The question “how many banks are in the US?” might seem straightforward, but its answer is anything but simple. The financial landscape of the United States is a dynamic ecosystem, constantly reshaped by economic forces, regulatory changes, technological advancements, and evolving consumer demands. What constitutes a “bank” itself can be a nuanced definition, leading to varying figures depending on the criteria applied. Understanding the number of banks isn’t merely an exercise in counting; it offers profound insights into the health, structure, and future direction of one of the world’s most complex financial systems. This exploration delves into the current state of U.S. banking, the historical trends that have shaped it, and the underlying factors driving its continuous transformation, all firmly within the realm of personal finance, business finance, and financial tools.

The Evolving Landscape of U.S. Banking

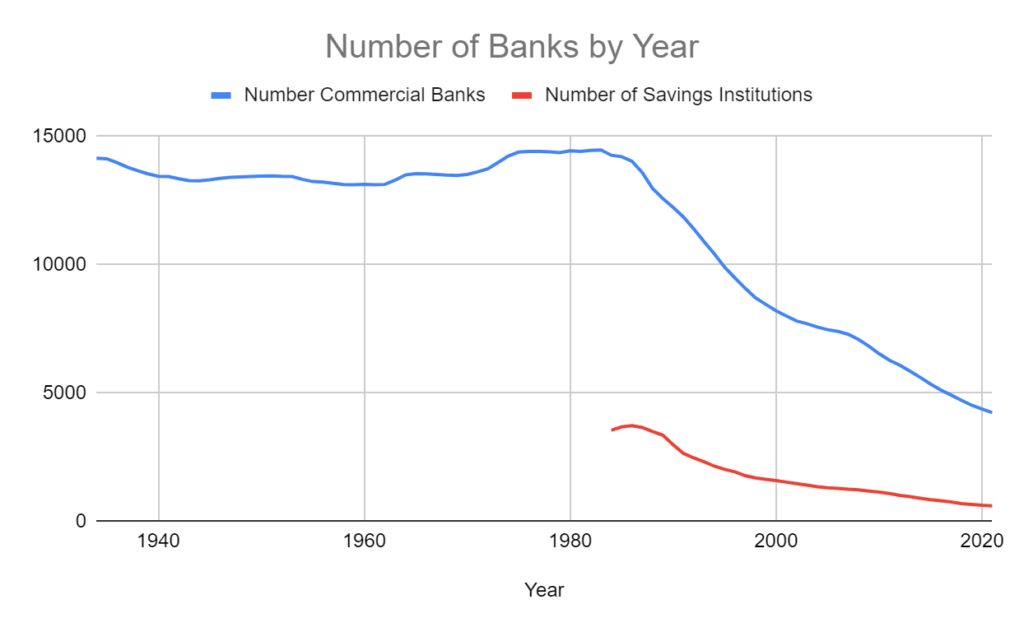

The narrative of U.S. banking is one of constant flux, marked by periods of expansion, consolidation, and reinvention. From a peak of over 14,000 commercial banks in the mid-1980s, the number has seen a significant decline, yet the industry’s total assets have skyrocketed. This paradox hints at a deeper story of efficiency, scale, and specialization that defines the modern financial era.

A Dynamic Industry in Flux

Historically, the U.S. boasted a highly fragmented banking system, a legacy of states’ rights and a distrust of centralized financial power. This led to a plethora of small, local banks serving specific communities. However, deregulation efforts beginning in the 1980s, coupled with technological progress, ushered in an era of rapid consolidation. The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994, for instance, removed many restrictions on interstate banking, accelerating mergers and acquisitions. This consolidation wasn’t just about fewer institutions; it was about the emergence of banking giants capable of operating across state lines and offering a wider array of services.

Today, the industry continues to navigate a complex environment. On one hand, fintech innovators are challenging traditional banking models, offering specialized services that often bypass established banks. On the other, the foundational role of traditional banks in providing credit, managing deposits, and facilitating payments remains indispensable. This interplay between legacy institutions and agile newcomers defines much of the industry’s current dynamic, influencing both its structure and the financial products available to consumers and businesses. The pace of change, driven by digital transformation and shifting customer expectations, ensures that the “number of banks” is never a static figure, but rather a snapshot of an industry in perpetual motion.

Distinguishing Between Bank Types

To accurately answer how many “banks” exist, we must first clarify what we’re counting. The term “bank” is often used broadly, but within the financial sector, there are critical distinctions:

- Commercial Banks: These are the most common type, accepting deposits, making loans to individuals and businesses, and offering a range of financial services like checking accounts, savings accounts, mortgages, and business loans. They are typically for-profit entities and are insured by the Federal Deposit Insurance Corporation (FDIC). When people ask “how many banks,” they are usually referring to these institutions.

- Credit Unions: Member-owned, non-profit financial cooperatives that offer many of the same services as commercial banks but are generally focused on serving specific communities or groups (e.g., employees of a certain company, residents of a specific area). They are insured by the National Credit Union Administration (NCUA). While functionally similar to banks for many purposes, they are legally distinct and are typically counted separately in official statistics.

- Investment Banks: These institutions primarily engage in activities like underwriting new stock and bond issues, facilitating mergers and acquisitions, and providing financial advisory services to corporations and governments. They typically do not accept consumer deposits or offer traditional retail banking services.

- Savings Institutions: Historically distinct from commercial banks, savings and loan associations (S&Ls) and savings banks focused more on residential mortgages and consumer savings. Today, many have converted to commercial bank charters, blurring the lines, but some independent savings institutions still exist.

For the purpose of answering “how many banks,” the focus is overwhelmingly on FDIC-insured commercial banks and savings institutions, which are the primary providers of retail and commercial banking services to the general public and businesses.

Unpacking the Numbers: What Constitutes a Bank?

Understanding the precise count of banks requires delving into official statistics and the methodologies used by regulatory bodies. The number fluctuates, not just daily, but fundamentally due to the specific criteria employed.

Defining “Bank” for Counting Purposes

When regulators and financial economists count “banks,” they primarily refer to institutions that are federally or state-chartered and whose deposits are insured by the FDIC. This definition is crucial because it includes a vast majority of institutions that offer traditional banking services to the public. These institutions operate under strict regulatory oversight, ensuring stability and depositor confidence.

- FDIC-Insured Institutions: The gold standard for counting, as it covers nearly all depository institutions that serve the public. This includes both commercial banks and savings institutions, regardless of whether they hold federal (national) or state charters.

- State vs. Federally Chartered: Banks can be chartered either by a state or by the federal government (through the Office of the Comptroller of the Currency, OCC). Both types are subject to federal oversight, particularly if they are FDIC-insured, but their primary chartering authority differs. Counting both ensures a comprehensive view of the traditional banking sector.

It’s important to note that this definition usually excludes credit unions (which are NCUA-insured), investment banks (which don’t take deposits), and non-bank financial institutions like mortgage companies, payday lenders, or fintech startups that partner with banks for deposit services but don’t hold bank charters themselves. While these entities play a significant role in the broader financial ecosystem, they are not “banks” in the strict regulatory sense for this specific count.

Key Data Sources and Their Revelations

The primary source for the number of FDIC-insured institutions is, unsurprisingly, the Federal Deposit Insurance Corporation (FDIC). The FDIC regularly publishes data on the number of insured commercial banks and savings institutions.

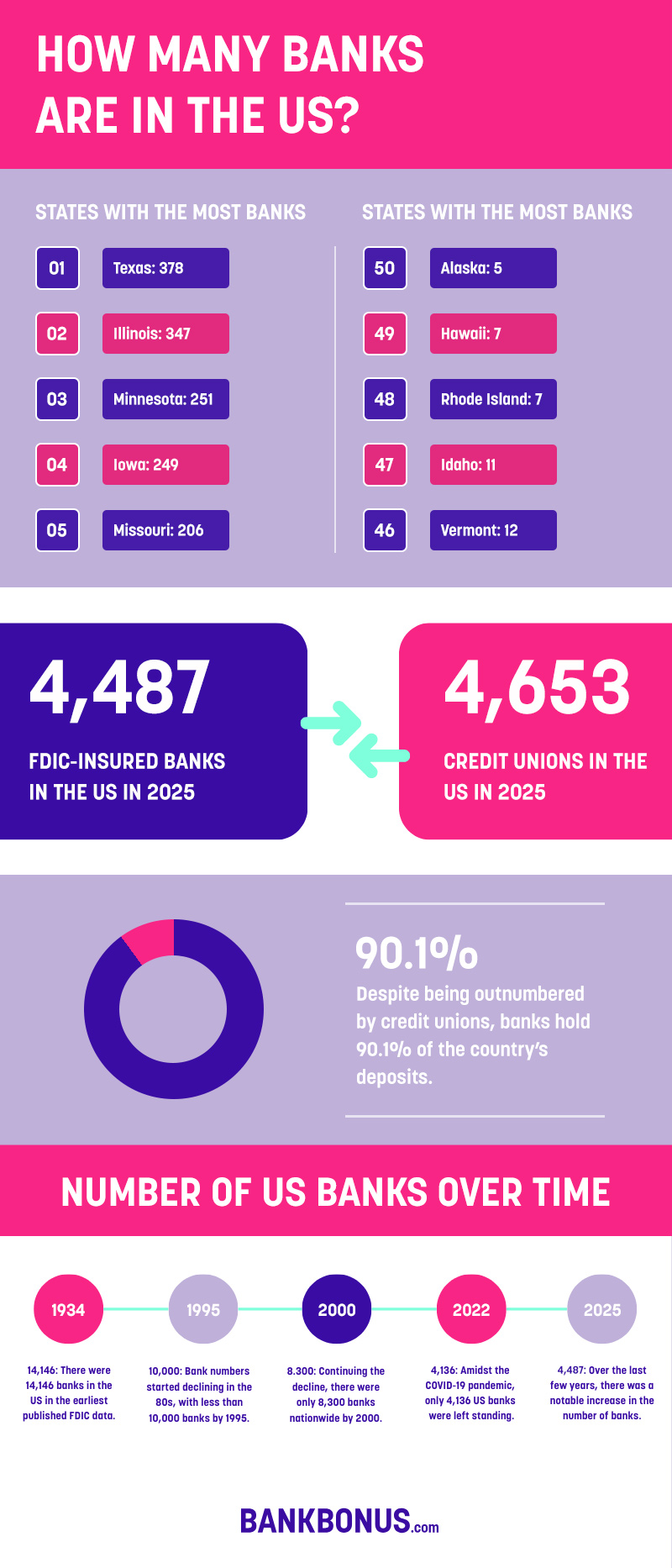

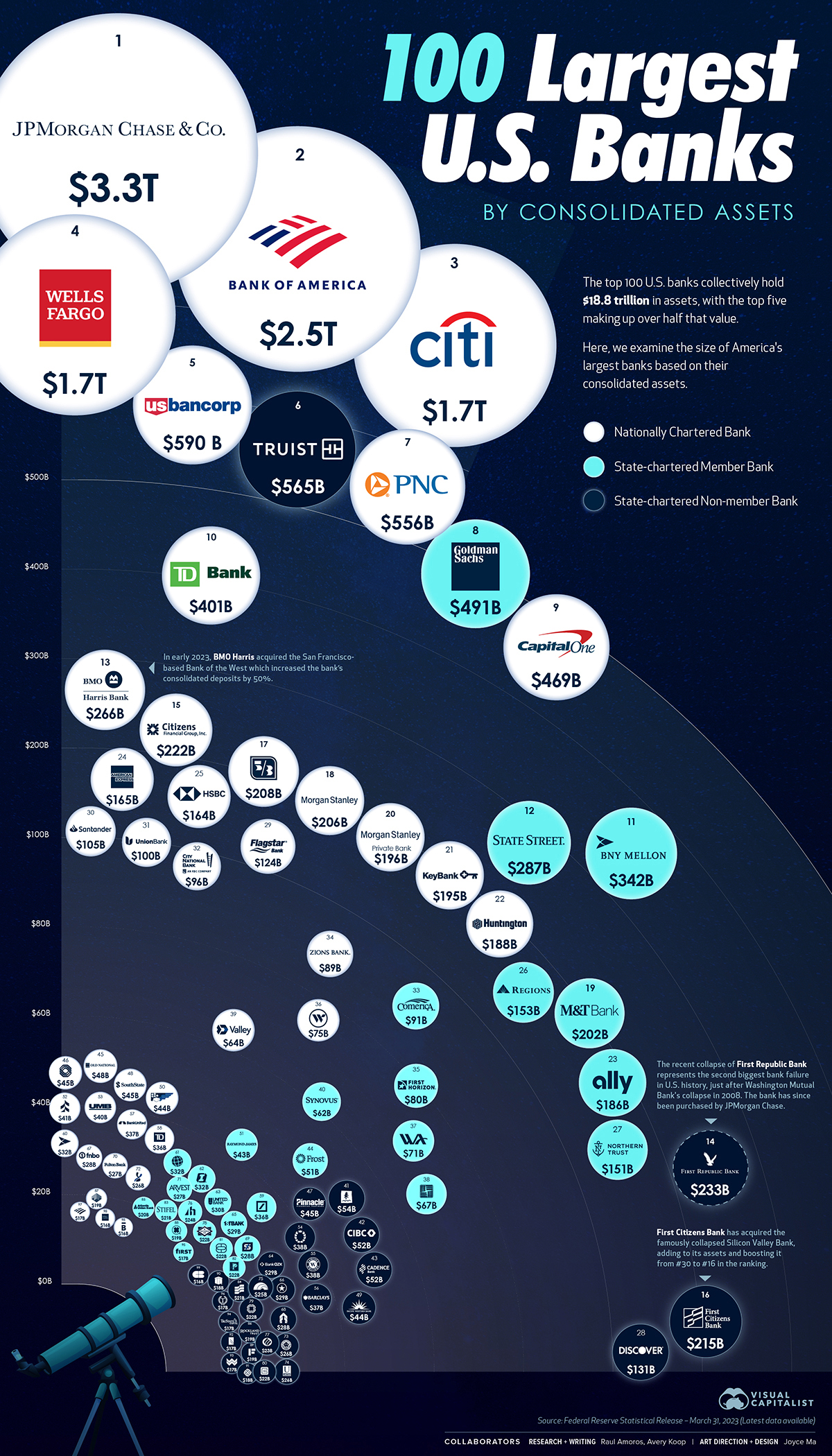

As of the latest available data (e.g., Q4 2023), the number of FDIC-insured institutions typically hovers around 4,600 to 4,700. This figure represents a dramatic decrease from the post-WWII peak of over 14,000 institutions in 1984. The trend has been one of continuous decline for decades, driven largely by mergers and acquisitions. However, this decline in numbers does not equate to a decline in financial services or assets. The aggregate assets held by these fewer institutions have grown exponentially, indicating a concentration of wealth and services into larger, more diversified entities. For instance, while there are fewer banks, the average bank size, measured by assets, has increased significantly. This means that larger banks are serving more customers and handling greater volumes of transactions than ever before.

The Role of Credit Unions

While not strictly “banks” in the FDIC-insured commercial sense, credit unions form a vital parallel financial system in the U.S. They offer similar services—checking accounts, savings accounts, loans, credit cards—but operate under a different legal and philosophical framework. As member-owned non-profits, their primary goal is to serve their members, often leading to lower fees and better interest rates on deposits and loans compared to commercial banks.

The National Credit Union Administration (NCUA) is the independent federal agency that charters and supervises federal credit unions and insures deposits up to $250,000 per member, per account. As of recent figures (e.g., late 2023/early 2024), there are typically around 4,600 to 4,700 federally and state-chartered credit unions in the U.S. This number has also seen a gradual decline over the years, though at a slower pace than commercial banks, largely due to mergers driven by economies of scale and the need to offer more competitive services. When combined, the total number of FDIC-insured banks and NCUA-insured credit unions is roughly double the count of just banks, providing a more complete picture of the U.S. depository institution landscape, numbering close to 9,000 to 10,000 institutions.

Why the Numbers Fluctuate: Drivers of Consolidation and Growth

The persistent decline in the number of traditional banks isn’t random; it’s the result of powerful economic, regulatory, and technological forces that continually reshape the industry.

Regulatory Pressures and Compliance Costs

Following the 2008 financial crisis, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 introduced sweeping regulatory changes aimed at preventing a recurrence. While necessary for financial stability, these regulations imposed significant compliance costs, particularly on smaller community banks. The burden of hiring compliance officers, investing in new reporting systems, and navigating complex rules disproportionately affected institutions with fewer resources. For many small banks, the cost of compliance became a powerful incentive to merge with larger institutions that could more easily absorb these overheads. This regulatory environment, while crucial for systemic safety, inadvertently accelerated consolidation, making it challenging for smaller players to remain independent and profitable.

Technological Advancements and Competition

The digital revolution has profoundly impacted banking. Consumers increasingly expect seamless online and mobile banking experiences, instant transactions, and personalized financial tools. Meeting these expectations requires substantial investment in technology infrastructure, cybersecurity, and skilled IT personnel. Fintech companies, unburdened by legacy systems, have been particularly agile in developing innovative digital solutions, from payment apps to robo-advisors. This technological arms race, coupled with heightened competition from fintechs and larger banks with deeper pockets, puts immense pressure on smaller banks to either innovate or merge. Many choose the latter, seeking scale to fund necessary tech upgrades and compete effectively in the digital age.

Economic Cycles and Market Dynamics

Economic booms and busts also play a significant role. During periods of economic growth, banks may expand, but also become attractive acquisition targets. During downturns, weaker institutions may face financial distress, making them vulnerable to takeover by stronger banks or even leading to failure. The low-interest-rate environment that persisted for many years post-2008 squeezed net interest margins, making it harder for banks, especially smaller ones heavily reliant on traditional lending, to generate sufficient profits. This pressure often pushed them towards consolidation as a strategy for efficiency and enhanced profitability. Market dynamics, including shareholder demands for growth and profitability, further fuel the merger and acquisition activity.

The Pursuit of Scale and Efficiency

Ultimately, a significant driver of consolidation is the pursuit of scale and efficiency. Larger banks can spread fixed costs (like technology, compliance, and marketing) over a larger asset base, leading to lower per-unit costs. They can also offer a broader range of specialized products and services, from complex derivatives for corporate clients to sophisticated wealth management for high-net-worth individuals, which smaller banks cannot. The ability to achieve economies of scale and scope allows larger institutions to be more competitive on pricing, invest more in innovation, and potentially offer greater returns to shareholders, making consolidation an attractive proposition for both acquiring and acquired entities.

The Impact of Banking Density on Consumers and Businesses

The changing number of banks isn’t just an abstract statistic; it has tangible implications for how individuals and businesses access financial services and for the overall health of local economies.

Access to Capital and Financial Services

A declining number of banks, particularly the disappearance of community banks, can sometimes lead to reduced access to capital and financial services in certain regions, especially rural or underserved areas. Community banks are often deeply embedded in their local economies, possessing intimate knowledge of local businesses and residents. This local expertise allows them to make more nuanced lending decisions, often providing credit to small businesses and individuals that larger, more centralized banks might overlook due to standardized underwriting criteria. When a local bank merges or closes, the vacuum it leaves can make it harder for local entrepreneurs to secure loans, hindering economic growth and job creation in those communities. While larger banks have extensive branch networks, their decision-making processes can be more centralized, potentially reducing responsiveness to highly localized needs.

Competition and Innovation

The balance between the number of banks and the level of competition is critical. A healthy banking sector requires robust competition to drive innovation, keep fees competitive, and ensure a wide range of product offerings. If consolidation leads to too few dominant players, there’s a risk of reduced competition, potentially resulting in higher fees, fewer choices for consumers, and less incentive for banks to innovate. Conversely, too many small, inefficient banks might struggle to invest in necessary technology or offer competitive services. The ideal scenario involves a diverse mix of large, mid-sized, and community banks, each playing a distinct role and fostering a dynamic competitive environment. This ensures that both sophisticated corporate clients and local small businesses have access to appropriate and affordable financial solutions.

The Role of Community Banks

Despite the overall trend of consolidation, community banks continue to play a crucial role in the U.S. financial system. Their unique value proposition lies in their deep community ties, relationship-based lending, and personalized customer service. They are often the primary source of financing for small businesses and agricultural ventures, acting as engines of local economic development. Many also cater specifically to underserved populations, fostering financial inclusion.

However, community banks face ongoing challenges, including the high cost of regulatory compliance, the need to invest in digital technologies to meet customer expectations, and intense competition from larger banks and fintechs. Policymakers and industry advocates recognize their importance and are exploring ways to support their continued viability, such as tailoring regulations to their specific business models and fostering innovation through partnerships. The resilience of community banking is a testament to the enduring value of localized, relationship-driven finance, even in an increasingly globalized and digital world.

The Future of U.S. Banking: Trends and Predictions

The trajectory of U.S. banking suggests continued evolution, with several key trends poised to shape the industry’s structure and the services it provides.

Continued Digital Transformation

The shift towards digital banking is irreversible. AI-powered analytics will enable more personalized financial advice and risk assessment. Blockchain technology could revolutionize payment systems and enhance security. Mobile banking apps will become even more sophisticated, offering integrated budgeting tools, investment platforms, and seamless access to credit. This digital imperative will continue to drive investments in technology, pushing banks towards greater efficiency and fostering collaboration with or acquisition of fintech innovators. Banks that fail to adapt will struggle to retain customers, particularly younger generations who prioritize digital convenience.

Regulatory Adaptations

Regulators are constantly grappling with how to oversee a rapidly evolving financial landscape. We can expect ongoing efforts to balance financial stability with fostering innovation. This might include:

- Tailored Regulation: Further refinement of regulations to distinguish between large, systemically important institutions and smaller community banks, easing the burden where appropriate.

- Fintech Oversight: Developing frameworks for regulating fintech companies and non-bank financial institutions that increasingly offer bank-like services, ensuring consumer protection without stifling innovation.

- Cybersecurity Focus: Heightened emphasis on cybersecurity regulations and resilience, as financial services become even more digitized and susceptible to cyber threats.

The regulatory environment will need to remain agile, adapting to new technologies and business models while maintaining the core objectives of safety and soundness.

The Rise of Niche Banking and Fintech Partnerships

While consolidation among traditional banks may continue, there’s also a growing trend towards niche banking and specialization. Fintech companies have demonstrated the power of focusing on specific financial needs or customer segments. This could lead to a future where traditional banks either acquire these niche players or partner with them to offer specialized services. We might see more “Banking-as-a-Service” (BaaS) models, where licensed banks provide the underlying infrastructure for fintechs to offer their branded financial products. This collaborative approach allows banks to leverage innovation without extensive in-house development and enables fintechs to operate within a regulated framework.

Balancing Scale with Local Needs

The ongoing challenge for the U.S. banking system will be to balance the economic advantages of scale with the critical need for localized service and access to capital. While large national banks offer convenience and a broad array of services, community banks remain essential for fostering local economies and supporting small businesses. The future likely holds a hybrid model, where technology allows larger banks to offer more personalized experiences, and community banks leverage technology to extend their reach and efficiency while maintaining their core relationship-based approach. The number of banks will continue to fluctuate, but the focus will increasingly be on how effectively the entire financial ecosystem serves the diverse needs of American consumers and businesses.

In conclusion, the question of “how many banks are in the US” reveals a story far richer than a simple count. It speaks to a dynamic industry shaped by history, driven by innovation, and critically vital to the nation’s economic health. While the raw number of traditional banks has decreased significantly, the financial services sector as a whole has become more diverse, efficient, and technologically advanced. Understanding these trends is crucial for anyone engaging with personal finance, investing, or navigating the broader business financial landscape, ensuring that the critical function of capital allocation and financial management continues to evolve responsibly and effectively.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.