In an increasingly digital world, the concept of trust—its creation, maintenance, and verification—has become paramount. For decades, this trust has largely resided with centralized authorities: banks, governments, social media platforms, and large corporations. These intermediaries have served as the gatekeepers of information and transactions, holding immense power and responsibility. However, the rise of “blockchain technologies” presents a paradigm shift, offering a decentralized, transparent, and immutable alternative for establishing trust without reliance on a central figure. Far from being a mere buzzword associated solely with volatile cryptocurrencies, blockchain is a foundational technological innovation with the potential to redefine how we interact, transact, and secure information across virtually every industry.

At its core, blockchain is a distributed ledger technology (DLT) that records transactions in a secure, verifiable, and permanent way. Imagine a digital ledger that is not controlled by any single entity, but rather is replicated and synchronized across a vast network of computers. Every time a new transaction occurs, it is added as a “block” of data to this chain, cryptographically linked to the previous block, forming an unbroken, chronological record. This chain, once established, is incredibly difficult to alter, ensuring data integrity and fostering a new era of digital trust. Understanding blockchain is to understand a fundamental shift in how digital information can be managed, secured, and shared, moving us from a trust-in-intermediaries model to a trust-in-code model.

The Foundational Principles of Blockchain

To truly grasp the revolutionary nature of blockchain, it’s essential to dissect its underlying principles. These tenets collectively contribute to its resilience, security, and unique capabilities, distinguishing it from traditional database systems.

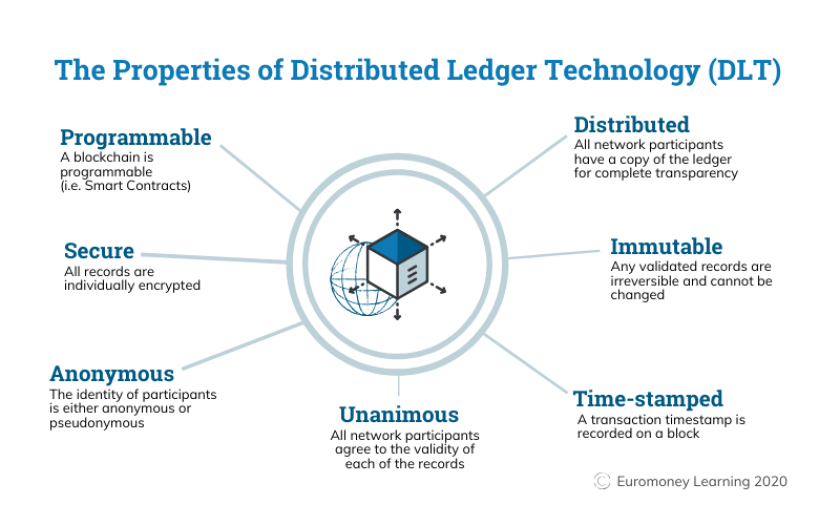

Decentralization

Perhaps the most defining characteristic of blockchain is decentralization. Unlike conventional systems where a central server or authority manages all data and operations, a blockchain network is distributed across numerous nodes (computers). Each node holds a full copy of the ledger, and there is no single point of control or failure. This removes the need for intermediaries, drastically reducing the risk of censorship, data manipulation, or system outages that plague centralized systems. Decisions and validations are made collectively by the network participants, making the system inherently more robust and resistant to attack.

Distributed Ledger Technology (DLT)

Blockchain is a specific type of Distributed Ledger Technology (DLT). A DLT is a database that is consensually shared and synchronized across multiple sites, institutions, or geographies, accessible by multiple people. All participants in the network have their own identical copy of the ledger. Any update to the ledger must be validated by the network’s consensus mechanism before it is propagated to all copies. This distribution ensures transparency, as all participants can view the same immutable record, and integrity, as tampering with one copy would not affect the others and would be immediately evident.

Cryptographic Security

Cryptography is the backbone of blockchain security. Each block in the chain contains a cryptographic hash of the previous block, creating an unbreakable link. A hash is a unique digital fingerprint of a block’s data. If even a single piece of information within an older block is altered, its hash changes, breaking the link and invalidating all subsequent blocks. This makes the blockchain virtually immutable and tamper-proof. Additionally, digital signatures, enabled by public-key cryptography, ensure the authenticity and integrity of transactions, verifying that transactions originate from the legitimate owner and have not been altered in transit.

Consensus Mechanisms

For a decentralized network to function, there must be a way for all participants to agree on the current state of the ledger. This is achieved through consensus mechanisms. These algorithms are crucial for validating new transactions and blocks, ensuring that all copies of the ledger remain synchronized and accurate. The most well-known mechanism is Proof of Work (PoW), used by Bitcoin, where “miners” compete to solve complex computational puzzles to add new blocks. The first to solve it broadcasts the new block, and others verify it. Other mechanisms include Proof of Stake (PoS), where validators are chosen based on the amount of cryptocurrency they “stake” as collateral, and various other, more energy-efficient models designed for different use cases.

How Blockchain Works: A Step-by-Step Overview

Understanding the fundamental principles sets the stage for appreciating the operational flow of a blockchain. While implementations vary, the core process remains consistent across most blockchain networks.

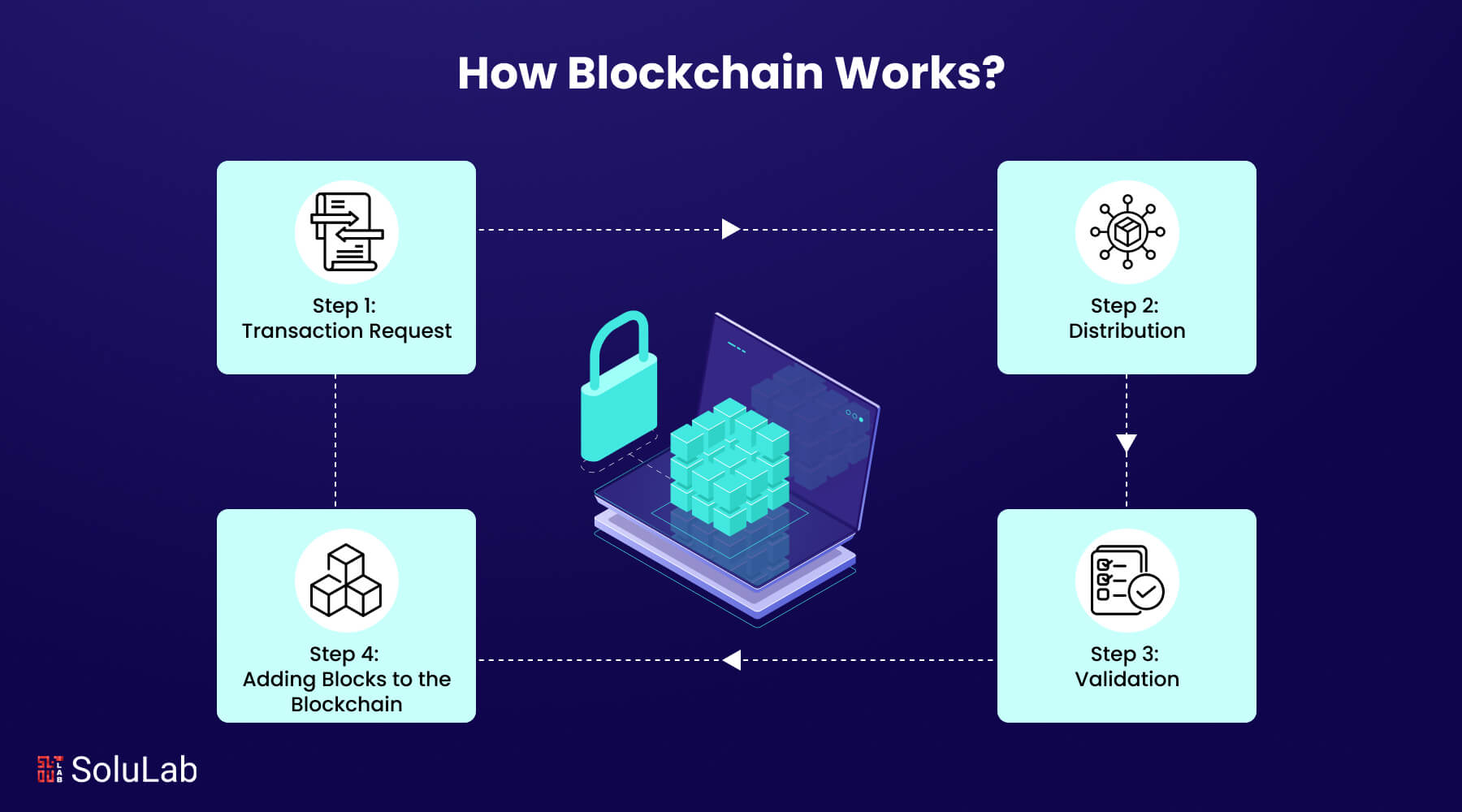

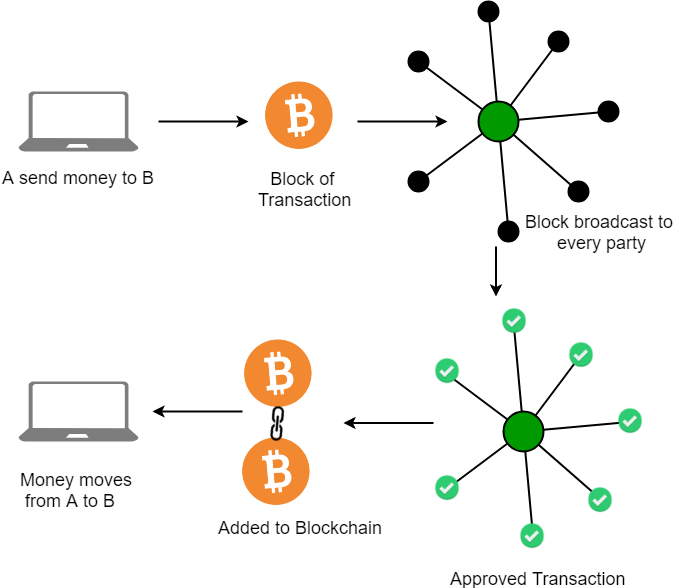

Transaction Initiation and Verification

The journey begins when a user initiates a transaction, for example, sending digital assets or recording data. This transaction is typically signed digitally by the sender using their private key, proving ownership and intent. Once signed, the transaction is broadcast to the peer-to-peer network. Nodes in the network receive this transaction and independently verify its legitimacy – checking for valid signatures, sufficient funds (if applicable), and adherence to network rules.

Block Creation

Verified transactions are then gathered into a “block” of data. Each block has a maximum capacity for transactions. Before a block can be added to the chain, it must also include a timestamp, a unique identifier (nonce), and the cryptographic hash of the previous block, linking it directly to the chain’s history. The act of creating and preparing a block for addition is often referred to as “mining” in PoW systems or “validating” in PoS systems.

Adding to the Chain

Once a block is ready (e.g., a PoW puzzle is solved, or a PoS validator is chosen), it is broadcast to the entire network. Other nodes then verify the integrity of this newly proposed block, checking its hash, the validity of its transactions, and its link to the previous block. If a consensus is reached (e.g., a majority of nodes agree it’s valid), the new block is officially added to the end of the blockchain. This makes the ledger longer by one block, and the new state of the ledger is propagated to all network participants.

Immutability and Transparency

Once a block is added and confirmed, it becomes a permanent part of the blockchain. Because each block contains the hash of the preceding block, altering any past block would require re-calculating the hashes of all subsequent blocks, which is computationally infeasible for a sufficiently large and active network. This immutability ensures that once information is recorded, it cannot be retroactively changed or deleted, providing an unprecedented level of data integrity. Furthermore, because every participant holds a copy of the ledger, and new transactions are visible to all (though identities can remain pseudonymous), the blockchain offers a high degree of transparency.

Beyond Cryptocurrencies: Diverse Applications of Blockchain

While Bitcoin famously introduced blockchain to the world, limiting its understanding to digital currencies misses the vast spectrum of its potential applications. Blockchain is a general-purpose technology, capable of transforming industries far beyond finance.

Supply Chain Management

Blockchain offers an unparalleled solution for tracking products from their origin to the consumer. By recording every step of a product’s journey on an immutable ledger—from raw materials to manufacturing, shipping, and retail—companies can achieve unprecedented transparency and traceability. This helps in verifying authenticity, combating counterfeiting, identifying sources of contamination in food chains, and ensuring ethical sourcing, all while reducing administrative overhead.

Digital Identity and Cybersecurity

Traditional digital identity systems are centralized, making them vulnerable to breaches and giving individuals little control over their personal data. Blockchain can enable “self-sovereign identity,” where individuals own and control their digital identities, granting access to specific information only when and to whom they choose. This significantly enhances privacy and security, as identity attributes are stored securely on the blockchain, and users can selectively disclose verifiable credentials without revealing unnecessary personal data.

Healthcare and Data Management

In healthcare, blockchain can address critical challenges related to data interoperability, security, and patient privacy. Securely storing and sharing patient records across different providers, maintaining an immutable audit trail of medical treatments, drug prescriptions, and even clinical trials can improve care coordination and research. Furthermore, it can help prevent medical fraud and ensure the integrity of pharmaceutical supply chains.

Voting Systems

The integrity of electoral processes is a cornerstone of democracy. Blockchain offers a promising path to enhance the transparency and security of voting systems. By recording each vote as an encrypted, anonymous transaction on a blockchain, it could create a tamper-proof record, ensure that every vote is counted only once, and allow for auditable elections, all while protecting voter privacy.

Intellectual Property Protection

Artists, creators, and inventors often struggle to prove ownership and protect their intellectual property (IP). Blockchain can provide an immutable timestamp and record of creation, effectively registering IP and demonstrating its existence at a particular point in time. This can simplify royalty distribution, copyright management, and provide verifiable proof in cases of infringement.

Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into lines of code. They automatically execute and enforce the terms when predefined conditions are met, without the need for intermediaries. For example, a smart contract could automatically release payment to a supplier once goods are verified as delivered, or disburse insurance payouts upon confirmation of an event. This reduces costs, eliminates delays, and increases trust in agreements across various sectors, from legal agreements to real estate and insurance.

The Technical Landscape: Challenges and Future Trends

Despite its transformative potential, blockchain technology is still evolving and faces several technical challenges that developers and researchers are actively addressing. The future of blockchain will be defined by how successfully these hurdles are navigated and by continued innovation.

Scalability Issues

One of the most significant challenges for many public blockchains, particularly those using PoW, is scalability. Processing a high volume of transactions quickly and efficiently remains an obstacle. Bitcoin, for instance, processes only a few transactions per second, compared to thousands or tens of thousands for centralized payment networks. Solutions being explored include sharding (dividing the network into smaller, more manageable segments), layer-2 solutions (off-chain protocols that process transactions off the main blockchain and then settle them on-chain), and adopting more efficient consensus mechanisms.

Interoperability

As the number of blockchain networks proliferates, the ability for these disparate systems to communicate and exchange data seamlessly—interoperability—becomes crucial. Currently, different blockchains often operate in silos. Achieving true interoperability would unlock greater utility, allowing assets and data to flow between various chains, fostering a more connected and efficient blockchain ecosystem. Projects focused on “cross-chain bridges” and standardized protocols are key to addressing this.

Regulatory Hurdles and Adoption

The decentralized and global nature of blockchain technology presents complex regulatory challenges. Governments worldwide are grappling with how to classify and regulate digital assets, smart contracts, and decentralized autonomous organizations (DAOs). Uncertainty in regulatory frameworks can hinder mainstream adoption and innovation. As the technology matures, clearer, more harmonized regulatory guidelines will be essential for widespread integration into traditional economies.

Quantum Computing Threats

The cryptographic algorithms that secure current blockchains rely on the mathematical difficulty of certain problems, such as prime factorization. While currently unfeasible, future quantum computers could potentially solve these problems rapidly, rendering existing cryptographic methods vulnerable. Researchers are actively developing “quantum-resistant” cryptographic algorithms to future-proof blockchain security against this potential threat.

Evolution of Consensus Mechanisms and Governance

The pursuit of more efficient, secure, and democratic consensus mechanisms continues. Beyond PoW and PoS, new models like Delegated Proof of Stake (DPoS), Proof of Authority (PoA), and others are being refined. Furthermore, the concept of decentralized autonomous organizations (DAOs), where community members vote on proposals and govern the network directly through smart contracts, represents an evolving frontier in blockchain governance.

Enterprise Blockchain Solutions

While public blockchains like Ethereum are open to anyone, many enterprises are exploring private or consortium blockchains. These controlled environments offer advantages like higher transaction speeds, greater privacy (by restricting access to authorized participants), and easier integration with existing corporate systems. Hybrid models, combining elements of public and private chains, are also gaining traction, allowing businesses to leverage blockchain’s benefits while maintaining necessary control and confidentiality.

Conclusion: A Paradigm Shift in Digital Trust

Blockchain technologies are undeniably more than a passing fad; they represent a fundamental architectural shift in how we conceive of and interact with digital information, assets, and trust. By offering a decentralized, transparent, and immutable ledger, blockchain empowers individuals and organizations to operate with unprecedented levels of security, efficiency, and autonomy. From streamlining global supply chains and securing digital identities to revolutionizing finance and enabling new forms of governance, its applications are vast and growing.

The journey of blockchain is still in its early stages, marked by ongoing technical advancements, evolving regulatory landscapes, and the continuous exploration of new use cases. While challenges related to scalability, interoperability, and energy consumption remain, the relentless innovation within the tech community is steadily addressing these issues. As we move forward, blockchain is poised to become an increasingly integral part of the digital infrastructure, not just as a technology for cryptocurrencies, but as a foundational layer enabling a more trustworthy, resilient, and equitable digital future. Its profound impact will be felt across every sector, reshaping the very fabric of our connected world by decentralizing trust and empowering the individual.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.