Interest is often described as the “rent” paid for the use of money. Whether you are a borrower seeking to understand the true cost of a mortgage or an investor looking to maximize the growth of your portfolio, understanding how to compute interest is a fundamental pillar of financial literacy. In the world of personal finance, the difference between simple and compound interest can represent thousands, if not millions, of dollars over a lifetime.

By mastering these calculations, you move from being a passive participant in the economy to an active strategist capable of making informed decisions about debt, savings, and investments. This guide explores the mechanics of interest computation, the nuances of different financial products, and the tools you can use to project your financial future.

Understanding the Fundamentals: Simple vs. Compound Interest

Before diving into complex financial models, one must distinguish between the two primary ways interest is calculated. The distinction lies in whether interest is earned only on the initial amount or if it also earns interest on itself.

Simple Interest: The Straightforward Approach

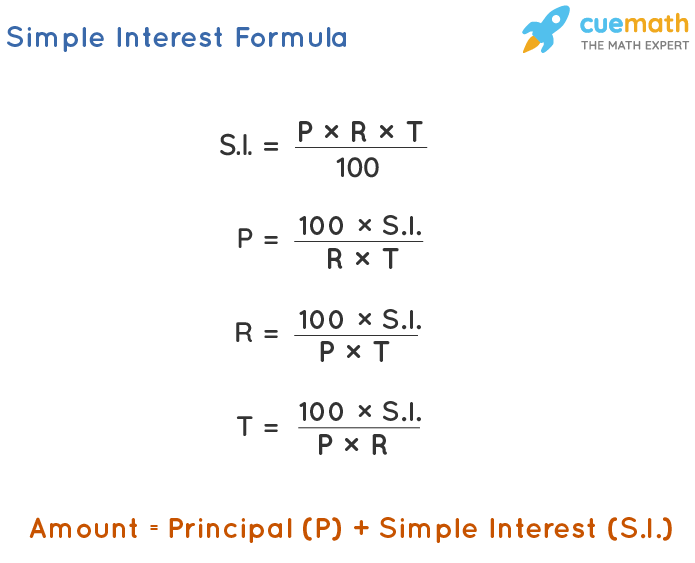

Simple interest is the most basic form of calculation. It is determined by multiplying the daily interest rate by the principal by the number of days that elapse between payments. Simple interest is most commonly used in short-term personal loans or specific types of consumer credit.

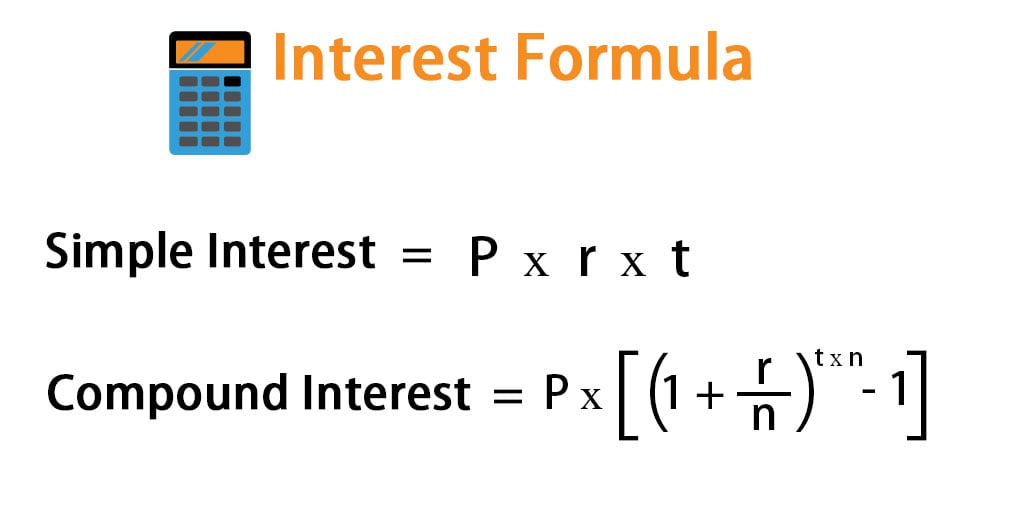

The formula for simple interest is:

I = P × r × t

- P (Principal): The initial amount of money borrowed or invested.

- r (Annual Interest Rate): The interest rate expressed as a decimal (e.g., 5% becomes 0.05).

- t (Time): The duration for which the money is borrowed or invested, usually expressed in years.

For example, if you invest $10,000 at a 5% simple interest rate for three years, you would earn $1,500 in interest ($10,000 × 0.05 × 3). At the end of the term, your total balance would be $11,500.

Compound Interest: The Engine of Wealth Creation

Compound interest is what Albert Einstein allegedly called the “eighth wonder of the world.” Unlike simple interest, compound interest is calculated on the initial principal and also on the accumulated interest of previous periods. This creates a “snowball effect” where your wealth grows at an accelerating rate.

The formula for compound interest is:

A = P(1 + r/n)^{nt}

- A: The future value of the investment/loan, including interest.

- n: The number of times interest is compounded per year (e.g., 12 for monthly, 365 for daily).

If you take that same $10,000 at 5% interest but compound it monthly for three years, your total would be approximately $11,614.72. The extra $114.72 is the result of your interest earning its own interest.

The Key Variables: Principal, Rate, and Time

Every interest calculation relies on these three pillars. The Principal is your starting point; the larger the principal, the more significant the absolute interest figures. The Rate is the price of the money; even a 1% difference in rates can lead to massive discrepancies in long-term outcomes. Finally, Time is the most potent variable in compounding. The longer you allow interest to accrue, the more the exponential nature of compounding takes over, making early retirement planning more effective than starting late with larger sums.

Practical Applications: Computing Interest on Loans and Mortgages

For most individuals, interest is something they pay rather than earn. From credit cards to home loans, knowing how to compute the cost of debt allows you to prioritize which liabilities to pay off first.

Amortization Schedules: Decoding Monthly Payments

Most long-term loans, like mortgages or auto loans, use an amortization schedule. This is a table detailing each periodic payment on an amortizing loan. While your monthly payment remains constant, the proportion of that payment going toward interest versus principal changes over time.

In the early stages of a 30-year mortgage, the majority of your payment is directed toward interest. As the principal balance decreases, the interest calculated on that balance also decreases, allowing more of your monthly payment to “attack” the principal. Computing this requires an understanding of how the monthly interest rate (Annual Rate / 12) is applied to the remaining balance each month.

The Impact of Interest Rates on Long-term Debt

When interest rates rise even slightly, the total cost of a loan can skyrocket. For instance, on a $300,000 mortgage, the difference between a 4% interest rate and a 6% interest rate over 30 years is over $130,000 in total interest paid. By learning to compute these figures, borrowers can see the value of waiting for better market conditions or improving their credit scores to secure a lower rate.

Strategies to Minimize Interest Expenses

Once you know how to compute the interest on your debt, you can employ strategies to reduce it. One of the most effective methods is making “principal-only” payments. Because interest is typically calculated based on the current outstanding balance, reducing that balance faster than scheduled drastically lowers the total interest accrued over the life of the loan. Even one extra payment per year on a mortgage can shave years off the term and save tens of thousands of dollars.

The Investor’s Perspective: Calculating Returns on Savings and Investments

On the flip side of the coin, interest computation is the primary tool for evaluating the success of an investment strategy. Whether you are looking at safe-haven assets or growth-oriented accounts, the math remains the central arbiter of value.

High-Yield Savings Accounts and CDs

For conservative investors, High-Yield Savings Accounts (HYSA) and Certificates of Deposit (CDs) are common tools. These typically use daily or monthly compounding. When comparing these products, it is vital to look at the Annual Percentage Yield (APY). While the nominal interest rate tells you the “face value” rate, the APY accounts for the frequency of compounding, providing a more accurate picture of what you will actually earn in a year.

The Rule of 72: A Shortcut for Projecting Growth

For those who want to compute interest outcomes without a scientific calculator, the “Rule of 72” is an invaluable mental model. To estimate how many years it will take for your money to double at a given fixed annual interest rate, divide 72 by that rate.

- At a 6% interest rate, your money doubles in 12 years (72 / 6).

- At a 10% interest rate, your money doubles in about 7.2 years (72 / 10).

This simple computation helps investors quickly weigh the opportunity costs of different investment vehicles.

Annual Percentage Yield (APY) vs. Annual Percentage Rate (APR)

In the financial world, these two terms are often confused. APR (Annual Percentage Rate) is typically used for loans and represents the simple interest rate over a year plus fees. APY (Annual Percentage Yield) is used for investment and savings accounts and includes the effect of compounding. When you are computing interest for a savings account, always use the APY to see the true growth potential.

Advanced Financial Tools and Digital Computation Methods

In the modern era, you don’t need to do all these calculations by hand. However, knowing how to use digital tools effectively requires an understanding of the underlying logic.

Using Spreadsheet Functions (Excel/Google Sheets)

Spreadsheets are the professional’s tool of choice for computing complex interest scenarios. Functions like =PMT, =FV, and =IPMT allow you to model various financial futures.

- =PMT: Calculates the payment for a loan based on constant payments and a constant interest rate.

- =FV: Calculates the future value of an investment based on periodic, constant payments and a constant interest rate.

- =RATE: Helps you determine the interest rate necessary to reach a specific financial goal within a set timeframe.

By building your own interest models in a spreadsheet, you can perform “what-if” analysis—adjusting variables like the interest rate or monthly contribution to see how they impact your net worth over decades.

Financial Calculators and Online Tools

There are thousands of specialized calculators available online for specific needs, such as “Credit Card Payoff Calculators” or “Compound Interest Calculators.” These tools are excellent for quick checks, but the savvy individual uses them to verify their own manual computations. Understanding the “why” behind the numbers ensures that you aren’t misled by marketing materials that might emphasize a low interest rate while hiding a high APY or frequent compounding periods.

Conclusion: Empowering Financial Literacy Through Calculation

The ability to compute interest is more than just a mathematical skill; it is a vital survival tool in a debt-based economy. By understanding the mechanics of simple and compound interest, you gain the clarity needed to navigate the complexities of mortgages, credit cards, and retirement accounts.

Whether you are seeking to eliminate debt or build a legacy of wealth, the formulas remain the same. The math of interest rewards the disciplined and the informed. By consistently applying these calculations to your personal finances, you can minimize the “rent” you pay to others and maximize the growth of your own capital, ensuring a more secure and prosperous financial future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.