For millions of Americans, Social Security benefits represent a cornerstone of their retirement security, providing a reliable income stream that can supplement pensions, 401(k)s, and personal savings. Yet, despite its critical role, many individuals find themselves asking a fundamental question: “How much Social Security will I actually receive?” The answer, as with many financial matters, is not a simple fixed number. It’s a complex calculation influenced by a multitude of factors, unique to each individual’s work history, earnings, and claiming decisions.

Understanding how your Social Security benefits are determined is not just an academic exercise; it’s a vital component of robust retirement planning. By demystifying the calculation process and identifying the variables that impact your payout, you can make informed decisions today that profoundly affect your financial well-being in the future. This article will break down the intricacies of Social Security benefits, guiding you through the calculation process, the key factors influencing your amount, and strategies to help you maximize this essential retirement income.

The Fundamentals of Social Security Benefits Calculation

At its core, your Social Security benefit amount is directly linked to your lifetime earnings. The Social Security Administration (SSA) uses a specific formula to translate your work history into a monthly benefit.

Your Earnings History: The Foundation

The SSA tracks your earnings throughout your career, specifically focusing on the 35 years in which you earned the most. It’s crucial to understand that only earnings up to the “Social Security Wage Base” for each year are counted. This wage base is the maximum amount of earnings subject to Social Security taxes each year and typically increases annually to account for inflation and wage growth. If you work fewer than 35 years, “zero” earnings will be factored into those missing years, potentially lowering your overall average. Conversely, if you work more than 35 years, your lowest-earning years will be dropped in favor of your highest.

Average Indexed Monthly Earnings (AIME)

Once your highest 35 years of earnings are identified, the SSA “indexes” those earnings. Indexing adjusts your past earnings to reflect the general increase in wages that has occurred since the year you earned the money. This process ensures that your past earnings are expressed in terms of current dollar values, providing a fairer representation of your lifetime contributions. After indexing, these adjusted annual earnings are summed and then divided by the number of months in 35 years (420 months) to arrive at your Average Indexed Monthly Earnings (AIME). The AIME is a crucial intermediate step in determining your benefit.

Primary Insurance Amount (PIA)

Your AIME is then used to calculate your Primary Insurance Amount (PIA). The PIA is the benefit you would receive if you start collecting Social Security benefits at your Full Retirement Age (FRA). The SSA uses a three-part progressive formula, applying “bend points” to your AIME. These bend points mean that lower income brackets of your AIME are replaced at a higher percentage than higher income brackets. This progressive formula is designed to ensure that lower-income workers receive a proportionately higher benefit relative to their earnings than higher-income workers. For example, a certain percentage of the first “x” dollars of your AIME is included, a lower percentage of the next “y” dollars, and an even lower percentage for the amount above that. These bend points are also indexed to national wage growth each year.

Spousal and Dependent Benefits

It’s also important to remember that Social Security benefits extend beyond just the primary worker. Spouses, ex-spouses, and eligible dependent children may also be able to claim benefits based on your work record, typically up to 50% of your PIA, provided certain conditions are met. This can significantly increase the total amount of Social Security income a family receives.

Factors Influencing Your Benefit Amount

While your earnings history forms the bedrock of your benefit calculation, several other critical factors can dramatically alter the final amount you receive each month.

When You Claim: The Age Factor

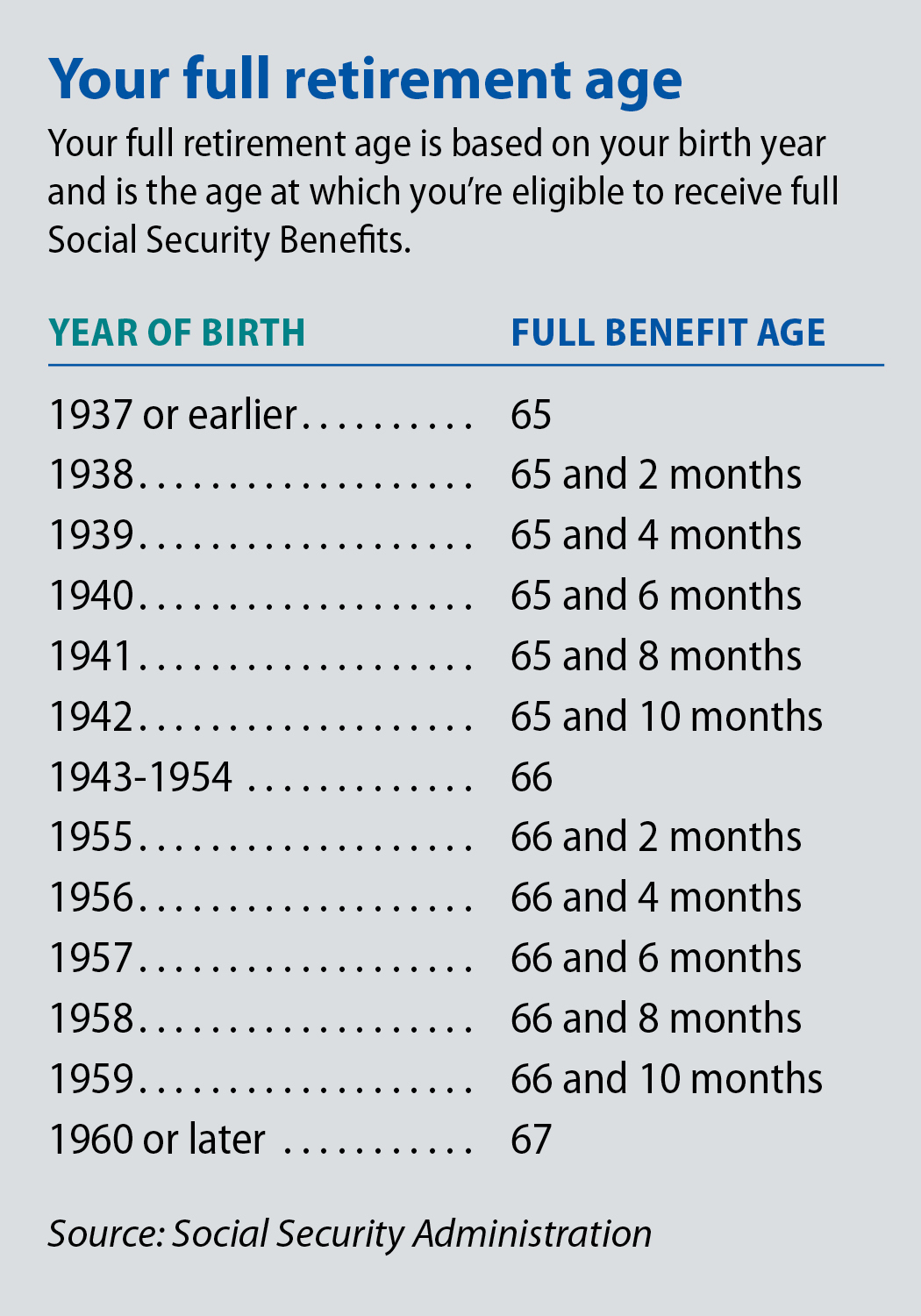

Perhaps the most significant decision impacting your Social Security benefit is when you choose to start collecting. Your Full Retirement Age (FRA) is the age at which you are entitled to 100% of your PIA. FRA varies based on your birth year:

-

Born 1943-1954: FRA is 66.

-

Born 1960 or later: FRA is 67.

-

For those born between 1955 and 1959, FRA gradually increases from 66 and 2 months to 66 and 10 months.

-

Claiming Early (as early as age 62): If you claim benefits before your FRA, your monthly benefit will be permanently reduced. The reduction can be substantial, as much as 30% if you claim at age 62 with an FRA of 67. This reduction accounts for the fact that you will likely receive benefits for a longer period.

-

Claiming at Full Retirement Age: You receive 100% of your PIA.

-

Delaying Claiming (up to age 70): For each year you delay claiming past your FRA, up to age 70, your monthly benefit increases by a certain percentage, known as “Delayed Retirement Credits.” These credits currently add 8% per year to your benefit, compounding annually. Delaying from FRA (e.g., 67) to age 70 can result in a permanent increase of 24% (3 years x 8% per year) to your monthly benefit, a powerful incentive for those who can afford to wait.

Your Work History: The 35-Year Rule

As mentioned, the SSA uses your 35 highest-earning years. If you don’t have 35 years of earnings, zero-earning years will be factored into the average, reducing your AIME and consequently your PIA. Working longer, particularly if your later career years are higher-earning, can replace those lower- or zero-earning years, thereby increasing your average.

Maxed-Out Earnings and the Social Security Wage Base

The Social Security wage base sets a limit on the amount of earnings subject to Social Security taxes and, therefore, counted in your benefit calculation. For instance, in 2024, the wage base was $168,600. If you earned $200,000 in 2024, only the first $168,600 would count towards your Social Security benefit calculation. Earning above the wage base in a given year does not further increase your future Social Security benefits, although it may still contribute to your overall 35 highest earning years.

Other Income and Taxes (Provisional Income, WEP/GPO)

It’s also important to note that your Social Security benefits can be taxable. If your “provisional income” (which includes adjusted gross income, tax-exempt interest, and 50% of your Social Security benefits) exceeds certain thresholds, a portion of your benefits may be subject to federal income tax.

Furthermore, if you receive a pension from employment not covered by Social Security (e.g., some government employees) or if you are a spouse or widow(er) receiving a government pension based on work not covered by Social Security, your Social Security benefits might be reduced by the Windfall Elimination Provision (WEP) or the Government Pension Offset (GPO), respectively. These provisions are designed to prevent “double-dipping” benefits that would not otherwise be allowed.

Estimating Your Social Security Benefits

Given the complexity, how can you get a reliable estimate of your future Social Security benefits? Fortunately, the SSA provides several excellent tools and resources.

Using Your Social Security Statement

The most accurate and personalized estimate comes directly from the Social Security Administration. The SSA mails annual Social Security Statements to workers aged 60 and over who are not yet receiving benefits. You can also create an account online at SSA.gov to access your statement at any age. This statement provides:

- A detailed record of your annual earnings history (check this for accuracy!).

- Estimated benefits at age 62, at your Full Retirement Age, and at age 70.

- Estimates for disability and survivor benefits.

Reviewing your statement regularly is critical, not only to plan your retirement but also to ensure your earnings record is accurate. Errors could lead to lower benefits down the line.

Online Calculators and Tools (SSA.gov)

The SSA website (www.ssa.gov) offers various online calculators that allow you to project your benefits under different scenarios. You can input different retirement ages, future earnings estimates, and even explore how survivor benefits or disability benefits might work. These tools are invaluable for scenario planning and understanding the impact of different claiming strategies.

Financial Planners and Professional Guidance

For a more comprehensive and personalized approach, especially when integrating Social Security into a broader retirement strategy, consulting with a qualified financial planner can be highly beneficial. They can help you understand the nuances, model various claiming strategies specific to your financial situation, and coordinate your Social Security benefits with other income sources, savings, and investments.

Strategies to Maximize Your Social Security Benefits

Understanding the calculation is the first step; the next is strategically planning to optimize your benefits.

Working Longer and Higher Earned Income

Since your 35 highest-earning years are used, continuing to work, especially if you’re in your peak earning years, can significantly boost your AIME. Replacing lower-earning years from early in your career with higher earnings later on will directly increase your PIA. Even part-time work in retirement can contribute to replacing a low or zero-earning year.

Strategic Claiming Age Decisions

This is arguably the most impactful decision.

- Delaying to Age 70: If you are in good health, have sufficient other retirement income, and no immediate need for the funds, delaying benefits until age 70 is often the best strategy to maximize your individual monthly benefit. The 8% annual increase from Delayed Retirement Credits is a powerful guaranteed return that is difficult to replicate elsewhere.

- Coordinating with a Spouse: For married couples, the decision of when each spouse claims benefits becomes even more strategic. One spouse might claim early to provide income, while the higher earner delays until age 70 to maximize their benefit, which will also provide a higher survivor benefit if they pass away first. Various “file and suspend” or “restricted application” strategies (though some have been phased out) historically allowed for sophisticated claiming plans. It’s vital to stay updated on current rules and discuss options with a financial advisor.

Understanding Cost-of-Living Adjustments (COLAs)

Social Security benefits are designed to maintain their purchasing power over time. Each year, benefits are subject to a Cost-of-Living Adjustment (COLA), which is based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If inflation rises, your monthly benefit will generally increase, helping you keep pace with rising costs. While you cannot control COLAs, understanding they exist adds another layer of security to your benefits.

Social Security in Your Overall Retirement Plan

Social Security was never intended to be your sole source of retirement income, but rather a vital leg of a three-legged stool (Social Security, pensions/workplace plans, and personal savings).

Integrating Benefits with Savings and Investments

When planning for retirement, view your projected Social Security benefits as a guaranteed income floor. This allows you to plan how much you need to save and invest in your 401(k), IRA, and other accounts to cover the remainder of your desired retirement lifestyle. Knowing your estimated benefits helps you gauge your savings gap and adjust your contribution rates accordingly.

Addressing Potential Shortfalls

If your estimated Social Security benefits, combined with other income sources, fall short of your projected retirement expenses, this foresight allows you to take corrective action. This could involve increasing savings, adjusting investment strategies, delaying retirement, or planning for part-time work during your early retirement years.

The Future of Social Security: What to Watch For

While Social Security is currently solvent and expected to pay full benefits for several decades, long-term projections indicate that without congressional action, the trust funds may eventually only be able to pay a percentage of promised benefits. While this does not mean Social Security will “run out,” it highlights the importance of staying informed about proposed changes and building a diverse retirement portfolio that isn’t solely reliant on Social Security.

In conclusion, understanding “how much Social Security benefits” you can expect is a fundamental aspect of financial literacy and retirement preparedness. By grasping the calculation methodology, recognizing the critical factors that influence your payout, and strategically planning your claiming age, you empower yourself to make the most of this invaluable program. Proactive engagement with your Social Security statement, utilizing online tools, and seeking professional advice will ensure that this essential income stream plays its maximum role in securing your financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.