Navigating federal tax obligations for employers can be a complex endeavor, and Form 941, the Employer’s Quarterly Federal Tax Return, stands as a cornerstone of these responsibilities. While the ideal scenario involves submitting this form with full payment by the due date, circumstances sometimes dictate that an employer must file the return without an accompanying remittance. Understanding the correct procedure for mailing Form 941 when no payment is included is critical for compliance, avoiding unnecessary penalties, and maintaining a healthy relationship with the Internal Revenue Service (IRS). This guide will meticulously detail the process, implications, and best practices for employers in this specific situation.

Understanding Form 941: Your Employer’s Quarterly Federal Tax Return

Form 941 is more than just a piece of paper; it’s a vital mechanism through which employers report income taxes, Social Security tax, and Medicare tax withheld from employees’ paychecks, as well as the employer’s share of Social Security and Medicare tax. This quarterly filing is a fundamental aspect of payroll tax compliance for most businesses in the United States.

Who Needs to File Form 941?

Generally, if you pay wages subject to income tax withholding, Social Security, or Medicare taxes, you must file Form 941 quarterly. This applies to a vast majority of employers, regardless of business size. There are a few exceptions, such as seasonal employers who don’t pay wages year-round (who may indicate on their first 941 filing they will not file for subsequent quarters) or household employers and agricultural employers, who typically use different forms (Form 943 or Schedule H, Form 1040). Understanding your filing obligation is the first step toward effective tax management.

What Form 941 Reports

The form requires employers to detail various financial aspects of their payroll for the quarter. This includes the total wages, tips, and other compensation paid; federal income tax withheld; taxable Social Security and Medicare wages; and the calculated employer and employee share of Social Security and Medicare taxes. It also accounts for any adjustments to taxes and details previous deposits made. The accuracy of these figures is paramount, as discrepancies can lead to significant issues.

The Importance of Timely Filing

Even without payment, timely filing of Form 941 is non-negotiable. The IRS imposes penalties for both failure to file on time and failure to pay on time. Filing on time demonstrates your commitment to compliance, even if payment is delayed. The due dates for Form 941 are generally April 30, July 31, October 31, and January 31 for the respective quarters. If a due date falls on a weekend or holiday, the deadline shifts to the next business day. Missing these deadlines can trigger late-filing penalties, which accrue on the unpaid tax from the due date of the return until the date of payment.

The IRS’s Stance on Filing Without Payment

While the IRS prefers that you file Form 941 with full and timely payment, they understand that financial difficulties can arise. The agency explicitly instructs employers on how to proceed when payment cannot be made with the return. Filing without payment is always preferable to not filing at all.

Why You Might File Without Payment

There are several legitimate reasons an employer might find themselves in a position to file Form 941 without accompanying payment. These can range from temporary cash flow issues, unexpected business downturns, or even an administrative oversight that causes a delay in payment processing, even if funds are available. Regardless of the reason, the core principle remains: file the form accurately and on time, then address the payment issue separately.

Consequences of Not Paying on Time

Failure to pay on time will result in penalties and interest. The failure-to-pay penalty is typically 0.5% of the unpaid taxes for each month or part of a month that the taxes remain unpaid, capped at 25% of your unpaid taxes. Interest also accrues on underpayments, which can be compounded daily. Additionally, if the amounts were deposited late, or not at all, you might face significant failure-to-deposit penalties, which can be even higher depending on the length of the delay. The IRS treats withheld taxes as a trust fund, meaning that these funds are held in trust for the government. Misusing or failing to remit these funds can lead to severe consequences, including personal liability for responsible individuals within the business.

IRS Payment Options and Alternatives

If you cannot pay the full amount due, the IRS offers several options. You can make partial payments to reduce penalties and interest. More formally, you may be able to request an installment agreement, allowing you to make monthly payments over a set period. Another option, though less common for payroll taxes, is an Offer in Compromise (OIC), which allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe, under specific circumstances of financial hardship. Exploring these options proactively can prevent further escalation of penalties and potential enforcement actions.

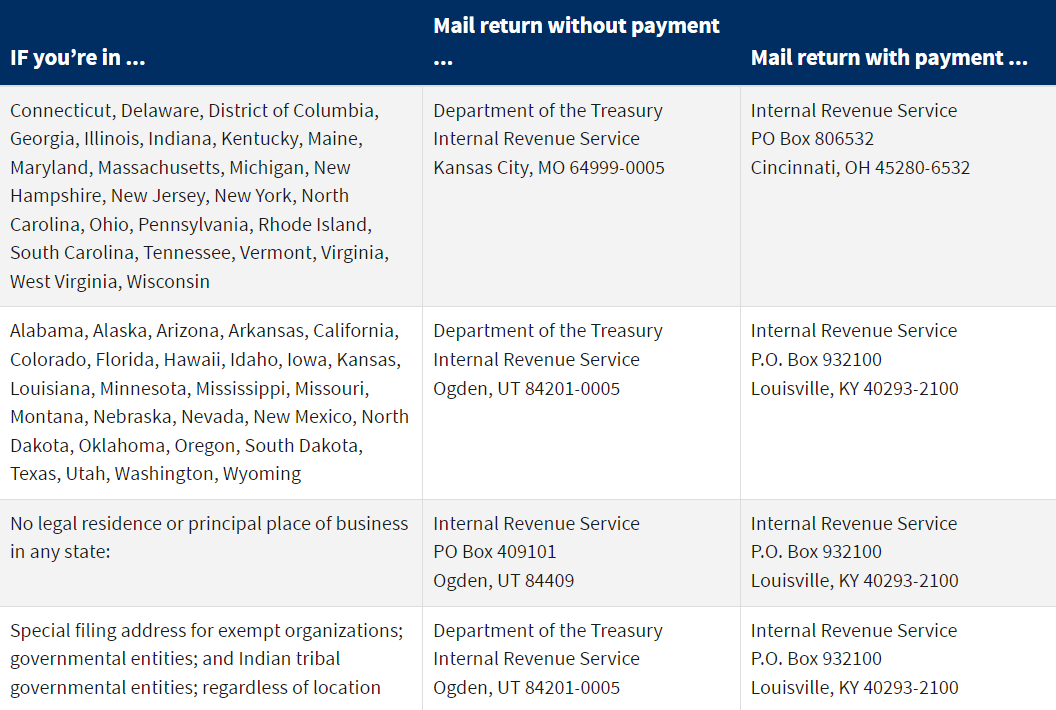

Identifying the Correct Mailing Address for Form 941 (No Payment)

This is the core question and arguably the most crucial detail for employers facing this situation. The IRS maintains different mailing addresses for forms submitted with payment versus those submitted without payment. Sending your Form 941 to the wrong address can cause significant delays in processing, potentially leading to additional penalties or complications.

IRS Mailing Addresses: A State-by-State Guide (General Concept)

The IRS utilizes various processing centers across the country. The specific mailing address for Form 941 depends on two primary factors: the state where your business is located and whether you are enclosing a payment. It is critical to consult the official IRS instructions for Form 941 for the relevant tax year, as addresses can occasionally change. These instructions are typically found within Publication 15 (Circular E), Employer’s Tax Guide, or directly on the IRS website.

Distinguishing Between “With Payment” and “Without Payment” Addresses

The IRS’s rationale for separate addresses is rooted in their processing workflow. Returns with payments often go to a different lockbox or processing center designed to handle financial transactions securely and efficiently. Returns without payment, conversely, are directed to centers that focus solely on document processing and record-keeping. Using the “without payment” address ensures your form is correctly routed to the appropriate department for recording your timely filing, even as the payment issue remains outstanding.

For example, an employer in New York mailing Form 941 with payment might send it to one address (e.g., Department of the Treasury, Internal Revenue Service, P.O. Box 80101, Cincinnati, OH 45280-0001), while the same employer mailing Form 941 without payment would send it to another (e.g., Department of the Treasury, Internal Revenue Service, Cincinnati, OH 45999-0005). These are illustrative examples, and actual addresses must be confirmed with the official IRS instructions for the relevant tax year. Failing to differentiate can result in your form being delayed or misplaced, potentially triggering failure-to-file penalties despite your best efforts.

Using IRS.gov for the Most Current Information

The most reliable and up-to-date source for IRS mailing addresses is the official IRS website, IRS.gov. Navigate to the “Instructions for Form 941” for the specific year you are filing. Within these instructions, you will find a dedicated section titled “Where to File,” which clearly lists the appropriate mailing addresses based on your business’s location and whether you are including a payment. Always cross-reference with the current year’s instructions to avoid outdated information. You can also search for “Where to File Form 941” directly on the IRS website.

Best Practices for Employers Filing Form 941

Beyond knowing where to mail your form, adopting a robust set of best practices can significantly streamline your payroll tax compliance and mitigate risks.

Maintaining Accurate Payroll Records

The foundation of accurate Form 941 filing is meticulous record-keeping. Employers must maintain detailed records of all wages paid, tips reported, federal income tax withheld, and Social Security and Medicare taxes calculated for each employee. These records are essential for accurately completing Form 941 and for audit purposes. Utilize reliable payroll software or work with a professional payroll service provider to ensure accuracy and compliance.

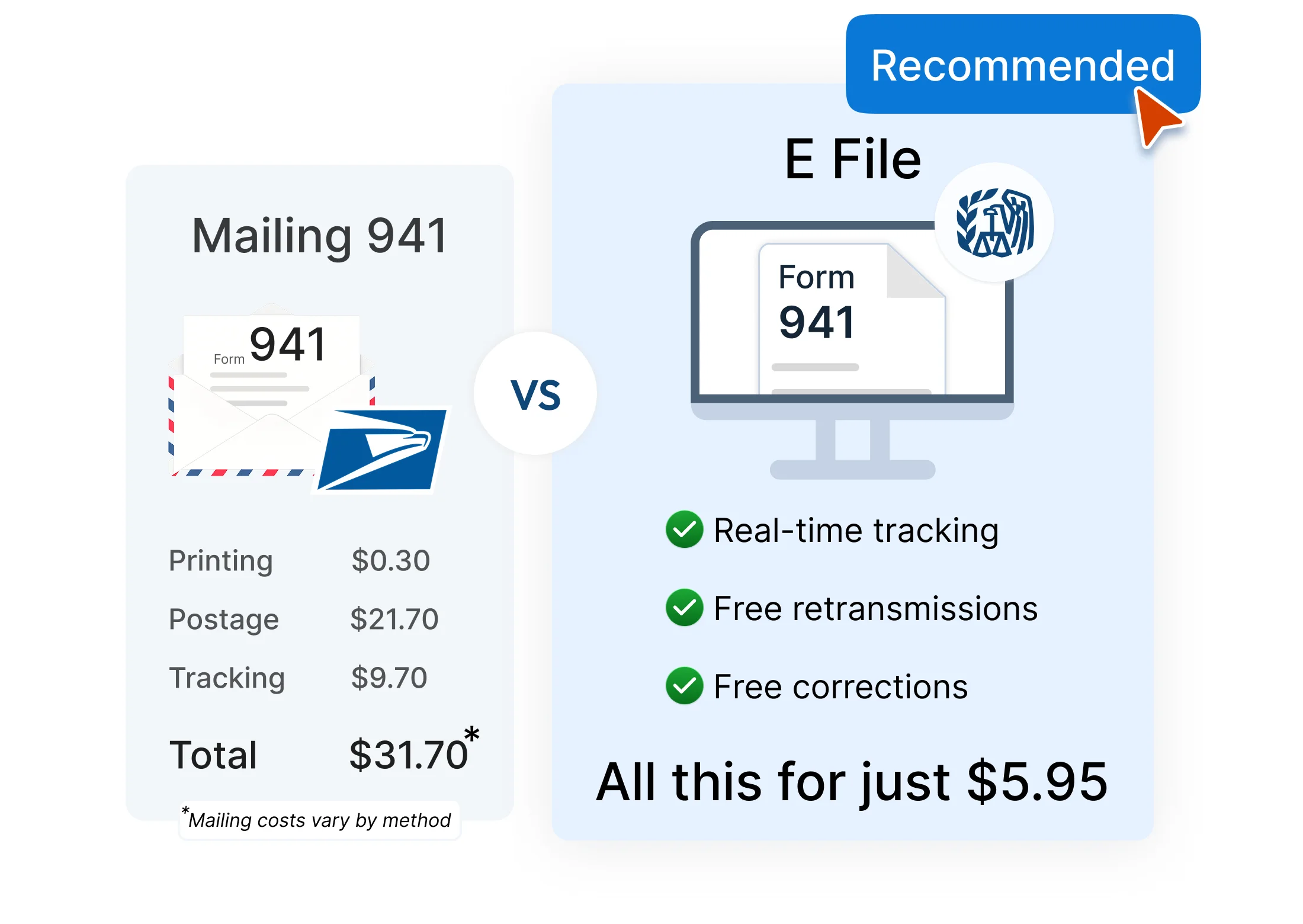

Utilizing Electronic Filing (E-file)

For most employers, electronic filing (e-file) of Form 941 is not just an option but often a requirement or highly recommended best practice. E-filing offers numerous advantages: it reduces errors, provides immediate confirmation of receipt, and generally expedites processing. Many payroll software providers and tax professionals offer e-filing services. If you e-file, you do not need to mail a paper copy of the form. When e-filing without payment, the system will simply register the filing, and you would then address the payment separately through EFTPS (Electronic Federal Tax Payment System) or other approved methods.

Proactive Communication with the IRS

If you anticipate significant challenges in meeting your tax obligations, proactive communication with the IRS is always advisable. While they may not always grant exceptions, demonstrating a good-faith effort to comply and address issues transparently can be beneficial. Responding promptly to any IRS notices or inquiries is also crucial. Ignoring correspondence can escalate issues unnecessarily.

Navigating Payment Challenges and Penalties

Even with the correct mailing address, the underlying issue of unpaid taxes remains. Understanding the landscape of penalties and available relief options is key to managing this challenge effectively.

Understanding IRS Penalties for Late Payment and Failure to Deposit

As mentioned, two primary penalties arise when taxes are not paid on time: the failure-to-pay penalty and the failure-to-deposit penalty. The failure-to-deposit penalty can be particularly severe, ranging from 2% to 15% of the underpayment, depending on how late the deposit is. For example, deposits not made by the due date but paid within 5 days are subject to a 2% penalty. If paid more than 15 days late, it can jump to 10%. If not paid within 10 days after the date of the first notice from the IRS demanding payment, the penalty becomes 15%. This often applies even if the Form 941 itself was filed on time but the payroll tax deposits were not made according to the employer’s deposit schedule (monthly or semi-weekly). Employers must understand their specific deposit schedule and adhere to it strictly.

Requesting a Payment Plan (Installment Agreement)

If you cannot pay your full tax liability immediately, consider requesting an installment agreement. This allows you to make monthly payments for up to 72 months. While interest and late-payment penalties still apply, they may be reduced. To request an installment agreement for employer taxes, you might need to contact the IRS directly or apply for a short-term payment plan (up to 180 days) or a long-term installment agreement if you have other tax balances. It’s important to note that you must be current with all other filing and payment requirements to qualify for and maintain an installment agreement.

Seeking Professional Guidance

When faced with complex tax situations, especially those involving payment difficulties, consulting with a qualified tax professional (e.g., a CPA, enrolled agent, or tax attorney) is highly recommended. They can provide personalized advice, help you understand your options, negotiate with the IRS on your behalf, and ensure you remain compliant while addressing financial challenges. Their expertise can be invaluable in navigating the intricacies of IRS regulations and minimizing potential liabilities.

In conclusion, mailing Form 941 without payment requires careful attention to detail, specifically regarding the correct IRS mailing address. While challenging, addressing this situation correctly is crucial for avoiding further penalties and maintaining your business’s good standing with the IRS. Always prioritize timely filing, even if payment is delayed, and proactively explore all available payment options and professional guidance.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.