The landscape of personal finance has undergone a radical transformation over the last decade, shifting from the tactile exchange of physical currency to the seamless, instantaneous world of digital ledgers. At the forefront of this revolution is Cash App, a financial service platform developed by Block, Inc. that has redefined how individuals manage, send, and receive capital. While the core functionality of the app is centered on peer-to-peer (P2P) transfers, it has evolved into a multi-faceted financial tool that bridges the gap between traditional banking and the burgeoning digital economy.

Understanding how to send money via Cash App is no longer just a technical convenience; it is a fundamental skill in modern financial literacy. Whether you are splitting a dinner bill, paying a freelance contractor, or managing a side hustle, the platform offers a streamlined pipeline for liquidity. This guide explores the financial mechanics of Cash App, the protocols for secure transfers, and how to integrate this tool into your broader personal finance strategy.

The Foundations of Your Digital Wallet: Setup and Configuration

Before executing a single transaction, it is essential to understand the financial architecture of Cash App. Unlike a traditional bank account that requires physical documentation and lengthy approval processes, Cash App operates on a “mobile-first” philosophy, prioritizing speed and accessibility. However, the effectiveness of the tool depends heavily on how you configure your source of funds.

Establishing the Link: Debit Cards vs. Credit Cards

The first step in sending money is connecting a funding source. In the realm of personal finance, the choice between a debit card and a credit card is significant. Cash App allows you to link a traditional bank account via a debit card for seamless, no-fee transfers. Conversely, using a credit card to send money typically incurs a 3% transaction fee. From a financial management perspective, utilizing a debit link is almost always preferable to avoid unnecessary overhead and the potential for high-interest debt accumulation.

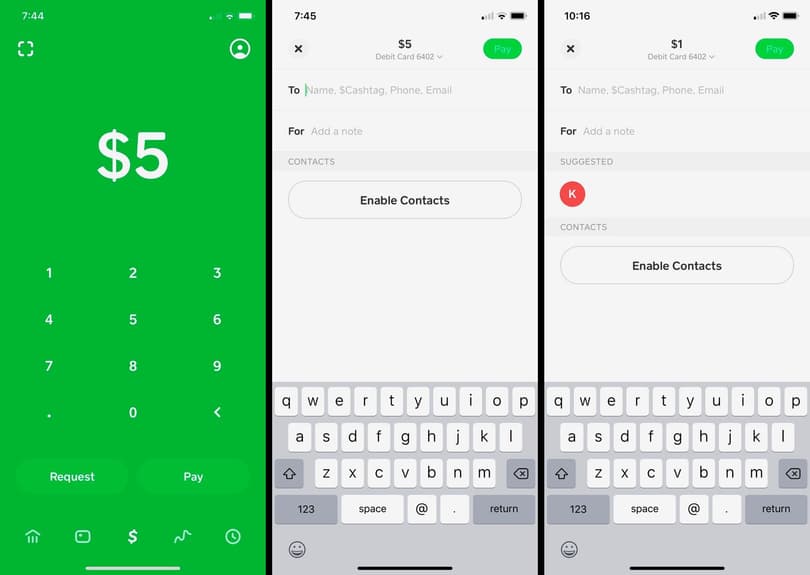

The $Cashtag: Your Unique Financial Identity

A defining feature of Cash App is the $Cashtag—a unique username that acts as a digital routing address. In the context of financial security and privacy, the $Cashtag allows users to receive funds without disclosing sensitive information like bank account numbers or phone digits. When setting up your profile, choosing a professional and recognizable $Cashtag is vital, especially if you intend to use the platform for business transactions or professional reimbursements.

Verification and Transaction Limits

For the casual user, Cash App imposes initial limits on how much can be sent or received. To unlock the full potential of the platform, users must undergo a verification process, which typically involves providing a full legal name, the last four digits of a Social Security Number, and a date of birth. From a personal finance standpoint, this verification is a crucial step in anti-money laundering (AML) compliance and “Know Your Customer” (KYC) regulations, ensuring that your capital remains within a regulated and protected ecosystem.

Executing the Transfer: Precision and Liquidity

The primary utility of Cash App is the “Send” function. While the interface is designed for simplicity, the financial implications of each tap are permanent. Navigating the mechanics of a transfer requires a blend of technical accuracy and financial mindfulness.

The Step-by-Step Sending Process

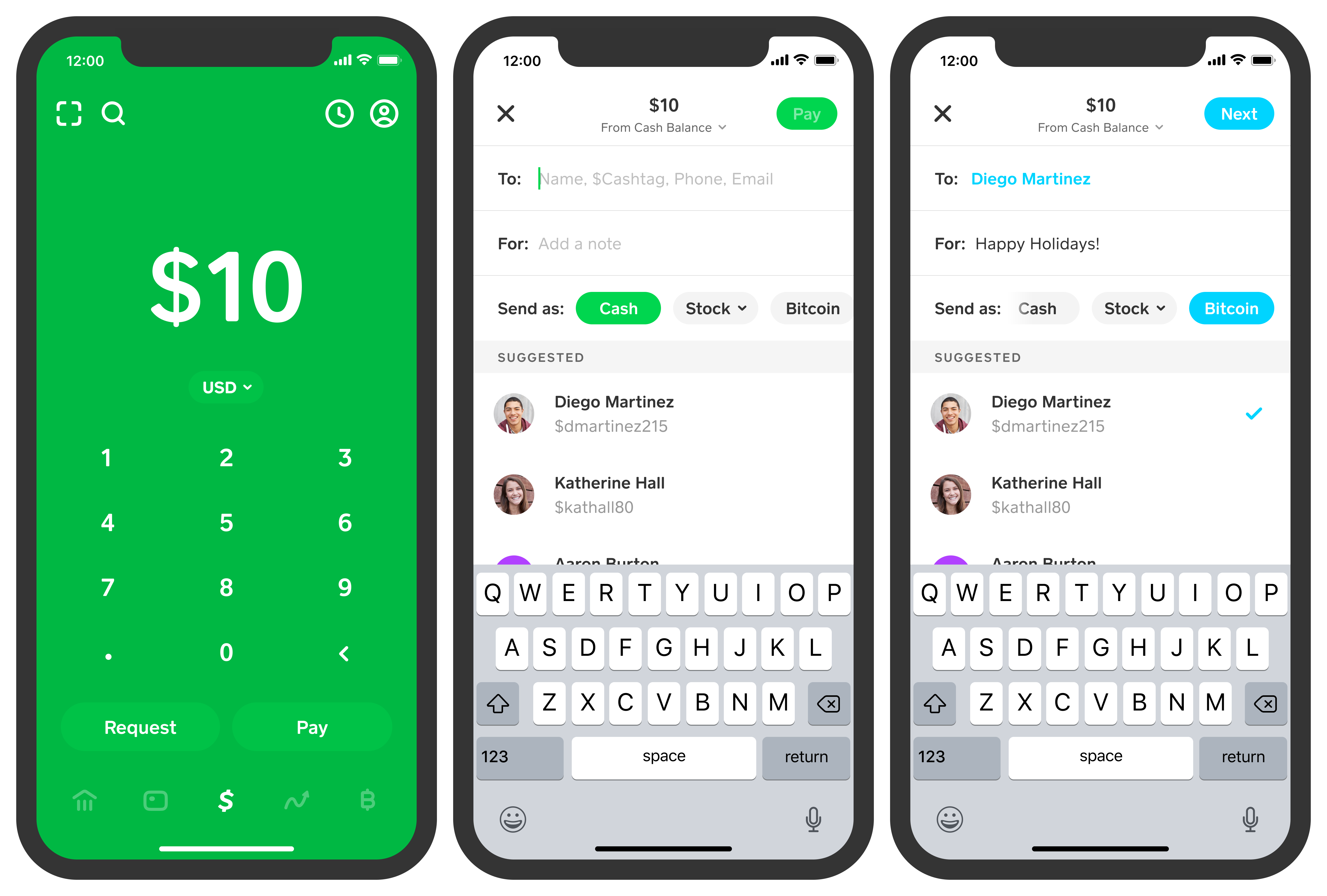

To initiate a transfer, the user enters the desired amount on the app’s main keypad and taps “Pay.” The next screen requires the recipient’s $Cashtag, email, or phone number. A critical best practice in digital finance is the “Double-Check Rule.” Because P2P transfers are often instantaneous and difficult to reverse, verifying the recipient’s identity before hitting “Pay” is the most effective way to prevent capital loss.

Instant vs. Standard Deposits: Managing Cash Flow

When you receive money or move funds from your Cash App balance back to your bank account, you are presented with two options: Standard and Instant.

- Standard Transfers are free and typically take 1–3 business days. This is the recommended route for non-urgent financial planning.

- Instant Deposits carry a small percentage fee (usually 0.5% to 1.75%) but provide immediate liquidity.

For those focusing on wealth preservation, minimizing these small convenience fees is a disciplined habit that prevents “death by a thousand cuts” to your net worth.

Handling Payment Disputes and Mistakes

One of the most misunderstood aspects of digital financial tools is the “chargeback” or refund process. Unlike credit card transactions, which offer robust consumer protections, Cash App payments are generally considered “cash-like.” If you send money to the wrong person, your primary recourse is to “Request” the money back. Understanding this lack of a safety net is vital for any user; it emphasizes the need for high-level diligence during the transaction process.

Expanding the Portfolio: Investing and Wealth Building

Cash App has transcended its origins as a simple payment app to become a micro-investing platform. For many, it serves as the entry point into the world of equities and digital assets, allowing for the fractionalization of wealth building.

Fractional Shares and the Equities Market

The app allows users to purchase fractional shares of publicly traded companies with as little as $1. This is a powerful tool for personal finance, as it lowers the barrier to entry for the stock market. Instead of needing hundreds of dollars to buy a single share of a high-priced tech stock, a user can invest small amounts of their “leftover” cash balance, facilitating a strategy known as dollar-cost averaging.

Bitcoin Integration and Digital Assets

Cash App was one of the first major P2P platforms to fully integrate Bitcoin. Users can buy, sell, and even “get paid in Bitcoin” by automatically converting a percentage of their direct deposits. While the volatility of digital assets requires a high risk tolerance, the ease of sending Bitcoin directly to other wallets makes Cash App a functional bridge between traditional fiat currency and the decentralized finance (DeFi) space.

The Cash Card and “Boosts”

The Cash Card is a customizable Visa debit card linked directly to your Cash App balance. From a budgeting perspective, the “Boost” feature is particularly intriguing. Boosts allow users to select specific merchants (e.g., grocery stores or coffee shops) and receive instant discounts or Bitcoin back on purchases. In an era of high inflation, leveraging these micro-savings tools is a strategic way to reduce daily expenses and increase discretionary income.

Security Protocols and Financial Integrity

As with any platform that handles liquid assets, security is the most critical component. Protecting your digital wallet is synonymous with protecting your physical bank account.

Implementing Multi-Factor Authentication

To safeguard your funds, Cash App provides several layers of security. Enabling the “Security Lock” feature—which requires a PIN, Touch ID, or Face ID for every transaction—is non-negotiable for anyone serious about their financial security. This prevents unauthorized transfers in the event that your mobile device is compromised.

Recognizing Scams and Phishing

The rise of P2P apps has unfortunately led to a rise in sophisticated financial scams. Common tactics include “Cash App Fridays” giveaways that ask for a small “verification fee” or “support” accounts that ask for your sign-in code. A golden rule in personal finance applies here: if an offer seems too good to be true, it is. Official Cash App representatives will never ask for your PIN or sign-in code, and they will never ask you to send them money for “test” purposes.

Tax Implications and Documentation

For those using Cash App for side hustles or business transactions, it is important to be aware of IRS regulations. Currently, the threshold for reporting third-party network transactions is subject to evolving tax laws. Keeping meticulous records of your “Business” vs. “Personal” payments within the app is essential for accurate tax filing. Cash App provides monthly statements and a yearly tax document for those who use the platform for investing, ensuring that your financial activities remain transparent and compliant with federal regulations.

Conclusion: The Role of Cash App in a Modern Financial Strategy

The ability to send money through Cash App is more than a technical convenience; it is a manifestation of the “velocity of money” in the 21st century. By reducing the friction between earning, spending, and investing, Cash App has democratized access to financial services that were once reserved for those with traditional banking relationships.

However, the ease of use should not be mistaken for a lack of consequence. Effective personal finance requires a disciplined approach to every transaction, a keen eye for security, and a strategic understanding of how tools like fractional investing and instant liquidity fit into your long-term goals. Whether you are using it to pay a friend back for lunch or as a vehicle for your first foray into the stock market, mastering Cash App is a vital step toward achieving digital financial fluency. In the modern economy, your smartphone is your wallet, your bank, and your broker—managing it with professional rigor is the key to financial stability.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.