In the intricate world of personal finance, the term “interest” holds a significant, multifaceted meaning. Beyond its general definition of curiosity or engagement, in financial vernacular, “interest” represents the cost of borrowing money or the reward for lending it. It is the lifeblood of savings accounts, the engine of investment growth, and a crucial component in assessing debt. For anyone aspiring to build wealth, grow their savings, or simply make their money work harder for them, understanding “how to find interest” — in terms of identifying opportunities to earn it and optimizing its accumulation — is a fundamental skill. This comprehensive guide will navigate the landscape of financial interest, exploring its mechanics, traditional and modern avenues for earning it, strategies for maximization, and the tools available to empower your financial journey.

Understanding the Fundamentals of Financial Interest

Before embarking on the quest to find interest, it’s paramount to grasp its foundational concepts. Financial interest isn’t a monolith; it manifests in various forms, each with distinct implications for your money.

Simple vs. Compound Interest: The Power of Growth

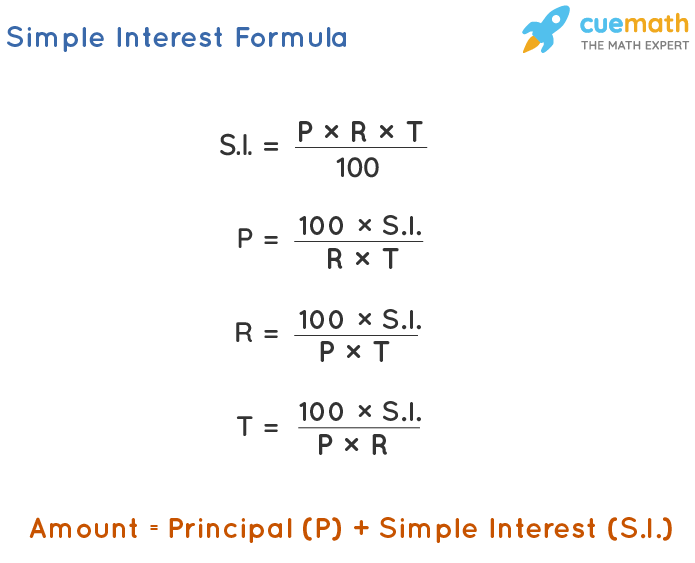

The most crucial distinction to understand is between simple and compound interest. Simple interest is calculated solely on the principal amount of a loan or deposit. For instance, if you deposit $1,000 into an account earning 5% simple annual interest, you’ll earn $50 each year, and your total will be $1,050 after year one, $1,100 after year two, and so on.

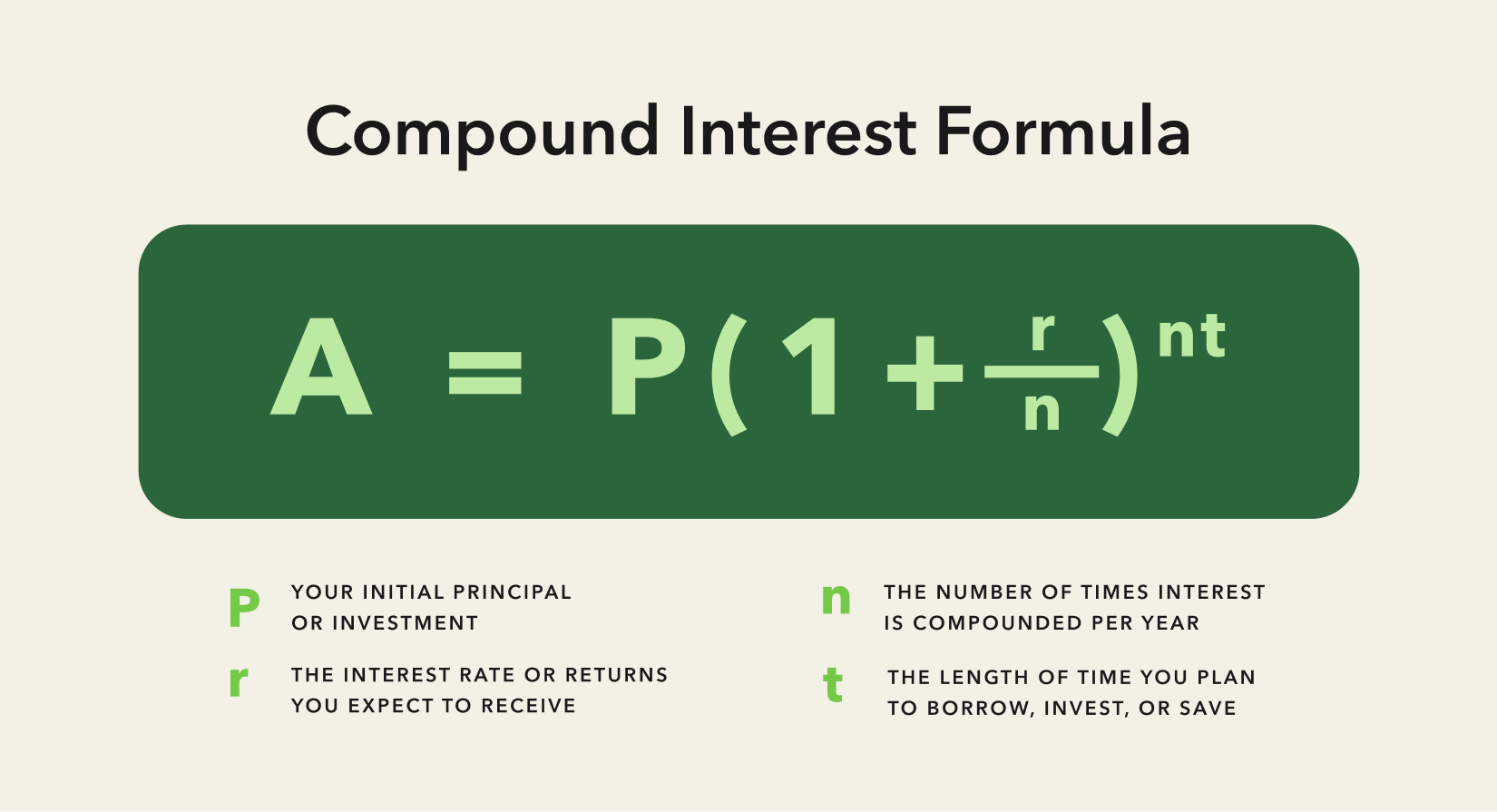

Compound interest, however, is often lauded as the “eighth wonder of the world” for good reason. It’s calculated on the initial principal and on the accumulated interest from previous periods. Using the same example, if your $1,000 earns 5% compound annual interest, you’d earn $50 in the first year. In the second year, the 5% would be calculated on $1,050, yielding $52.50. This seemingly small difference accelerates over time, leading to exponential growth. The more frequently interest is compounded (e.g., daily, monthly, quarterly), the faster your money grows. Understanding and harnessing compound interest is central to long-term wealth accumulation.

Key Interest Rate Terminology: APY, APR, Fixed vs. Variable

Navigating financial products requires familiarity with specific terms:

- Annual Percentage Yield (APY): This represents the effective annual rate of return, taking into account the effect of compounding interest. APY is particularly useful when comparing savings accounts or CDs, as it provides a true picture of how much you’ll earn over a year.

- Annual Percentage Rate (APR): This is the yearly interest rate charged for borrowing money, without taking into account compounding. APR is commonly used for loans, credit cards, and mortgages. While it indicates the base cost, comparing different APRs can be tricky if they have different compounding frequencies.

- Fixed Interest Rates: These rates remain constant throughout the life of a loan or investment. They offer predictability, which can be advantageous in volatile markets or for budgeting purposes.

- Variable Interest Rates: These rates can fluctuate over time based on market conditions, typically tied to a benchmark like the prime rate or SOFR (Secured Overnight Financing Rate). Variable rates can offer lower initial payments but carry the risk of increasing costs or decreasing returns.

The Impact of Inflation on Your Interest Earnings

While earning interest is beneficial, its true value is eroded by inflation. Inflation is the rate at which the general level of prices for goods and services is rising, and subsequently, the purchasing power of currency is falling. If your savings account offers a 2% APY but inflation is running at 3%, your “real” return is actually negative 1%, meaning your money is losing purchasing power over time. Therefore, finding interest means not just identifying accounts that pay interest, but those that pay above the rate of inflation to preserve and grow your wealth in real terms.

Navigating Traditional Avenues for Earning Interest

For decades, certain financial products have served as reliable, albeit sometimes modest, sources of interest income. These traditional avenues often prioritize safety and liquidity, making them suitable for emergency funds and conservative investors.

High-Yield Savings Accounts (HYSAs) and Money Market Accounts

High-Yield Savings Accounts (HYSAs) are an excellent starting point for earning more on your readily accessible cash. Unlike traditional savings accounts at brick-and-mortar banks that often offer paltry interest rates (e.g., 0.01% APY), HYSAs, typically offered by online banks, can provide APYs significantly higher (e.g., 4-5% or more). They offer flexibility, allowing you to deposit and withdraw money as needed, making them ideal for emergency funds or short-term savings goals.

Money Market Accounts (MMAs) share similarities with HYSAs but often come with features like check-writing capabilities and debit cards. While their interest rates are generally competitive with HYSAs, they might have higher minimum balance requirements or transaction limits. Both HYSAs and MMAs are typically FDIC-insured up to $250,000 per depositor, per institution, offering peace of mind.

Certificates of Deposit (CDs): Locking in Returns

Certificates of Deposit (CDs) offer a way to earn a guaranteed fixed interest rate for a specific period, known as the “term.” Terms can range from a few months to several years (e.g., 3 months, 1 year, 5 years). In exchange for agreeing to keep your money deposited for the entire term (early withdrawals usually incur penalties), banks offer higher interest rates than standard savings accounts.

CDs are an excellent option for money you don’t need immediate access to and for which you desire predictable returns. Strategies like “CD laddering” involve staggering CDs with different maturity dates to maintain some liquidity while still locking in higher rates.

Bonds: Lending to Governments and Corporations

Bonds represent a loan made by an investor to a borrower (typically a corporation or government entity). In return for lending your money, the borrower promises to pay you regular interest payments (called “coupon payments”) over a set period and to return your principal at maturity.

- Government Bonds (e.g., Treasury Bills, Notes, Bonds, Savings Bonds): Issued by national, state, or municipal governments, these are generally considered very low-risk, especially U.S. Treasury bonds, which are backed by the full faith and credit of the U.S. government.

- Corporate Bonds: Issued by companies to raise capital. These carry higher risk than government bonds but often offer higher interest rates to compensate investors for that increased risk.

Bonds are a staple in diversified investment portfolios, providing a steady stream of income and acting as a counterbalance to more volatile assets like stocks.

Annuities: Securing Future Income Streams

Annuities are contracts, typically purchased from insurance companies, designed to provide a steady stream of income in retirement. You pay a lump sum or a series of payments to the insurance company, and in return, they provide you with regular payments, either immediately or at a future date. Annuities can be complex, offering various features and riders, and their suitability depends heavily on individual financial goals and risk tolerance. While they can provide guaranteed income and tax-deferred growth, they often come with fees and restrictions.

Exploring Modern and Alternative Interest-Bearing Opportunities

The financial landscape is ever-evolving, with new technologies and platforms creating innovative ways to find and earn interest, often with potentially higher returns but sometimes with increased risk.

Peer-to-Peer (P2P) Lending Platforms

P2P lending platforms connect individual borrowers directly with individual lenders, bypassing traditional banks. As a lender, you can invest in a portion of a loan (or many loans) to individuals or small businesses, earning interest on your contribution. Platforms like LendingClub or Prosper allow you to diversify across multiple loans, mitigating some risk. The interest rates can be significantly higher than traditional savings accounts, but so is the risk of borrower default. Thorough due diligence and diversification are crucial here.

Robo-Advisors and Diversified Investment Portfolios

While not strictly “interest-bearing” in the traditional sense, robo-advisors build and manage diversified portfolios of exchange-traded funds (ETFs) and mutual funds, which often include bond funds. These bond funds pool money from many investors to buy various bonds, generating income (which can be thought of as a form of interest) for the fund’s investors. Robo-advisors offer a low-cost, automated way to invest in a broad range of assets, including those that generate income, tailored to your risk profile. Platforms like Betterment or Wealthfront simplify investing, making it accessible even for beginners.

Real Estate Crowdfunding and REITs

Investing directly in real estate can be capital-intensive, but real estate crowdfunding platforms allow you to invest smaller amounts in specific real estate projects (e.g., commercial properties, residential developments) and earn returns, sometimes including interest payments from debt-based projects or rental income.

Alternatively, Real Estate Investment Trusts (REITs) are companies that own, operate, or finance income-generating real estate. They trade on major stock exchanges like stocks and are legally required to distribute at least 90% of their taxable income to shareholders annually, typically in the form of dividends (which are akin to interest payments derived from rental income or property financing). REITs offer a liquid way to invest in real estate and earn regular income.

Stablecoins and Decentralized Finance (DeFi) for Crypto Interest

For those comfortable with the volatile world of cryptocurrency, stablecoins (cryptocurrencies pegged to stable assets like the U.S. dollar) offer a potential avenue for earning high interest. Decentralized Finance (DeFi) platforms allow users to lend out their stablecoins to other users and earn substantial interest rates (sometimes double-digit percentages). This is achieved through “yield farming,” “staking,” or “liquidity providing.” However, this space carries significant risks, including smart contract vulnerabilities, platform hacks, regulatory uncertainty, and impermanent loss. While the potential returns are high, the risk profile is equally elevated, making it suitable only for investors with a high-risk tolerance and a deep understanding of the underlying technology.

Strategies for Maximizing Your Interest Income

Finding interest is only half the battle; maximizing it requires strategic planning and consistent effort.

The Art of Diversification: Spreading Your Bets

Putting all your money into a single interest-bearing account or investment is risky. Diversification, the practice of spreading your investments across various asset classes, industries, and geographies, is critical. By diversifying, you reduce the impact of any single investment’s poor performance on your overall portfolio. This applies to interest-bearing assets too – a mix of HYSAs, CDs, different types of bonds, and potentially some higher-risk alternative assets can provide a more resilient income stream.

Automation and Regular Contributions

The power of compound interest is amplified by consistent contributions. Automating your savings and investment contributions means a portion of your income is regularly directed to your interest-earning accounts without you having to think about it. This systematic approach ensures that your principal consistently grows, leading to more interest being earned on a larger base over time. Set up automatic transfers from your checking account to your HYSAs, investment accounts, or bond purchases.

Understanding Tax Implications of Interest Income

Interest income is generally taxable. The type of interest and the account it’s held in determine how and when it’s taxed. For instance, interest from savings accounts and CDs is typically taxed as ordinary income. Interest from municipal bonds, however, can be exempt from federal, state, and local taxes for residents of the issuing state. Interest earned within tax-advantaged retirement accounts (like IRAs or 401(k)s) grows tax-deferred or tax-free. Understanding these nuances can significantly impact your net returns and should be a key consideration in choosing where to find interest.

Reinvesting Your Earnings: The Compounding Advantage

To truly harness the power of compound interest, reinvest your earnings whenever possible. Instead of withdrawing the interest you earn, let it remain in the account or investment so that it, too, can start earning interest. This accelerates the compounding effect, transforming small gains into significant wealth over the long run. Many investment platforms and bond funds offer options for automatic reinvestment of dividends or interest payments.

Leveraging Financial Tools to Discover and Manage Interest

The digital age provides an abundance of tools designed to help you find the best interest rates and manage your interest-bearing assets effectively.

Comparison Websites and Aggregators

Websites like Bankrate, NerdWallet, and DepositAccounts.com are invaluable resources for comparing interest rates on savings accounts, CDs, money market accounts, and even mortgage rates. They aggregate data from numerous financial institutions, allowing you to easily sort and filter options based on APY, minimum deposits, terms, and other features. Regularly checking these sites ensures you’re always aware of the most competitive rates available.

Budgeting and Investment Tracking Apps

Apps like Mint, Personal Capital (now Empower Personal Wealth), and YNAB (You Need A Budget) can help you track your income, expenses, and investments. While primarily budgeting tools, many also offer features to monitor your savings balances, investment performance, and even project future growth, allowing you to see the impact of the interest you’re earning across your entire financial portfolio. These tools provide a holistic view of your financial health and help identify opportunities to allocate more funds to interest-earning vehicles.

Financial Advisors and Personalized Guidance

For those with complex financial situations, significant assets, or a desire for tailored strategies, a qualified financial advisor can be an indispensable resource. An advisor can help you understand your risk tolerance, define your financial goals, and construct a diversified portfolio that includes appropriate interest-earning assets. They can also provide insights into tax-efficient strategies and guide you through the intricacies of various investment products, ensuring you “find interest” in a way that aligns perfectly with your individual circumstances.

In conclusion, “how to find interest” is a question with profound implications for your financial future. It’s about more than just locating an account that pays a percentage; it’s about understanding the mechanisms of growth, identifying opportunities across a spectrum of risk and reward, strategically maximizing returns through diversification and automation, and intelligently leveraging modern tools and expertise. By mastering these principles, you empower your money to work diligently for you, transforming passive savings into active wealth accumulation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.