Tax season, for many, is synonymous with a specific kind of anxiety — the gnawing uncertainty of what you might owe, or worse, what you do owe but haven’t yet discovered. Whether you’re a seasoned taxpayer, a new entrepreneur, or someone who’s just received an unexpected notice from the Internal Revenue Service (IRS), knowing your exact tax liability is the critical first step towards financial peace of mind and responsible tax management. Ignoring a potential tax debt won’t make it disappear; in fact, it often leads to penalties and interest that can significantly inflate the original amount.

This article serves as your comprehensive guide to navigating the IRS system and accurately determining your tax obligations. We’ll explore the primary methods available to you, break down how to interpret IRS communications, and outline the proactive steps you can take to manage and mitigate any outstanding tax debt. Understanding how to see how much you owe the IRS is not just about avoiding trouble; it’s about empowering yourself with the financial clarity needed to make informed decisions and maintain a healthy financial standing.

Understanding Your Tax Obligation Landscape

Before diving into the “how-to,” it’s essential to grasp why knowing your IRS debt is so crucial and the common scenarios that can lead to such obligations in the first place. A clear understanding of the landscape empowers you to approach the process strategically.

Why Knowing Your IRS Debt Matters

The importance of accurately assessing your IRS debt cannot be overstated. Firstly, it allows for proper financial planning and budgeting. When you know the exact amount due, you can allocate funds, adjust your spending, or explore payment options without the stress of an unknown future bill. Secondly, timely payment or establishment of a payment plan helps you avoid costly penalties and interest. The IRS is meticulous about applying these charges, which can quickly compound an already challenging situation. Penalties can range from failure-to-pay and failure-to-file to accuracy-related penalties. Thirdly, and perhaps most importantly, knowing your debt provides immense psychological relief. The burden of an unknown financial obligation can be a significant source of stress; resolving that uncertainty is the first step towards resolving the debt itself. Finally, staying current with your tax obligations protects your financial future, impacting everything from your ability to secure loans to avoiding more severe enforcement actions by the IRS.

Common Scenarios Leading to IRS Debt

IRS debt can arise from various situations, some of which are more common than others. One primary cause is underpayment of estimated taxes. This typically affects self-employed individuals, independent contractors, or those with significant income not subject to standard withholding. If you don’t pay enough taxes throughout the year via quarterly estimated payments, you’ll owe a lump sum at tax time, potentially with penalties.

Another frequent scenario is insufficient wage withholding. Many employees rely on their W-4 forms to dictate how much tax is withheld from each paycheck. If this form isn’t updated after life changes (marriage, new child, second job) or filled out incorrectly, too little tax might be withheld, leading to an unexpected bill.

Missed deadlines or unfiled returns are also major culprits. Failing to file your tax return by the due date (even if you can’t pay) or neglecting to pay by the due date will immediately trigger penalties and interest. Furthermore, audit adjustments can lead to debt if the IRS reviews your return and determines you understated your income or overstated deductions, resulting in additional tax due. Lastly, if you have prior year balances that were never fully resolved, they can accumulate and contribute to your current IRS debt.

Primary Methods to Check Your IRS Balance

The IRS has made significant strides in providing accessible tools for taxpayers to manage their accounts and ascertain their financial standing. Understanding these primary methods is key to accurately determining your current tax obligation.

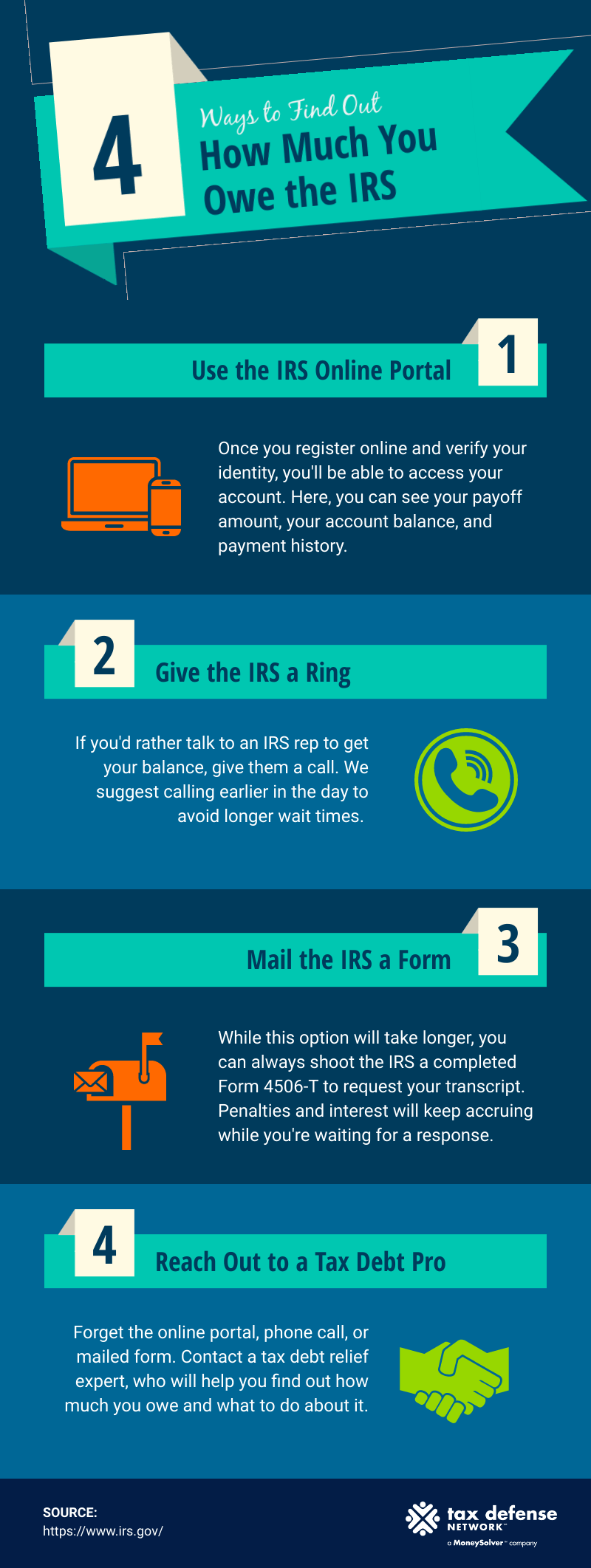

Using the IRS Online Account

The most efficient and increasingly popular method for individuals to check their tax balance is through their IRS Online Account. This digital portal offers a personalized, secure gateway to your federal tax information. To access it, you’ll typically need to create an account and verify your identity, a process that might involve providing personal details and answering financial questions. Once logged in, your online account provides a wealth of information:

- Balance Due: The most direct answer to “how much do I owe?” This section will clearly display your current outstanding balance, including tax, penalties, and interest for all applicable tax years.

- Payment History: You can review all payments made to the IRS, helping you reconcile your records.

- Payment Plans: If you have an existing payment plan, you can view the details, make changes, or request a new one.

- Tax Records: Access to key tax records like tax transcripts, which we’ll discuss next.

- Notices: You can often view digital copies of certain notices from the IRS.

The benefits of using the online account are numerous: it’s available 24/7, provides real-time updates, and allows for direct interaction with your tax information from the comfort of your home. It’s an indispensable tool for proactive tax management.

Reviewing Your Tax Transcripts

For a more detailed breakdown of your tax situation, especially if you need to understand how a balance was derived or if you’re trying to reconstruct past tax filings, tax transcripts are invaluable. A tax transcript is a summary of your tax return information or account activity. You can request various types of transcripts, most commonly:

- Account Transcript: This shows most line items from your filed tax return, along with any changes or adjustments made by you or the IRS, as well as payment history and balances due. It’s particularly useful for seeing an overview of your tax account for a specific year, including any outstanding debt.

- Record of Account Transcript: This combines the information from the tax return transcript and the account transcript, providing a comprehensive view of your tax return and any adjustments.

- Wage and Income Transcript: This lists data from information returns received by the IRS, such as W-2s, 1099s, and 1098s, which is helpful for verifying income reported for a given year.

You can request transcripts online through your IRS Online Account, by mail using Form 4506-T (Request for Transcript of Tax Return), or by calling the IRS. While they don’t explicitly state “you owe $X,” the account transcript will show assessments, payments, and resulting balances, allowing you to calculate or confirm your debt.

Contacting the IRS Directly

While digital tools are efficient, sometimes a direct conversation is necessary. You can contact the IRS by phone to inquire about your balance. Be prepared for potentially long wait times, especially during peak tax season. When you call, ensure you have the following information readily available to verify your identity: your Social Security number, date of birth, address, and your prior year’s tax return. The representative will be able to access your account and provide you with your current balance due.

It’s advisable to have a pen and paper ready to jot down the information provided, including the exact amount, the tax period it pertains to, and any reference numbers. While less convenient than the online methods, direct contact can be beneficial if you have complex questions or issues that aren’t easily resolved through self-service options.

Deciphering IRS Notices and Bills

Receiving a letter from the IRS can be unsettling, but it’s crucial to open and read it carefully. These notices are official communications that often contain vital information about your tax account, including any outstanding balances.

Understanding Different Notice Types

The IRS issues a wide array of notices, each with a specific purpose. When it comes to outstanding debt, you’re most likely to encounter:

- CP Notices: These generally inform you about changes to your tax return, proposed adjustments, or a balance due. For example, a CP14 notice is one of the most common, informing you that you owe taxes and specifying the amount, interest, and payment due date. A CP501, CP503, or CP504 may indicate a balance due and subsequent steps like intent to levy if unpaid.

- Letter Notices: These are typically more complex and may involve audits, appeals, or collection actions. For instance, a Letter 1153 may be a Final Notice of Intent to Levy and Notice of Your Right to a Hearing, signaling serious collection efforts if the debt isn’t addressed.

It’s important not to dismiss any IRS correspondence. Even if you believe it’s an error, it requires your attention and response.

Key Information to Locate on a Notice

When you receive an IRS notice or bill, don’t panic. Systematically review the document for these key pieces of information:

- Notice Number: Usually found in the top right corner (e.g., CP14, LTR 1153). This helps you identify the type of communication and its purpose.

- Tax Year: The specific tax year the notice pertains to. You might have separate notices for different years.

- Amount Due: The total amount you owe, including original tax, penalties, and interest.

- Due Date: The deadline by which you must pay the amount or respond to avoid further penalties or collection actions.

- Reason for the Notice: A brief explanation of why the IRS is contacting you and how the balance was determined.

- Payment Options: Information on how to pay the amount due.

- Contact Information: A phone number and/or address to write to if you have questions or wish to dispute the notice.

Understanding these elements will allow you to quickly grasp the implications of the notice and formulate an appropriate response.

What to Do if You Disagree with a Notice

If you believe the IRS notice is incorrect or that you don’t owe the amount stated, do not ignore it. You have the right to dispute the assessment.

- Gather Supporting Documentation: Collect any records, receipts, or explanations that support your claim. This might include amended returns, proof of payments, or documentation for deductions.

- Contact the IRS: Use the contact information provided on the notice. Be prepared to clearly explain why you disagree and provide your supporting evidence.

- Request an Appeal or Reconsideration: Depending on the type of notice and the stage of the dispute, you might be able to request an appeal within the IRS Office of Appeals or ask for an audit reconsideration. This often requires submitting a formal request and evidence.

- Seek Professional Help: If the dispute is complex or involves a significant amount, it is highly advisable to consult with a tax professional (such as a CPA, Enrolled Agent, or tax attorney) who can help you navigate the process.

Strategies for Managing and Resolving Your IRS Debt

Discovering you owe the IRS can be daunting, but it’s a manageable situation with the right approach. The key is to act promptly and explore the various options available for payment and resolution.

Immediate Payment Options

If you have the financial capacity, paying your IRS debt in full and on time is always the best course of action to avoid additional penalties and interest. The IRS offers several convenient payment methods:

- IRS Direct Pay: This free service allows you to make direct payments from your checking or savings account. You can schedule payments up to 365 days in advance.

- Debit Card, Credit Card, or Digital Wallet: You can pay through third-party payment processors. While convenient, these processors typically charge a small fee.

- Electronic Federal Tax Payment System (EFTPS): This is a free service provided by the U.S. Department of the Treasury. It’s ideal for making all federal tax payments, including estimated taxes, and offers robust record-keeping features.

- Electronic Funds Withdrawal (EFW): If you e-file your tax return, you can authorize an electronic funds withdrawal from your bank account to pay any balance due directly from your tax preparation software or tax professional.

- Check or Money Order: You can mail a check or money order to the IRS, but ensure it’s made out to the “U.S. Treasury” and includes your name, address, daytime phone number, Social Security number, the tax year, and the related tax form number.

Choose the method that best suits your financial situation and offers the most convenience.

If You Can’t Pay in Full: Payment Plans

Many taxpayers find themselves unable to pay their full tax liability immediately. The IRS understands this and offers several alternatives to help you manage your debt:

- Short-Term Payment Plan: If you can pay your full balance within 180 days, you might be granted a short-term extension. Interest and penalties will still accrue, but it offers flexibility without setting up a formal installment agreement.

- Installment Agreement (IA): This allows you to make monthly payments for up to 72 months. The IRS will usually grant an IA if you owe $50,000 or less in combined tax, penalties, and interest, and have filed all required returns. While in an IA, penalties and interest continue to accrue, but at a reduced rate for certain penalties. You can apply for an IA online through your IRS Online Account.

- Offer in Compromise (OIC): An OIC allows certain taxpayers to resolve their tax liability with the IRS for a lower amount than what they originally owe. The IRS considers an OIC if there’s doubt as to collectability (you cannot pay the full amount), doubt as to liability (there’s a genuine dispute about whether you owe the tax), or effective tax administration (collecting the full amount would cause economic hardship). An OIC is a complex process and is not available to everyone.

- Currently Not Collectible (CNC) Status: If the IRS determines that you cannot pay any of your tax debt due to financial hardship, it may place your account in CNC status. This means the IRS temporarily stops collection efforts, though interest and penalties continue to accrue, and the IRS can periodically review your financial situation.

Each of these options has specific eligibility requirements and implications, so it’s important to understand them fully before committing.

Seeking Professional Assistance

Navigating IRS debt and payment options can be complex, especially if your situation is unique or involves significant amounts. This is where professional assistance becomes invaluable:

- Tax Professionals: Certified Public Accountants (CPAs), Enrolled Agents (EAs), and tax attorneys specialize in tax law and can represent you before the IRS. They can help you understand your options, prepare necessary forms (like OIC applications), communicate with the IRS on your behalf, and negotiate favorable payment terms.

- IRS Taxpayer Advocate Service (TAS): TAS is an independent organization within the IRS that helps taxpayers who are experiencing significant hardship or believe the IRS is not treating them fairly. If you’ve tried to resolve your issue through normal channels and haven’t succeeded, TAS might be able to assist.

- Low Income Taxpayer Clinics (LITCs): LITCs provide free or low-cost assistance to individuals who meet certain income requirements and are involved in disputes with the IRS or need help understanding their taxpayer rights and responsibilities.

Don’t hesitate to seek expert advice if you feel overwhelmed or unsure about how to proceed. A professional can save you time, stress, and potentially a significant amount of money.

Proactive Steps to Avoid Future IRS Debt

While knowing how to manage existing debt is crucial, the ultimate goal is to avoid accumulating it in the first place. Proactive tax planning and diligent record-keeping can significantly reduce your chances of owing the IRS a substantial sum.

Accurate Withholding and Estimated Payments

The most direct way to prevent future tax debt is to ensure you’re paying enough throughout the year.

- Adjust Your W-4: If you’re an employee, regularly review and update your Form W-4, Employee’s Withholding Certificate, especially after major life events (marriage, birth of a child, new job, or spouse’s job change). The IRS Tax Withholding Estimator tool can help you calculate the correct amount to withhold.

- Make Estimated Payments: If you’re self-employed, an independent contractor, or have significant income not subject to withholding (like rental income or investments), you generally need to make quarterly estimated tax payments. Use Form 1040-ES, Estimated Tax for Individuals, to calculate and submit these payments. Don’t underestimate; paying a little more than you expect to owe can prevent underpayment penalties.

Maintaining Meticulous Records

Good record-keeping is the backbone of accurate tax filing and can be your best defense in case of an IRS inquiry.

- Income Documentation: Keep all W-2s, 1099s (from banks, brokers, clients), and other income statements.

- Expense Records: For deductions, keep receipts, invoices, and bank statements. Categorize your expenses clearly, especially for business or self-employment income.

- Mileage Logs: If you claim vehicle expenses, maintain detailed logs.

- Home Office Documentation: If you claim a home office, keep records of related expenses.

- Retain Records: Generally, keep tax records for at least three years from the date you filed your original return or two years from the date you paid the tax, whichever is later. For certain items, longer retention periods may apply.

Digital record-keeping through scanning and cloud storage can make this process more efficient and secure.

Regular Financial Reviews and Tax Planning

Your financial situation is dynamic, and so are tax laws. Regular check-ups are essential.

- Annual Tax Review: Even if you use a tax preparer, take time each year to review your financial situation in light of tax implications. Consider any new income streams, significant purchases, or life changes.

- Stay Informed: Tax laws can change, sometimes with little notice. Subscribing to tax news updates or consulting with a tax professional can help you stay abreast of relevant developments.

- Proactive Planning: Instead of reacting to a tax bill, plan proactively. This might involve strategies like contributing to retirement accounts, utilizing tax-advantaged investments, or making charitable contributions to optimize your tax liability.

Conclusion

Understanding “how to see how much I owe the IRS” is a fundamental aspect of sound personal finance. From leveraging the convenience of the IRS Online Account and delving into tax transcripts to deciphering official notices and exploring various payment solutions, the tools and options are available to you. While discovering a tax debt can be stressful, ignoring it is never the answer.

By taking proactive steps — accurately managing your withholding, meticulously maintaining records, and engaging in regular tax planning — you can significantly reduce the likelihood of future IRS debt. Should you find yourself with an outstanding balance, remember that the IRS offers various avenues for resolution, and professional guidance is readily available for complex situations. Empowering yourself with knowledge and taking decisive action will not only address your immediate tax obligations but also lay a stronger foundation for your long-term financial health and peace of mind.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.