For many Americans, Social Security represents the bedrock of their retirement strategy. Yet, despite its importance, the actual mechanism behind how the Social Security Administration (SSA) determines your monthly check remains a mystery to most. It is often viewed as a “black box” where work history goes in and a check comes out. However, the calculation is a precise, transparent mathematical process designed to replace a portion of your pre-retirement income.

Understanding this formula is not just an academic exercise; it is a critical component of personal financial planning. By deconstructing the variables—from your highest-earning years to the age at which you choose to file—you can make informed decisions that could potentially result in hundreds of thousands of dollars in additional lifetime income.

The Foundation: Your Earnings History and the 35-Year Rule

The calculation of your Social Security benefit begins with your lifetime earnings. Unlike some private pension plans that might only look at your final five years of salary, the SSA takes a much broader view of your career.

The Importance of the 35-Year Average

To calculate your benefit, the SSA looks at your entire work history and selects the 35 years in which you earned the most. These years do not need to be consecutive. If you worked for 40 years, the five lowest-earning years are simply dropped from the calculation. However, if you have fewer than 35 years of covered earnings, the SSA will fill in the remaining years with zeros. These zeros can significantly drag down your average, which is why financial advisors often recommend working at least 35 years to maximize your base benefit.

Wage Indexing: Adjusting for Inflation

A common misconception is that the SSA uses the raw dollar amounts from your past paychecks. In reality, the SSA uses “wage indexing” to ensure that your past earnings are viewed in the context of today’s economy. This process adjusts your historical earnings to account for the general increase in wages that has occurred over your career. For example, the money you earned in 1985 is multiplied by an indexing factor to make it comparable to the value of a dollar today. Earnings are indexed up to the year you turn 60; earnings after age 60 are used at their actual value.

The Social Security Wage Base Cap

It is also important to note that Social Security only counts earnings up to a certain limit each year, known as the “Contribution and Benefit Base.” Earnings above this cap are not subject to Social Security taxes, and consequently, they are not factored into your benefit calculation. For high earners, this means that their benefit is “capped,” regardless of how much their total compensation exceeds the annual limit.

From Earnings to AIME: Calculating Your Base Average

Once your top 35 years of earnings are indexed and identified, the SSA moves to the next phase: determining your Average Indexed Monthly Earnings (AIME). This figure represents the monthly average of your career earnings after adjusting for inflation.

Calculating the AIME

The math is relatively straightforward: the SSA sums the indexed earnings from your top 35 years and divides that total by 420 (the number of months in 35 years). The resulting number is your AIME. This figure serves as the raw material for the actual benefit formula. If your AIME is high, your potential benefit is higher, but the relationship is not strictly linear due to the progressive nature of the program.

The Progressive Nature of the Formula

The Social Security benefit formula is intentionally designed to be “weighted” or progressive. This means it replaces a higher percentage of pre-retirement income for lower-wage earners than it does for higher-wage earners. This is achieved through a mechanism known as “bend points.”

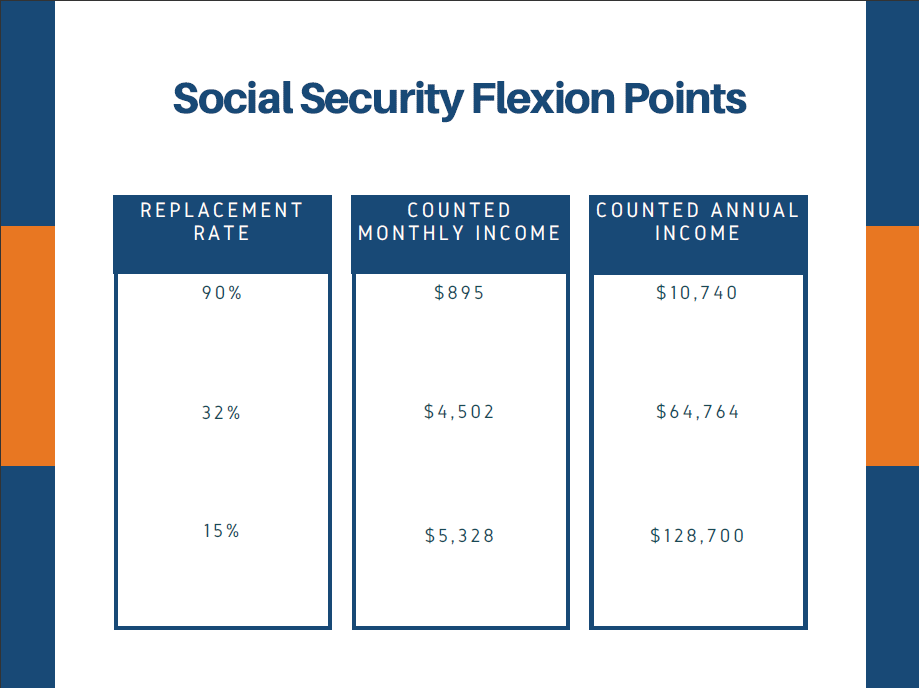

Understanding “Bend Points” and the PIA

The Primary Insurance Amount (PIA) is the actual dollar amount you are entitled to receive if you claim benefits at your Full Retirement Age (FRA). To get from the AIME to the PIA, the SSA applies three different percentages to your monthly average. For a worker reaching age 62 in 2024, the formula is:

- 90% of the first $1,174 of AIME.

- 32% of AIME between $1,174 and $7,078.

- 15% of AIME over $7,078.

These dollar thresholds ($1,174 and $7,078) are the “bend points.” Because the highest percentage (90%) applies only to the first segment of your earnings, the program provides a robust safety net for those with modest career earnings while still providing a larger (though proportionally lower) check for those who paid more into the system.

The Impact of Timing: When You Claim Matters

While the PIA defines your “base” benefit, the age at which you actually apply for benefits can drastically alter the amount you receive every month. This is arguably the most important decision a retiree can make within the realm of personal finance.

Full Retirement Age (FRA)

Your Full Retirement Age is the age at which you are entitled to 100% of your PIA. For anyone born in 1960 or later, the FRA is 67. If you were born earlier, your FRA may be 66 or a few months past 66. Claiming exactly at your FRA ensures you receive exactly what the formula calculated based on your 35-year history.

The Penalty for Early Filing

You can choose to start receiving Social Security benefits as early as age 62. However, doing so results in a permanent reduction of your monthly check. This reduction is roughly 6.67% per year for the first three years before your FRA, and 5% for each year before that. If your FRA is 67 and you claim at 62, your monthly benefit will be reduced by 30%. This is a significant “haircut” that persists for the rest of your life.

Delayed Retirement Credits: The Reward for Waiting

Conversely, if you delay claiming benefits past your FRA, your benefit will increase by 8% for every year you wait, up to age 70. There is no benefit to waiting past age 70. For someone with an FRA of 67 who waits until 70, their benefit will be 124% of their PIA. In a low-yield investment environment, a guaranteed 8% annual increase is an incredibly powerful financial tool that is difficult to replicate in the private market.

External Factors and Post-Calculation Adjustments

Even after your initial benefit is calculated and your claiming age is factored in, several external variables can influence the net amount deposited into your bank account.

Cost-of-Living Adjustments (COLA)

Social Security is one of the few sources of retirement income that is protected against inflation. Every year, the SSA evaluates the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). If inflation has occurred, benefits are increased via a Cost-of-Living Adjustment (COLA). This ensures that the purchasing power of your benefit does not erode as the price of goods and services rises over your retirement years.

The Impact of Taxes and Medicare

For many retirees, the “gross” Social Security benefit is not the “net” amount they receive. If your “provisional income” (your adjusted gross income plus non-taxable interest plus half of your Social Security benefits) exceeds certain thresholds, up to 85% of your Social Security benefits may be subject to federal income tax. Additionally, if you are enrolled in Medicare Part B, the premiums are typically deducted directly from your Social Security check, reducing the take-home amount.

The Windfall Elimination Provision (WEP)

A final crucial factor in benefit calculation applies to those who have worked in jobs where they did not pay Social Security taxes, such as certain government positions or work in foreign countries. The Windfall Elimination Provision (WEP) can modify the 90% bend point in the PIA formula, potentially reducing the benefit. This is designed to prevent workers who receive a pension from non-covered work from also receiving the “weighted” advantage intended for low-wage earners.

Conclusion: Strategic Planning for Maximum Benefits

Calculating your Social Security benefit is a multi-step process that rewards longevity, consistency, and patience. It begins with a 35-year look-back at your earnings, moves through an inflation-adjusted averaging process, and is finally shaped by the age at which you choose to enter the system.

From a financial planning perspective, the complexity of the formula highlights the importance of staying informed. Whether it is deciding to work one more year to replace a “zero” in your 35-year history or choosing to delay benefits until age 70 to lock in the 8% annual credits, small changes in your strategy can lead to significant shifts in your financial security. By understanding how the gears of the Social Security machine turn, you can move from passive recipient to active strategist, ensuring you maximize this vital component of your wealth.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.