For many, the phrase “tax season” evokes a sense of dread or confusion. However, at its core, the federal tax return is one of the most significant financial documents an individual or business owner will handle each year. It is not merely a bureaucratic requirement; it is a comprehensive summary of your financial life over the past twelve months. Understanding the nuances of a federal tax return is essential for effective personal finance management, optimizing your tax liability, and ensuring long-term financial health.

In this guide, we will break down what a federal tax return is, how it functions within the context of the U.S. economy, and why it serves as a cornerstone for your broader financial strategy.

Understanding the Basics: What Exactly is a Federal Tax Return?

A federal tax return is a formal set of documents filed with the Internal Revenue Service (IRS) that reports your income, expenses, and other pertinent financial information for a specific tax year. It allows the government to calculate your tax liability—the amount of money you owe the federal government—and determines whether you have overpaid throughout the year or still owe a balance.

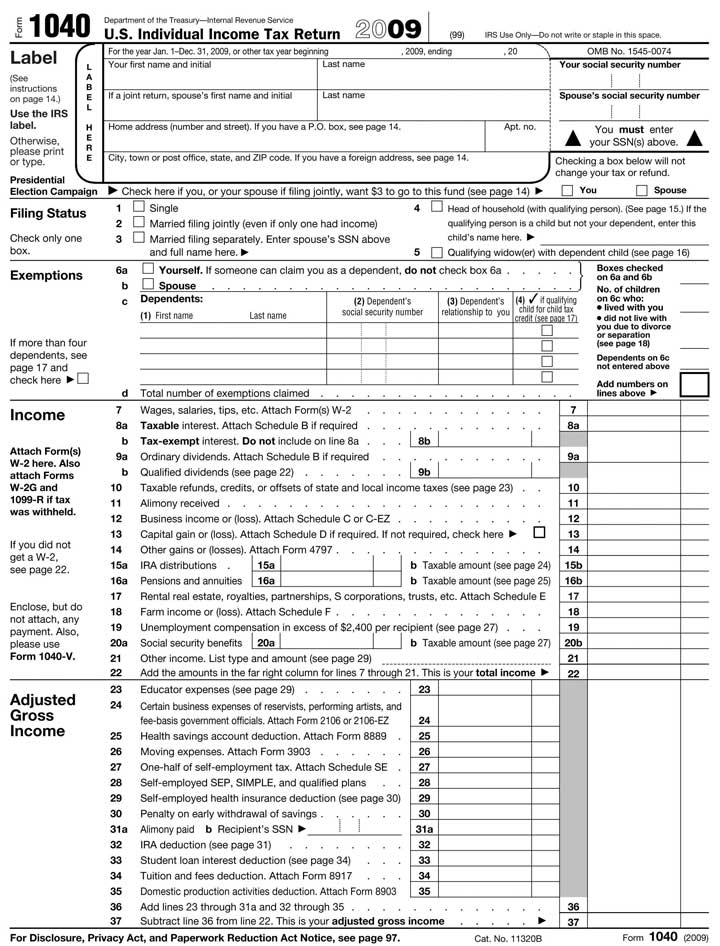

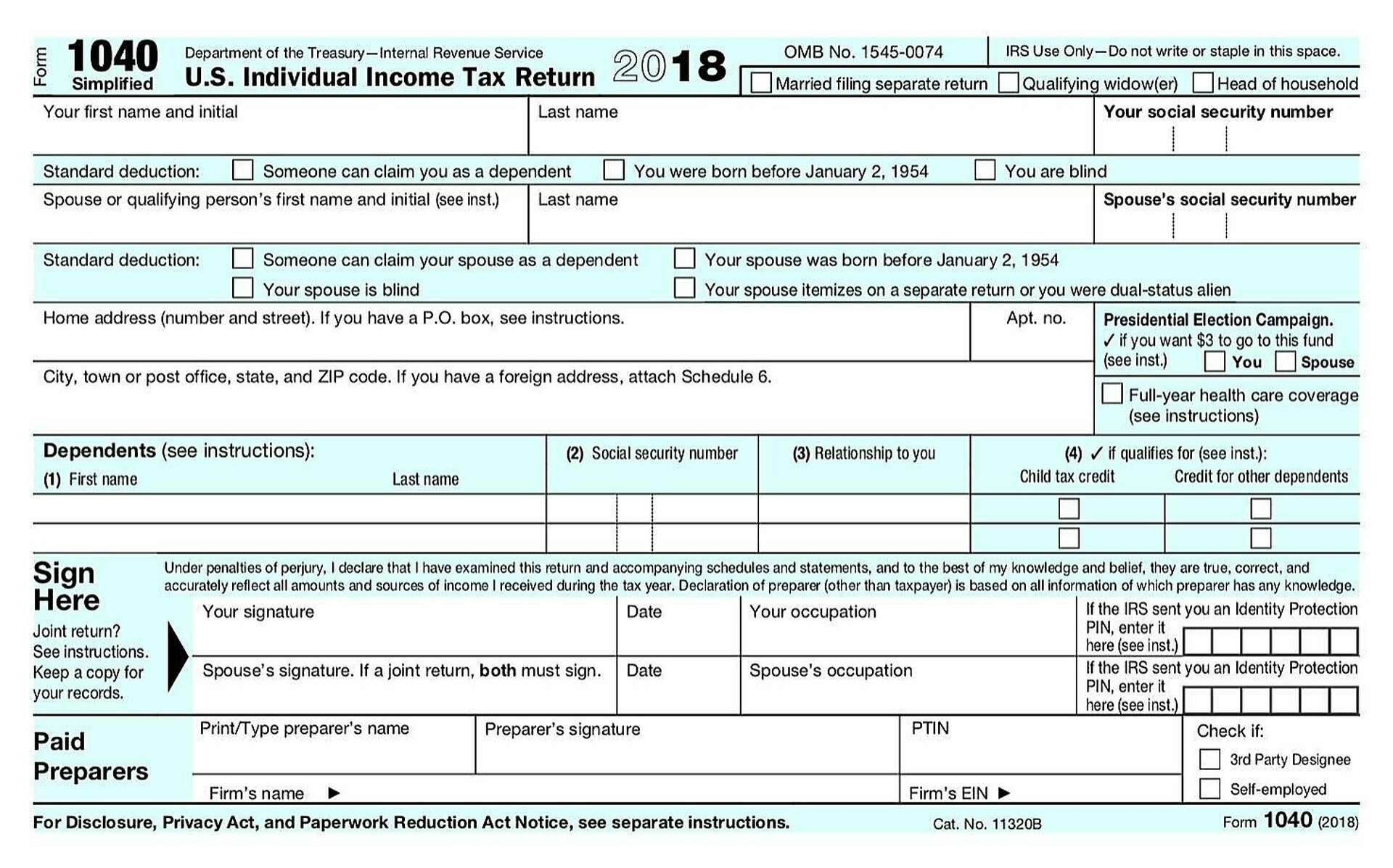

The Anatomy of Form 1040

The primary document used by individual taxpayers is IRS Form 1040, officially titled the “U.S. Individual Income Tax Return.” While the form has evolved over the years, its purpose remains the same: to provide a standardized way for the IRS to assess what you owe. The form consists of various sections where you report wages, interest, dividends, and other forms of income, followed by sections for adjustments and deductions that reduce your taxable income.

The Role of the Internal Revenue Service (IRS)

The IRS is the federal agency responsible for collecting taxes and enforcing the tax laws passed by Congress. When you file a return, you are essentially self-reporting your financial activity. The IRS uses these returns to fund federal programs, infrastructure, and national defense. For the taxpayer, the return serves as a “settling of accounts” between themselves and the state.

Who is Required to File?

Not every individual is required to file a federal tax return. The requirement generally depends on your gross income, filing status (such as single, married filing jointly, or head of household), and age. For example, if your income falls below a certain threshold set by the IRS, you may not be legally obligated to file. However, many people with low incomes choose to file anyway to claim refundable tax credits, such as the Earned Income Tax Credit (EITC), which can result in a significant refund.

The Mechanics of Filing: How Your Return is Calculated

The process of completing a tax return is a logical progression of additions and subtractions. Understanding this flow is vital for anyone looking to master their personal finances.

Reporting Your Total Gross Income

The starting point of any return is your total gross income. This includes every dollar earned from various sources during the calendar year. For employees, this is usually reported on a W-2 form. For independent contractors, freelancers, or those with “side hustles,” income is often reported via 1099 forms. Gross income isn’t just limited to wages; it also encompasses:

- Interest and dividends from investments.

- Capital gains from the sale of assets (like stocks or real estate).

- Rental income.

- Retirement distributions.

- Unemployment compensation.

Calculating Adjusted Gross Income (AGI)

Once you have your total income, you are allowed to make certain “above-the-line” adjustments. These might include contributions to a traditional IRA, student loan interest payments, or health savings account (HSA) contributions. Subtracting these adjustments from your total income results in your Adjusted Gross Income (AGI). Your AGI is a critical number because it often determines your eligibility for various tax credits and deductions.

Taxable Income: Standard vs. Itemized Deductions

After calculating your AGI, you have the option to reduce your taxable income further using deductions. Most taxpayers choose the Standard Deduction, which is a flat dollar amount based on your filing status. However, if you have significant expenses—such as mortgage interest, state and local taxes (SALT), or large medical bills—you may choose to Itemize Deductions. By subtracting these deductions from your AGI, you arrive at your Taxable Income, which is the actual amount the IRS uses to calculate your tax bill based on current tax brackets.

Maximizing Your Outcome: Credits, Deductions, and Refunds

The goal for most taxpayers is to minimize their tax liability and, if possible, secure a refund. To do this effectively, one must understand the difference between tax deductions and tax credits.

The Difference Between Deductions and Credits

While both reduce the amount you pay, they do so in different ways. A deduction reduces the amount of income that is subject to tax. For example, if you are in the 22% tax bracket, a $1,000 deduction saves you $220. A credit, on the other hand, is a dollar-for-dollar reduction of your actual tax bill. A $1,000 credit saves you exactly $1,000. Because credits directly slash the tax you owe, they are generally considered more valuable than deductions.

Common Tax Credits to Leverage

Tax credits are often used by the government to incentivize certain behaviors or provide relief to specific groups. Common credits include:

- Child Tax Credit (CTC): Provides financial relief to parents with qualifying children.

- Earned Income Tax Credit (EITC): A benefit for low-to-moderate-income working individuals and couples, particularly those with children.

- Education Credits: Such as the American Opportunity Tax Credit (AOTC) or the Lifetime Learning Credit (LLC), which help offset the costs of higher education.

Understanding the Tax Refund

A tax refund is not “free money” from the government; it is a return of your own money that you overpaid throughout the year. Most employees have taxes withheld from their paychecks. If the total amount withheld (plus any refundable credits) exceeds your actual tax liability, the IRS sends you the difference as a refund. Conversely, if you did not pay enough through withholding or estimated payments, you will owe the IRS the balance.

The Logistics of Filing: Deadlines, Documentation, and Methods

Filing a federal tax return requires organization and attention to detail. Missing a deadline or failing to report income can lead to penalties and interest charges.

Key Deadlines and Extensions

The traditional deadline for filing a federal tax return is April 15th. If this date falls on a weekend or holiday, it is moved to the next business day. If you cannot meet this deadline, you can request an automatic six-month extension, moving your filing deadline to October 15th. However, it is crucial to note that an extension to file is not an extension to pay. If you owe money, you must still estimate and pay that amount by April 15th to avoid late-payment penalties.

Gathering Essential Documentation

Accuracy is paramount when filing. You should gather all relevant documents before you begin, including:

- Income Statements: W-2s and all types of 1099s.

- Expense Records: Receipts for business expenses, medical bills, or charitable contributions if you plan to itemize.

- Investment Records: Statements showing capital gains or losses.

- Form 1098: For reporting mortgage interest or student loan interest.

E-Filing vs. Paper Returns

In the modern era, the vast majority of taxpayers file electronically (e-filing). E-filing is faster, more accurate, and allows for quicker processing of refunds. Many choose to use tax preparation software, which guides the user through a series of questions to populate the forms. Alternatively, individuals with complex financial situations—such as business owners or high-net-worth investors—often hire a Certified Public Accountant (CPA) or tax professional to ensure compliance and optimization.

Beyond the Deadline: Why Tax Returns Matter for Your Financial Future

While many view the federal tax return as a once-a-year obligation, it plays a much larger role in your overall financial life and wealth-building strategy.

Proof of Income for Loans and Mortgages

Your federal tax return is the ultimate verification of your income. When you apply for a mortgage, a business loan, or even certain types of insurance, lenders will almost always request your last two years of tax returns. They use this data to assess your debt-to-income ratio and determine your creditworthiness. Maintaining clean, accurate returns is essential for accessing the capital needed to buy a home or start a business.

Tax Planning as a Wealth-Building Strategy

Proactive tax planning is a hallmark of sophisticated personal finance. By reviewing your tax return, you can identify trends and opportunities for the coming year. For instance, if you notice a high tax bill, you might decide to increase your contributions to a 401(k) or 403(b) to lower your taxable income. Alternatively, you might engage in “tax-loss harvesting” in your brokerage account to offset capital gains.

Historical Record and Audit Protection

Your tax returns serve as a historical record of your financial journey. It is generally recommended to keep copies of your returns and supporting documents for at least three to seven years. In the event of an IRS audit, these records are your primary defense, proving that the income and deductions you reported were accurate.

In conclusion, a federal tax return is far more than a set of forms; it is a vital instrument of financial accountability and planning. By understanding how income is reported, how deductions and credits work, and the importance of timely filing, you can take control of your financial destiny. Whether you are aiming for a larger refund or looking to minimize your liability, mastering the federal tax return is a crucial step toward achieving long-term financial stability and success.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.