Navigating the complexities of the tax system can often feel like a daunting task, yet understanding how to legally reduce your taxable income is one of the most powerful financial strategies available. It’s not about avoiding taxes; it’s about optimizing your financial picture by taking advantage of the deductions, credits, and tax-advantaged accounts the law provides. By proactively planning and making informed decisions, individuals and businesses can significantly lower their tax burden, free up capital for savings and investments, and accelerate their journey towards financial independence. This article will delve into practical, actionable strategies to help you effectively reduce your taxable income, transforming the annual tax season from a dreaded obligation into an opportunity for financial growth.

Understanding Taxable Income and Its Impact

Before diving into reduction strategies, it’s crucial to grasp what taxable income is and why minimizing it holds such significance for your financial well-being. A clear understanding of these foundational concepts empowers you to make more strategic decisions throughout the year.

Defining Taxable Income

At its core, taxable income is the portion of your gross income that is subject to taxation by federal, state, and sometimes local governments. It’s not simply your total earnings. Instead, it’s derived after accounting for various adjustments, deductions, and exemptions.

Your financial journey typically starts with Gross Income, which includes all earned income (wages, salaries, tips, business profits) and unearned income (interest, dividends, capital gains, rental income). From this, certain above-the-line deductions are subtracted to arrive at your Adjusted Gross Income (AGI). AGI is a critical figure as it often determines your eligibility for various tax credits and deductions. Finally, from your AGI, you subtract either the Standard Deduction (a fixed dollar amount based on your filing status) or Itemized Deductions (specific expenses like mortgage interest, state and local taxes, and charitable contributions) to arrive at your Taxable Income. This final figure is what the IRS uses to calculate your tax liability based on the progressive tax bracket system.

Why Reducing Taxable Income Matters

The primary and most apparent benefit of reducing taxable income is a lower tax bill. When less of your income is subject to taxation, you retain more of your hard-earned money. However, the benefits extend far beyond just paying less at tax time:

- Increased Disposable Income: More money in your pocket means greater financial flexibility for saving, investing, debt reduction, or discretionary spending.

- Enhanced Eligibility for Tax Credits and Deductions: Many valuable tax credits and deductions are subject to income phase-outs. A lower AGI can bring you within the eligibility thresholds for benefits like the Child Tax Credit, education credits, or the premium tax credit for health insurance.

- Improved Cash Flow: By reducing the amount withheld from your paycheck or owed at tax time, you improve your overall cash flow, making it easier to manage monthly expenses and build emergency savings.

- Accelerated Wealth Accumulation: The money saved on taxes can be reinvested, leading to compounded returns and a faster accumulation of wealth over time. This is especially true when utilizing tax-advantaged investment vehicles that also reduce taxable income.

Leveraging Pre-Tax Deductions and Contributions

One of the most straightforward and effective ways to reduce your taxable income is through pre-tax deductions and contributions. These strategies reduce your Adjusted Gross Income (AGI) directly, often before the money even reaches your bank account, thereby immediately lowering the income figure subject to taxation.

Retirement Account Contributions

Contributing to certain retirement accounts is perhaps the most universally accessible and impactful pre-tax strategy. Not only do these accounts help secure your financial future, but they also offer immediate tax advantages.

- Traditional IRA: Contributions to a Traditional IRA are often tax-deductible, reducing your taxable income in the year they are made. The earnings grow tax-deferred until withdrawal in retirement. Contribution limits apply, with additional “catch-up” contributions allowed for those aged 50 and older.

- Employer-Sponsored Plans (401(k), 403(b), TSP): If your employer offers a 401(k) or similar plan, contributing to it on a pre-tax basis is an excellent strategy. These contributions are automatically deducted from your paycheck before taxes are calculated, significantly reducing your taxable income. Many employers also offer a matching contribution, providing “free money” alongside your tax savings.

- Self-Employed Retirement Plans (SEP IRA, Solo 401(k)): For the self-employed or small business owners, options like a SEP IRA or Solo 401(k) allow for substantial pre-tax contributions, providing powerful avenues to reduce taxable income while saving for retirement.

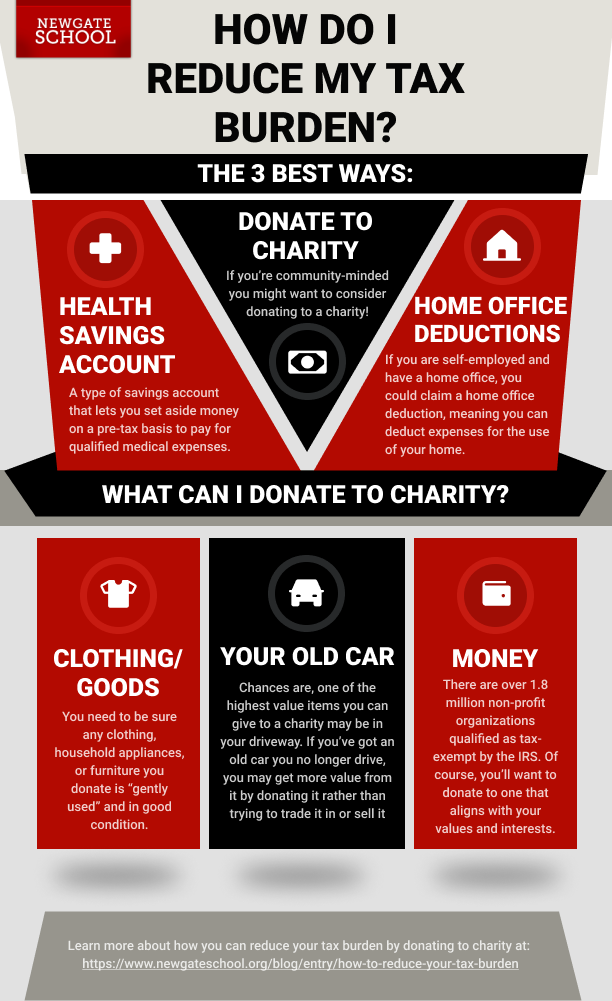

Health Savings Accounts (HSAs)

Often dubbed the “triple tax advantage” account, a Health Savings Account (HSA) is an incredibly powerful tool for those enrolled in a high-deductible health plan (HDHP).

- Pre-Tax Contributions: Contributions to an HSA are tax-deductible, reducing your AGI. If made through payroll deduction, they are also exempt from FICA taxes (Social Security and Medicare).

- Tax-Free Growth: The funds in an HSA grow tax-free. You can invest these funds similar to a retirement account, allowing your money to compound over time.

- Tax-Free Withdrawals: Qualified medical expenses can be paid for with tax-free withdrawals at any age. After age 65, funds can be withdrawn for any purpose without penalty, though non-medical withdrawals will be taxed as ordinary income, much like a Traditional IRA. HSAs can effectively serve as a supplemental retirement account for healthcare costs.

Other Pre-Tax Benefits

Several other avenues allow for pre-tax deductions that can chip away at your taxable income:

- Flexible Spending Accounts (FSAs): Both Healthcare FSAs and Dependent Care FSAs allow you to set aside pre-tax money from your paycheck to pay for qualified medical or dependent care expenses. While beneficial, FSAs are generally “use-it-or-lose-it” within the plan year, unlike HSAs.

- Student Loan Interest Deduction: You can deduct up to a certain amount of student loan interest paid during the year, even if you don’t itemize deductions. This is an “above-the-line” deduction, meaning it reduces your AGI.

- Alimony Paid (for agreements before 2019): If you pay alimony under a divorce or separation agreement executed before January 1, 2019, you may be able to deduct those payments.

Maximizing Tax Credits and Deductions

Beyond the pre-tax contributions that directly reduce your AGI, a wealth of other deductions and credits can significantly lower your taxable income or even reduce your final tax bill dollar-for-dollar. It’s crucial to understand the distinction: deductions reduce the amount of income subject to tax, while credits reduce the amount of tax you owe.

Itemized Deductions vs. Standard Deduction

Every taxpayer has a choice: take the Standard Deduction (a fixed amount determined by your filing status, adjusted annually for inflation) or Itemize Deductions (listing out specific eligible expenses). You should itemize if your total eligible itemized deductions exceed your standard deduction amount. Common itemized deductions include:

- State and Local Taxes (SALT): A combined deduction for state and local income, sales, and property taxes, capped at $10,000 per household.

- Home Mortgage Interest: Interest paid on your primary and secondary home mortgages is deductible, up to certain limits.

- Medical and Dental Expenses: Expenses exceeding a certain percentage (e.g., 7.5%) of your AGI can be deducted.

- Charitable Contributions: Donations to qualified charities, whether cash or property, are deductible. Recent tax law changes have allowed some taxpayers to claim a limited cash contribution deduction even if they take the standard deduction.

Accurate record-keeping is paramount when itemizing.

Education-Related Tax Benefits

The government offers several tax breaks for students and families paying for higher education:

- American Opportunity Tax Credit (AOTC): A partially refundable credit for qualified education expenses for eligible students during their first four years of higher education. It can be worth up to $2,500 per eligible student.

- Lifetime Learning Credit (LLC): A non-refundable credit that can help pay for undergraduate, graduate, and professional degree courses, as well as courses taken to acquire job skills. It’s worth up to $2,000 per tax return.

- Student Loan Interest Deduction: As mentioned earlier, this “above-the-line” deduction allows you to deduct up to a certain amount of student loan interest.

Business and Self-Employment Deductions

For entrepreneurs, freelancers, and small business owners, myriad deductions can dramatically reduce taxable income. These deductions relate directly to the costs of running your business:

- Home Office Deduction: If you use a portion of your home exclusively and regularly for business, you can deduct a percentage of your housing costs (rent, utilities, insurance, depreciation).

- Qualified Business Income (QBI) Deduction: Also known as the Section 199A deduction, this allows eligible self-employed individuals and small business owners to deduct up to 20% of their qualified business income.

- Business Expenses: Virtually all ordinary and necessary expenses incurred to operate your business are deductible, including office supplies, professional development, travel, business meals (50% deductible), software subscriptions, advertising, and legal/professional fees.

- Self-Employment Tax Deduction: Self-employed individuals pay both the employer and employee portions of Social Security and Medicare taxes. You can deduct one-half of your self-employment tax from your gross income.

Other Key Tax Credits

While deductions reduce taxable income, credits directly reduce your tax liability, making them incredibly valuable:

- Child Tax Credit (CTC): A credit for qualifying children, potentially partially refundable.

- Earned Income Tax Credit (EITC): A refundable credit for low-to-moderate income working individuals and families, designed to help offset income and payroll taxes.

- Child and Dependent Care Credit: For expenses incurred caring for a qualifying child or dependent to allow you to work or look for work.

- Residential Energy Credits: Credits for homeowners who make energy-efficient improvements to their homes, such as installing solar panels or energy-efficient windows.

Strategic Investing for Tax Efficiency

Beyond year-to-year deductions, a long-term strategy involving tax-efficient investing can significantly reduce your lifetime tax burden and accelerate wealth accumulation. It’s not just about what you earn, but how you grow and access it.

Tax-Advantaged Investment Accounts

While some retirement accounts offer pre-tax contributions, others focus on tax-free growth and withdrawals, which is equally crucial for tax efficiency.

- Roth IRA and Roth 401(k): Contributions to Roth accounts are made with after-tax dollars, meaning they don’t reduce your current taxable income. However, qualified withdrawals in retirement are entirely tax-free. This can be highly advantageous if you expect to be in a higher tax bracket during retirement.

- 529 Plans: Designed for education savings, 529 plans offer state tax deductions on contributions in many states, and the earnings grow tax-free. Withdrawals for qualified education expenses are also tax-free, making them an excellent vehicle for college savings.

- Annuities: While complex, deferred annuities allow investments to grow tax-deferred until withdrawal. This means you don’t pay taxes on investment gains annually, but rather when you take income from the annuity.

Capital Gains Management

How you manage your investment portfolio can significantly impact your capital gains tax liability.

- Long-Term vs. Short-Term Capital Gains: Assets held for more than one year are subject to lower long-term capital gains tax rates, which are significantly lower than ordinary income tax rates for many individuals. Conversely, assets held for one year or less are subject to short-term capital gains rates, which are taxed at your ordinary income tax rate. Strategic timing of sales is key.

- Tax-Loss Harvesting: This strategy involves selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income. By selling losing positions, you can reduce your overall taxable income and then reinvest the proceeds into other assets. This should be done carefully, adhering to wash-sale rules.

Municipal Bonds

For high-income earners, municipal bonds (or “munis”) can be an attractive option. The interest earned on municipal bonds is often exempt from federal income tax and, in many cases, from state and local taxes as well, especially if you buy bonds issued by your own state or locality. This tax exemption can make their effective yield higher than taxable bonds for those in higher tax brackets.

Long-Term Planning and Professional Guidance

Reducing taxable income is not a one-time event; it’s an ongoing process that requires diligent record-keeping, regular review, and, for many, professional expertise. A proactive approach is key to optimizing your tax position year after year.

Importance of Record Keeping

The bedrock of any effective tax reduction strategy is meticulous record-keeping. Without proper documentation, many deductions and credits cannot be claimed or substantiated if challenged by the IRS.

- Organize Everything: Keep all receipts, invoices, bank statements, investment statements, and contribution confirmations in an organized manner.

- Digital vs. Physical: While physical files work, digital solutions (scanning receipts, using expense tracking apps, cloud storage) offer greater accessibility, backup, and searchability.

- Categorize Expenses: Group similar expenses (e.g., medical, charitable, business supplies) to streamline the process when it’s time to prepare your return.

Regular Tax Planning

Don’t wait until April 14th to think about your taxes. Tax planning should be a year-round activity:

- Adjust Withholding: Review your W-4 form with your employer to ensure the correct amount of tax is being withheld from your paycheck. Too little can result in a tax bill, while too much means you’re giving the government an interest-free loan.

- Quarterly Reviews: Periodically review your income, deductions, and credits throughout the year. This is particularly important for self-employed individuals who need to make estimated tax payments.

- Anticipate Life Changes: Major life events—marriage, divorce, birth of a child, home purchase, career change—all have significant tax implications and should prompt a tax planning review.

When to Seek Professional Advice

While many tax reduction strategies can be implemented independently, there are times when the complexity of your financial situation warrants professional guidance.

- Complex Financial Situations: If you own a business, have significant investments, deal with foreign income, or have undergone major life changes, a professional can help navigate the intricacies.

- Ensuring Compliance: Tax laws are constantly evolving. A Certified Public Accountant (CPA) or Enrolled Agent (EA) stays abreast of these changes, ensuring you remain compliant while maximizing your benefits.

- Identifying Missed Opportunities: A tax professional can often identify deductions or credits you might have overlooked, providing tailored advice based on your unique circumstances. They can also help with long-term strategic tax planning, such as estate planning or retirement distribution strategies.

Reducing taxable income is a foundational pillar of sound financial management. By consistently applying the strategies outlined—from leveraging pre-tax contributions and maximizing deductions and credits to employing tax-efficient investment approaches and engaging in proactive planning—you can significantly enhance your financial health. Remember, the goal is not merely to save money on taxes, but to empower yourself with greater financial control and accelerate your journey towards long-term wealth and security. Embrace continuous learning and don’t hesitate to consult with qualified tax professionals to navigate the nuances and ensure you’re making the most informed decisions for your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.