In the complex ecosystem of global finance, few numbers hold as much weight for the average consumer and business owner as the “prime rate.” It is the invisible hand that guides the cost of borrowing, influences the feasibility of homeownership, and dictates the growth potential of small businesses. If you have recently checked your credit card statement or applied for a line of credit, you have likely felt the ripple effects of the current prime rate.

As of today, the prime rate stands as a critical barometer for the health and direction of the economy. Set against a backdrop of fluctuating inflation and central bank policy shifts, understanding what this rate is—and how it is determined—is essential for anyone looking to navigate their personal or professional finances with confidence.

The Mechanics of the Prime Rate: Definition and Determination

The prime rate is fundamentally defined as the base interest rate that commercial banks charge their most creditworthy corporate customers. While it may seem like a figure reserved for “big business,” it serves as the foundational benchmark for almost all consumer lending products in the United States and many other developed economies.

The 300 Basis Point Rule

The prime rate does not exist in a vacuum. In the United States, there is a direct and almost mechanical relationship between the federal funds rate—set by the Federal Reserve—and the prime rate. Historically, and by industry convention, the prime rate is set exactly 3 percentage points (or 300 basis points) above the federal funds target range’s upper limit.

When the Federal Open Market Committee (FOMC) meets to decide on monetary policy, their decision to raise, lower, or maintain the federal funds rate causes an immediate, symbiotic shift in the prime rate. This predictability allows financial markets to price loans with a degree of consistency, even during volatile economic cycles.

The Role of The Wall Street Journal Prime Rate

While individual banks have the technical authority to set their own prime rates, the industry relies on a consensus figure. The Wall Street Journal (WSJ) publishes the “Prime Rate” based on a survey of the 30 largest banks in the country. When at least 23 out of these 30 banks change their rate, the WSJ updates its published figure. This published rate is what most lenders use as the index for variable-rate loans, making it the “official” prime rate for the majority of the financial world.

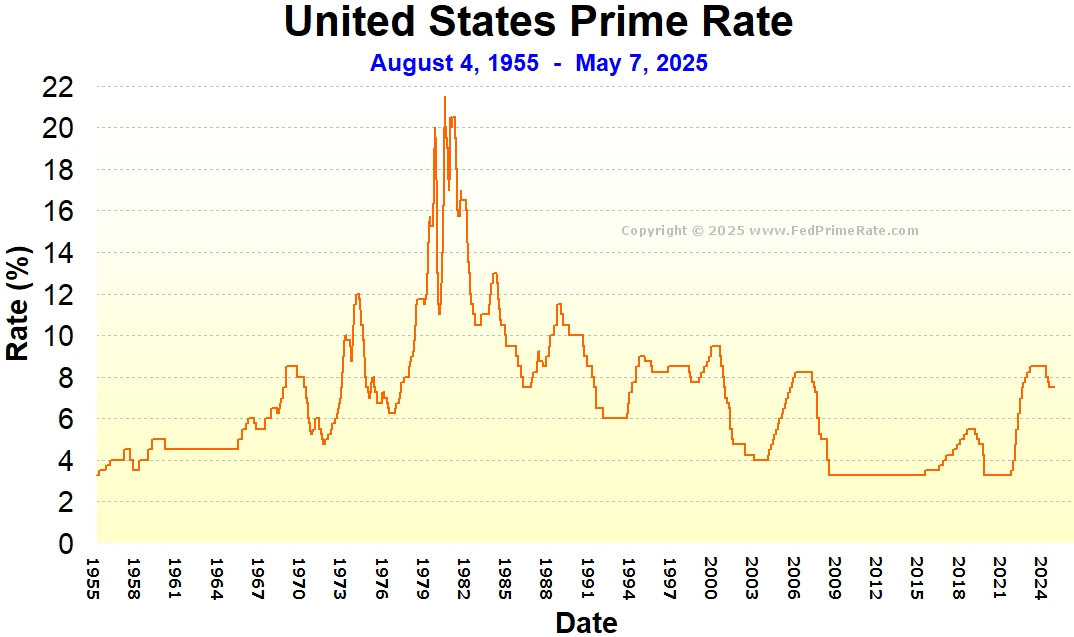

Why Today’s Rate is Historically Significant

To understand the prime rate as of today, one must look at the trajectory of the last few years. Following a long period of historically low rates, the economy saw a rapid ascent in the prime rate as the Federal Reserve sought to combat record-high inflation. This has pushed the prime rate to levels not seen in over a decade, fundamentally changing the math for savers and borrowers alike. Today’s rate represents a “restrictive” monetary environment, designed to cool spending and stabilize the purchasing power of the dollar.

How the Prime Rate Influences Your Personal Finances

The prime rate is not just a corporate metric; it is a personal one. Most consumer debt is structured as “Prime + X%.” Therefore, when the prime rate moves, the interest you pay on your existing or future debt moves in lockstep.

Credit Cards and Variable APRs

The most immediate impact of today’s prime rate is seen on credit card balances. Most credit cards come with a variable Annual Percentage Rate (APR). If your credit card agreement states that your interest rate is “Prime + 15%,” and the prime rate increases by 0.25%, your credit card APR will follow suit almost instantly. In a high-prime-rate environment, carrying a balance becomes significantly more expensive, leading to a “debt trap” where more of your monthly payment goes toward interest rather than the principal balance.

Home Equity Lines of Credit (HELOCs)

For homeowners, the prime rate is the primary driver of the cost of a Home Equity Line of Credit (HELOC). Unlike traditional fixed-rate mortgages, HELOCs are almost always variable-rate products tied directly to the prime rate. As the rate has climbed recently, many homeowners have seen their monthly interest-only payments double or even triple, impacting their monthly cash flow and discretionary spending.

Personal Loans and Auto Financing

While some personal and auto loans offer fixed rates, many—especially those from fintech lenders or credit unions—are tied to the prime rate. Even for fixed-rate products, the “starting” rate offered to new borrowers is influenced by the current prime rate. When the prime rate is high, the barrier to entry for purchasing a new vehicle or consolidating debt becomes higher, requiring consumers to have better credit scores to secure manageable terms.

The Broader Economic Impact of Prime Rate Fluctuations

Beyond individual bank accounts, the prime rate acts as a throttle for the broader economy. It is one of the primary tools used to manage the speed of economic growth and the rate of inflation.

Small Business Lending and Growth

Small businesses are the backbone of the economy, but they are also the most sensitive to prime rate changes. Most small business loans, including SBA loans and revolving lines of credit, are tied to the prime rate. When the rate is high, the cost of capital increases. This often leads small business owners to delay expansion, pause hiring, or reduce inventory orders. Effectively, a high prime rate acts as a cooling mechanism for the business sector.

The Fight Against Inflation

The central bank utilizes the prime rate indirectly to control inflation. By making borrowing more expensive, the “demand” side of the economy slows down. People buy fewer houses, businesses invest in fewer projects, and consumers spend less on credit. This reduction in spending helps to bring supply and demand back into balance, eventually lowering the rate of price increases for goods and services.

Impact on the Housing Market

While 30-year fixed mortgage rates are more closely tied to the 10-year Treasury yield, they still move in the same general direction as the prime rate. A high prime rate creates an environment of “tighter” credit. Lenders become more risk-averse, and the overall cost of financing a home increases. This can lead to a stagnation in home prices as buyers find themselves priced out of the monthly payments required at current rates.

Strategies for Managing Finances in a High-Prime Environment

When the prime rate is elevated, as it is today, passive financial management can be costly. Proactive strategies are required to protect your wealth and minimize unnecessary interest expenses.

Refinancing and Consolidation

If you are holding high-interest debt tied to a variable prime rate, now is the time to look at debt consolidation. Moving variable-rate credit card debt into a fixed-rate personal loan can provide “rate certainty.” Even if the fixed rate is relatively high, it protects you from further potential hikes in the prime rate and provides a clear timeline for debt elimination.

Prioritizing Variable-Rate Debt

In a rising or high-rate environment, the “debt avalanche” method becomes even more effective. This involves paying off the debt with the highest interest rate first. Since variable-rate debts (like credit cards and HELOCs) are currently the most expensive, focusing your extra payments there provides the highest “return” on your money by saving you the most in future interest charges.

Improving Credit Scores to Beat the “Spread”

While you cannot control the prime rate, you can control the “margin” or “spread” that lenders add to it. A lender might offer a loan at “Prime + 2%” to someone with excellent credit, but “Prime + 7%” to someone with fair credit. By improving your credit score—through timely payments, low credit utilization, and monitoring for errors—you can effectively lower your personal interest rate even when the national prime rate remains high.

Maximizing Yield on Savings

There is a silver lining to a high prime rate: savings rates usually rise alongside it. High-yield savings accounts (HYSAs) and Certificates of Deposit (CDs) often offer their best returns when the prime rate is elevated. For those with cash reserves, this is an opportune time to move money out of traditional low-interest checking accounts and into vehicles that provide a meaningful real return on investment.

Conclusion: Staying Informed in a Dynamic Market

The prime rate as of today is more than just a statistic; it is a reflection of the current economic struggle to balance growth with stability. Whether you are a consumer trying to manage monthly bills or an investor looking for the next opportunity, the prime rate serves as a North Star for financial decision-making.

By understanding that the prime rate is intrinsically linked to Federal Reserve policy and that it dictates the cost of everything from your credit card to your business’s line of credit, you can make more informed choices. In a world where interest rates can shift the landscape of your net worth, staying educated is the best investment you can make. Keep a close watch on the Wall Street Journal prime rate and the FOMC’s announcements, as these will continue to shape the financial reality of tomorrow.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.