Securing adequate funding is often the most significant hurdle for small business owners looking to launch, sustain, or scale their operations. While traditional commercial loans are an option, the Small Business Administration (SBA) loan program remains the “gold standard” of business financing. Because the SBA guarantees a portion of the loan—typically between 50% and 85%—lenders are more willing to offer favorable terms, lower interest rates, and longer repayment periods. However, the path to approval is rigorous and demands meticulous financial preparation. Understanding the mechanics of the SBA application process is essential for any entrepreneur seeking to leverage this powerful financial tool.

1. Selecting the Right SBA Loan Program for Your Needs

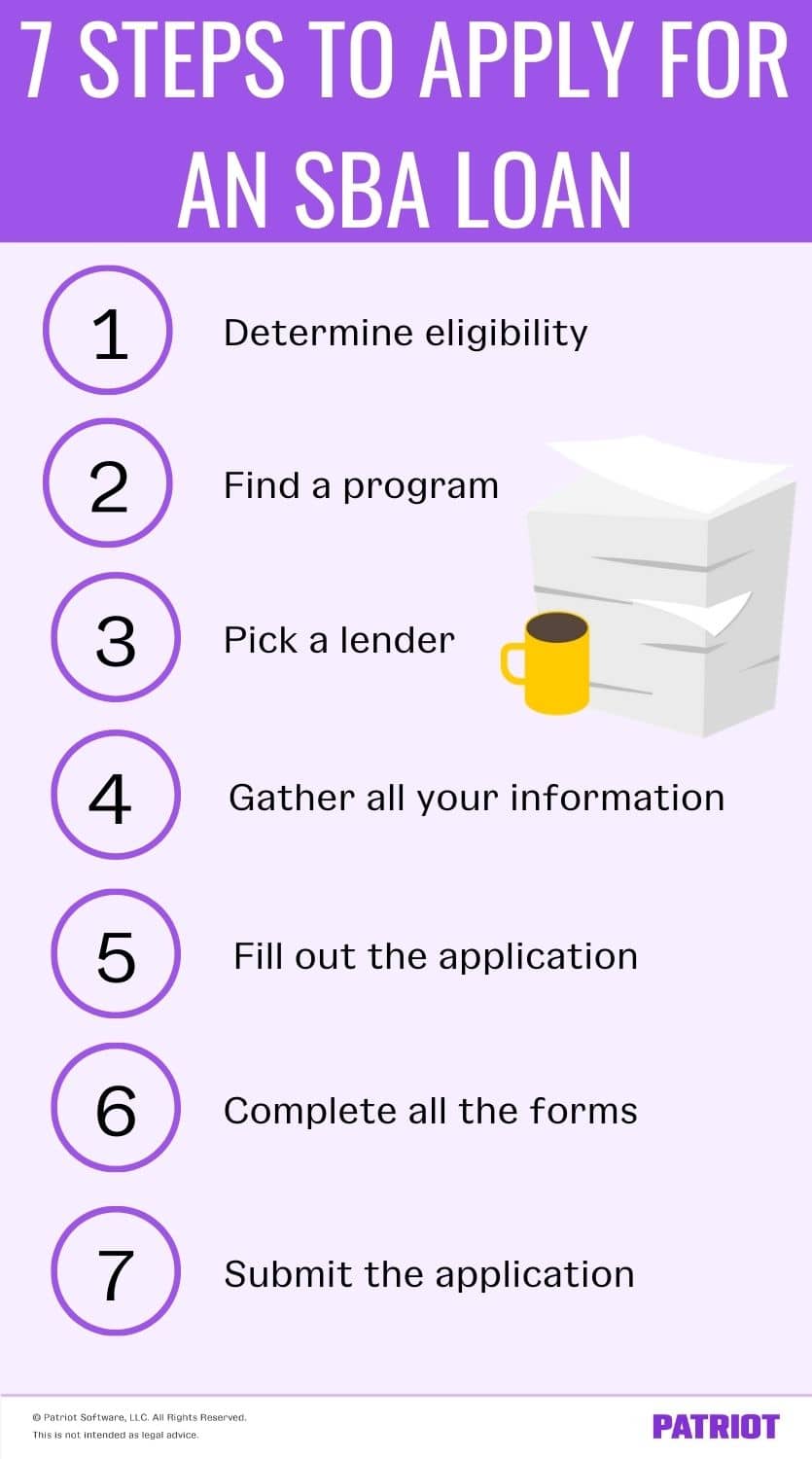

Before diving into paperwork, you must identify which SBA loan program aligns with your specific financial objectives. The SBA does not lend money directly to small business owners; instead, it sets guidelines for loans made by its partnering lenders (banks, credit unions, and community development organizations).

The 7(a) Loan Program: The Versatile Flagship

The 7(a) loan is the SBA’s most popular program due to its flexibility. It is designed for general business purposes, including working capital, debt refinancing, and the purchase of furniture, fixtures, and supplies. With loan amounts up to $5 million, the 7(a) is ideal for businesses that need a significant capital infusion but may not meet the strict collateral requirements of traditional bank loans.

The CDC/504 Loan Program: Real Estate and Equipment

If your goal is to purchase commercial real estate or heavy machinery, the CDC/504 program is the superior choice. This program involves a partnership between a traditional lender and a Certified Development Company (CDC). It offers long-term, fixed-rate financing that helps businesses grow by acquiring “brick and mortar” assets. The 504 loan typically requires a 10% equity contribution from the borrower, making it more accessible than many commercial real estate loans that require 20% to 30% down.

Microloans and SBA Express

For startups or smaller-scale projects, the SBA Microloan program provides loans up to $50,000. These are often administered through non-profit community-based organizations and include mandatory business coaching. For those who prioritize speed, the SBA Express loan offers an accelerated turnaround time for approval (usually within 36 hours), though it carries a lower maximum loan amount of $500,000 and slightly higher interest rates.

2. Preparing Your Financial Documentation and Eligibility

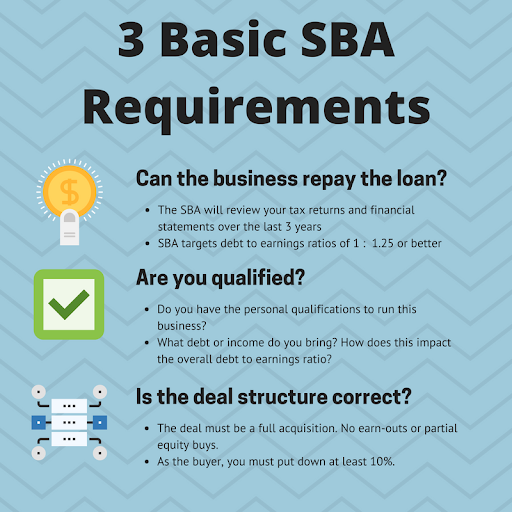

The most time-consuming phase of the SBA application process is the documentation stage. Because the federal government is guaranteeing the loan, the scrutiny regarding your financial health is intense. You must prove that your business is a “small” entity according to SBA size standards and that you have exhausted other financing options.

Personal and Business Credit Profiles

Your creditworthiness is the cornerstone of your application. Most SBA lenders look for a personal credit score of 680 or higher. Furthermore, the SBA uses the FICO SBSS (Small Business Scoring Service) score to pre-screen 7(a) loans. This score aggregates your personal credit, business credit, and financial data. Ensuring your reports are free of errors and that your debt-to-income ratio is manageable is a prerequisite for a successful application.

The Essential Document Checklist

Lenders will require a “loan package” that provides a 360-degree view of your financial history. At a minimum, you should have the following ready:

- Tax Returns: Personal and business federal income tax returns for the previous three years.

- Financial Statements: A current profit and loss (P&L) statement, a balance sheet, and a projected financial forecast for the next one to three years.

- Legal Documents: Articles of incorporation, business licenses, and copies of existing contracts or leases.

- Personal Financial Statement: Specifically, SBA Form 413, which details your personal assets and liabilities.

Crafting a Compelling Business Plan

A bank will not lend to a business that cannot articulate its path to profitability. Your business plan should include an executive summary, a description of your market niche, a competitive analysis, and a clear explanation of how the SBA funds will be utilized. In the “Money” niche, the “Use of Proceeds” section is critical; it must demonstrate that the capital will generate enough cash flow to service the debt while still allowing the business to grow.

3. Navigating the Application and Lender Matching Process

Once your documentation is organized, the next step is finding a lender that participates in SBA programs. Not all banks are created equal when it comes to SBA lending; some specialize in certain industries, while others have much higher volume and experience.

Finding an SBA-Approved Lender

The SBA offers a tool called “Lender Match,” which connects small businesses with participating SBA-approved lenders. However, for the smoothest experience, many financial experts recommend working with a “Preferred Lender” (PLP). Preferred lenders have been granted delegated authority by the SBA to make final credit decisions without sending the application to the SBA for a separate review. This can shave weeks off the approval timeline.

Completing the Official SBA Forms

While each bank has its own internal application, you will inevitably have to fill out standard SBA forms. The most common is SBA Form 1919, the Borrower Information Form. This document asks for details regarding the business’s ownership, its history with government debt, and any criminal history of the owners. Honesty is paramount here; any discrepancies discovered during the background check can lead to an automatic disqualification.

Collateral and Personal Guarantees

One of the most common misconceptions is that SBA loans do not require collateral. While the SBA prohibits a lender from denying a loan solely because of a lack of collateral, they will generally require a lien on all available business assets. Furthermore, if the loan is not fully secured by business assets, the lender may require a lien on personal real estate (such as your home). Additionally, any individual with a 20% or greater ownership stake in the business must provide a personal guarantee, making them personally liable for the debt if the business defaults.

4. The Underwriting, Approval, and Closing Phase

After you submit your full package, the application enters the underwriting phase. This is where the lender’s credit department stress-tests your financials to ensure you can survive economic downturns or fluctuations in revenue.

The Underwriting Timeline

The duration of the underwriting process depends on the complexity of your business and the specific loan program. A standard 7(a) loan might take 60 to 90 days from initial contact to funding, whereas an SBA Express loan is much faster. During this period, the underwriter may ask “clarifying questions” regarding your debt-service coverage ratio (DSCR). Generally, SBA lenders look for a DSCR of 1.15x or higher, meaning your business generates 15% more cash flow than is required to cover your total debt obligations.

The Commitment Letter and Closing

If the underwriter is satisfied, you will receive a commitment letter outlining the final terms of the loan, including the interest rate (usually the Prime Rate plus a spread) and the repayment term. Once you sign this, you move to closing. The closing process involves a final check of your documents, the recording of liens, and the payment of SBA guarantee fees. These fees are based on the loan amount and the maturity of the loan, though they are often rolled into the total loan amount to reduce out-of-pocket costs for the borrower.

5. Strategic Considerations for Long-Term Success

Applying for an SBA loan is more than just a transaction; it is a strategic financial move that requires long-term planning. To increase your chances of approval and ensure you can manage the debt effectively, consider these final insights.

Working with SBA Resource Partners

The SBA funds several resource partners, such as Small Business Development Centers (SBDCs) and SCORE (Service Corps of Retired Executives). These organizations provide free consulting and can help you review your financial statements and business plan before you ever step foot in a bank. Leveraging these experts can help you identify potential “red flags” in your application that might lead to a rejection.

Avoiding Common Application Pitfalls

The most common reasons for SBA loan denials in the financial sector include insufficient cash flow, a lack of management experience in the industry, and poor credit history. To avoid these, ensure your financial projections are grounded in reality—not just optimism. If your business has seasonal fluctuations, explain how you will manage debt payments during “lean” months.

The Impact of Debt on Business Valuation

From a purely financial perspective, an SBA loan is a form of leverage. While it provides the capital needed for growth, it also sits as a liability on your balance sheet. For business owners considering an eventual exit or sale, it is important to remember that most SBA loans must be paid off or assumed by the buyer upon the sale of the business. Managing your debt-to-equity ratio throughout the life of the loan is essential for maintaining the overall valuation of your enterprise.

By treating the SBA application as a rigorous audit of your business’s financial viability, you can approach the process with confidence. While the requirements are demanding, the reward—access to low-cost, long-term capital—is often the catalyst that transforms a struggling startup into a market-leading corporation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.