In the realm of finance, numbers are the language of progress. Whether you are tracking the growth of a retirement portfolio, evaluating the success of a marketing campaign’s ROI, or measuring year-over-year revenue for a startup, the ability to calculate and interpret percent increase is a fundamental skill. It moves beyond simple arithmetic, serving as a vital diagnostic tool that reveals the velocity of wealth accumulation and the efficiency of capital allocation.

Understanding percent increase allows investors and professionals to strip away the noise of raw currency figures and focus on relative performance. A $1,000 gain is impressive on a $5,000 investment (a 20% increase), but it is negligible on a $1,000,000 portfolio (a 0.1% increase). This guide provides a comprehensive deep dive into how to find percent increase, specifically through the lens of personal and business finance.

The Mathematical Foundation of Wealth Measurement

Before applying the concept to complex financial instruments, one must master the basic formula. In finance, percent increase represents the relative change between an initial value and a final value, expressed as a portion of the original amount.

The Standard Percent Increase Formula

To find the percent increase, you follow a three-step mathematical process:

- Subtract the original value (the starting amount) from the new value (the current amount). This gives you the “absolute increase.”

- Divide that absolute increase by the original value.

- Multiply the resulting decimal by 100 to convert it into a percentage.

Mathematically, it looks like this:

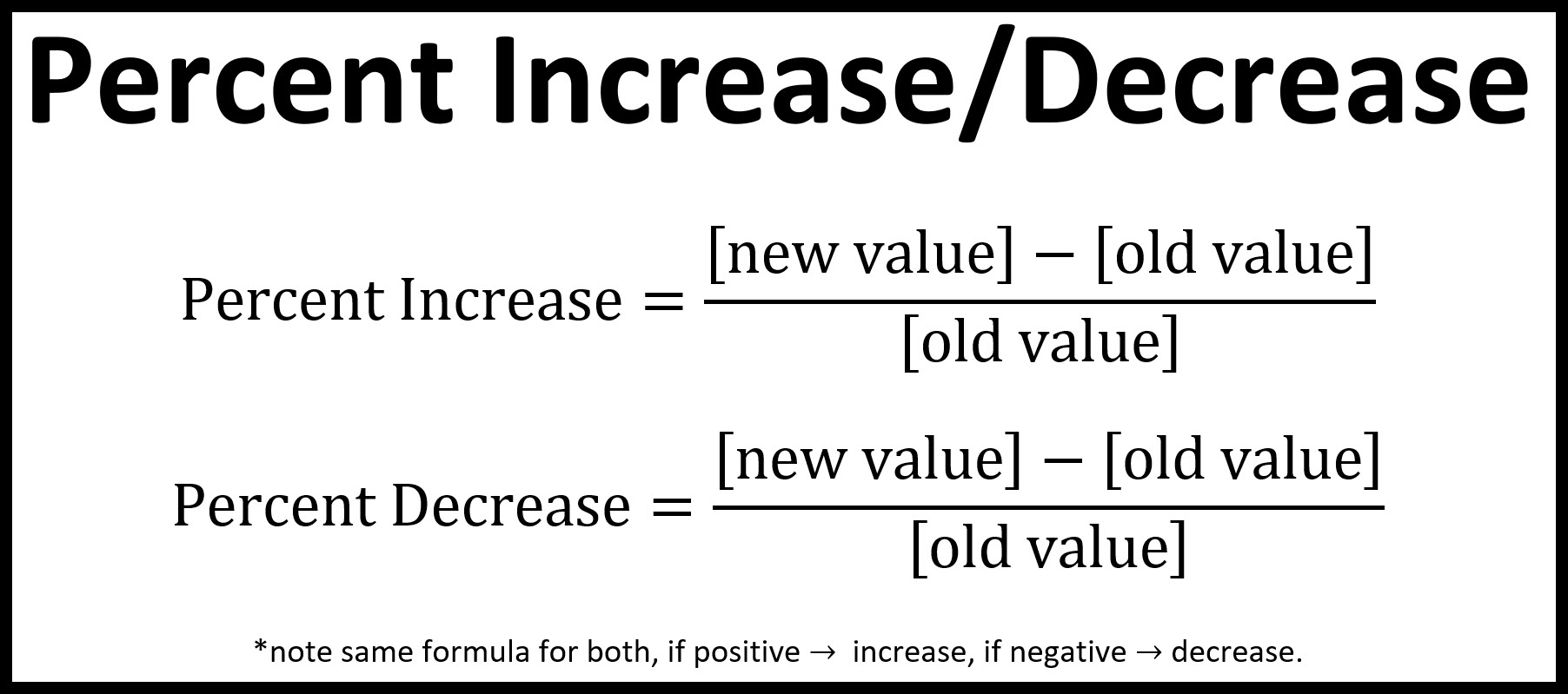

[(New Value - Old Value) / Old Value] x 100 = Percent Increase

Why the Base Value Matters

A common mistake in financial analysis is dividing by the new value instead of the original value. In the context of money, your “base” is your initial risk or your starting capital. If you buy a share of stock at $100 and it rises to $150, your profit is $50. Dividing that $50 by the $100 starting price shows a 50% increase. If you mistakenly divided by the $150 ending price, you would calculate 33%, which inaccurately represents your actual return on investment (ROI).

Applying Percent Increase to Investment Portfolios

For the individual investor, percent increase is the primary metric for evaluating the health of an asset allocation strategy. While dollar amounts pay the bills, percentages tell you if your strategy is actually beating the market.

Measuring Capital Gains

The most frequent use of percent increase in investing is calculating capital gains. When evaluating a stock, mutual fund, or real estate asset, the percent increase indicates how much the asset has appreciated over a specific period. This is essential for comparing disparate assets. For example, if your gold holdings increased by 5% while your S&P 500 index fund increased by 12%, the percentage gives you a clear indication of where your capital is working hardest, regardless of how much total cash is in each account.

Dividend Growth Tracking

Income-focused investors use percent increase to track “Dividend Growth.” If a company paid a dividend of $1.20 per share last year and raised it to $1.32 this year, the 10% increase is a signal of the company’s financial health and commitment to shareholders. Consistently calculating these increases helps investors identify “Dividend Aristocrats”—companies that have increased their payouts for at least 25 consecutive years.

Real vs. Nominal Returns: Factoring in Inflation

In finance, it is crucial to distinguish between nominal percent increase and real percent increase. If your savings account offers a 4% interest rate (a 4% nominal increase), but inflation is running at 5%, your “real” percent increase is actually a negative 1%. By applying the percent increase formula to the Consumer Price Index (CPI) and comparing it to your portfolio’s growth, you can determine if your purchasing power is truly expanding or if you are simply treading water.

Business Performance: Tracking Revenue and Margin Expansion

For business owners and corporate finance executives, percent increase is the gold standard for reporting growth to stakeholders. It provides context to financial statements that raw numbers cannot offer.

Year-over-Year (YoY) Revenue Growth

Total revenue is a “vanity metric” unless it is compared to previous performance. Financial analysts prioritize Year-over-Year (YoY) growth to account for seasonality. If a retail business makes $500,000 in December and $300,000 in January, a simple month-over-month calculation would show a decrease. However, if they compare January of this year ($300,000) to January of last year ($250,000), the 20% increase reveals a thriving business that is successfully scaling.

Margin Expansion and Efficiency

Profitability is not just about how much you sell, but how much you keep. Percent increase is used to track “margin expansion.” If a company’s gross margin moves from 20% to 25%, that represents a significant increase in operational efficiency. Calculating the percent increase in expenses versus the percent increase in revenue is also vital. If revenue increases by 10% but operating costs increase by 15%, the business is becoming less efficient despite growing in size—a red flag for any business owner.

Customer Acquisition Cost (CAC) and Lifetime Value (LTV)

In modern business finance, particularly in SaaS (Software as a Service), tracking the percent increase in Customer Acquisition Cost is a survival skill. If the cost to acquire a customer increases by 50% over a year, the business must find a way to increase the Customer Lifetime Value by a corresponding or greater percentage to remain viable.

Personal Finance: Managing Inflation and Income Growth

On a microeconomic level, your household is a small business. Applying percent increase calculations to your personal budget can lead to better financial security and more effective career planning.

Assessing Salary Increases and Merit Raises

When negotiating a salary, most professionals focus on the total dollar amount. However, evaluating the percent increase is more strategic. If you receive a $5,000 raise on a $50,000 salary, that is a 10% increase. If you receive the same $5,000 raise on a $100,000 salary, it is only a 5% increase. Understanding these percentages helps you benchmark your career progression against industry standards and inflation. If the cost of living (inflation) has increased by 7% and your raise was only 5%, you have effectively received a pay cut in terms of purchasing power.

Tracking Expense Inflation in the Household Budget

By calculating the percent increase in fixed costs—such as rent, insurance premiums, or utility bills—you can identify “lifestyle creep” or predatory pricing. If your grocery bill has seen a 20% increase over six months without a change in your diet, it signals a need to audit your shopping habits or switch to more cost-effective suppliers. This quantitative approach removes the emotion from budgeting and replaces it with data-driven decision-making.

Net Worth Velocity

Net worth is the ultimate scorecard in personal finance. Calculating the percent increase in your net worth annually—known as “Net Worth Velocity”—can be a powerful motivator. In the early stages of wealth building, this percentage is often high because the base is small. As you move toward retirement, the percentage may stabilize, but the absolute dollar values become larger. Monitoring this rate ensures you are on track to meet your long-term financial goals.

Avoiding Common Pitfalls in Financial Data Analysis

While the formula for percent increase is straightforward, the interpretation of the results requires nuance. Misunderstanding these figures can lead to poor investment choices or flawed business strategies.

The Low Base Effect

One of the most deceptive aspects of percent increase is the “low base effect.” A penny stock that moves from $0.01 to $0.02 has experienced a 100% increase. While this sounds extraordinary, the actual value gained is minimal, and the volatility required to move that distance is often extreme. Investors should always look at the absolute values alongside the percentages to maintain a realistic perspective on risk and reward.

Percentage Increase vs. Percentage Points

There is a frequent confusion between a “percent increase” and an “increase in percentage points.” If an interest rate moves from 10% to 12%, it has increased by 2 percentage points. However, the percent increase of that interest rate is actually 20% (since 2 is 20% of 10). In the world of finance, failing to distinguish between these two can lead to massive errors in debt service calculations and investment projections.

The Asymmetry of Gains and Losses

Perhaps the most important lesson in financial percent increase is the asymmetry of recovery. If an investment drops by 50%, it does not require a 50% increase to get back to even; it requires a 100% increase. Understanding this mathematical reality highlights the importance of risk management and capital preservation. The higher the percentage loss, the exponentially higher the percentage gain required to recover the original principal.

Conclusion

Mastering the calculation of percent increase is more than a mathematical exercise; it is a prerequisite for financial literacy. In the worlds of investing, business management, and personal finance, this single metric provides the clarity needed to evaluate performance, benchmark growth, and make informed decisions. By consistently applying the percent increase formula to your revenue, expenses, and portfolios, you transform raw data into a strategic roadmap for long-term financial success. Whether you are aiming for a 10% raise or a 10% reduction in corporate overhead, the path to your goal begins with knowing exactly how to measure the climb.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.