Deciding when to claim Social Security is arguably the most significant financial decision most Americans will make in their lifetime. Unlike a traditional savings account or a 401(k), Social Security acts as a government-backed, inflation-adjusted annuity that lasts for the duration of your life. However, the timing of your claim can result in a permanent difference of hundreds of thousands of dollars in cumulative lifetime benefits. While the earliest possible age to claim is 62 and the latest age to see benefit increases is 70, the “right” time is rarely a matter of luck; it is a matter of strategic financial planning.

In this guide, we will analyze the trade-offs associated with different filing ages, the impact of life expectancy on your “breakeven” point, and how to integrate Social Security into a broader personal finance strategy.

Understanding the Mechanics of the Social Security Timeline

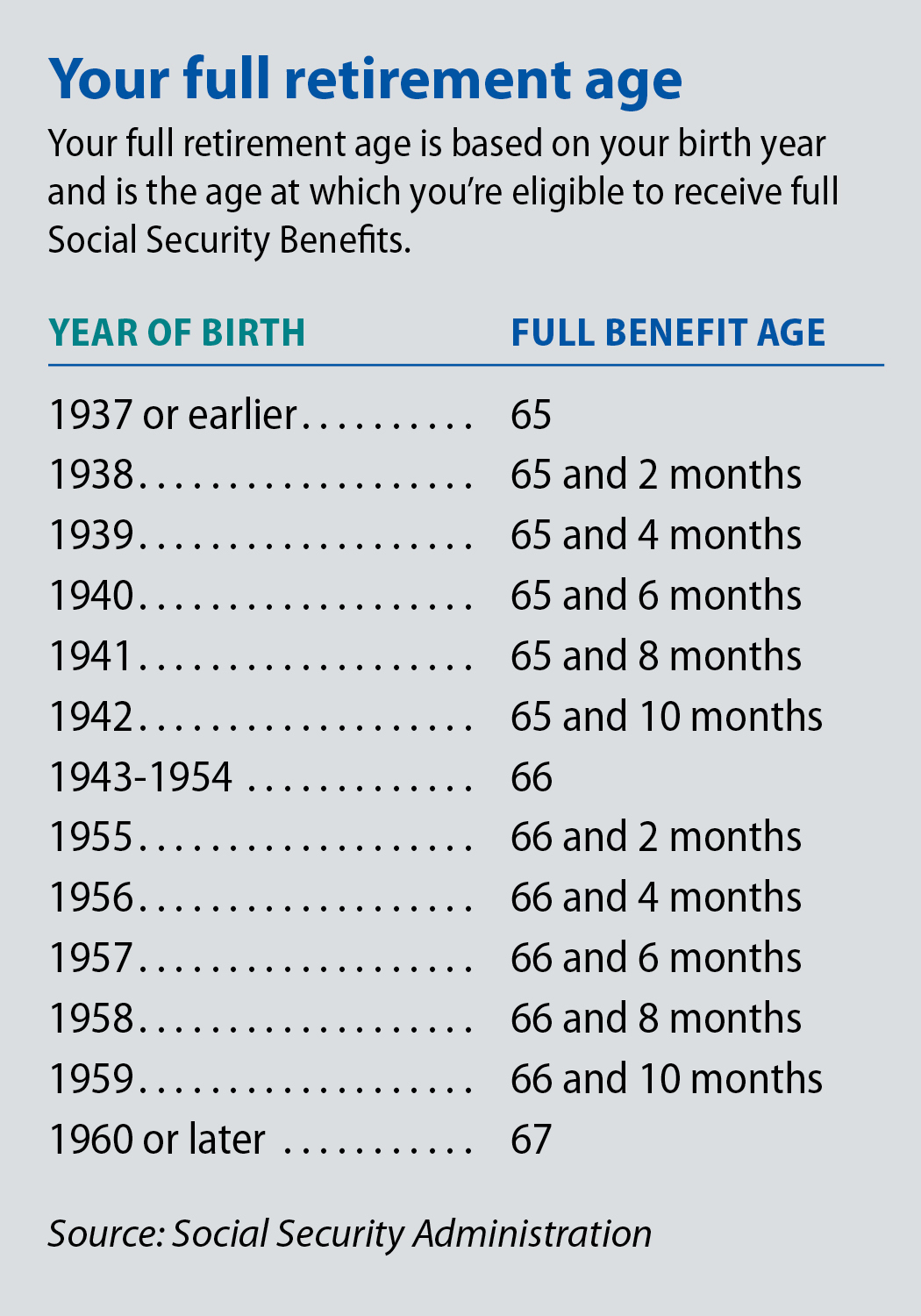

To make an informed choice, you must first understand how the Social Security Administration (SSA) calculates your “Primary Insurance Amount” (PIA). This is the monthly benefit you are entitled to at your Full Retirement Age (FRA). For those born in 1960 or later, the FRA is 67.

Early Filing at Age 62: The Cost of Immediacy

Filing at age 62 is the most common choice, often driven by a desire for immediate cash flow or health concerns. However, this comes at a steep price. If your FRA is 67 and you file at 62, your monthly check is permanently reduced by 30%. This reduction is actuarial; the SSA assumes you will receive more checks over a longer period, so each individual check must be smaller. For many, the immediate liquidity is helpful, but it leaves very little room for error if they live into their 90s.

The Full Retirement Age (FRA) Benchmark

Your FRA is the “neutral” point in the Social Security system. At this age, you receive 100% of your earned benefit. Perhaps more importantly, once you reach your FRA, the “Earnings Test” no longer applies. If you claim benefits before your FRA while still working, the SSA may temporarily withhold a portion of your benefits if your income exceeds certain thresholds. Once you hit your FRA, you can earn an unlimited amount of income without any reduction in your Social Security checks.

Delayed Retirement Credits: The Power of 70

For every year you delay claiming Social Security past your FRA up until age 70, your benefit increases by approximately 8% per year in “delayed retirement credits.” This is a guaranteed, risk-free return that is virtually impossible to match in the private market. By waiting until age 70, a person with an FRA of 67 would receive 124% of their PIA. Over the course of a retirement lasting 20 or 30 years, this compounded increase serves as a powerful hedge against inflation and longevity risk.

Financial Variables and the Breakeven Analysis

When viewing Social Security through the lens of personal finance, the goal is often to maximize the total “lifetime wealth” generated by the system. This requires a “breakeven analysis”—calculating the age at which the total value of higher monthly payments from a delayed claim surpasses the total value of smaller payments received starting at an earlier age.

Evaluating Life Expectancy and Health

The “breakeven” age for delaying from 62 to 67 is typically around age 77. If you delay until 70, the breakeven point compared to age 62 is often around age 80. Therefore, the decision is largely a bet on your own longevity. If you have chronic health issues or a family history of shorter lifespans, claiming early may be the mathematically superior choice. Conversely, if you are in good health and have relatives who lived into their late 80s or 90s, delaying as long as possible is almost always the better financial move.

The Impact of Continued Employment

If you are still working in your early 60s, the “Money” niche perspective suggests that claiming Social Security is often counterproductive. Not only does the aforementioned Earnings Test reduce your benefits if you earn over the annual limit ($22,320 in 2024), but those benefits are also subject to income tax. If you are in a high tax bracket due to a professional salary, taking Social Security early might result in you keeping only a fraction of the check after taxes and withholdings. In this scenario, using your salary to fund your lifestyle while letting your Social Security benefit grow at 8% per year is a superior capital allocation strategy.

Tax Implications of Social Security Benefits

Social Security is not always tax-free. Depending on your “combined income” (adjusted gross income + tax-exempt interest + half of your Social Security benefits), you may pay federal income tax on up to 85% of your benefits. For high-net-worth individuals, managing the timing of these benefits is a critical component of tax planning. Claiming later can sometimes allow for “tax-efficient windows” earlier in retirement where you can perform Roth IRA conversions at lower tax rates before the large Social Security checks begin.

Strategic Considerations for Couples and Survivors

Social Security planning is not a solo endeavor for married couples. The rules regarding spousal and survivor benefits add a layer of complexity that can be leveraged to increase a household’s total net worth.

Coordinating Spousal Benefits

Under current law, a spouse is entitled to either their own retirement benefit or 50% of their partner’s FRA benefit, whichever is higher. Strategic couples often look at their benefits as a joint portfolio. A common strategy involves the lower-earning spouse claiming their benefit early to provide some household cash flow, while the higher-earning spouse delays until age 70. This ensures that the largest possible benefit is maximized for the long term.

Survivor Benefits: Protecting the Long-Term Security of a Spouse

One of the most overlooked aspects of Social Security is its role as a form of life insurance. When one member of a couple passes away, the smaller of the two Social Security checks disappears, and the survivor keeps the larger one. By having the “primary breadwinner” delay until age 70, they are not just increasing their own check; they are effectively buying a larger “life insurance policy” for the surviving spouse. For a widow or widower who may live decades longer than their partner, that maximized benefit can be the difference between aging in place and financial hardship.

Incorporating Social Security into a Broader Portfolio

In the world of wealth management, Social Security should be viewed as the “fixed income” or “bond” portion of your retirement portfolio. Because it is adjusted for inflation and backed by the federal government, it provides a safety net that allows you to be more or aggressive—or more conservative—with your other investments.

Bridging the Gap with 401(k) and IRA Withdrawals

Many retirees are afraid to delay Social Security because they need the income to retire at 65. However, from a financial engineering standpoint, it often makes more sense to “spend down” a portion of your 401(k) or traditional IRA between ages 65 and 70 to “buy” the higher Social Security benefit. By using your invested assets to “bridge the gap,” you are essentially trading volatile market assets for a guaranteed, inflation-protected stream of income. This reduces “sequence of returns risk,” which is the risk that a market downturn early in retirement will permanently deplete your portfolio.

Inflation Protection and the COLA Advantage

One of the most valuable features of Social Security is the Cost-of-Living Adjustment (COLA). Unlike most private annuities or corporate pensions, Social Security benefits increase along with the Consumer Price Index. When you delay your benefit, the COLA is applied to a larger base amount. An 8% increase on a $3,000 check is significantly more impactful than an 8% increase on a $2,000 check. In an era of economic uncertainty and fluctuating inflation, the value of a maximized, inflation-adjusted benefit cannot be overstated.

Conclusion: Making the “Right” Choice for Your Financial Future

Ultimately, the decision of when to collect Social Security is a balance of mathematics, health, and personal philosophy. While the “Money” perspective emphasizes that delaying until age 70 offers the highest expected return and the best protection against longevity risk, individual circumstances always dictate the final move.

If you need the money to survive, have poor health, or have a unique investment opportunity that exceeds an 8% guaranteed return, claiming early is a valid choice. However, for the majority of Americans, Social Security is the most stable pillar of their financial house. By treating it as a strategic asset—understanding the breakeven points, accounting for tax implications, and coordinating with a spouse—you can transform a standard government benefit into a powerful engine for long-term financial security. Don’t view it as a race to get your money back from the system; view it as a strategic investment in your future self.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.