In the world of personal finance and professional investment, numbers are the primary language. However, raw data often fails to tell the full story. To truly understand the health of a portfolio, the efficiency of a business, or the impact of a savings plan, one must master the relationship between numbers. This is where the percentage calculation becomes the most vital tool in a financial toolkit.

Understanding how to figure out a percentage of two numbers is not merely a middle-school math exercise; it is the foundation of financial literacy. Whether you are calculating the dividend yield on a stock, determining the interest rate on a loan, or assessing the growth of your net worth, percentages provide the context necessary to make informed, strategic decisions.

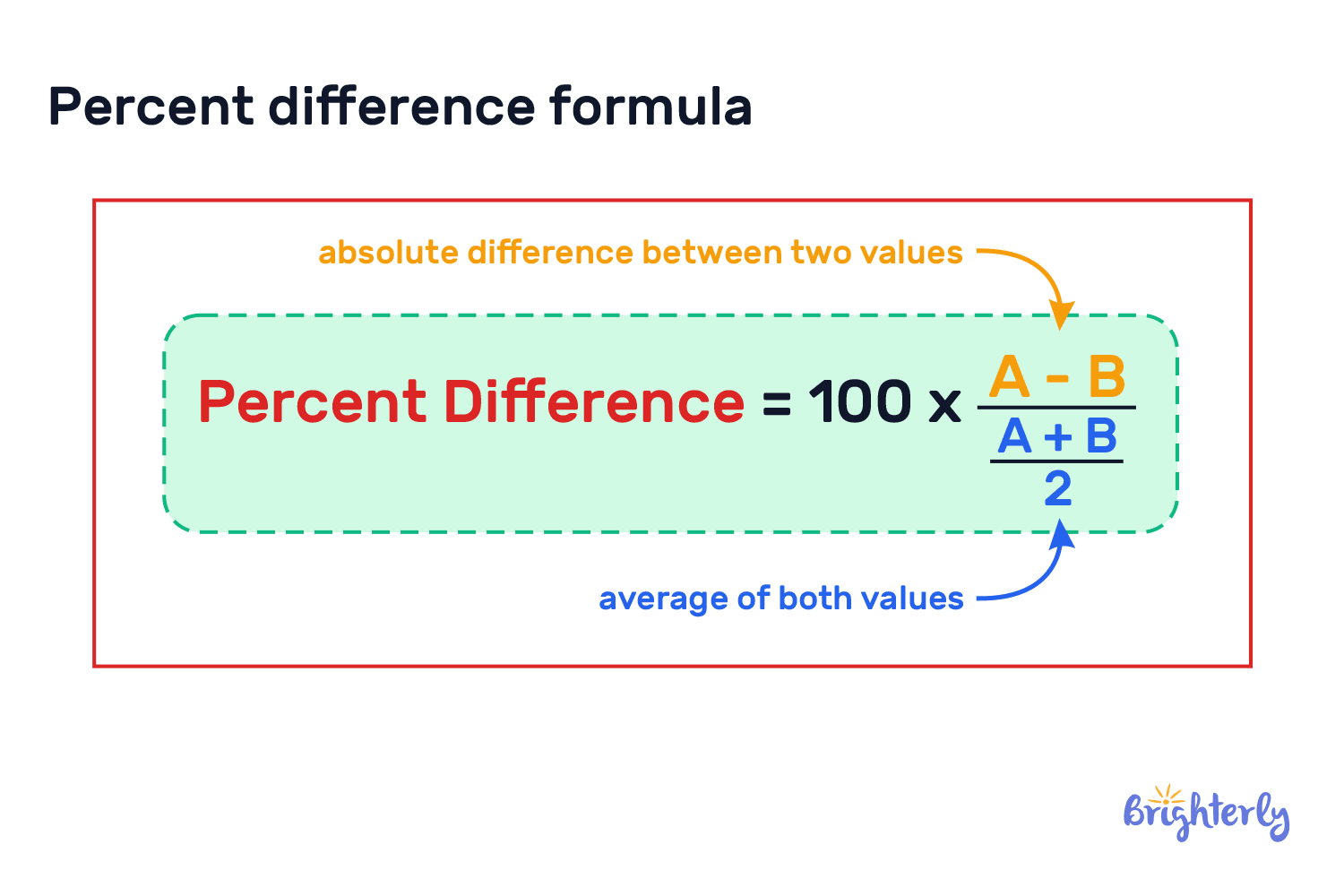

The Fundamentals of Percentage Calculations in Finance

At its core, a percentage is a way of expressing a ratio as a fraction of 100. In finance, this allows us to compare disparate figures on an equal playing field. Without percentages, comparing a $500 profit on a $5,000 investment to a $5,000 profit on a $100,000 investment would be confusing. Percentages clarify that the former is a 10% return, while the latter is only 5%.

The Core Formula: Part over Whole

The basic formula for finding the percentage of two numbers is:

(Part / Whole) × 100 = Percentage

In a financial context, the “Part” is usually the specific value you are investigating (such as interest earned, tax paid, or a price discount), and the “Whole” is the base value (the principal investment, total income, or original price).

For example, if you earned $250 in interest on a savings account balance of $10,000, you would divide 250 by 10,000 to get 0.025. Multiplying by 100 gives you 2.5%. This simple calculation allows you to compare that savings account’s performance against inflation or other investment vehicles.

Percentage Increase vs. Percentage Decrease

Financial trends are rarely static. Understanding the “Percentage Change” is crucial for tracking market volatility or salary growth. The formula for this is slightly different:

[(New Value – Old Value) / Old Value] × 100

If your stock portfolio was worth $50,000 last year and is worth $55,000 today, the calculation would be:

($55,000 – $50,000) / $50,000 = 0.10.

Multiplying by 100 results in a 10% increase. Conversely, if the value dropped, the result would be a negative percentage, indicating a loss. Mastering this distinction is the first step in sophisticated trend analysis and risk management.

Practical Applications: From Discounts to Interest Rates

The most common daily encounter with percentages involves consumer finance. While these may seem like small calculations, their cumulative effect on a person’s financial health over a lifetime is massive.

Evaluating Sales and Consumer Savings

When a retailer offers a “30% off” sale, or a service provider increases their rates by 15%, being able to calculate the dollar impact instantly is a hallmark of a disciplined spender. To find the dollar amount of a percentage discount, you reverse the basic formula:

(Percentage / 100) × Original Price = Discount Amount

If a luxury watch is listed at $2,400 with a 15% discount, you calculate (15/100) × 2,400 to find a $360 savings. Understanding these figures helps in “opportunity cost” analysis—deciding if the money saved is better utilized in an interest-bearing account or used to pay down high-interest debt.

Understanding APR and Effective Interest

Debt is often the biggest hurdle to wealth accumulation. Credit cards, mortgages, and auto loans are all priced using Annual Percentage Rates (APR). However, many consumers fail to realize how a small percentage change can lead to thousands of dollars in interest over time.

Calculating the percentage of interest relative to the principal helps in prioritizing debt repayment via the “avalanche method.” By identifying which debt has the highest percentage cost—rather than just the highest dollar balance—you can minimize the total interest paid. For instance, a $1,000 credit card balance at 24% APR is significantly more “expensive” than a $5,000 student loan at 4% APR, even though the latter has a larger total balance.

Advanced Financial Metrics: ROI and Profit Margins

For the investor or business owner, percentages are the ultimate benchmarks for success. They allow for “vertical analysis,” where every line item on a financial statement is compared to a base figure to identify inefficiencies or strengths.

Calculating Return on Investment (ROI)

ROI is perhaps the most important percentage in the world of money. it measures the gain or loss generated on an investment relative to the amount of money invested.

ROI = (Current Value of Investment – Cost of Investment) / Cost of Investment

If you purchased an investment property for $300,000 and spent $50,000 on renovations, your total cost is $350,000. If you later sell it for $450,000, your ROI is ($450,000 – $350,000) / $350,000, which equals approximately 28.5%. This percentage allows you to determine if the time and capital risked were worth the reward compared to passive investments like index funds.

Net vs. Gross Profit Margins

In business finance, knowing the percentage of revenue that turns into profit is essential for sustainability.

- Gross Profit Margin: This is (Gross Profit / Revenue) × 100. It shows the percentage of revenue remaining after deducting the cost of goods sold.

- Net Profit Margin: This is (Net Income / Revenue) × 100. This is the “bottom line” percentage—how much of every dollar earned actually stays in the company’s pocket after taxes, interest, and operating expenses.

A company might have millions in revenue, but if its net profit margin is only 2%, it is in a precarious financial position. Analyzing these percentages helps investors identify “lean” companies that are efficient at converting sales into actual wealth.

Percentages in Personal Budgeting and Tax Planning

Beyond investing and debt, percentages serve as the guardrails for a healthy personal financial plan. They help move the needle from “spending what is left” to “allocating with intention.”

The 50/30/20 Rule

One of the most popular budgeting frameworks is based entirely on percentages of your after-tax income:

- 50% for Needs: Housing, utilities, groceries, and insurance.

- 30% for Wants: Dining out, travel, and hobbies.

- 20% for Savings and Debt Repayment: Building an emergency fund and investing for retirement.

By calculating these percentages monthly, you can see if your lifestyle is “out of balance.” If your housing costs are 65% of your income, the percentage calculation highlights a structural flaw in your finances that a simple dollar-to-dollar budget might obscure.

Effective Tax Rate Calculations

In the United States and many other countries, tax systems are progressive, meaning different portions of your income are taxed at different rates. This makes your “Effective Tax Rate” the most important percentage to know for tax planning.

Effective Tax Rate = (Total Tax Paid / Total Taxable Income) × 100

Knowing your effective rate (e.g., 18%) rather than just your top marginal bracket (e.g., 24%) allows for more accurate retirement projections and helps you decide whether to contribute to a traditional 401(k) or a Roth IRA.

Tools for Financial Precision

While the mental math of “moving the decimal point” is a great skill, professional-grade financial management requires precision. Modern tools make calculating complex percentages effortless, but you must know how to input the data correctly.

Leveraging Digital Spreadsheets

Programs like Microsoft Excel or Google Sheets are the industry standard for financial percentage calculations. To find the percentage of a value in a cell, you simply use the formula =A1/B1 and then click the “Percent Style” button.

For more complex needs, such as Compound Annual Growth Rate (CAGR), spreadsheets use the formula: =((End Value/Start Value)^(1/Number of Periods))-1. This percentage tells you the mean annual growth rate of an investment over a specified period of time longer than one year, accounting for the “snowball effect” of compounding.

Financial Calculators and Future Value

When dealing with time-value-of-money problems—such as how much your current savings will be worth in 20 years given a certain percentage of return—financial calculators are indispensable. Understanding the percentage of “inflation-adjusted returns” is the difference between a retirement plan that works on paper and one that works in reality. If you expect a 7% market return but inflation is at 3%, you must calculate your “real” percentage of growth as roughly 4% to ensure your future purchasing power.

In conclusion, the ability to figure out a percentage of two numbers is the bridge between being a passive observer of your money and becoming an active manager of your wealth. By applying these formulas to your spending, your debt, your investments, and your taxes, you gain a level of clarity that allows for long-term financial security. Percentages turn raw numbers into actionable intelligence, ensuring that every dollar you earn is working as efficiently as possible for your future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.