For most individuals, a mortgage is the most significant financial obligation they will ever undertake. Because the principal amounts are so high and the terms are so long—often spanning 15 to 30 years—even a fraction of a percentage point in the interest rate can result in tens of thousands of dollars in savings or costs over the life of the loan. However, the definition of a “good” interest rate is not a static number. It is a moving target influenced by global economic shifts, federal policy, and the unique financial profile of the borrower. To understand what constitutes a good rate in today’s market, one must look beyond the daily headlines and analyze the mechanics of the lending industry.

The Macroeconomic Landscape: Why Rates Fluctuate

The primary driver of mortgage rates is not the individual bank, but rather the broader economic environment. To identify a good rate, a borrower must first understand the benchmark against which all rates are measured.

The Role of the Federal Reserve and Treasury Yields

While the Federal Reserve does not directly set mortgage rates, its influence is profound. When the Fed adjusts the federal funds rate to combat inflation or stimulate growth, it triggers a ripple effect across the entire financial system. Mortgage rates generally track the yield on the 10-year Treasury note. When investors are confident in the economy, they may pull out of bonds, causing yields (and mortgage rates) to rise. Conversely, during times of economic uncertainty, investors flock to the safety of government bonds, which typically drives yields and mortgage rates downward. A “good” rate today might have been considered astronomical three years ago, yet remains historically low when compared to the double-digit rates of the 1980s.

Fixed-Rate vs. Adjustable-Rate Mortgages (ARMs)

A good rate also depends on the structure of the loan. Fixed-rate mortgages provide the security of a consistent payment for the duration of the loan. In contrast, Adjustable-Rate Mortgages (ARMs) often offer a lower “teaser” rate for an initial period (such as five, seven, or ten years). For a borrower planning to sell the property or refinance within a short window, a “good” rate might be a 5/1 ARM that sits 1% below the 30-year fixed average. However, for a long-term homeowner, that same rate represents a significant risk of future escalation. Deciding which rate is “good” requires a clear assessment of one’s intended timeline for property ownership.

The Individual Equation: Personal Variables that Define Your Rate

A bank’s “advertised” rate is rarely the rate a borrower actually receives. Lenders use a process called risk-based pricing to determine the specific interest rate for each applicant. Therefore, a good rate is one that is at or below the market average for your specific risk tier.

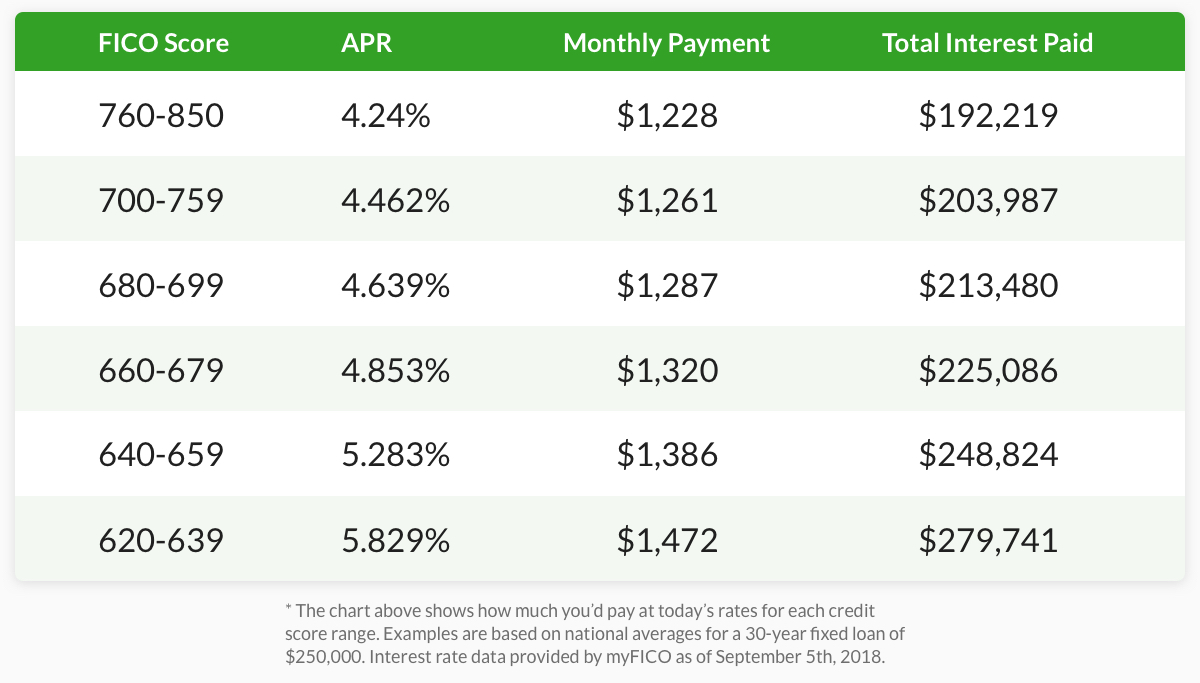

The Critical Impact of Credit Scores

Your credit score is the single most influential factor in the rate you are offered. Lenders typically categorize borrowers into tiers. Those with “Excellent” credit (usually 740 or higher) are eligible for the lowest possible rates. A borrower with a 760 score might be offered a 6.5% rate, while a borrower with a 620 score might be quoted 7.8% for the exact same house. In the context of personal finance, a good rate is any rate that aligns with the top-tier pricing for your credit bracket. If your score is on the cusp of a higher tier, it is often financially prudent to spend a few months improving your credit profile before locking in a rate, as the long-term savings are substantial.

Loan-to-Value (LTV) Ratio and Down Payments

The amount of equity you have in a home acts as a buffer for the lender. The Loan-to-Value ratio—the percentage of the home’s value that is financed—dictates the level of risk the bank assumes. Generally, a down payment of 20% or more eliminates the need for Private Mortgage Insurance (PMI) and secures a more favorable interest rate. Borrowers putting down only 3% or 5% may find that their interest rate is slightly higher to compensate for the increased risk of default. When evaluating if a rate is good, you must factor in whether it includes or excludes the cost of mortgage insurance, as the “effective” rate on your monthly cash flow may be much higher than the nominal interest rate suggests.

Debt-to-Income (DTI) Ratio and Loan Type

Lenders also examine your Debt-to-Income ratio to ensure you aren’t overleveraged. A lower DTI can sometimes lead to more competitive offers. Furthermore, the type of loan—Conventional, FHA, VA, or USDA—has its own “good” rate standard. VA loans, for example, often offer lower interest rates than conventional loans but come with specific funding fees. A good rate for an FHA borrower might be higher than a good rate for a conventional borrower, but the FHA loan may be the only viable path to homeownership for that individual.

Strategies to Secure and Optimize Your Rate

Securing a good mortgage rate is not a passive activity; it requires a combination of timing, negotiation, and mathematical analysis.

The Power of Rate Shopping and Comparison

One of the most common mistakes in personal finance is accepting the first mortgage quote provided by a primary bank. Studies consistently show that borrowers who obtain quotes from at least three different lenders save thousands of dollars. Different institutions—credit unions, national banks, and independent mortgage brokers—have different overhead costs and risk appetites. A “good” rate is the lowest one you can find after a comprehensive search. It is essential to request a Loan Estimate from each lender, which provides a standardized breakdown of the interest rate and associated fees, allowing for an “apples-to-apples” comparison.

Buying Down the Rate with Discount Points

In many cases, you can “buy” a lower interest rate by paying discount points at closing. One point typically costs 1% of the total loan amount and reduces the interest rate by approximately 0.25%. Whether this results in a “good” deal depends on your break-even point. For example, if paying $4,000 in points saves you $100 a month on your mortgage, it will take 40 months to break even. If you plan to stay in the home for 10 years, buying down the rate is an excellent financial move. If you plan to move in three years, it is a poor use of capital.

Timing the Market vs. Rate Locks

Mortgage rates can fluctuate daily or even hourly based on economic data releases. Once you find a rate that fits your budget and is competitive with current averages, the next step is “locking” that rate. A rate lock protects you from increases during the 30 to 60 days it takes to close the loan. While some borrowers try to “time the market” to catch a dip, this is notoriously difficult. A good rate is one that is locked in at a level that makes the monthly payment sustainable for your household budget, regardless of what happens to the market the following week.

The True Cost: Interest Rate vs. APR

In the pursuit of a low interest rate, many borrowers fall into the trap of ignoring the “Annual Percentage Rate” (APR). Understanding the distinction between these two figures is vital for anyone focused on their financial health.

Why the APR Matters More Than the Nominal Rate

The interest rate refers specifically to the cost of borrowing the principal balance. The APR, however, is a broader measure that includes the interest rate plus other costs, such as lender fees, closing costs, and mortgage insurance. A lender might offer a “good” interest rate of 6.2% but charge high origination fees that push the APR to 6.8%. Meanwhile, another lender might offer a 6.4% interest rate with zero fees, resulting in a 6.45% APR. In this scenario, the higher interest rate is actually the better deal. Always use the APR as your primary metric for determining the competitiveness of a mortgage offer.

Refinancing: When Does a New Rate Become “Good”?

For existing homeowners, a good rate is defined by its relationship to their current rate. The traditional rule of thumb was that a 1% to 2% drop in rates justified a refinance. However, with the rise of “no-cost” refinances and shorter break-even periods, even a 0.5% to 0.75% reduction can be beneficial depending on the remaining balance of the loan. A good refinance rate is one that lowers your monthly obligation or shortens your loan term enough to offset the closing costs of the new loan within a reasonable timeframe (usually 24 to 36 months).

Conclusion: Defining Your “Good” Rate

Ultimately, a good interest rate on a mortgage is a intersection of market conditions and personal financial readiness. While you cannot control the Federal Reserve or global inflation, you can control your credit score, your debt levels, and the thoroughness of your lender research.

A good rate is one that allows you to build equity without straining your monthly cash flow, fits within a long-term investment strategy, and represents the most competitive offer available for your specific financial profile. By focusing on the APR, shopping among multiple lenders, and understanding the impact of your credit tier, you can secure a mortgage that serves as a foundation for long-term wealth rather than a financial burden. In the world of money and personal finance, knowledge and preparation are the most effective tools for turning a market average into a personal advantage.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.