Compound interest is often referred to as the “eighth wonder of the world.” This attribution, frequently linked to Albert Einstein, underscores a fundamental truth in the realm of personal finance: the ability of money to grow exponentially over time is the most potent tool an investor possesses. Unlike simple interest, which is calculated solely on the principal amount, compound interest is calculated on the initial principal and also on the accumulated interest of previous periods.

Finding compound interest—both in terms of calculating it and identifying the right financial vehicles to capture it—is the cornerstone of long-term wealth building. Whether you are a novice saver or a seasoned investor, understanding the mechanics of compounding is essential for achieving financial independence.

Understanding the Mechanics of Compound Interest

To effectively “find” and utilize compound interest, one must first deconstruct how it functions. At its core, compounding is the process where the value of an investment increases because the earnings on an investment, both capital gains and interest, earn interest as time passes.

Simple vs. Compound Interest

The difference between simple and compound interest may seem negligible in the short term, but over decades, the gap becomes a chasm. Simple interest is linear. If you invest $1,000 at a 5% simple interest rate, you earn $50 every year. After 20 years, you have $2,000.

In contrast, compound interest is exponential. Using the same $1,000 at a 5% interest rate compounded annually, you earn $50 in the first year. In the second year, however, you earn 5% on $1,050, which is $52.50. By the 20th year, your balance would be approximately $2,653. The “extra” $653 is the result of interest earning interest.

The Variables: Principal, Rate, Time, and Frequency

There are four primary levers that determine how much compound interest you will find at the end of your investment horizon:

- Principal (P): The initial amount of money you invest or deposit.

- Interest Rate (r): The annual interest rate (expressed as a decimal).

- Time (t): The number of years the money is invested.

- Compounding Frequency (n): The number of times interest is compounded per year (e.g., daily, monthly, quarterly, or annually).

The frequency of compounding is a silent but powerful variable. The more frequently interest is added to your principal, the faster your wealth grows. Daily compounding yields more than annual compounding because your interest starts earning its own interest much sooner.

How to Calculate Compound Interest: Formulas and Tools

While modern technology has made manual calculations largely unnecessary, understanding the underlying math provides a deeper insight into how your wealth is generated. To “find” the future value of an investment, we use a specific mathematical framework.

The Mathematical Formula

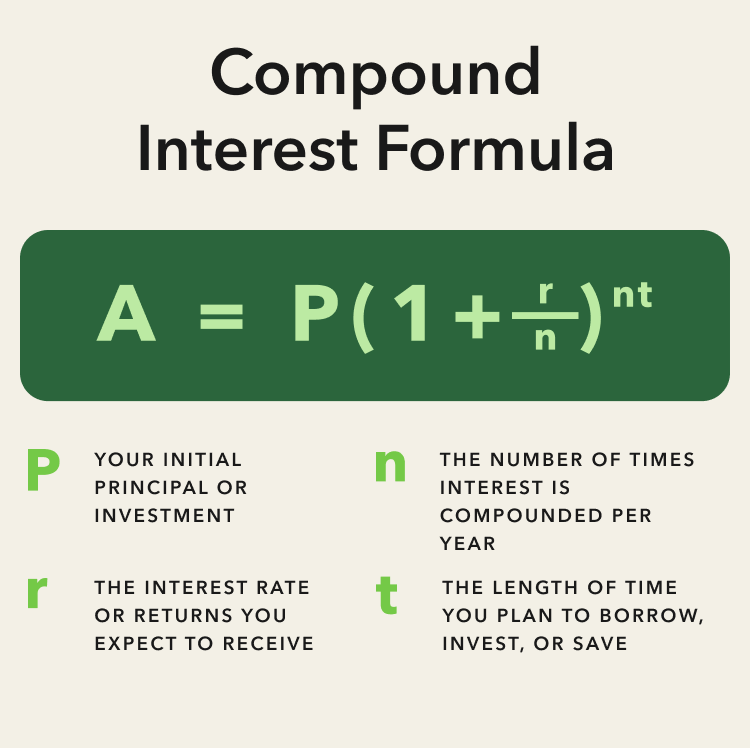

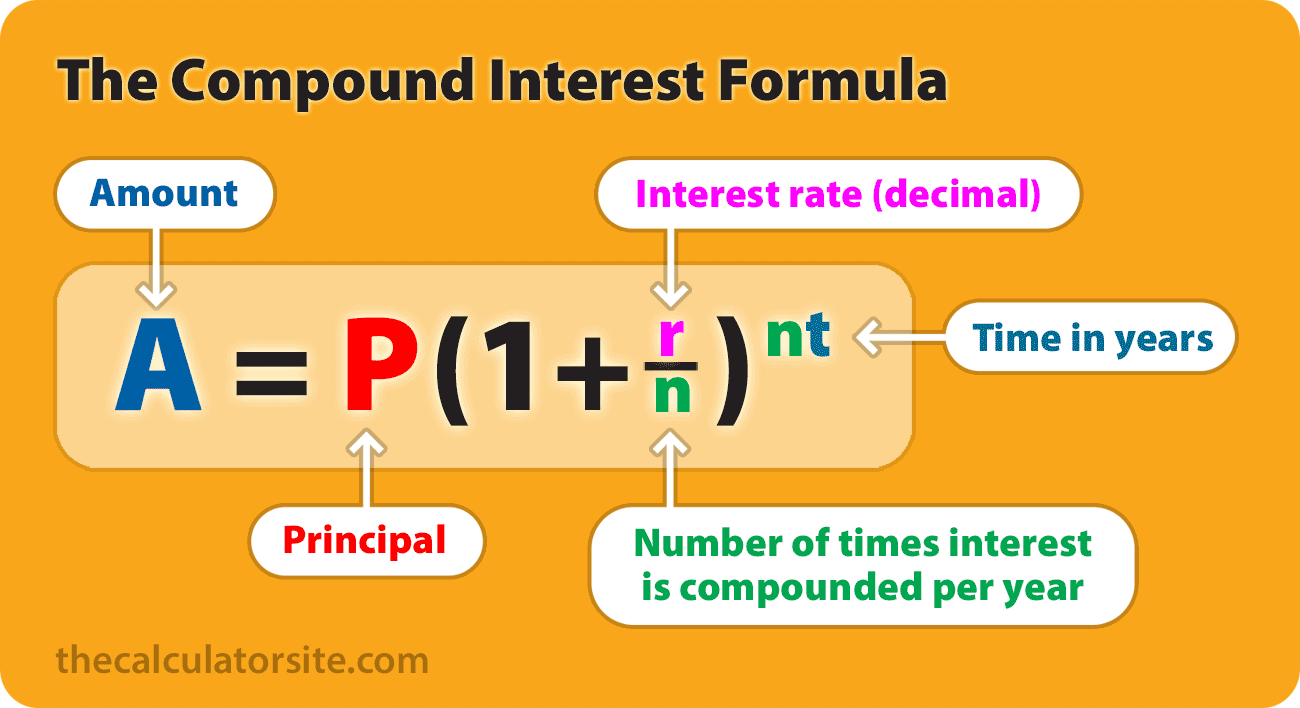

The standard formula for compound interest is:

A = P(1 + r/n)^(nt)

- A = the future value of the investment/loan, including interest.

- P = the principal investment amount.

- r = the annual interest rate (decimal).

- n = the number of times that interest is compounded per year.

- t = the number of years the money is invested for.

For example, if you deposit $5,000 into a high-yield savings account with a 4% interest rate compounded monthly (n=12) for 10 years (t=10), the calculation would look like this:

A = 5000(1 + 0.04/12)^(12*10).

The resulting balance would be approximately $7,454.16.

The Rule of 72 (The Quick Shortcut)

For those who want to find the impact of compound interest without a calculator, the “Rule of 72” is an invaluable mental shortcut. It estimates how long it will take for an investment to double at a fixed annual rate of interest.

Simply divide 72 by your annual interest rate. For instance, if your investment returns 6% per year, it will take roughly 12 years (72 / 6 = 12) for your money to double. If you can find an investment that returns 9%, your money doubles in just 8 years. This rule highlights why even small increases in your rate of return can lead to massive differences in long-term wealth.

Utilizing Financial Calculators and Spreadsheets

In a professional or business finance context, finding compound interest is usually handled via software. Programs like Microsoft Excel or Google Sheets use the FV (Future Value) function. The syntax is =FV(rate, nper, pmt, [pv], [type]).

This tool is particularly useful because it allows you to factor in monthly contributions (pmt), which more accurately reflects how most people save for retirement. Finding the “find” in this context moves from a manual math problem to a dynamic simulation of your financial future.

Strategies to Maximize Compounding Effects

Knowing how to calculate interest is only half the battle; the other half is structuring your finances to maximize its effects. Compounding rewards specific behaviors and punishes delay.

The Importance of Early Entry

The most critical factor in the compound interest equation is not the interest rate or the principal—it is time. This is often referred to as the “Cost of Waiting.”

Consider two investors: Investor A starts at age 20, investing $200 a month until age 30, and then stops entirely. Investor B starts at age 30 and invests $200 a month every month until age 60. Despite Investor B contributing for three times as many years, Investor A will likely end up with a larger nest egg because their initial investments had an extra decade to compound. To find the most compound interest, you must start as early as possible.

Increasing Contribution Frequency

While the initial principal is important, the “fuel” for the compounding engine is consistent, recurring contributions. When you add money to your investment regularly (monthly or with every paycheck), you are increasing the base upon which interest is calculated. This creates a “snowball effect.” As the principal grows through both contributions and interest, the subsequent interest payments become progressively larger, leading to vertical growth in the later stages of the investment timeline.

Minimizing Fees and Taxes

One of the greatest enemies of compound interest is the “leakage” caused by high management fees and taxes. In the world of investing, a 1% management fee might sound small, but over 30 years, it can strip away hundreds of thousands of dollars from your final balance. To find and keep the maximum amount of interest, investors should look toward low-cost index funds and tax-advantaged accounts like IRAs or 401(k)s, where interest can grow unhindered by annual tax hits.

Real-World Applications in Personal Finance

Where do you actually go to find compound interest? In the modern financial landscape, it exists in several forms, ranging from “safe” bank products to more volatile market instruments.

Compound Interest in Savings Accounts and CDs

For those seeking low risk, compound interest is found in High-Yield Savings Accounts (HYSAs) and Certificates of Deposit (CDs). These accounts typically offer an Annual Percentage Yield (APY) that reflects the effect of compounding over a year. While the rates here are generally lower than the stock market, they provide a guaranteed way to see your money grow daily or monthly without the risk of principal loss.

The Power of Reinvested Dividends

In the stock market, compound interest takes the form of capital appreciation and, perhaps more importantly, reinvested dividends. Many established companies pay out a portion of their profits to shareholders. By utilizing a Dividend Reinvestment Plan (DRIP), you automatically use those dividends to buy more shares of the stock. This increases the number of shares you own, which in turn increases the next dividend payment. This is a pure form of compounding that has historically been a primary driver of total returns in the S&P 500.

Retirement Accounts: 401(k)s and IRAs

Retirement accounts are the ultimate environment for compound interest. Because these accounts are tax-deferred (like a traditional 401(k)) or tax-free (like a Roth IRA), the money that would have normally gone to the government in taxes stays in your account to earn more interest. Furthermore, many employers offer a “match” on 401(k) contributions. This match is essentially an immediate 100% return on your investment, which then begins to compound alongside your own contributions.

Conclusion: The Discipline of Patience

Finding compound interest is not a “get rich quick” scheme; it is a “get rich surely” strategy. The math is irrefutable, but the execution requires psychological discipline. The greatest challenge to compounding is the temptation to withdraw funds or stop contributions during market downturns.

To truly find the power of compound interest, one must adopt a long-term perspective. Wealth is built in the “boring” middle years, where the growth seems slow and the progress is incremental. However, if you understand the formula, utilize the right financial tools, and give your investments the gift of time, the physics of finance will eventually take over. The result is a financial foundation that grows not just through your labor, but through the tireless, exponential work of your money itself.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.