In today’s dynamic economic climate, managing personal finances effectively is more critical than ever. For many individuals, a car payment represents one of the largest fixed monthly expenses, second only to housing. While the allure of a new vehicle can be strong, the reality of its accompanying financial commitment can sometimes become a burden, squeezing budgets and limiting financial flexibility. Understanding how to strategically reduce this payment can unlock significant monthly savings, alleviate stress, and free up capital for other financial goals, whether that’s saving for a down payment, investing, or simply building an emergency fund. This comprehensive guide will delve into the various avenues available for lowering your car payment, offering practical, actionable advice within the realm of personal finance.

Understanding Your Current Car Loan Landscape

Before you can effectively strategize to lower your car payment, you must first have a clear and comprehensive understanding of your current financial obligations and the terms of your existing auto loan. This foundational step is crucial for identifying potential leverage points and making informed decisions.

Analyzing Your Loan Agreement

Pull out your original loan documents. Key pieces of information you need to identify include:

- Current Interest Rate (APR): This is perhaps the most significant factor influencing your monthly payment. A high APR means a larger portion of your payment goes towards interest rather than the principal.

- Original Loan Term: How many months was your loan originally set for?

- Remaining Loan Term: How many months do you still have left to pay?

- Current Principal Balance: How much do you still owe on the vehicle?

- Original Loan Amount: The total amount borrowed.

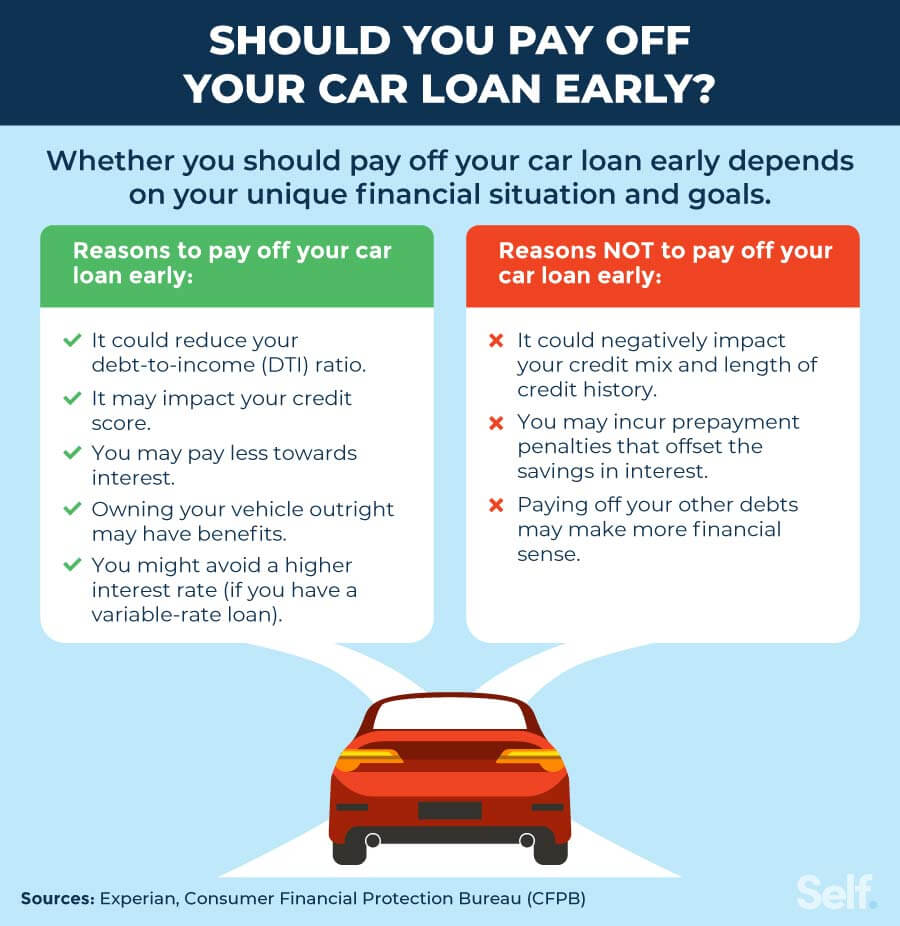

- Prepayment Penalties: Some older or subprime loans may include penalties for paying off the loan early. While less common now, it’s vital to check your contract.

- Vehicle’s Current Value: Research your car’s market value using reputable sources like Kelley Blue Book (KBB), Edmunds, or NADAguides. This will tell you if you have positive equity (car is worth more than you owe) or negative equity (you owe more than the car is worth, also known as being “upside down”). This figure is crucial for refinancing eligibility.

Understanding these elements provides a baseline. If your interest rate is significantly higher than current market rates, or if you’ve accumulated positive equity in your vehicle, you likely have strong grounds for pursuing a lower payment.

Assessing Your Financial Position

Beyond the loan itself, evaluate your broader financial health. Has your credit score improved since you first took out the loan? Lenders offer better rates to borrowers with excellent credit. Have your income or expenses changed? A clear picture of your current income, expenses, and overall debt-to-income ratio will help you determine how much flexibility you have and what kind of new payment you can comfortably afford. Creating a detailed budget using financial tools or simple spreadsheets can illuminate areas where you might be overspending and demonstrate the impact a lower car payment could have.

Strategies for Immediate Payment Reduction

Once you’ve assessed your current situation, it’s time to explore the most common and effective strategies for reducing your monthly car payment. These methods primarily revolve around adjusting the terms of your loan.

Refinancing Your Auto Loan

Refinancing is often the most direct and impactful way to lower your car payment. It involves taking out a new loan to pay off your existing auto loan, ideally with more favorable terms. The primary goal is usually to secure a lower interest rate, which directly translates to a smaller monthly payment and less interest paid over the life of the loan.

When to consider refinancing:

- Improved Credit Score: If your credit score has significantly improved since you financed your car, you’re likely eligible for better rates.

- Lower Market Rates: Interest rates fluctuate. If current auto loan rates are lower than your original rate, refinancing could save you money.

- Original High-Interest Loan: If you originally purchased your car with a subprime loan or a high-interest rate due to limited credit history, refinancing with a prime lender can drastically cut your costs.

- Positive Equity: Lenders are more inclined to refinance loans where the borrower has positive equity in the vehicle.

- Original Long Term, Now Want Shorter: If your original loan was for 72 months and you’re now halfway through with a better financial standing, you might refinance for a shorter term at a lower rate, potentially keeping your payment similar but saving significantly on interest.

When applying for refinancing, shop around. Compare offers from multiple banks, credit unions, and online lenders. Each will have different criteria and rates, so finding the best fit is key.

Extending Your Loan Term

Another common method to reduce your monthly payment, especially if refinancing to a lower interest rate isn’t feasible, is to extend the loan term. For example, if you have two years left on a five-year loan, you might refinance it into a new four-year loan. While this will lower your monthly outlay, it’s important to understand the trade-offs:

- More Interest Paid: A longer loan term means you’ll be paying interest for a longer period, resulting in a higher total cost over the life of the loan, even if the monthly payment is lower.

- Increased Risk of Negative Equity: Extending the loan term can prolong the period during which you might be “underwater” on your loan, meaning you owe more than the car is worth. This can make selling or trading in the vehicle difficult.

This strategy should be considered primarily if you are facing a temporary financial hardship and need immediate relief, or if the interest rate on the extended term is still very competitive.

Exploring Payment Deferral or Modification

If you’re facing a short-term financial crisis, such as a job loss or unexpected medical expenses, contacting your current lender directly to discuss payment deferral or loan modification options might be a temporary solution.

- Payment Deferral: Some lenders offer the option to skip one or two payments, adding them to the end of your loan term. This provides immediate relief but will slightly increase the total interest paid and extend your loan duration. This is usually reserved for genuine hardship cases.

- Loan Modification: In more severe cases of hardship, lenders might be willing to modify the loan terms, potentially lowering the interest rate or extending the term, to prevent default. This is less common for auto loans than mortgages but worth exploring if you’re truly struggling.

These options are generally not long-term solutions for lowering your car payment but can be a lifeline during difficult times. Always understand the full implications and get any agreements in writing.

Long-Term Approaches to Financial Relief

While refinancing and term extension offer immediate payment relief, integrating these strategies with broader financial planning can lead to even greater long-term savings and financial stability.

Paying Down Principal Early

If your goal isn’t just a lower monthly payment but also reducing the total cost of your car, consider making extra payments directly towards your loan’s principal. Even small, consistent additional payments can significantly reduce the amount of interest you pay over the loan’s life and shorten the loan term.

How it works: Ensure any extra payments are explicitly designated towards the principal. Some lenders automatically apply extra funds to future payments, which doesn’t accelerate payoff or reduce interest as effectively. Check your loan agreement or contact your lender to confirm their policy. Even adding an extra $50 or $100 to your payment each month can make a substantial difference over time.

Boosting Your Income Streams

A direct way to make your car payment feel less burdensome is to increase the amount of money flowing into your household. This isn’t a direct reduction of the payment itself, but it reduces the payment’s impact on your budget. Consider:

- Side Hustles: From freelance work to ride-sharing, food delivery, or selling crafts online, numerous side hustles can generate extra income.

- Negotiating a Raise: If appropriate, negotiate for a higher salary or seek opportunities for promotion at your current job.

- Selling Unused Items: Decluttering your home and selling items you no longer need can provide a quick influx of cash that can be used to make additional principal payments.

Even a modest increase in income can make your existing car payment more manageable and free up funds for other financial priorities.

Improving Your Credit Score

Your credit score is a powerful determinant of the interest rates you’ll receive on any loan. A higher credit score signals lower risk to lenders, making you eligible for better terms. If you’re not ready to refinance immediately, focus on improving your credit score in the interim.

Strategies for credit score improvement:

- Pay All Bills on Time: Payment history is the most significant factor in your credit score.

- Reduce Credit Card Balances: Lowering your credit utilization ratio (amount of credit used vs. available) can significantly boost your score.

- Avoid New Credit Applications: Each new application results in a hard inquiry, which can temporarily lower your score.

- Review Your Credit Report: Regularly check your credit report for errors and dispute any inaccuracies.

By systematically improving your credit score, you position yourself for the best possible interest rates when the time comes to refinance or apply for any future loans.

Practical Steps to Implement Your Plan

Once you’ve decided on a strategy, the next step is execution. Navigating the process effectively requires organization and diligence.

Gathering Necessary Documentation

Regardless of whether you’re refinancing or negotiating with your current lender, you’ll need a standard set of documents:

- Proof of Income: Pay stubs, tax returns, or bank statements.

- Identification: Driver’s license or other government-issued ID.

- Current Loan Information: Your existing loan statement, showing your current balance and account number.

- Vehicle Information: Your car’s VIN (Vehicle Identification Number), make, model, year, and mileage.

- Proof of Insurance: Your auto insurance policy details.

Having these documents readily available will streamline the application process and prevent delays.

Comparing Lender Offers

This is a critical step, especially for refinancing. Don’t settle for the first offer you receive. Apply to several different financial institutions – traditional banks, credit unions, and online lenders specializing in auto refinancing. Each will assess your creditworthiness and offer rates based on their internal algorithms and risk tolerance.

- Credit Unions: Often known for offering competitive rates to their members.

- Online Lenders: Many online platforms specialize in quick and convenient refinancing, with competitive rates.

- Traditional Banks: Your existing bank might offer a loyalty discount, but always compare.

When comparing offers, look beyond just the monthly payment. Consider the total interest paid over the life of the loan, any fees associated with the new loan, and the overall loan terms. Utilize online comparison tools and calculators to truly understand the long-term impact of each offer.

Navigating the Application Process

Once you’ve chosen a lender, carefully complete their application. Be thorough and honest. If you have questions, don’t hesitate to ask. Most lenders now offer online applications, making the process relatively straightforward. After approval, you’ll sign new loan documents, and the new lender will pay off your old loan. Ensure you receive confirmation that your old loan account has been closed and that your new payment schedule is clearly established.

The Broader Impact of a Lower Car Payment

Successfully lowering your car payment is not just about reducing one expense; it has a ripple effect that can significantly enhance your overall financial well-being and flexibility.

Freeing Up Monthly Cash Flow

The most immediate and tangible benefit of a lower car payment is the increase in your monthly disposable income. This freed-up cash flow can be directed towards a multitude of financial goals, such as:

- Building an Emergency Fund: Strengthening your financial safety net for unexpected expenses.

- Paying Down High-Interest Debt: Tackling credit card debt or personal loans with even higher interest rates.

- Increasing Savings: Contributing more to retirement accounts, college funds, or a down payment for a home.

- Investing: Allocating funds to investment vehicles for long-term wealth accumulation.

- Improving Quality of Life: Allowing for more discretionary spending on experiences, hobbies, or personal development, without jeopardizing financial stability.

This flexibility transforms a previously rigid expense into a powerful tool for achieving personal financial objectives.

Reducing Overall Debt Burden

By securing a lower interest rate or by paying off your loan faster through principal payments, you’re not just reducing your monthly outlay; you’re also decreasing the total amount of interest paid over the life of the loan. This directly reduces your overall debt burden, making you financially lighter and closer to debt-free status. For individuals aiming for significant financial milestones like early retirement or purchasing a home, reducing debt is a cornerstone strategy.

Achieving Greater Financial Flexibility

A lower car payment contributes to a more robust and resilient personal budget. With less money tied up in a fixed expense, you gain greater agility to respond to economic changes, pursue new opportunities, or weather unforeseen financial storms. This flexibility reduces financial stress, empowers you to make proactive financial decisions rather than reactive ones, and ultimately contributes to a greater sense of financial security and peace of mind.

In conclusion, lowering your car payment is a goal that is well within reach for many car owners. By diligently analyzing your current loan, exploring refinancing options, understanding the implications of loan term adjustments, and integrating smart financial habits, you can significantly reduce this recurring expense. The benefits extend far beyond just a smaller bill, paving the way for improved cash flow, reduced debt, and enhanced financial flexibility that will serve your financial goals for years to come.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.