For the average individual or family, health insurance is often the second-largest monthly expense, trailing only behind housing costs. In the landscape of personal finance, understanding the true cost of health insurance is not just about looking at a monthly premium; it is about calculating the total cost of ownership, managing risk, and leveraging financial tools to mitigate out-of-pocket exposure.

The price of health insurance is a moving target, influenced by age, geography, plan type, and the degree of financial risk an individual is willing to shoulder. To manage your budget effectively, you must look beyond the sticker price and analyze the structural components of health care financing.

Understanding the Base Cost: Premiums and Plan Tiers

The most visible cost of health insurance is the monthly premium—the fee you pay to the insurance company to keep your policy active. In the United States, these costs vary significantly based on how you obtain coverage and the level of protection you choose.

The Metal Tiers: Bronze, Silver, Gold, and Platinum

The Affordable Care Act (ACA) marketplace categorized plans into “metal tiers” to help consumers compare costs. These tiers do not reflect the quality of medical care but rather how the costs are shared between the insurer and the policyholder.

- Bronze Plans: These have the lowest monthly premiums but the highest out-of-pocket costs when you receive care. They are often the most cost-effective choice for healthy individuals who rarely see a doctor.

- Silver Plans: These represent the middle ground and are the most popular. They offer moderate premiums and deductibles. Notably, Silver plans are the only ones eligible for cost-sharing reductions if your income falls within certain brackets.

- Gold and Platinum Plans: These carry high monthly premiums but very low deductibles and copayments. From a financial planning perspective, these are “predictable” plans, ideal for those with chronic conditions who require frequent medical services.

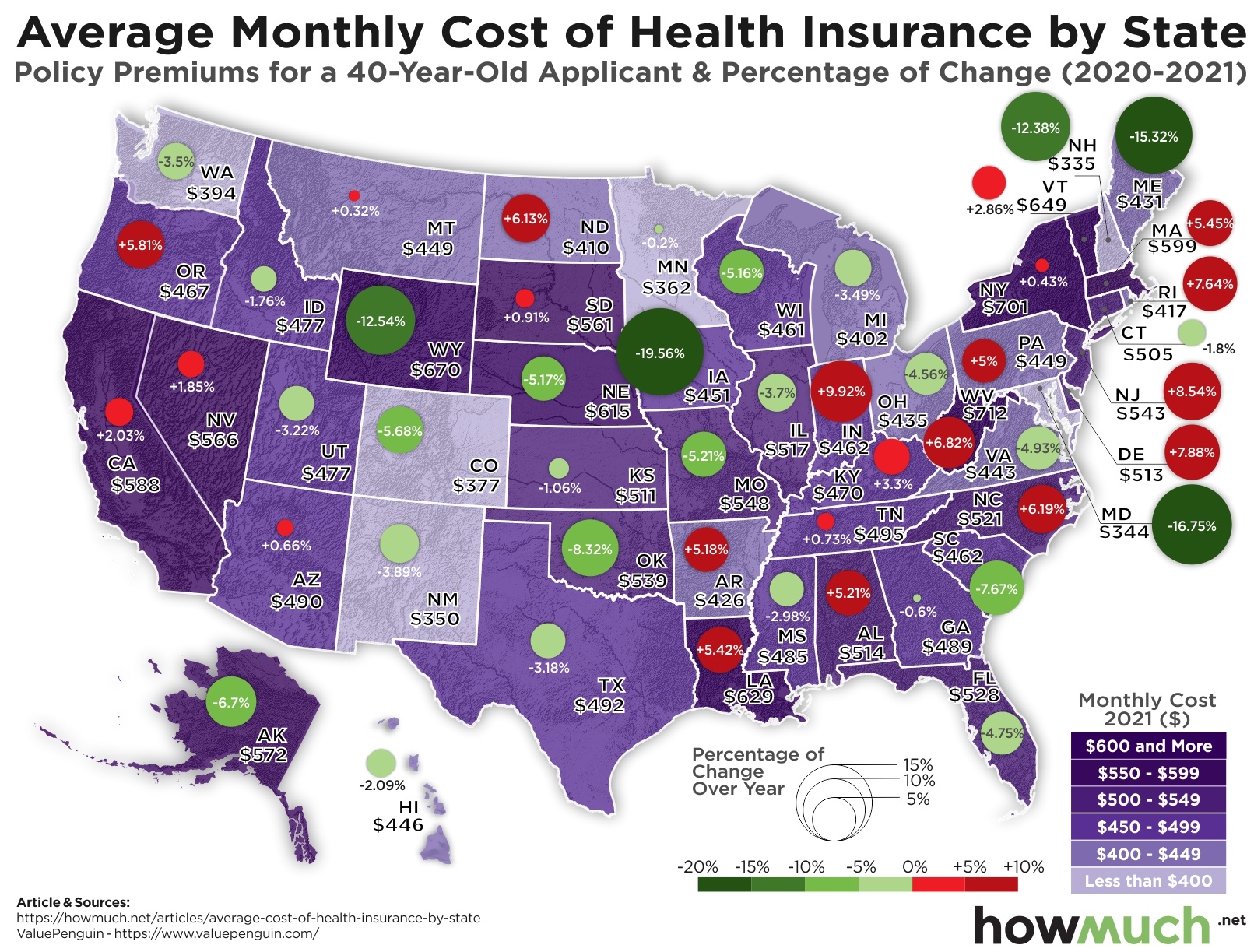

How Age and Location Influence Your Monthly Rates

Insurance companies utilize “community rating” and “age rating” to determine premiums. While the ACA prevents insurers from charging more for pre-existing conditions, they can still charge older individuals up to three times more than younger individuals. Additionally, geography plays a massive role; a plan in a rural area with limited competition among providers may cost significantly more than a similar plan in a metropolitan hub where several hospital systems compete for patients.

Employer-Sponsored vs. Individual Marketplace Plans

For most Americans, the “real” cost of health insurance is masked by employer subsidies. According to recent data, the average annual premium for family coverage through an employer is over $22,000, but the employee typically only pays about 25% to 30% of that amount. When transitioning to the individual marketplace (as a freelancer or entrepreneur), the sudden jump to paying 100% of the premium can be a significant financial shock.

Beyond the Premium: Decoding Out-of-Pocket Expenses

To answer “how expensive is health insurance,” one must account for the “hidden” costs that occur only when you actually use the healthcare system. These costs can turn a “cheap” plan into a financial burden very quickly.

Deductibles and Their Impact on Monthly Cash Flow

The deductible is the amount you must pay out-of-pocket for covered health care services before your insurance plan begins to pay. In the modern financial era, “High Deductible Health Plans” (HDHPs) have become the norm. While they lower your monthly premium, a deductible of $3,000 or $7,000 means you must have that liquidity available in a high-yield savings account or an HSA to cover an emergency. Failing to account for the deductible in your emergency fund is a common personal finance oversight.

Copayments vs. Coinsurance: Paying for Service

Once your deductible is met, you still share the cost with the insurer through copayments (fixed fees, such as $30 for a doctor visit) or coinsurance (a percentage of the total bill, usually 20%). In a financial model, coinsurance is the riskier of the two. A 20% coinsurance on a $50,000 surgery is $10,000, which can be devastating if you haven’t tracked your plan’s maximum limits.

The Importance of the Out-of-Pocket Maximum

The out-of-pocket maximum is the most important number for financial risk management. It is the absolute ceiling on what you will pay in a policy year for covered “in-network” services. Once you hit this limit, the insurance company pays 100% of allowed charges. For 2024, the legal limit for an individual is $9,450. When budgeting, you should always ensure your “worst-case scenario” involves having access to this amount of capital.

Strategic Financial Tools for Health Care Management

Sophisticated financial planning treats health insurance not just as a cost, but as an opportunity to utilize tax-advantaged vehicles. By choosing the right plan, you can actually lower your overall tax liability.

Health Savings Accounts (HSAs) as an Investment Vehicle

If you are enrolled in a qualifying High Deductible Health Plan, you gain access to a Health Savings Account (HSA). Financial experts often refer to the HSA as the “ultimate” retirement account due to its triple tax advantage:

- Tax-Deductible Contributions: Money goes in pre-tax, lowering your taxable income.

- Tax-Free Growth: Any interest or investment gains within the account are not taxed.

- Tax-Free Withdrawals: As long as the money is used for qualified medical expenses, it is never taxed.

For those in high tax brackets, the HSA can effectively “discount” health care costs by 20% to 35%, depending on their marginal tax rate.

Flexible Spending Accounts (FSAs): Use It or Lose It

Unlike an HSA, an FSA is usually employer-sponsored and does not require a high-deductible plan. It allows you to set aside pre-tax dollars for medical expenses. However, the “use it or lose it” rule applies; if you don’t spend the money by the end of the year (or grace period), the funds revert to the employer. This requires careful annual forecasting of your medical needs to avoid losing money.

Tax Credits and Subsidies for Lowering Costs

For those buying insurance on the individual marketplace, the Premium Tax Credit (PTC) is a vital tool. This credit is based on household income relative to the Federal Poverty Level. For many middle-income earners, these subsidies can reduce a $600 monthly premium down to $100 or less, fundamentally changing the affordability equation of health care.

Hidden Costs and How to Mitigate Financial Risk

Even with a robust plan, certain variables can drive up the “expense” of health insurance unexpectedly. Awareness of these factors is essential for maintaining a stable financial plan.

In-Network vs. Out-of-Network Penalties

The “Network” is the list of doctors and hospitals that have negotiated rates with your insurer. Stepping outside of this network can be the most expensive mistake a consumer makes. Out-of-network providers can “balance bill” you for the difference between what they charge and what the insurance company pays. Always verify that both the facility and the specific provider (such as an anesthesiologist) are in-network before elective procedures.

Prescription Drug Formularies and Tiered Pricing

The cost of medication is often segmented into tiers. Tier 1 (Generics) might cost $10, while Tier 4 (Specialty drugs) might require 50% coinsurance. If you rely on specific maintenance medications, you must review the “formulary” of a plan before signing up. A plan with a lower premium might actually be more expensive if it places your necessary medication in a high-cost tier.

The Cost of Being Uninsured: A Risk Management Perspective

In a discussion about the expense of insurance, one must consider the expense of not having it. A single major medical event, such as a heart attack or a serious car accident, can result in hospital bills exceeding $100,000. In the United States, medical debt remains a leading cause of bankruptcy. Viewing health insurance premiums as a “risk premium” helps frame the cost as a defensive investment against total financial ruin.

Maximizing Value: How to Choose the Most Cost-Effective Plan

The most “expensive” plan is often the one that doesn’t fit your lifestyle. Choosing the right plan requires a mathematical comparison of different scenarios.

Analyzing Your Annual Medical Utilization

To find the most cost-effective plan, start by auditing your last 24 months of medical usage. Do you visit the doctor twice a year for check-ups, or do you have monthly physical therapy?

- Low Utilizers: Should prioritize low-premium, high-deductible plans (HDHPs) and funnel the savings into an HSA.

- High Utilizers: Should prioritize Gold or Platinum plans with low deductibles and low coinsurance, as the higher premium is offset by the insurance company picking up a larger share of frequent bills.

Comparing Total Cost of Ownership (TCO) Across Plans

To truly understand the cost, use this formula:

(Monthly Premium x 12) + Expected Out-of-Pocket Costs = Total Cost of Ownership.

When you run this calculation, you might find that a “Gold” plan with a $1,000 monthly premium and $0 deductible is actually cheaper over a year than a “Bronze” plan with a $400 premium and a $9,000 deductible, especially if you have an upcoming surgery planned.

In conclusion, health insurance is as expensive as your risk profile and financial strategy allow it to be. By understanding the interaction between premiums, deductibles, and tax-advantaged accounts, you can transform health insurance from a confusing monthly drain into a managed component of your long-term wealth strategy. Whether through employer plans or the marketplace, the goal remains the same: minimizing the financial impact of medical care while maximizing your protection against the unknown.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.