In the realm of personal finance and wealth management, the ability to calculate and interpret percentages is perhaps the most fundamental skill an individual can possess. Whether you are evaluating a potential investment, determining your tax liability, or simply trying to stick to a monthly budget, percentages are the universal language of value. Understanding “how to get a percentage of something” is not merely a middle-school math requirement; it is a critical tool for navigating the complexities of the modern economy.

When we talk about money, we are rarely dealing with static numbers. We are dealing with growth, decay, ratios, and distributions. From the interest rate on a high-yield savings account to the percentage of your portfolio allocated to emerging markets, these figures dictate your financial trajectory. This guide explores the essential mechanics of percentage calculations through the lens of financial strategy, ensuring you have the quantitative foundation necessary to build lasting wealth.

The Fundamental Formula: Why Percentage Competency is Your Best Financial Asset

To master your money, you must first master the core equation of the percentage. At its simplest, a percentage represents a part of a whole, expressed as a fraction of 100. In financial terms, this allows us to compare different scales of value on a level playing field.

The Core Equation Explained

The basic formula to find the percentage of a total is:

** (Part / Whole) × 100 = Percentage **

For example, if you earned $1,200 in dividends this year from a $20,000 investment portfolio, you would divide 1,200 by 20,000 to get 0.06. Multiplying by 100 gives you 6%. In a financial context, this 6% represents your dividend yield. Understanding this simple division is the first step in auditing your financial health. It allows you to move away from looking at “dollars earned” in a vacuum and start looking at “efficiency of capital.”

Decimal Conversions and Financial Ratios

In professional finance, we often bypass the “multiplication by 100” step and work directly with decimals. A 7% interest rate is 0.07; a 25% tax bracket is 0.25. Converting percentages to decimals is essential when using financial tools or spreadsheets like Excel and Google Sheets.

If you want to find 15% of your $5,000 monthly income for a retirement contribution, the calculation is $5,000 × 0.15 = $750. Being able to toggle between percentages, decimals, and fractions allows a savvy investor to quickly scan a balance sheet and identify where their capital is flowing most effectively.

Percentages in Personal Finance: Budgeting and Savings Strategies

Budgeting is essentially an exercise in percentage allocation. Without a percentage-based framework, it is difficult to determine if your spending is sustainable as your income fluctuates.

The 50/30/20 Rule: Allocating Your Income

One of the most popular financial frameworks is the 50/30/20 rule. This strategy suggests that you should allocate your after-tax income into three distinct percentage buckets:

- 50% for Needs: Housing, utilities, groceries, and insurance.

- 30% for Wants: Dining out, hobbies, and travel.

- 20% for Financial Goals: Debt repayment, emergency funds, and retirement investments.

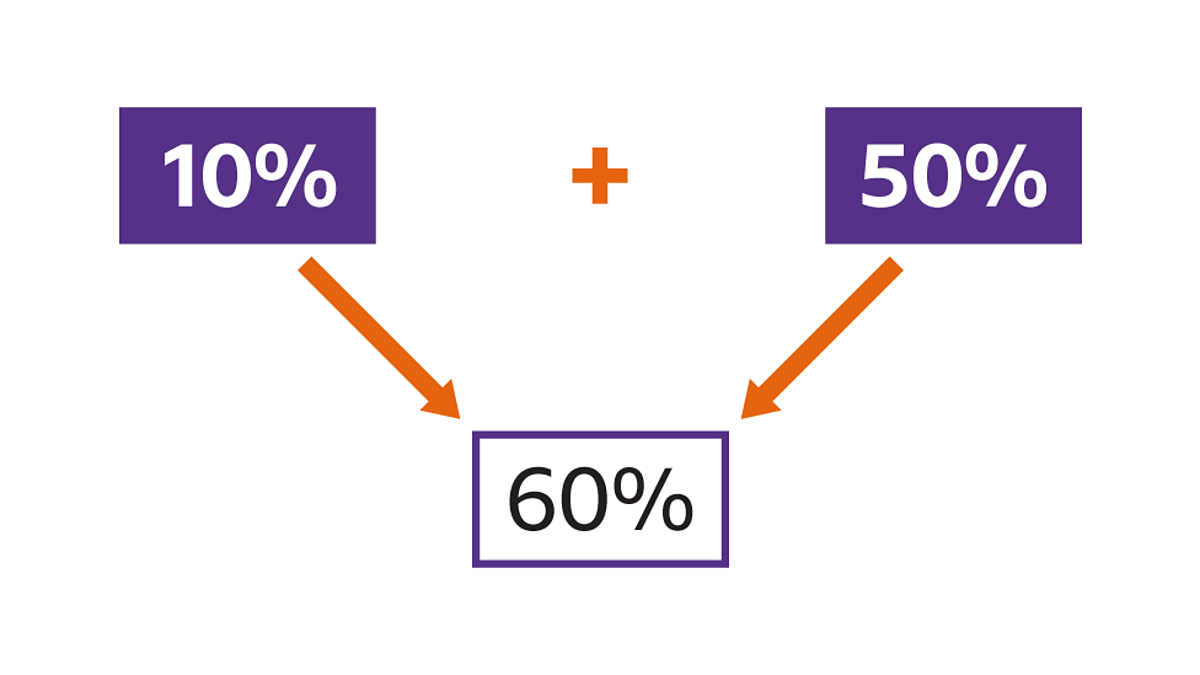

By calculating these percentages, you can identify “lifestyle creep.” If your income increases by 10% but your “Needs” bucket expands to consume 60% of your total income, your financial foundation is becoming less stable despite earning more money.

Calculating Interest Earned on Savings Accounts

When you see a bank advertising a 4.5% Annual Percentage Yield (APY), you are looking at the percentage of your balance that the bank will pay you over a year. To calculate how much you will earn in a single month, you divide the annual percentage by 12.

For instance, a $10,000 balance at 4.5% APY (0.045) would yield roughly $450 in a year. Understanding how to calculate this percentage allows you to compare different financial products—such as Certificates of Deposit (CDs) versus Money Market Accounts—to ensure your cash is working as hard as possible.

Investment Mathematics: ROI and Portfolio Allocation

In the world of investing, percentages are the primary metric for performance. Investors use them to determine if a risk was worth the reward and to ensure their assets are properly diversified.

Determining Return on Investment (ROI)

The most critical percentage for any investor is the Return on Investment (ROI). This tells you the percentage of profit or loss relative to the original amount invested. The formula is:

[(Current Value – Original Value) / Original Value] × 100 = ROI

If you bought a stock for $150 and it is now worth $180, your profit is $30. Dividing $30 by the original $150 gives you 0.20, or a 20% ROI. This percentage is vital because it allows you to compare the performance of a stock to a real estate investment or a bond, even if the dollar amounts are vastly different.

Asset Allocation and Diversification Percentages

A healthy investment portfolio is never concentrated in a single asset. Financial advisors often recommend a specific percentage split based on your age and risk tolerance, such as 70% equities and 30% fixed income.

To manage this, you must regularly calculate what percentage of your total wealth each asset class represents. If your stocks have a great year, they might grow to represent 85% of your portfolio. To “rebalance,” you would calculate the dollar amount needed to sell in stocks and move into bonds to return to your target 70/30 percentage split. This disciplined, math-based approach removes emotion from the investing process.

The Impact of Costs: Taxes, Inflation, and Interest Rates

While we focus on percentages that help us grow money, we must also calculate the percentages that take it away. Taxes, inflation, and interest on debt are the “silent” percentages that can erode wealth if left unmonitored.

Calculating Sales Tax and Income Tax Brackets

Taxes are almost always calculated as a percentage of a transaction or income. If you are in a 22% federal income tax bracket, it does not mean you pay 22% on every dollar (due to the progressive nature of the system), but it does mean that your marginal dollar is taxed at that percentage.

Understanding how to calculate the percentage of your paycheck that goes toward taxes is essential for accurate cash-flow forecasting. If you are a freelancer, you must manually set aside a percentage (often 25-30%) of every check to cover self-employment taxes. Failing to calculate this percentage accurately can lead to severe financial penalties.

Understanding APR and the Cost of Borrowing

The Annual Percentage Rate (APR) represents the cost of borrowing money. Whether it is a 19% APR on a credit card or a 7% interest rate on a mortgage, this percentage determines the total cost of the item you are purchasing.

To see the impact, consider a $1,000 balance on a credit card with a 20% APR. If you only pay the minimum, you aren’t just paying back the $1,000; you are paying a percentage of that balance in interest every month. Calculating the “percentage cost of debt” helps you prioritize which loans to pay off first—always target the highest percentage rates first, as they are the most expensive “anti-investments.”

Advanced Financial Forecasting: Compound Growth and Changes

To truly excel in money management, one must understand how percentages behave over time and how they differ from “percentage points.”

Compound Interest: The Percentage That Builds Wealth

Compound interest is often called the eighth wonder of the world. It is the process where the percentage of interest you earn is added back to your principal, so you earn a percentage on your previous interest in the next period.

While the basic percentage formula is linear, compound interest is exponential. Using the “Rule of 72” is a quick way to use percentages to forecast wealth: divide 72 by your expected annual percentage return to see how many years it will take for your money to double. At a 7% return, your money doubles roughly every 10 years (72 / 7 ≈ 10.2).

Percentage Change vs. Percentage Points

A common mistake in financial reporting is confusing a “percentage change” with “percentage points.” If a central bank raises interest rates from 3% to 4%, that is a 1 percentage point increase. However, in terms of the cost of interest, it is a 33.3% increase (1 divided by 3).

In the world of business finance, these distinctions are crucial. If your profit margin drops from 10% to 8%, you haven’t just lost 2%; you have experienced a 20% decrease in profit efficiency. Being precise with these calculations allows for more accurate business analysis and personal financial pivoting.

Conclusion: The Strategic Value of Financial Numeracy

Mastering “how to get a percentage of something” is the cornerstone of financial literacy. It transforms numbers from abstract figures into actionable insights. By applying these formulas to your budget, your investments, and your debts, you gain a level of control over your financial future that “guesswork” can never provide.

In the pursuit of wealth, percentages provide the map and the compass. They tell you where you are (allocation), how fast you are moving (ROI and growth), and what obstacles are in your way (taxes and inflation). By consistently applying these mathematical principles, you move beyond simple accounting and into the realm of strategic wealth building. Whether you are calculating a 15% tip or a 7% compounded retirement projection, you are using the most powerful tool in the financial kit: the ability to see the world in ratios and realize the true value of every dollar.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.