For many individuals, the journey toward financial independence and personal security is anchored by a single, significant milestone: homeownership. However, the path to owning a piece of real estate is rarely paved with liquid cash. Instead, it is built upon a foundational financial instrument known as a mortgage. At its core, a mortgage is more than just a loan; it is a sophisticated legal and financial contract that allows individuals to leverage future earnings to secure a tangible asset today. In the realm of personal finance, understanding the intricacies of a mortgage is essential, as it often represents the largest financial commitment a person will make in their lifetime.

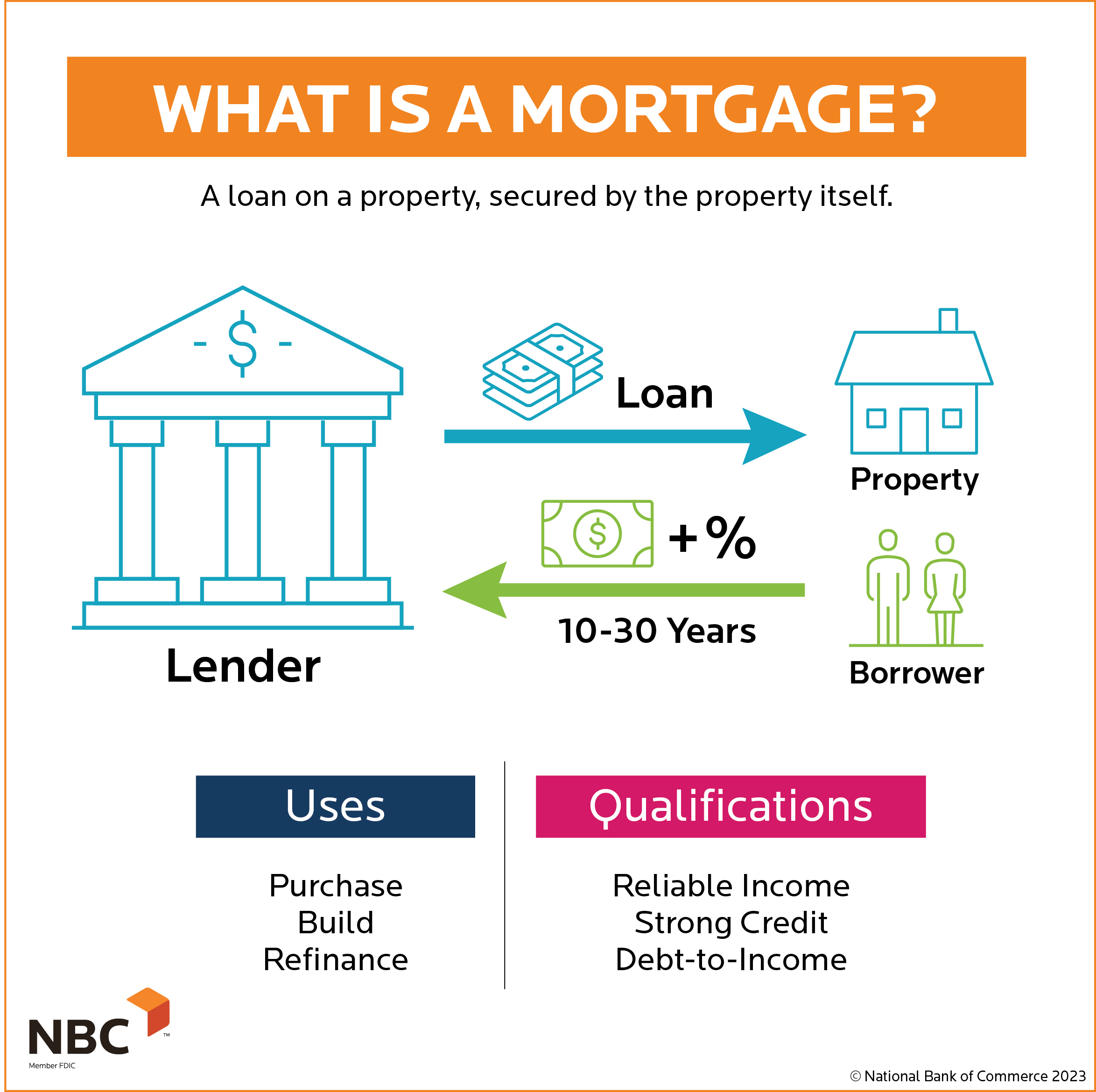

A mortgage is a debt instrument, secured by the collateral of specified real estate property, that the borrower is obliged to pay back with a predetermined set of payments. If the borrower fails to make these payments, the lender—typically a bank or credit union—has the legal right to seize the property through a process known as foreclosure. This relationship between the borrower, the lender, and the asset creates a unique dynamic that influences everything from national interest rates to individual retirement planning.

The Mechanics of a Mortgage: How Home Financing Works

To navigate the world of personal finance effectively, one must understand how a mortgage functions beyond the monthly payment. A mortgage is structured to balance the lender’s risk with the borrower’s ability to pay, all while accounting for the time value of money.

Principal and Interest: The Core Components

Every mortgage payment is primarily divided into two parts: principal and interest. The principal is the actual amount of money borrowed to purchase the home. The interest is the cost of borrowing that money, expressed as a percentage. In the early years of a mortgage, a significant portion of each payment goes toward interest. As the loan matures, a larger share is applied to the principal, a process known as amortization. Understanding this balance is crucial for homeowners who wish to build equity—the portion of the home they truly “own”—more quickly.

The Role of the Down Payment

The down payment is the initial equity a buyer puts into the property. From a “Money” niche perspective, the down payment is a critical lever. A larger down payment reduces the total loan amount, which lowers monthly payments and total interest paid over the life of the loan. Traditionally, a 20% down payment is the gold standard, as it often allows the borrower to avoid additional costs like Private Mortgage Insurance (PMI) and secures more favorable interest rates. However, various financial strategies allow for lower down payments, provided the borrower understands the long-term cost implications.

Amortization Schedules and Loan Terms

The “term” of a mortgage refers to the length of time the borrower has to repay the loan. The most common terms in the United States are 15 and 30 years. A 30-year mortgage offers lower monthly payments, providing the borrower with more “cash flow” flexibility for other investments or expenses. Conversely, a 15-year mortgage usually carries a lower interest rate and results in significantly less interest paid over time, though it requires a higher monthly financial commitment. Choosing between these terms is a strategic decision that depends on one’s broader financial goals and risk tolerance.

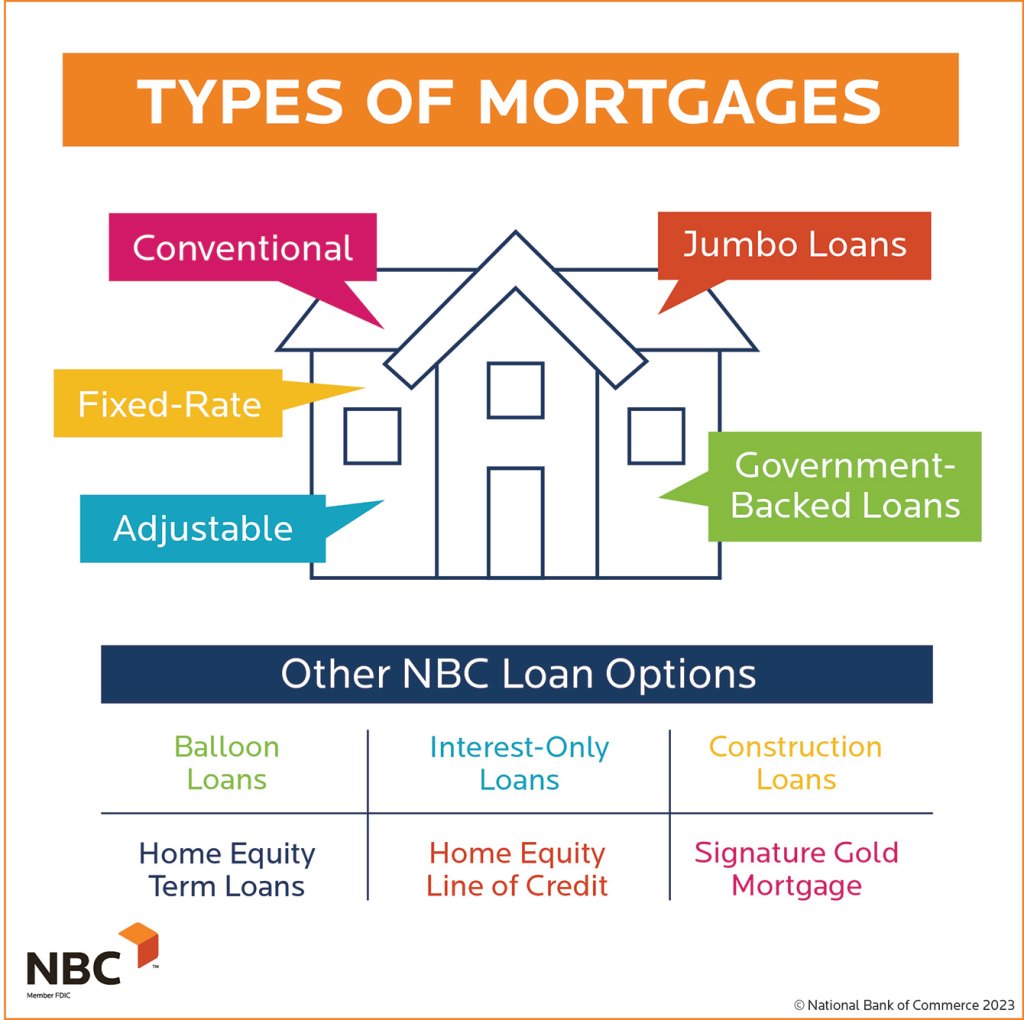

Types of Mortgages: Choosing the Right Financial Vehicle

Not all mortgages are created equal. The financial industry has developed a variety of products to suit different economic climates and borrower profiles. Selecting the right type of mortgage can save a borrower tens of thousands of dollars over the duration of the loan.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

The most common choice is the fixed-rate mortgage, where the interest rate remains the same for the entire life of the loan. This provides predictability and protection against rising market interest rates. On the other hand, an Adjustable-Rate Mortgage (ARM) offers a lower initial interest rate for a set period (e.g., five or seven years), after which the rate adjusts based on market indices. ARMs can be beneficial for those who plan to sell or refinance before the adjustment period begins, but they carry the risk of significantly higher payments in the future.

Government-Backed Loans: FHA, VA, and USDA

For those who may not qualify for traditional financing, the government offers programs to encourage homeownership. FHA loans, insured by the Federal Housing Administration, allow for lower credit scores and down payments as low as 3.5%. VA loans are available to veterans and active-duty service members, often requiring no down payment at all. USDA loans target rural homebuyers with low-to-moderate incomes. While these loans make entry into the market easier, they often come with specific fees or insurance requirements that must be factored into the long-term budget.

Conventional and Jumbo Loans

Conventional loans are not insured by the federal government and typically follow the guidelines set by Fannie Mae or Freddie Mac. They are often the preferred choice for borrowers with strong credit scores and stable income. However, when the price of a luxury property or a home in a high-cost area exceeds “conforming” limits, borrowers must turn to Jumbo loans. These require more stringent credit checks and larger down payments because they represent a higher risk for the lender.

The True Cost of Borrowing: Beyond the Monthly Payment

One of the most common mistakes in personal finance is equating a mortgage payment solely with principal and interest. In reality, the total cost of homeownership involves several other recurring expenses that can impact a household’s net worth and monthly liquidity.

Property Taxes and Homeowners Insurance

Lenders generally require borrowers to pay property taxes and homeowners insurance as part of their monthly mortgage bill. These funds are held in an “escrow” account and paid out by the lender when the bills are due. Property taxes vary significantly by location and can increase over time, potentially raising the monthly payment even if the mortgage has a fixed interest rate. Insurance is equally vital, protecting the asset (and the lender’s collateral) from fire, theft, and natural disasters.

Private Mortgage Insurance (PMI)

If a borrower puts down less than 20% on a conventional loan, the lender will typically require Private Mortgage Insurance. PMI protects the lender in case the borrower defaults. For the borrower, however, it is an added expense that provides no direct benefit to their equity. Smart financial planning involves monitoring the home’s value; once the loan-to-value ratio reaches 80%, the borrower can often request to cancel PMI, freeing up cash for other investments.

Closing Costs and Maintenance Reserves

The financial burden of a mortgage begins before the first payment is even made. Closing costs—which include appraisal fees, title insurance, and loan origination fees—typically range from 2% to 5% of the purchase price. Furthermore, a responsible homeowner must maintain a “maintenance reserve.” Unlike renting, where the landlord covers repairs, the homeowner is responsible for everything from a leaky roof to a broken HVAC system. Integrating these costs into a long-term financial plan is essential to avoid “house poor” scenarios where all income is consumed by housing costs.

The Path to Approval: Preparing Your Financial Profile

Securing a mortgage is a rigorous process that requires the borrower to present a “clean” and robust financial profile. Lenders look at several key metrics to determine creditworthiness and the interest rate they will offer.

Credit Scores and Interest Rate Sensitivity

A credit score is perhaps the most influential factor in the mortgage process. It serves as a shorthand for a borrower’s reliability. A higher score—typically 740 or above—unlocks the lowest possible interest rates. Even a 0.5% difference in an interest rate can result in tens of thousands of dollars in savings over 30 years. Therefore, improving one’s credit score before applying for a mortgage is one of the most effective ways to optimize personal wealth.

Debt-to-Income Ratio (DTI)

Lenders use the Debt-to-Income ratio to ensure a borrower isn’t overextending themselves. This ratio compares total monthly debt payments (including the prospective mortgage) to gross monthly income. Most lenders prefer a DTI of 36% or lower, though some programs allow for higher limits. Managing existing debts—such as student loans, car payments, and credit card balances—is vital for those looking to maximize their mortgage borrowing power.

The Importance of Pre-Approval

In a competitive real estate market, a pre-approval letter is an essential tool. This is a document from a lender stating exactly how much they are willing to lend based on a preliminary review of the borrower’s finances. From a strategic standpoint, pre-approval allows a buyer to move quickly and provides a clear boundary for their housing search, ensuring they remain within a budget that supports their overall financial health.

Mortgage Management and Long-Term Financial Health

Once the mortgage is secured and the keys are handed over, the focus shifts from acquisition to management. A mortgage is a dynamic tool that can be adjusted as market conditions and personal circumstances change.

Refinancing Strategies

Refinancing involves replacing an existing mortgage with a new one, typically to take advantage of lower interest rates or to change the loan term. A “rate-and-term” refinance can lower monthly payments, while a “cash-out” refinance allows homeowners to tap into their home’s equity to fund renovations, consolidate high-interest debt, or invest in other assets. However, because refinancing involves new closing costs, it is important to calculate the “break-even point”—the moment when the savings from the lower rate outweigh the costs of getting the new loan.

Equity Building and Wealth Creation

For many, a mortgage is a forced savings account. Each month, a portion of the payment goes toward the principal, increasing the owner’s stake in the property. Over decades, this equity builds significant wealth, especially if the property appreciates in value. This equity can eventually be used to fund retirement through a downsized sale or a reverse mortgage, or it can be passed down as an inheritance, serving as a pillar of generational wealth.

The Debate: Paying Off the Mortgage Early

A common question in personal finance is whether to use extra cash to pay down a mortgage early or to invest that money in the stock market. The answer depends on the interest rate of the mortgage versus the expected return on investments. If a mortgage has a 3% interest rate and the stock market offers a historical average of 7-10%, it may be more mathematically sound to invest. However, the psychological peace of mind that comes with being “debt-free” is a valid financial goal that many prioritize as they approach retirement.

In conclusion, a mortgage is far more than a simple loan for a house. It is a complex financial instrument that, when managed correctly, serves as a catalyst for wealth creation and financial stability. By understanding the mechanics of principal and interest, the variety of loan products available, and the importance of maintaining a strong financial profile, individuals can transform the challenge of a mortgage into a strategic advantage on their journey toward financial independence.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.