Purchasing a car is a significant financial decision for most individuals and families. For many, a car loan is an indispensable tool, enabling them to acquire reliable transportation without depleting their entire savings upfront. Among the various financing options available, securing a bank loan for a car remains one of the most traditional and often advantageous routes. Banks, with their established infrastructure and competitive offerings, provide a structured and transparent lending process. However, navigating this process requires careful preparation, a clear understanding of financial principles, and strategic decision-making. This comprehensive guide will walk you through the intricacies of obtaining a bank loan for your next vehicle, empowering you to make informed choices that align with your financial goals.

Understanding Car Loans and Their Importance

A car loan is fundamentally a financial agreement between you and a lender – in this case, a bank – where the bank provides you with a sum of money to purchase a vehicle, and you agree to repay that amount, plus interest, over a predetermined period. This period is known as the loan term, and repayments are typically made in fixed monthly installments.

What is a Car Loan?

At its core, a car loan is a secured loan, meaning the vehicle itself serves as collateral. If you default on your payments, the bank has the right to repossess the car to recover their losses. This security aspect often translates into lower interest rates compared to unsecured loans, as the risk to the lender is mitigated. The principal amount of the loan covers the car’s purchase price, often excluding a down payment, taxes, and fees, which may need to be paid separately or rolled into the loan depending on the terms.

Why Choose a Bank Loan?

While dealerships offer financing, and credit unions and online lenders present alternatives, banks often stand out for several reasons:

- Competitive Interest Rates: Banks, especially larger institutions, have vast financial resources and often offer some of the most competitive interest rates to attract borrowers, particularly those with strong credit profiles.

- Established Trust and Reputation: Banks are generally perceived as stable and reputable institutions, providing a sense of security and reliability in the lending process.

- Diverse Product Offerings: Many banks offer a range of loan products with flexible terms, allowing borrowers to find a solution that best fits their financial situation. They may also offer other services like checking accounts, savings, and credit cards, allowing for a consolidated banking relationship.

- Personalized Service: For existing bank customers, the process can be smoother, and there might be opportunities for preferential rates or dedicated support from a loan officer.

- Pre-Approval Options: Banks frequently offer pre-approval, which can significantly strengthen your bargaining position at the dealership by clarifying your budget and demonstrating your financial readiness.

Key Factors Influencing Your Loan

Several critical elements will dictate the terms and ultimate cost of your car loan:

- Credit Score: This three-digit number is arguably the most significant factor. A higher credit score (generally above 700) indicates a lower risk to lenders, leading to better interest rates and more favorable terms.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders use it to assess your ability to manage additional debt. A lower DTI ratio is more favorable.

- Loan Term: The length of time you have to repay the loan. Longer terms often mean lower monthly payments but result in more interest paid over the life of the loan. Shorter terms have higher monthly payments but save on overall interest.

- Interest Rate (APR): The annual percentage rate is the cost of borrowing money, expressed as a yearly percentage. It includes the interest rate plus any fees. A lower APR means a cheaper loan.

- Down Payment: The initial amount of money you pay towards the car’s purchase price. A larger down payment reduces the loan amount, lowers your monthly payments, and can secure a better interest rate.

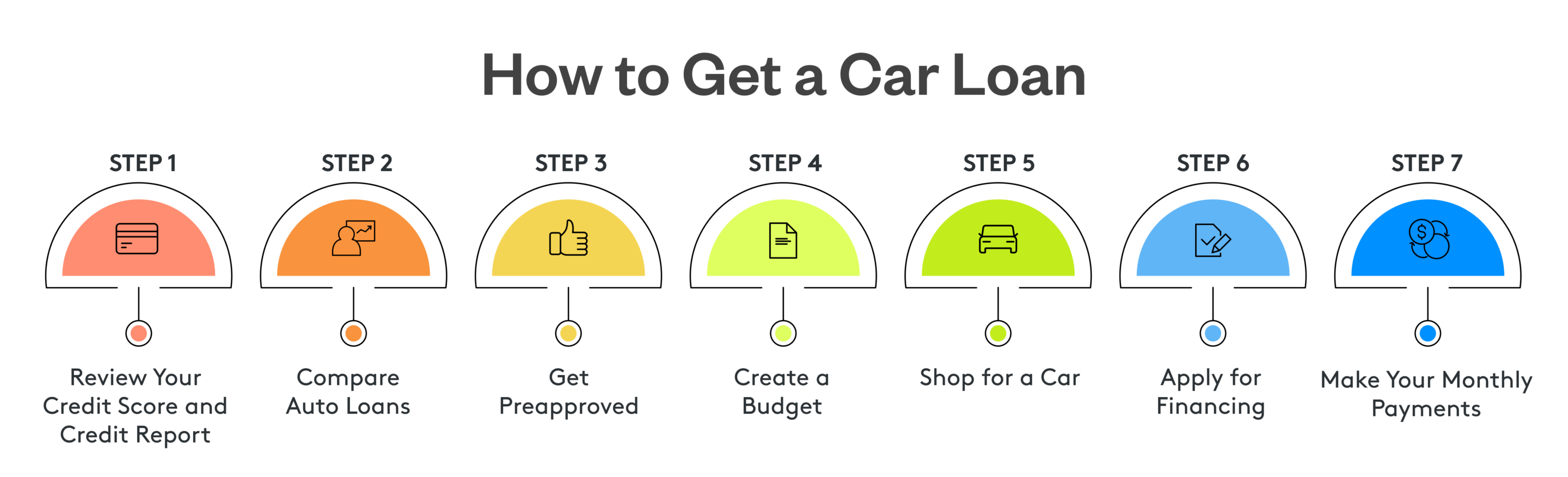

Preparing for Your Car Loan Application

Preparation is key to a smooth and successful car loan application process. Before you even step into a bank or a dealership, a thorough understanding of your financial standing and clear objectives for your car purchase are crucial.

Assessing Your Financial Health

Before applying, take an honest look at your finances:

- Check Your Credit Score and Report: Obtain free copies of your credit report from Equifax, Experian, and TransUnion via AnnualCreditReport.com. Review them for errors and dispute any inaccuracies. Understanding your score gives you an idea of the rates you might qualify for. If your score is low, consider taking steps to improve it before applying.

- Calculate Your Debt-to-Income (DTI) Ratio: Sum up all your recurring monthly debt payments (rent/mortgage, credit card minimums, student loans, etc.) and divide by your gross monthly income. Aim for a DTI below 36% for optimal loan eligibility.

- Review Your Income Stability: Lenders prefer borrowers with a stable and verifiable income. Have recent pay stubs, W-2s, or tax returns ready to demonstrate your earning capacity.

Budgeting for Your Car Purchase

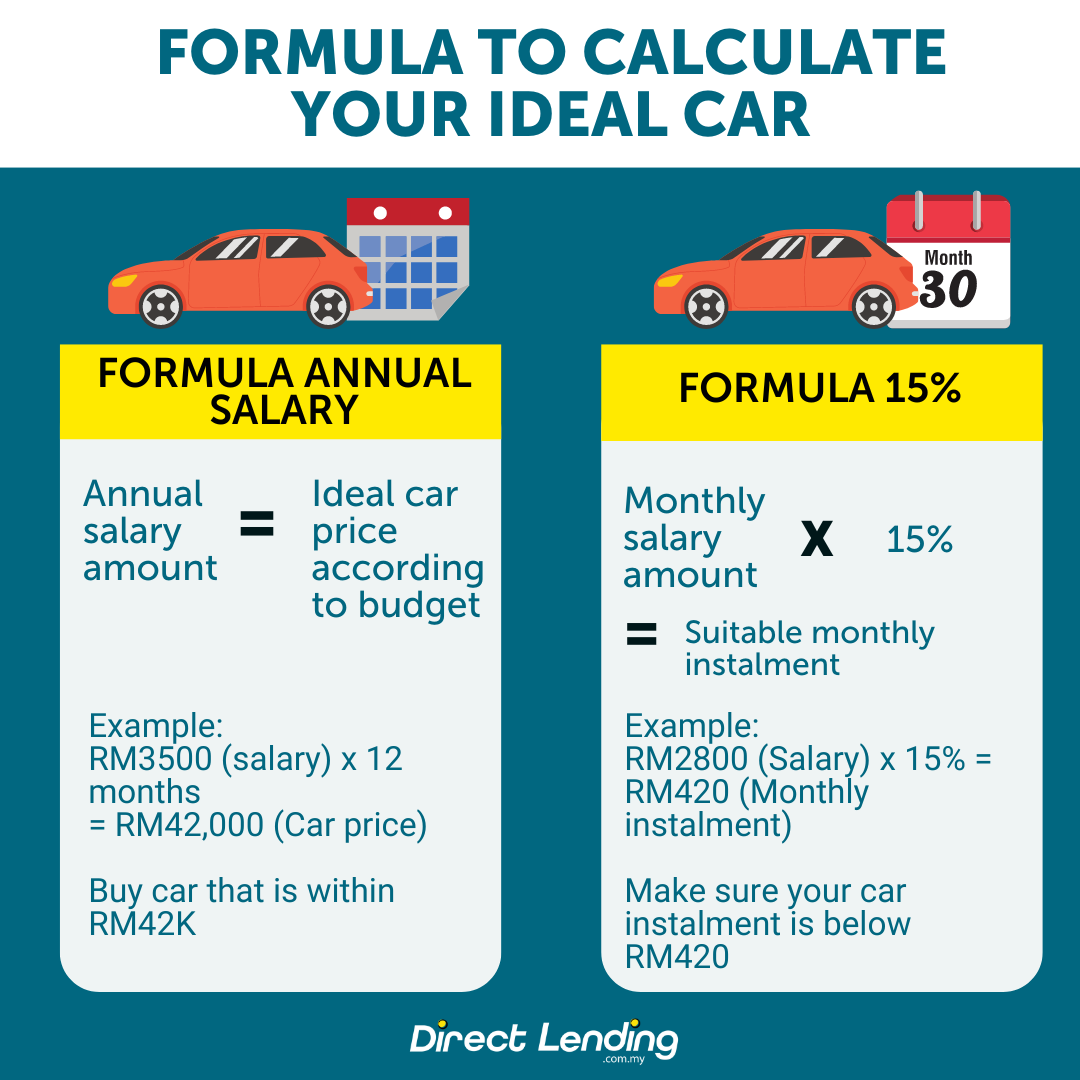

A car’s cost extends far beyond its sticker price. Develop a comprehensive budget:

- Determine Your Maximum Monthly Payment: Use online calculators to estimate what you can comfortably afford each month, factoring in all your existing expenses. Don’t just consider the principal and interest; account for insurance, fuel, maintenance, and potential parking fees.

- Plan Your Down Payment: Aim for at least 10-20% of the car’s purchase price, especially for new cars, to reduce your loan amount and potentially secure better terms. A larger down payment also helps mitigate the risk of being “upside down” on your loan (owing more than the car is worth).

- Account for Other Costs: Factor in sales tax, registration fees, title fees, and potential dealership documentation fees. These can add several hundred to thousands of dollars to the total cost.

Gathering Necessary Documentation

Having your documents organized beforehand will streamline the application process:

- Proof of Identity: Government-issued photo ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (last 1-2 months), W-2 forms (last 2 years), or tax returns (last 2 years if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information (if already chosen): Make, model, year, VIN, and sales price.

- Trade-in Information (if applicable): Title, registration, and loan payoff amount for your current vehicle.

Researching Car Options

Even before applying for the loan, having a clear idea of the car you want helps immensely.

- New vs. Used: New cars depreciate rapidly, but often come with manufacturer warranties and lower initial maintenance. Used cars are cheaper but might have higher maintenance costs.

- Make and Model: Research reliability, fuel efficiency, safety ratings, and average insurance costs for your desired vehicles.

- Market Value: Use resources like Kelley Blue Book (KBB) or Edmunds to determine fair market values for new and used cars to ensure you’re getting a reasonable price.

Navigating the Bank Loan Application Process

With your finances in order and documents prepared, you’re ready to engage with banks. This stage involves comparing offers, submitting your application, and understanding the outcomes.

Comparing Bank Loan Offers

Don’t settle for the first offer you receive. Shop around:

- Contact Multiple Banks: Reach out to your current bank, other national banks, and local community banks. Each may have different lending criteria and rates.

- Request Pre-Approval: This is a crucial step. Pre-approval means a bank has reviewed your finances and agreed to lend you a specific amount at a particular interest rate, before you’ve even picked out a car. This gives you a firm budget and strengthens your negotiating power at the dealership. Banks typically issue pre-approvals that are valid for 30-60 days.

- Scrutinize Loan Terms: Beyond the interest rate, compare:

- Loan Term: Shorter terms mean higher monthly payments but less interest paid overall.

- Fees: Look out for origination fees, application fees, or prepayment penalties.

- APR vs. Interest Rate: Remember APR includes other costs beyond just the interest.

- Payment Schedule: Understand when payments are due and what grace periods exist.

The Application Submission

Once you’ve chosen a bank or decided to pursue pre-approval:

- Complete the Application Accurately: Fill out all required fields truthfully and completely. Any discrepancies could delay or jeopardize your application.

- Submit All Required Documentation: Provide everything the bank asks for promptly. Missing documents are a common cause of delays.

- Be Prepared for Questions: Loan officers may follow up with questions about your financial history, employment, or the intended vehicle.

Understanding Loan Approval and Rejection

- Approval: Congratulations! The bank will provide you with a loan offer outlining the terms and conditions. Review this document meticulously before signing. If you have pre-approval, you can now use this to finalize your car purchase.

- Conditional Approval: Sometimes, a bank may approve your loan but with certain conditions, such as requiring a larger down payment, a co-signer, or proof of additional income.

- Rejection: If your application is rejected, don’t despair. The bank is legally required to provide you with the reasons for rejection. This feedback is invaluable for improving your financial standing for future applications. Common reasons include low credit score, high DTI, insufficient income, or a short credit history.

Pre-Approval: A Strategic Advantage

The importance of bank pre-approval cannot be overstated. It transforms you from a casual browser into a serious buyer with cash in hand.

- Empowers Negotiation: You know your maximum loan amount and interest rate, allowing you to focus on negotiating the car’s price with the dealership, rather than simultaneously worrying about financing.

- Sets a Clear Budget: Prevents you from falling in love with a car outside your financial reach.

- Streamlines Dealership Process: With financing already secured, the car buying process at the dealership can be much quicker and less stressful.

- Benchmarking Tool: Even if you end up taking dealership financing (which might sometimes offer promotional rates), your bank pre-approval serves as a benchmark to ensure the dealership’s offer is genuinely better.

Maximizing Your Loan Success and Managing Your Debt

Securing a car loan is just the first step. Effective management of the loan ensures you minimize costs and maintain a healthy financial profile.

Negotiating Loan Terms

Even after receiving an offer, there might be room for negotiation, especially with the dealership:

- Leverage Pre-Approval: Use your bank pre-approval to challenge any higher interest rates offered by the dealership.

- Focus on the Out-the-Door Price: Rather than just the monthly payment, negotiate the total price of the car including all fees and taxes. A lower overall price means a smaller loan amount and less interest paid.

- Be Wary of Add-ons: Dealerships often push extended warranties, GAP insurance (if not necessary), or other accessories. Assess if these are truly valuable before agreeing.

Avoiding Common Pitfalls

Be aware of potential traps that can increase your loan cost:

- Long Loan Terms: While 72- or 84-month loans offer lower monthly payments, you’ll pay significantly more in interest over the loan’s life and risk owing more than the car is worth as it depreciates.

- Focusing Only on Monthly Payment: This can lead to agreeing to longer terms or higher prices without realizing the total cost.

- Ignoring the APR: Always compare the Annual Percentage Rate, not just the advertised interest rate, as it provides a true reflection of the loan’s cost.

- Not Shopping Around: Failing to compare offers from multiple lenders can cost you hundreds or thousands of dollars in higher interest.

The Importance of Timely Repayment

Consistent and timely loan payments are paramount:

- Builds Credit History: Every on-time payment positively impacts your credit score, making it easier to secure future loans at better rates.

- Avoids Late Fees: Late payments incur fees and can be reported to credit bureaus, damaging your score.

- Prevents Repossession: Missing multiple payments can lead to the bank repossessing your vehicle.

Refinancing Options (When and Why)

Life circumstances change, and sometimes, so do interest rates. Refinancing your car loan involves taking out a new loan to pay off your existing one, often with more favorable terms.

- When to Consider Refinancing:

- Improved Credit Score: If your credit score has significantly improved since you took out the original loan.

- Lower Interest Rates: If market interest rates have dropped.

- High Original Rate: If you secured your original loan with a high interest rate due to a poor credit score at the time.

- To Lower Monthly Payments: By extending the loan term (though this means more interest overall).

- Benefits: Lower monthly payments, reduced total interest paid, or a shorter loan term.

- Process: Similar to applying for an initial car loan, you’ll shop around for offers, submit an application, and provide documentation.

Beyond the Loan: The Full Cost of Car Ownership

While securing the loan is a major hurdle, remembering the ongoing financial commitments associated with car ownership is crucial for long-term financial health.

Insurance Considerations

Car insurance is a legal requirement in most places and a significant ongoing expense.

- Quotes Before Purchase: Get insurance quotes for the specific make and model you intend to buy before finalizing the purchase. Some cars are significantly more expensive to insure than others.

- Required Coverage: If you have a loan, your bank will typically require comprehensive and collision coverage to protect their collateral.

- Shop Around: Just like loans, compare insurance policies from various providers to find the best rates and coverage.

Maintenance and Fuel Costs

These are often overlooked but essential components of car ownership:

- Scheduled Maintenance: Factor in regular oil changes, tire rotations, brake checks, and other recommended service intervals.

- Unexpected Repairs: Even new cars can require unexpected repairs. Having an emergency fund or a dedicated car maintenance savings account is wise.

- Fuel Efficiency: Consider the car’s miles per gallon (MPG) as a factor in your budget, especially with fluctuating fuel prices.

Depreciation and Resale Value

Cars are depreciating assets, meaning they lose value over time.

- Understanding Depreciation: Most cars lose a significant portion of their value in the first few years. This impacts your equity in the car and can affect trade-in values.

- Resale Value: Research which makes and models tend to hold their value better if you plan to sell or trade in the car in the future.

Obtaining a bank loan for a car is a structured process that, when approached with careful planning and financial literacy, can be highly beneficial. By understanding your financial standing, preparing thoroughly, comparing offers diligently, and managing your debt responsibly, you can secure favorable terms and enjoy your new vehicle without unnecessary financial strain. Remember, a car loan is a tool – use it wisely to achieve your transportation needs while safeguarding your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.