Inflation is often described by economists as the “hidden tax” on your wealth. It is the steady erosion of purchasing power, where the dollar in your pocket today buys less than it did yesterday. For any savvy investor or individual focused on personal finance, understanding how to measure this phenomenon is not just an academic exercise; it is a fundamental skill for wealth preservation. The primary tool used to measure this change is the Consumer Price Index (CPI).

By learning how to compute the inflation rate from CPI, you gain the ability to look past “nominal” figures—like your salary or your portfolio’s return—and see the “real” value of your money. This guide provides a comprehensive breakdown of the CPI, the mathematical formula for inflation, and how to apply these insights to your financial strategy.

1. Decoding the Consumer Price Index (CPI)

Before you can calculate the inflation rate, you must first understand the data source. The Consumer Price Index (CPI) is a statistical estimate constructed using the prices of a sample of representative items whose prices are collected periodically. Think of it as a “market basket” of goods and services that the average consumer purchases regularly.

Understanding the “Market Basket”

Government agencies, such as the Bureau of Labor Statistics (BLS) in the United States, track the prices of thousands of items across several categories. These categories include housing (the largest component), transportation, food and beverages, medical care, education, and recreation. Each category is “weighted” based on its importance to the average household budget. For instance, a 10% increase in the price of rent has a much larger impact on the CPI than a 10% increase in the price of postage stamps.

Headline CPI vs. Core CPI

When you look up CPI data to perform your calculations, you will often see two different figures. “Headline CPI” includes all items in the basket, including volatile categories like food and energy. While this represents the total cost of living, it can fluctuate wildly based on oil prices or seasonal crop yields.

“Core CPI,” on the other hand, strips away food and energy prices to reveal the underlying long-term inflation trend. For long-term financial planning and understanding the structural health of the economy, many investors prefer to look at Core CPI to filter out the “noise” of temporary price shocks.

CPI-U and CPI-W

The BLS provides different indices for different populations. The most commonly cited is the CPI-U, which represents “All Urban Consumers” and covers about 93% of the U.S. population. There is also the CPI-W, which covers “Urban Wage Earners and Clerical Workers.” For most personal finance applications, the CPI-U is the standard benchmark used for computing the general inflation rate.

2. The Mechanics: How to Calculate the Inflation Rate

Computing the inflation rate is a straightforward mathematical process once you have the CPI data for two specific points in time. The inflation rate is essentially the “percentage change” in the index over a specific period.

The Standard Inflation Formula

The formula to calculate the inflation rate between two periods is as follows:

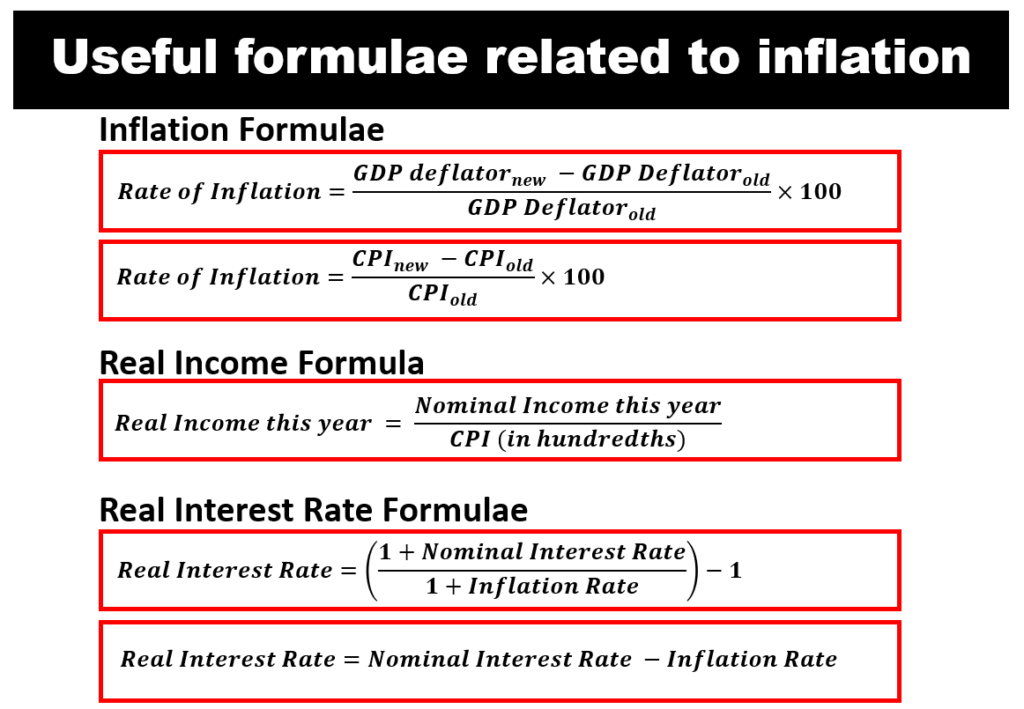

Inflation Rate = [(CPI at End Date – CPI at Beginning Date) / CPI at Beginning Date] × 100

In this equation:

- CPI at End Date: This is the current or more recent index value.

- CPI at Beginning Date: This is the historical index value you are comparing it against.

- The Result: Multiplying by 100 converts the decimal into a percentage, which is the standard way inflation is reported.

A Practical Example: Year-over-Year (YoY) Calculation

Let’s assume you want to calculate the inflation rate between January 2023 and January 2024. You go to the official BLS database and find the following (hypothetical) figures:

- CPI in January 2023: 300.5

- CPI in January 2024: 310.8

Using the formula:

- Subtract the old CPI from the new CPI: 310.8 – 300.5 = 10.3

- Divide the result by the old CPI: 10.3 / 300.5 = 0.03427

- Multiply by 100 to get the percentage: 0.03427 × 100 = 3.43%

This means that, on average, the cost of living increased by 3.43% over that one-year period.

Month-over-Month (MoM) and Cumulative Inflation

While year-over-year data is the most common, you can use this same formula to calculate month-over-month inflation (by using CPI data from two consecutive months). Additionally, you can calculate cumulative inflation over several decades. For example, if you wanted to see how much $100 in 1990 would be worth today, you would take the current CPI and compare it to the average CPI of 1990.

3. Real-World Financial Implications: Beyond the Numbers

Understanding the math is the first step; applying it to your “Money” strategy is where the value lies. Inflation impacts every facet of personal finance, from your paycheck to your retirement account.

The Erosion of Purchasing Power

If your local bank offers a savings account with a 1.0% interest rate, but the inflation rate you just calculated is 3.5%, you are technically losing money. In “nominal” terms, your balance is growing, but in “real” terms, your purchasing power is shrinking by 2.5% per year. This is why keeping excessive amounts of cash in low-yield accounts can be a dangerous long-term strategy. Knowing the inflation rate allows you to set a “hurdle rate” for your investments—the minimum return you need just to break even against rising prices.

Nominal vs. Real Interest Rates (The Fisher Equation)

In finance, the “Fisher Equation” relates the nominal interest rate to the real interest rate and inflation. The formula is:

Real Interest Rate ≈ Nominal Interest Rate – Inflation Rate

If you are a bond investor or a lender, this calculation is vital. If a corporate bond pays a 5% coupon (nominal rate) and inflation is 4%, your real return is only 1%. By computing the inflation rate from the CPI, you can accurately assess whether an investment is truly growing your wealth or simply treading water.

Cost of Living Adjustments (COLA)

Many employment contracts and government benefits (like Social Security in the U.S.) include Cost of Living Adjustments. These adjustments are usually tied directly to the CPI. If you are a freelancer or a business owner, you should use the CPI calculation to adjust your rates annually. If you haven’t raised your prices in two years while the CPI has risen by 7%, you have effectively given yourself a 7% pay cut.

4. Strategic Financial Planning in a High-Inflation Environment

Once you are comfortable calculating inflation, you can use that data to adjust your financial behavior. High inflation environments require a different playbook than low inflation periods.

Identifying Inflation-Hedged Assets

When your CPI calculations show a rising trend, it may be time to pivot toward assets that historically perform well under inflationary pressure. These often include:

- TIPS (Treasury Inflation-Protected Securities): These are government bonds where the principal increases with the CPI.

- Real Estate: Property values and rents often rise in tandem with general inflation.

- Commodities: Raw materials like gold, oil, and agricultural products often see price increases that lead the CPI.

- Equities with Pricing Power: Look for companies that can pass on higher costs to consumers without losing demand.

Budgeting for “Personal” Inflation

It is important to remember that the CPI is an average. If you spend a large portion of your income on gasoline and meat, and those specific categories are rising faster than the general index, your “personal inflation rate” may be higher than the national average. By looking at the sub-indices of the CPI (which breaks down costs by category), you can more accurately forecast your future expenses and adjust your budget accordingly.

Debt Management and Inflation

Interestingly, inflation can be a friend to those with fixed-rate debt. If you have a 30-year fixed mortgage at 3% and inflation rises to 6%, you are paying back your loan with “cheaper” dollars. Your debt stays the same in nominal terms, but as your wages (ideally) rise with inflation, the debt becomes a smaller percentage of your total income. Computing the inflation rate helps you decide whether to pay off debt aggressively or let it ride while investing in higher-yielding assets.

Conclusion

Calculating the inflation rate from the CPI is more than just a math problem; it is a vital diagnostic tool for your financial health. By mastering the formula—[(New CPI – Old CPI) / Old CPI] × 100—you empower yourself to see the true landscape of the economy. Whether you are negotiating a salary increase, choosing between investment vehicles, or simply trying to maintain your standard of living, the ability to quantify the changing value of money is the hallmark of a financially literate individual. In an era of economic volatility, those who monitor the CPI and understand its implications are best positioned to protect and grow their wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.