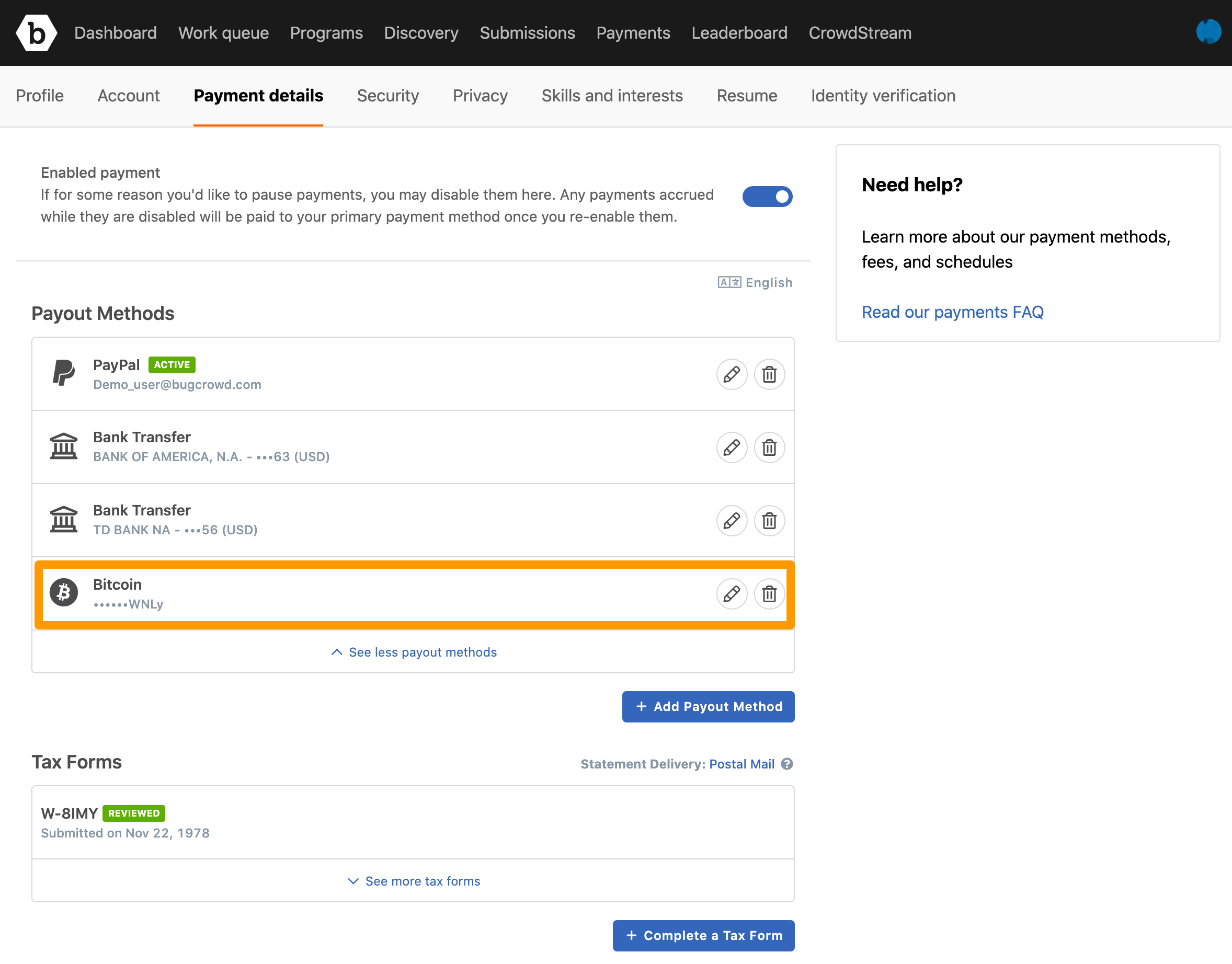

Bitcoin (BTC) has fundamentally reshaped our understanding of digital value transfer, ushering in an era of decentralized finance powered by groundbreaking technological innovation. At its core, a BTC payment is more than just sending money; it’s an intricate dance of cryptography, network protocols, and distributed ledger technology that enables secure, peer-to-peer transactions without the need for traditional financial intermediaries. To truly grasp “what is BTC payment,” one must delve into the sophisticated technological architecture that underpins this revolutionary system.

This article will explore the technical underpinnings of BTC payments, from the foundational blockchain to the mechanics of a transaction, its inherent advantages, and the ongoing technological challenges and solutions shaping its future. Our focus will remain strictly on the technological aspects, dissecting how Bitcoin’s engineering creates a novel payment paradigm.

The Foundational Technology: Blockchain and Cryptography

The very existence and functionality of BTC payments are inextricably linked to its underlying technology: the blockchain. This distributed ledger is the bedrock upon which all Bitcoin transactions are built, secured, and verified. Understanding its components is crucial to comprehending BTC payments.

Decentralization and Distributed Ledgers

Unlike conventional payment systems—which rely on central authorities like banks or payment processors to manage and verify transactions—Bitcoin operates on a decentralized network. This means there is no single point of control or failure. Instead, thousands of independent computers, known as “nodes,” collectively maintain and validate the entire transaction history.

The “blockchain” itself is a continuously growing list of records, called “blocks,” which are linked and secured using cryptography. Each block contains a timestamp, a reference to the previous block, and a batch of verified transactions. This distributed ledger is replicated across all nodes in the network, ensuring redundancy and transparency. Every participant can technically view the entire transaction history, albeit pseudonymously. This decentralized model is a radical departure from traditional centralized databases, offering unparalleled resilience against censorship and single-point attacks, making the network incredibly robust for processing payments.

Cryptographic Keys and Digital Signatures

Security in BTC payments is primarily achieved through sophisticated cryptography. Each Bitcoin user owns a pair of cryptographic keys: a public key and a private key.

- Private Key: This is a secret, alphanumeric string that grants control over a user’s Bitcoin. It functions much like a password, but its length and complexity make it virtually impossible to guess. The private key is used to generate a digital signature, which is essential for authorizing transactions. Losing a private key means losing access to one’s Bitcoin, as there’s no central “reset” mechanism.

- Public Key: Derived mathematically from the private key, the public key is shared openly. It is used to generate a Bitcoin address, which acts as the destination for incoming BTC payments—akin to an email address for digital currency.

When a user wants to make a BTC payment, they use their private key to digitally “sign” the transaction. This digital signature proves ownership of the Bitcoin being sent without revealing the private key itself. The network can then verify that the sender legitimately authorized the transaction using the sender’s public key. This system ensures non-repudiation; once a transaction is signed and broadcast, the sender cannot deny having sent it. The cryptographic link between public and private keys is the fundamental mechanism that secures ownership and authorizes the transfer of value in Bitcoin.

Mining and Transaction Validation

For a BTC payment to be considered complete and irreversible, it must be validated and included in a new block on the blockchain. This process is known as “mining.” Bitcoin miners are participants in the network who use powerful computing hardware to solve complex mathematical puzzles. The first miner to solve the puzzle for a new block gets to add a batch of pending transactions to that block and append it to the blockchain.

This “Proof-of-Work” mechanism serves several critical functions:

- Transaction Validation: Miners verify that each transaction within their proposed block is legitimate (e.g., the sender has sufficient funds, the digital signature is valid).

- Network Security: The computational effort required for mining makes it economically infeasible to tamper with past transactions. To alter a past block, an attacker would need to redo all the Proof-of-Work for that block and all subsequent blocks faster than the rest of the network, an almost impossible feat known as a “51% attack.”

- Block Creation: Successfully mining a block rewards the miner with newly minted Bitcoin (the “block reward”) and any transaction fees included in the block’s transactions. This incentivizes miners to continue contributing their computational resources to secure the network.

Once a transaction is included in a block and that block is added to the blockchain, it receives its first “confirmation.” As more blocks are added on top of it, the transaction becomes progressively more secure and practically irreversible. Typically, 3-6 confirmations are considered sufficient for high-value transactions, providing a robust level of finality.

Anatomy of a Bitcoin Transaction

Understanding the conceptual framework is one thing; dissecting the technical components of an actual BTC transaction reveals the precision engineered into the system.

Initiating a Payment: Wallets and Addresses

To send or receive BTC, users interact with a “Bitcoin wallet.” Technically, a Bitcoin wallet doesn’t hold Bitcoin itself; rather, it securely stores the user’s private keys and provides an interface to interact with the Bitcoin blockchain.

- Software Wallets: These are applications running on desktop computers or mobile devices. They can be “hot” wallets (connected to the internet) or “cold” wallets (offline for greater security).

- Hardware Wallets: Physical devices designed to store private keys in an isolated, offline environment, offering a high level of security against online threats.

- Paper Wallets: Private keys printed on paper, offering ultimate cold storage but requiring careful handling to prevent loss or damage.

When a user wants to send BTC, their wallet constructs a transaction message. This message specifies the amount of BTC to send, the recipient’s Bitcoin address, and the sender’s own Bitcoin address(es) from which the funds are drawn. The wallet then uses the sender’s private key(s) to create a digital signature for this transaction.

Transaction Inputs and Outputs

Every Bitcoin transaction is structured as a series of inputs and outputs. This is a fundamental concept that differs significantly from traditional banking, where accounts simply have a “balance.” In Bitcoin, there are no balances in the traditional sense; instead, Bitcoin exists as “Unspent Transaction Outputs” (UTXOs).

- Inputs: These are references to previous UTXOs that the sender received and now wishes to spend. Each input must be cryptographically signed by the private key corresponding to the public address that received the UTXO. The sum of the BTC value of all inputs must be equal to or greater than the sum of the outputs.

- Outputs: These specify the new UTXOs being created by the transaction. Typically, there are two types of outputs:

- The amount of BTC being sent to the recipient’s Bitcoin address.

- “Change” BTC being returned to a new address controlled by the sender (if the input UTXO was larger than the amount being sent).

The difference between the total input value and the total output value constitutes the transaction fee, which is collected by the miner who includes the transaction in a block. This UTXO model provides a robust and auditable chain of ownership for every fraction of Bitcoin.

Transaction Fees and Confirmation Times

Transaction fees are an integral part of the Bitcoin network’s operation, serving as an incentive for miners to include transactions in blocks. When a user initiates a BTC payment, they typically specify a fee rate (e.g., satoshis per virtual byte).

- Fee Determinants: The size of a transaction (in bytes, not BTC value), network congestion, and the desired confirmation speed all influence the optimal fee. During periods of high network activity, higher fees are needed to incentivize miners to prioritize a transaction.

- Confirmation Times: Once broadcast to the network, a transaction sits in the “mempool” (memory pool) of pending transactions. Miners pick transactions from the mempool, usually prioritizing those with higher fees, to include in the next block. A new block is mined approximately every 10 minutes on average. Thus, the first confirmation can take anywhere from seconds (if a transaction is immediately picked for the next block) to hours (during high congestion with low fees). The more confirmations a transaction receives, the more immutable it becomes.

This dynamic fee market and probabilistic confirmation time are technical characteristics that differentiate BTC payments from instant, fixed-fee traditional payment methods, requiring users to understand these nuances.

Key Technological Advantages of BTC Payments

The technological design of Bitcoin grants it several unique advantages over conventional payment systems, making it a compelling alternative for digital value transfer.

Enhanced Security and Immutability

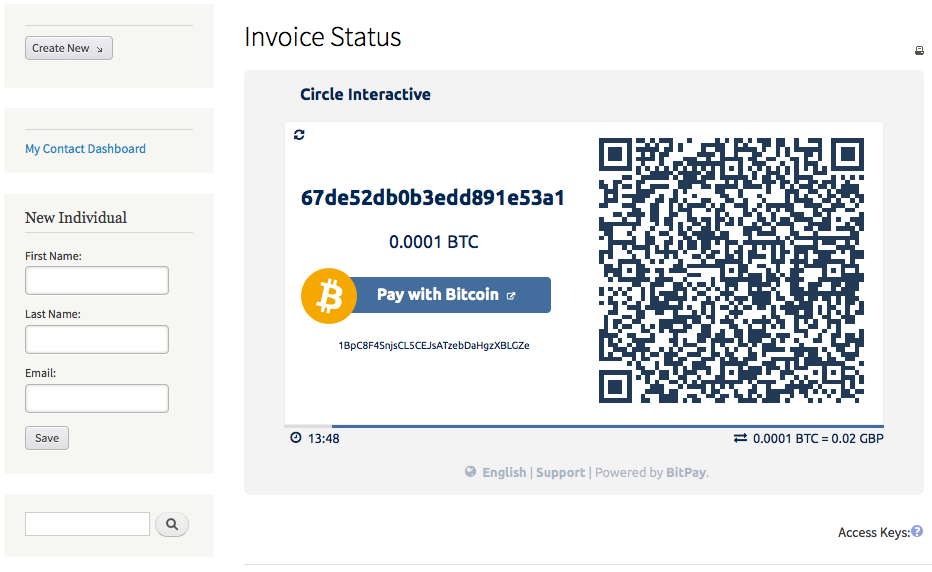

![]()

Bitcoin’s security is derived from its decentralized nature, cryptographic integrity, and the Proof-of-Work consensus mechanism.

- Immutability: Once a transaction is validated and included in a block, and that block is sufficiently buried under subsequent blocks, it becomes practically irreversible. This immutability prevents double-spending (the act of spending the same BTC twice) and makes fraudulent reversals extremely difficult, a stark contrast to chargebacks in traditional finance.

- Tamper-Proof Ledger: The cryptographic linking of blocks means that any attempt to alter a past transaction would require re-mining all subsequent blocks, an computationally unfeasible task for a single entity.

- Censorship Resistance: Because there is no central authority, no single entity can prevent a legitimate transaction from being processed or block an address from sending or receiving funds (though recipient services can choose not to accept transactions from certain addresses).

These security features are inherent to the blockchain technology itself, providing a robust framework for secure payments.

Global Reach and Borderless Transfers

The internet-native nature of Bitcoin means that BTC payments are inherently global and borderless.

- Peer-to-Peer Global Network: Any two individuals or entities, anywhere in the world, with an internet connection and a Bitcoin wallet, can send and receive BTC without geographical limitations. There are no “international transfer” fees or complex SWIFT codes.

- Elimination of Intermediaries: Traditional international payments involve multiple banks and correspondent networks, adding layers of cost, delay, and complexity. BTC payments bypass these entirely, facilitating direct peer-to-peer value exchange.

- 24/7 Availability: The Bitcoin network operates continuously, 24 hours a day, 7 days a week, unaffected by banking holidays or geographical time zones. This provides always-on payment infrastructure.

This global, direct transfer capability represents a significant technological leap for cross-border transactions, reducing friction and increasing efficiency.

Pseudonymity and Privacy Considerations

While the entire Bitcoin blockchain is public and transparent, BTC payments offer a degree of pseudonymity.

- Public Addresses, No Personal Data: Bitcoin addresses are strings of alphanumeric characters that do not directly reveal a user’s real-world identity. Transactions are linked to these addresses, not to names or personal information.

- Transaction Graph Analysis: However, due to the public nature of the blockchain, all transactions are recorded permanently. Sophisticated analytical techniques and tools can be used to trace the flow of BTC between addresses, potentially linking addresses to real-world identities if enough external information is available (e.g., if a user deposits BTC to an exchange that requires KYC).

- Enhanced Privacy Solutions: Ongoing technological research and development aim to further enhance transaction privacy, with advancements like CoinJoin (mixing transactions from multiple users to obscure their origins) and other cryptographic techniques seeking to break the linkability of transactions.

It’s crucial to understand that Bitcoin offers pseudonymity, not absolute anonymity, and the level of privacy can be influenced by user behavior and technological tools.

Challenges and Future Technological Developments

Despite its revolutionary nature, the Bitcoin network, and by extension BTC payments, faces technological hurdles that developers are actively addressing to improve its utility and adoption.

Scalability Solutions: Lightning Network and Beyond

One of the primary technical challenges for Bitcoin is scalability—the ability to process a high volume of transactions quickly and affordably. The current design limits the number of transactions per second (tps) that the main blockchain can handle, leading to potential congestion and higher fees during peak demand.

- Lightning Network: The most prominent “Layer 2” scaling solution. The Lightning Network operates off-chain, enabling instant, low-cost micro-payments between participants. Users open “payment channels” with each other, conducting multiple transactions off the main blockchain, and only settling the net result onto the main chain when the channel is closed. This drastically increases transaction throughput without burdening the main chain.

- Taproot Upgrade: A significant protocol upgrade implemented in 2021, Taproot introduces Schnorr signatures and Merkelized Abstract Syntax Trees (MAST). Technically, this improves transaction privacy, reduces transaction size for complex scripts (like multi-signature transactions), and lowers transaction fees, thereby contributing to overall network efficiency and scalability.

- Other Layer 2s and Sidechains: Research into other Layer 2 solutions and sidechains continues, exploring different approaches to offload transaction processing from the main Bitcoin blockchain while retaining its security guarantees.

These technological advancements are critical for Bitcoin to handle a global volume of payments comparable to traditional systems.

User Experience and Accessibility

For widespread adoption, the technical complexity of BTC payments needs to be abstracted away for the average user.

- Simplified Wallet Interfaces: Developers are constantly refining wallet software to be more intuitive, secure, and user-friendly, abstracting away cryptographic details and focusing on a seamless payment experience. Features like address books, QR code scanning, and integrated fiat-to-crypto on-ramps are becoming standard.

- Atomic Swaps and Interoperability: Research into atomic swaps allows for direct, trustless exchanges of different cryptocurrencies without an intermediary, improving liquidity and user flexibility. Efforts to make Bitcoin interoperable with other blockchain networks or traditional payment rails through bridges and gateways are also underway.

- Integrated Payment Gateways: Businesses are increasingly integrating Bitcoin payment gateways (e.g., BitPay, OpenNode) that handle the technical complexities of accepting BTC, converting it to fiat, and settling funds, making it as easy as accepting credit card payments.

Improving the technological interface and integration pathways is paramount to making BTC payments accessible to a broader audience.

Regulatory Technology and Compliance

As Bitcoin gains traction, the intersection of decentralized technology and traditional regulatory frameworks presents new challenges.

- AML/KYC Solutions: “RegTech” (Regulatory Technology) solutions are emerging to help exchanges and financial institutions comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations while interacting with the pseudonymous Bitcoin blockchain. These often involve sophisticated analytics to trace funds and identify suspicious activity.

- Blockchain Forensics: Tools for blockchain forensics are becoming more advanced, enabling law enforcement and regulatory bodies to analyze transaction patterns and identify entities involved in illicit activities, demonstrating that the transparency of the blockchain can be leveraged for compliance.

- Decentralized Identity (DID): Projects exploring decentralized identity solutions aim to provide users with self-sovereign digital identities that could potentially integrate with blockchain systems, offering a privacy-preserving way to prove identity for regulatory purposes without relying on central authorities.

The development of “RegTech” solutions is crucial for bridging the gap between Bitcoin’s decentralized ethos and the requirements of global financial compliance, fostering responsible innovation.

How to Make a BTC Payment (Tutorial Overview)

While this article is purely technical, a brief overview of the process from a user’s perspective helps contextualize the underlying technology.

Setting Up a Bitcoin Wallet

The first technical step is to choose and set up a Bitcoin wallet. This involves downloading a software wallet application (e.g., Exodus, BlueWallet) or acquiring a hardware wallet (e.g., Ledger, Trezor). During setup, the wallet generates the cryptographic private and public key pair(s) and displays your Bitcoin receiving address(es). Crucially, you will be given a “seed phrase” (a series of words) which is a human-readable form of your private key, essential for backing up and recovering your wallet. This seed phrase must be kept secret and secure offline.

Acquiring Bitcoin

To make a BTC payment, you first need to acquire Bitcoin. This typically involves using a cryptocurrency exchange (e.g., Coinbase, Binance, Kraken) where you can convert fiat currency (like USD or EUR) into BTC. Technically, these exchanges facilitate the peer-to-peer buying and selling of BTC, acting as trusted intermediaries. Once purchased, you can transfer the BTC from the exchange’s wallet to your personal, self-custodial wallet (which means you control the private keys).

Sending and Receiving BTC

To send BTC:

- Open your wallet: Access the “send” function within your chosen Bitcoin wallet.

- Enter recipient’s address: Obtain the recipient’s Bitcoin address (a long string of characters, often displayed as a QR code) and paste it into your wallet. The wallet’s software will perform a checksum to ensure the address format is valid.

- Specify amount: Enter the amount of BTC you wish to send.

- Set fee: Your wallet will typically suggest a transaction fee based on current network conditions. You can often adjust this, understanding that a higher fee usually means faster confirmation.

- Confirm and sign: Review the transaction details (address, amount, fee) and digitally sign the transaction using your private key (usually by entering your wallet password or confirming on a hardware device).

- Broadcast: Your wallet then broadcasts the signed transaction to the Bitcoin network.

Upon broadcast, the transaction enters the mempool, awaits miner confirmation, and is eventually added to a block, completing the BTC payment process, all driven by the sophisticated technological architecture detailed above.

In conclusion, a BTC payment is a powerful testament to the ingenuity of decentralized technology. It leverages blockchain, cryptography, and a peer-to-peer network to facilitate secure, immutable, and borderless value transfers. While facing ongoing technological challenges, the continuous innovation in scaling solutions, user experience, and regulatory technology continues to solidify Bitcoin’s position as a transformative force in the digital payment landscape.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.