For many Americans, Social Security represents a vital financial cornerstone, offering a lifeline in retirement, during disability, or to survivors. However, a common question arises for those who choose or need to continue working while collecting these benefits: “How much can I actually earn without jeopardizing my Social Security payments?” The answer is nuanced, depending primarily on your age relative to your “Full Retirement Age” (FRA) and the specific rules governing Social Security’s earnings test. Understanding these regulations is crucial for effective financial planning, ensuring you maximize your retirement income without unexpected reductions.

This article delves into the intricacies of earning while collecting Social Security, shedding light on the earnings limits, the mechanisms of benefit reduction, and strategic considerations for optimizing your financial future. We’ll cut through the confusion to provide a clear roadmap for navigating this important aspect of personal finance.

Navigating the Social Security Earnings Test

The Social Security Administration (SSA) implements an “earnings test” to determine if your benefits should be reduced if you work and earn above certain thresholds. This test is specifically designed for individuals who have not yet reached their Full Retirement Age (FRA). The underlying principle is that Social Security retirement benefits are primarily intended for those who have largely exited the workforce.

The Rationale Behind Earnings Limits

The Social Security program was conceived as a social insurance system to provide income primarily to retired workers, their spouses, and dependents. When individuals claim benefits before their Full Retirement Age (FRA) while still actively working and earning above a specified amount, the SSA’s earnings test comes into play. The rationale is to ensure that benefits are directed toward individuals who genuinely rely on Social Security as their primary or sole source of income in retirement. It’s not a penalty for working, but rather a mechanism to balance the system, allocating resources to those deemed most in need of retirement income support, rather than supplementing robust working salaries for those below FRA. Once you reach your FRA, this earnings test largely disappears, reflecting the system’s acknowledgment that you’ve reached the traditional retirement threshold.

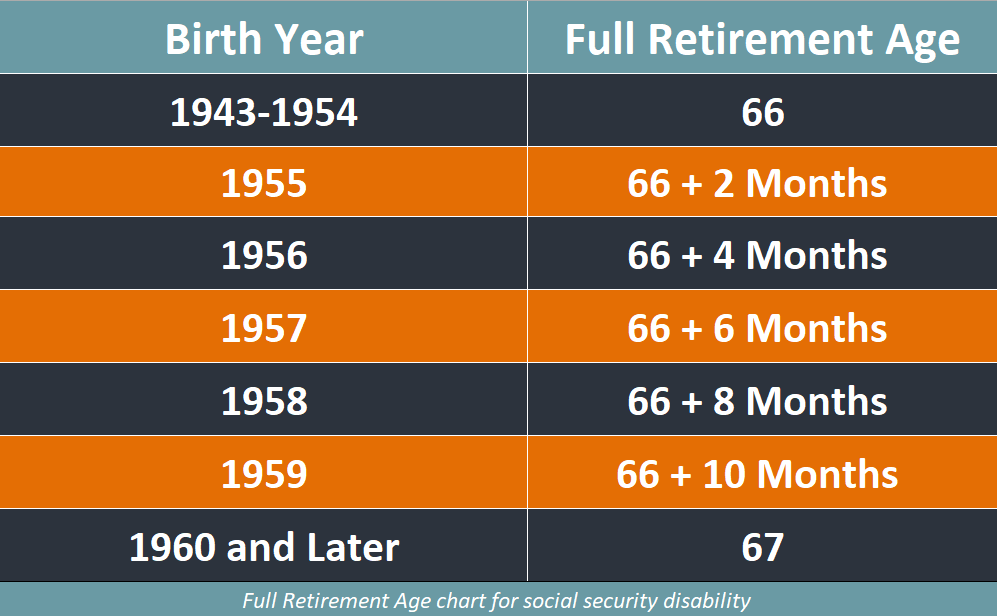

Identifying Your Full Retirement Age (FRA)

Your Full Retirement Age (FRA) is a pivotal concept in Social Security planning. It’s the age at which you are entitled to receive 100% of your primary insurance amount (PIA), the benefit calculated from your earnings record, without any reductions for claiming early or increases for delaying past FRA. Your FRA is determined by your birth year, reflecting historical adjustments to the Social Security system. For those born between 1943 and 1954, FRA is 66. It then gradually increases by two months for every birth year, reaching age 67 for anyone born in 1960 or later. Understanding your specific FRA is fundamental, as it dictates when the earnings test ceases to apply and when you can earn an unlimited amount without impacting your Social Security benefits. Knowing this age is the first step in strategic planning for your retirement income.

What Counts as “Earnings”?

When the Social Security Administration refers to “earnings” for the purpose of the earnings test, it’s essential to understand precisely what income sources are included and excluded. The earnings test primarily focuses on earned income, which encompasses wages you receive from an employer or net earnings from self-employment. This means if you’re working a job, your gross pay (before taxes and other deductions) counts. If you’re self-employed, your net profit after allowable business expenses are deducted is what the SSA considers.

Crucially, many other forms of income are not counted toward the earnings limit. These include pensions, annuities, investment income (like interest, dividends, or capital gains), rental income from properties not actively managed as a business, and government or military retirement benefits. Gifts and inheritances also do not count. This distinction is vital for financial planning, as it means you can have substantial income from these unearned sources without it affecting your Social Security benefits, regardless of your age. The earnings test solely targets income derived from active work.

Specific Earnings Limits and Benefit Reductions

The exact amount you can earn before your Social Security benefits are affected depends entirely on whether you are working before the year you reach your Full Retirement Age (FRA), in the year you reach your FRA, or at or after your FRA. Each scenario has distinct earnings limits and benefit reduction rules.

Working Before Your Full Retirement Age (FRA)

If you are collecting Social Security benefits and are below your Full Retirement Age (FRA) for the entire year, you are subject to the strictest earnings limits. For 2024, this annual earnings limit is $22,320. If your earned income exceeds this threshold, the Social Security Administration will reduce your benefits by $1 for every $2 you earn above the limit. For example, if you earn $24,320, which is $2,000 over the limit, your annual benefits will be reduced by $1,000 ($2,000 / 2). This reduction applies to your total annual benefits, potentially impacting every monthly payment. It’s imperative to track your earnings closely throughout the year if you fall into this category, as exceeding the limit can significantly diminish your expected Social Security income.

The Year You Reach Your Full Retirement Age

A different, more generous set of rules applies in the calendar year you reach your Full Retirement Age (FRA). For 2024, the earnings limit for this specific period is significantly higher: $59,520. More importantly, this limit only applies to earnings made in the months prior to your birth month, when you officially attain FRA. Once you reach your FRA in your birth month, the earnings test no longer applies for the remainder of that year, or any subsequent year.

The benefit reduction rate for this period is also different: the SSA will withhold $1 in benefits for every $3 you earn above the $59,520 limit. For instance, if you earn $62,520 in the months before your FRA, which is $3,000 over the limit, your benefits will be reduced by $1,000 ($3,000 / 3). This distinction is crucial for individuals who plan to work part of the year they turn FRA, allowing them to earn substantially more without as severe a reduction compared to years fully before FRA.

Earning at or After Your Full Retirement Age (FRA)

This is the most straightforward scenario: once you reach your Full Retirement Age (FRA), the Social Security earnings test completely ceases to apply. This means you can earn an unlimited amount of income from work, whether through wages or self-employment, without any reduction to your Social Security benefits. Your monthly benefit amount will be paid in full, regardless of how much you continue to earn. This is a significant milestone for many retirees, as it removes a major constraint on their ability to supplement their retirement income through work. Many individuals choose to delay claiming benefits until FRA precisely for this reason, or even beyond, to take advantage of delayed retirement credits, knowing that their future work won’t impact their Social Security. This freedom allows for greater flexibility in retirement planning and continued engagement in the workforce if desired.

The “First Year of Retirement” Special Rule

There’s a special rule designed for individuals who start collecting Social Security benefits mid-year and had high earnings in the preceding months before they intended to “retire” or reduce their work hours. This is known as the “monthly earnings test.” In your first year of collecting benefits, if you are below your FRA, the SSA can apply a monthly earnings limit instead of the annual limit. For 2024, this monthly limit is $1,860. If your earnings for the year would cause your benefits to be withheld under the annual test, but you have one or more months in which you earned below the monthly limit (and did not perform substantial services in self-employment), the SSA can pay you benefits for those “low earning” months. This prevents individuals from losing a significant portion of benefits for the entire year just because of high earnings in the early part of the year before they stopped or significantly reduced working. This rule usually only applies in the first year benefits are claimed; after that, the annual earnings test typically applies.

Practical Considerations and Reporting Requirements

Navigating the Social Security earnings test involves more than just understanding the limits; it also requires proactive engagement with the Social Security Administration (SSA). Proper reporting and awareness of how withheld benefits are treated are essential for a smooth experience.

How Benefits Are Withheld and Recalculated

When you exceed the earnings limit before your FRA, the Social Security Administration (SSA) will withhold your benefits to cover the reduction amount. They typically do this by withholding entire monthly checks until the total reduction amount is reached. For instance, if your annual benefit reduction is $2,000 and your monthly benefit is $1,000, the SSA might withhold two full months of benefits.

However, these withheld benefits are not permanently lost. At your Full Retirement Age (FRA), the SSA will recalculate your benefit amount to account for the months in which benefits were withheld due to the earnings test. This process, known as “adjustment of the reduction factor,” effectively credits you for the months you didn’t receive benefits. As a result, your future monthly benefit amount will be slightly higher, reflecting the fact that you effectively started receiving benefits later for those withheld months. While the immediate impact is a temporary loss of income, there’s a long-term adjustment to your benefit rate that partially compensates for it, increasing your benefit for the rest of your life.

The Importance of Accurate Earnings Reporting

Accurate and timely reporting of your estimated and actual earnings to the Social Security Administration (SSA) is critical. If you are receiving benefits and working below your Full Retirement Age (FRA), you are required to report your expected earnings for the current year. This allows the SSA to adjust your benefits proactively, preventing overpayments that would later need to be repaid. If your actual earnings differ from your estimates, you must update the SSA promptly.

Failure to report earnings accurately can lead to significant issues. If the SSA determines you were overpaid due to unreported earnings, they will demand repayment. This could involve withholding future benefits or requiring a direct payment. Conversely, if you overestimated your earnings and had too many benefits withheld, the SSA will eventually pay you back, but proactive reporting ensures you receive your rightful benefits without unnecessary delays or complications. Keeping the SSA informed helps prevent financial surprises and ensures compliance with their regulations.

Tax Implications of Earned Income and Benefits

It’s important to remember that earning while collecting Social Security can have significant tax implications, not just on your Social Security benefits, but on your overall income tax liability. Social Security benefits themselves can become taxable if your “combined income” exceeds certain thresholds. Your combined income is generally calculated as your adjusted gross income (AGI) plus any tax-exempt interest income, plus one-half of your Social Security benefits.

For single filers, if your combined income is between $25,000 and $34,000, up to 50% of your benefits may be taxable. If it exceeds $34,000, up to 85% of your benefits may be taxable. For married couples filing jointly, these thresholds are $32,000 and $44,000, respectively. Earning additional income from work, even if it doesn’t trigger the Social Security earnings test (e.g., if you are at or past FRA), can push your combined income above these thresholds, leading to a portion of your Social Security benefits being included in your taxable income. This means a higher tax bill. Understanding this interaction is crucial for comprehensive tax planning in retirement.

Strategic Planning for Maximizing Your Retirement Income

The decision to work while collecting Social Security is a personal one, often driven by financial need, a desire to stay active, or both. Strategic planning can help you navigate the rules effectively, ensuring your choices align with your broader retirement goals.

The Choice: Work and Collect vs. Defer and Grow

One of the most significant strategic decisions for individuals approaching retirement involves weighing the benefits of working while collecting Social Security versus deferring benefits to allow them to grow. If you are below your Full Retirement Age (FRA) and expect to earn above the annual limit, your Social Security benefits will be reduced. In this scenario, you might consider deferring your Social Security claim until you reach FRA or even later (up to age 70) to allow your benefits to accrue delayed retirement credits, resulting in a higher monthly payment for life.

While working and collecting provides immediate income, the benefit reductions can be substantial. Deferring, on the other hand, means forgoing current income, but it secures a larger, permanent monthly benefit in the future. The optimal choice depends on several factors: your current financial needs, your health, your anticipated longevity, and your ability to generate income from other sources. A careful analysis of these trade-offs, often with a financial advisor, is essential to make an informed decision that maximizes your long-term retirement security.

Integrating Earned Income into Your Overall Retirement Strategy

Integrating earned income with your Social Security benefits and other retirement assets requires a holistic approach to financial planning. Beyond just the earnings test, consider how earned income affects your overall tax situation, your savings rates, and your spending patterns. If working past FRA, for instance, additional income can reduce the need to draw down investment portfolios during market downturns, preserving capital for longer. It can also enable you to contribute more to tax-advantaged retirement accounts, even in your later years, if you have earned income.

Think of earned income not in isolation, but as one component of a multi-faceted retirement strategy. It can provide flexibility, cover unexpected expenses, fund discretionary spending, or even allow for additional savings that boost your long-term financial resilience. A well-integrated strategy considers all income sources—Social Security, pensions, investments, and earned income—to create a sustainable and robust financial plan for your entire retirement journey.

Beyond the Earnings Test: Other Income Streams

While the Social Security earnings test specifically targets income from work, it’s crucial to remember that many other income streams are entirely unaffected. Diversifying your income sources is a cornerstone of robust retirement planning. Pensions, private annuities, distributions from 401(k)s, IRAs, and other retirement accounts, as well as investment income from interest, dividends, and capital gains, do not count towards the Social Security earnings limit. This means you can generate substantial income from these avenues without any impact on your Social Security benefits, regardless of your age. Developing these other income streams through disciplined saving and investing throughout your working life provides significant financial flexibility and security in retirement, reducing reliance on earned income and mitigating the effects of the earnings test if you choose to work before your FRA.

Conclusion

Understanding how much you can earn while collecting Social Security is not merely about adhering to rules; it’s about strategic financial planning for your future. The earnings test, with its varying limits and reduction rates based on your age relative to your Full Retirement Age, is a critical factor for anyone considering working in retirement. While earning before FRA can lead to benefit reductions, these withheld amounts are often credited back through a higher future benefit. At or after your FRA, the constraints disappear entirely, offering complete freedom to earn as you wish.

The interplay between earned income, Social Security benefits, and tax implications is complex. By familiarizing yourself with these guidelines, accurately reporting your earnings, and integrating work into a comprehensive retirement plan that includes diverse income streams, you can make informed decisions that maximize your financial well-being and ensure a secure and fulfilling retirement.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.