Student loans are a significant financial commitment for millions, representing an investment in one’s future. However, navigating the complexities of repayment can be challenging, and missing payments can lead to a precarious situation: loan default. Defaulting on a student loan is a serious financial event with far-reaching consequences that can impact your credit, your assets, and your future financial opportunities. The good news is that understanding what default is, how to identify it, and what steps you can take to prevent or resolve it is crucial for protecting your financial well-being. This comprehensive guide will illuminate the signs of default, explain its ramifications, and empower you with the knowledge to either avoid this pitfall or climb out of it if you’ve already stumbled.

Understanding Student Loan Default: What It Means and Why It Matters

Before you can know if your loan is in default, it’s essential to grasp the precise definition and the critical distinction between delinquency and default. This foundational understanding is key to taking appropriate action.

Defining Default: Federal vs. Private Loans

The definition of default varies slightly depending on whether your loan is federal or private, though the core concept remains the same: a failure to repay as agreed.

- Federal Student Loans: For most federal student loans (like Stafford, Perkins, PLUS loans), default typically occurs after 270 days (approximately nine months) of non-payment. This period of non-payment can apply to scheduled payments or to failing to meet other terms of your loan agreement. Some federal loans, like Perkins Loans, may default sooner if specific conditions are violated. The federal government, or the guarantor of your loan, has a highly standardized process for determining when a loan officially enters default.

- Private Student Loans: Private student loans, issued by banks, credit unions, or other financial institutions, have their own specific terms and conditions outlined in your promissory note. Default on a private loan can happen much faster than with federal loans, sometimes after just one missed payment, or after a shorter period like 90 or 120 days of non-payment. The exact terms for default will be stipulated in your loan agreement. It is critical to review your private loan documents to understand these timelines.

The Critical Distinction: Delinquency vs. Default

It’s important not to confuse delinquency with default, though one inevitably leads to the other if left unaddressed.

- Delinquency: A loan becomes delinquent the very first day after a payment is missed. Your account is considered delinquent for as long as payments are overdue. During this period, you may receive reminders and notices from your loan servicer, and your delinquency will be reported to credit bureaus, negatively impacting your credit score.

- Default: Default is the more severe stage, occurring after an extended period of delinquency as defined by your loan terms. When a loan defaults, the entire unpaid balance of the loan, including accrued interest, often becomes immediately due and payable. This is known as “acceleration” of the debt. At this point, the loan leaves the hands of your original servicer and is typically transferred to a collection agency or directly to the government for federal loans.

Why Default is a Critical Financial Event

Defaulting on a student loan is not merely a bureaucratic hurdle; it is a critical financial event that triggers a cascade of serious repercussions. It signifies a profound breakdown in your ability or willingness to meet your financial obligations, which has lasting impacts on your creditworthiness, your financial freedom, and even your eligibility for certain benefits. Understanding this gravity underscores the importance of timely intervention.

Recognizing the Red Flags: Key Indicators Your Loan is in Default

Identifying whether your student loan is in default isn’t always immediately obvious, but there are clear signals and proactive steps you can take to confirm your status. Ignoring these signs will only exacerbate the problem.

Communication Breakdown: Ignoring Lender Outreach

One of the most significant indicators that your loan is heading towards or already in default is a persistent barrage of communication from your loan servicer or a collection agency.

- Frequent Calls and Emails: As you approach default, your servicer will increase their efforts to contact you, often through multiple phone calls, emails, and letters. These communications will escalate in urgency, moving from friendly reminders to warnings about the consequences of non-payment.

- Official Default Notices: If your loan officially defaults, you will receive formal written notices, often via certified mail, informing you of your default status and outlining the next steps, including the potential for collection actions.

- Collection Agency Involvement: For defaulted federal loans, the debt is often transferred to a collection agency. For private loans, lenders may also sell the debt to third-party collectors. If you start receiving communications from a collection agency rather than your original servicer, it’s a very strong sign that your loan is in default.

Checking Your Credit Report: A Vital Tool

Your credit report is an invaluable tool for monitoring the status of all your debts, including student loans. Lenders and servicers are required to report payment activity (or lack thereof) to the major credit bureaus.

- Negative Marks: Default will be reported as a severe negative item on your credit report. Look for terms like “default,” “charged-off,” “collections,” or “account transferred” under your student loan entries.

- Credit Score Drop: A default will cause a significant drop in your credit score, making it harder to secure other forms of credit (like mortgages, car loans, or even credit cards) in the future, often at less favorable terms.

- Annual Free Report: You are entitled to one free credit report annually from each of the three major credit bureaus (Experian, Equifax, and TransUnion) via AnnualCreditReport.com. Regularly checking these reports allows you to catch issues early.

Contacting Your Loan Servicer Directly

The most straightforward way to confirm your loan status is to contact your loan servicer directly. If you have federal loans, you can also use the National Student Loan Data System (NSLDS), which is the U.S. Department of Education’s central database for federal student aid, to identify your servicers and loan details. For private loans, you’ll need to contact the specific lender.

- Be Prepared with Information: Have your account number, Social Security number, and other identifying information ready when you call.

- Ask for Your Current Status: Specifically ask if your loan is in default, how many payments you’ve missed, and what options are available to you.

- Document Everything: Keep a record of who you spoke with, the date and time of the call, and what was discussed.

The Steep Cost of Default: Consequences You Can’t Ignore

Defaulting on a student loan isn’t just about a bad mark on your credit; it triggers a range of severe and often debilitating financial consequences that can follow you for years, making it difficult to achieve other financial goals.

Damaged Credit Score and Financial Future

This is often the first and most immediate consequence people think of. A default will severely damage your credit score, potentially by hundreds of points, and remain on your credit report for up to seven years. This damage can:

- Hinder Future Borrowing: Make it nearly impossible to qualify for new loans (mortgage, car, personal) or credit cards, or result in significantly higher interest rates if you do.

- Impact Employment and Housing: Some employers review credit reports as part of their hiring process, and landlords may check credit when evaluating rental applications.

- Increase Insurance Premiums: In some states, a poor credit history can even lead to higher car or home insurance premiums.

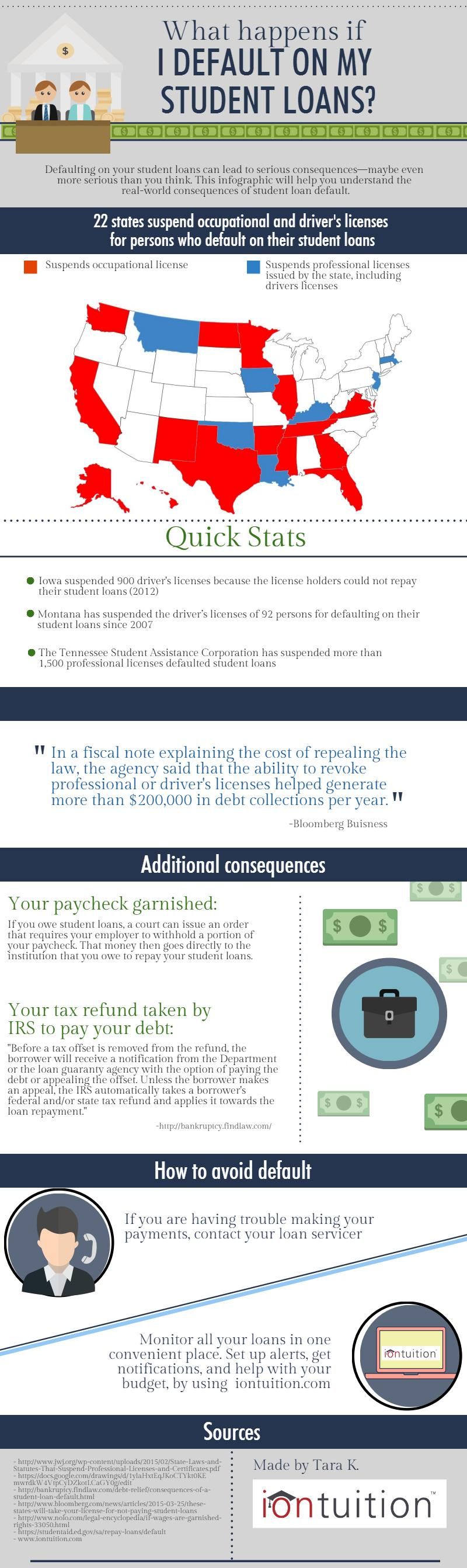

Wage Garnishment and Tax Refund Offset

These are some of the most aggressive and impactful collection methods the government can employ for defaulted federal student loans.

- Wage Garnishment: The government can order your employer to withhold a portion of your disposable pay (up to 15% for federal loans) to apply towards your defaulted loan, without needing a court order in most cases.

- Tax Refund Offset: Your federal and state income tax refunds, as well as certain federal benefit payments (like Social Security benefits, though with some exclusions), can be withheld to pay off your defaulted student loan.

- Social Security Benefit Offset: In extreme cases, a portion of your Social Security retirement or disability benefits can be offset to satisfy the debt.

Loss of Eligibility for Future Financial Aid

If you default on a federal student loan, you become ineligible for any future federal student aid, including grants, work-study, and new federal student loans. This can severely limit your ability to return to school or pursue further education.

Legal Action and Collection Fees

Both federal and private lenders can take legal action against you to collect the defaulted debt.

- Lawsuits: Lenders can sue you to obtain a judgment for the full amount of the loan, plus interest, collection costs, and attorney fees. Once a judgment is obtained, they can use various legal means to enforce it, such as levying bank accounts or placing liens on property.

- Collection Fees: The government can add significant collection fees (up to 25% of the principal and interest) to your defaulted federal loan balance, dramatically increasing the total amount you owe. Private lenders also have provisions for collection costs in their loan agreements.

Ineligibility for Deferment, Forbearance, and Income-Driven Repayment

Once your federal loan is in default, you lose access to valuable benefits that could help you manage your payments, such as deferment, forbearance, and enrollment in income-driven repayment (IDR) plans. These options are designed to prevent default, but they are generally unavailable once default has occurred, making it harder to get back on track.

Strategies for Resolution and Prevention: Getting Back on Track

The good news is that default is not a permanent state. There are pathways to resolve defaulted student loans and, even better, proactive strategies to prevent falling into default in the first place.

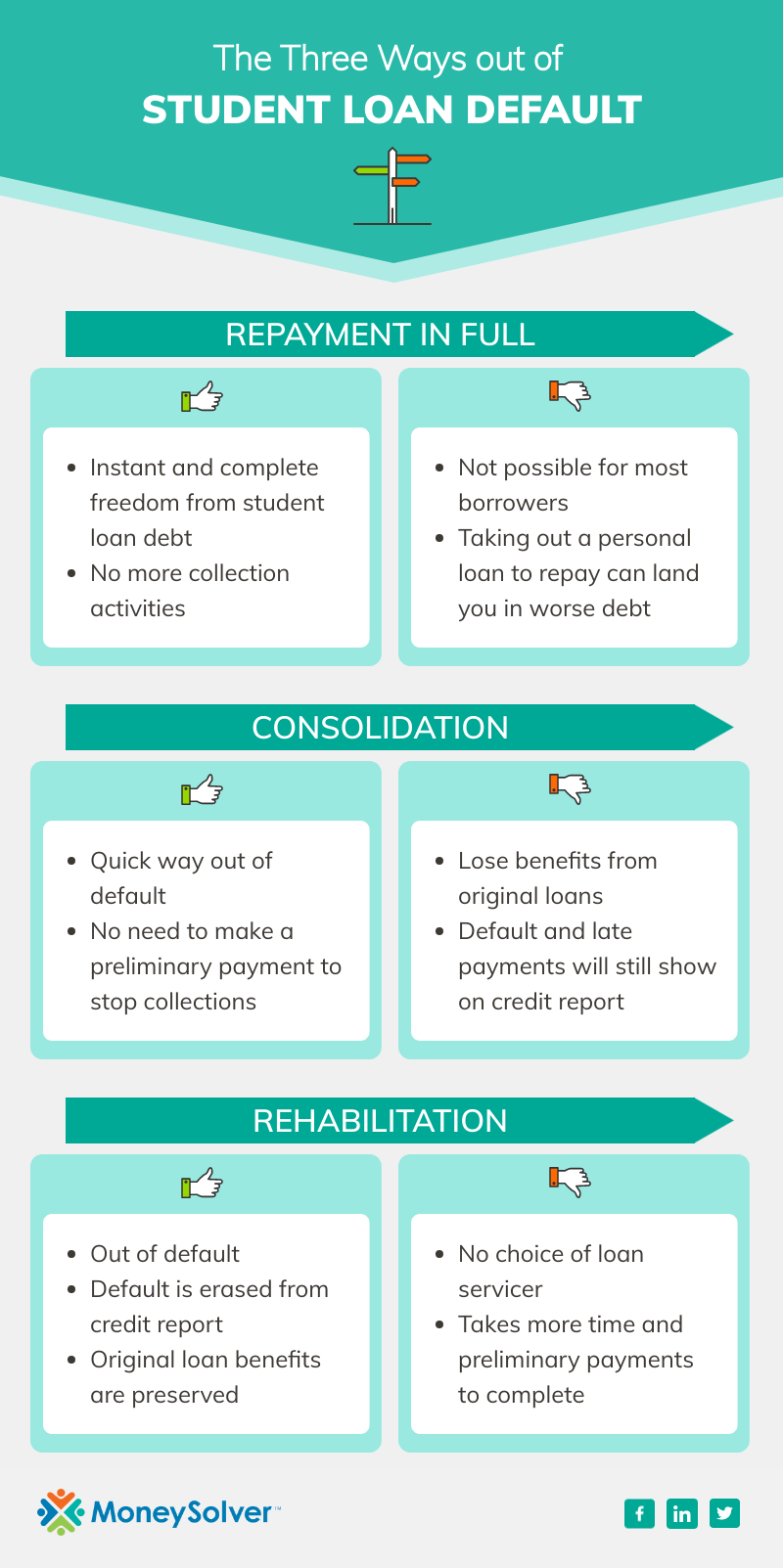

Resolving Default: Rehabilitation and Loan Consolidation

For federal student loans, two primary strategies exist to bring your loan out of default:

- Loan Rehabilitation: This is often considered the best option. It typically involves making nine voluntary, reasonable, and affordable monthly payments within a 10-month period. Once successfully completed, the default is removed from your credit report (though the history of late payments will remain), collection fees may be waived, and you regain eligibility for federal student aid and repayment options. You only get one chance to rehabilitate a defaulted federal student loan.

- Loan Consolidation: You can consolidate most defaulted federal student loans into a new Direct Consolidation Loan. To be eligible, you generally must either agree to repay the new loan under an Income-Driven Repayment (IDR) plan or make three consecutive, voluntary, on-time monthly payments on the defaulted loan before consolidation. While consolidation resolves the default, it does not remove the default from your credit history. It also often comes with a slightly higher interest rate and extends the repayment period.

Other Options: Repayment in Full or Compromise

While less common, these options are also available:

- Repayment in Full: If you have the means, paying the entire defaulted loan balance, including accrued interest and collection fees, will immediately resolve the default.

- Compromise (Settlement): In some cases, you may be able to negotiate a settlement with the collection agency or Department of Education to pay a lower lump sum than the full amount owed. This is typically reserved for extreme hardship cases and the difference forgiven may be taxable income.

Prevention is Key: Income-Driven Repayment Plans

For federal student loans, prevention is always better than cure. Income-Driven Repayment (IDR) plans are specifically designed to make your monthly loan payments affordable by capping them at a percentage of your discretionary income. There are several IDR plans (REPAYE, PAYE, IBR, ICR), each with slightly different terms. If your income is low enough, your payment could be as little as $0 per month, and these $0 payments still count toward forgiveness after a specified period (20 or 25 years, depending on the plan).

Temporary Relief: Deferment and Forbearance

If you’re facing a temporary financial hardship, federal student loan deferment or forbearance can provide a temporary pause or reduction in payments.

- Deferment: Allows you to temporarily postpone payments, and for some loans (like subsidized Stafford Loans), the government pays the interest during deferment.

- Forbearance: Allows you to temporarily stop or reduce your payments, but interest typically continues to accrue on all loan types, increasing your total debt.

- It’s crucial to apply for these before your loan defaults. They are not options once the loan is in default, though they can be critical tools to prevent it.

Proactive Communication with Your Servicer

The single most effective preventative measure is proactive and consistent communication with your loan servicer. If you anticipate difficulty making a payment, or if your financial situation changes, contact them immediately. They can inform you of available options like IDR plans, deferment, or forbearance, which can keep your loan in good standing and prevent the severe consequences of default.

Understanding the signs and consequences of student loan default is the first step towards financial empowerment. By knowing what to look for, utilizing available resources, and engaging proactively with your loan servicer, you can safeguard your financial future and navigate your student loan obligations successfully. Don’t let fear or confusion paralyze you; take action to understand your loan status and leverage the options available to you.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.