing a favorable mortgage and building a stable financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.