In the world of finance, percentages are the universal language. Whether you are tracking the growth of a retirement account, evaluating the success of a marketing campaign’s ROI, or determining how much of your monthly income should go toward rent, the “percentage” is the most critical unit of measurement. Understanding how to derive these figures is not merely a mathematical exercise; it is a fundamental skill for achieving financial literacy and long-term stability.

While the basic formula for a percentage is taught in primary school, its applications in personal and business finance are multifaceted and often misunderstood. To “get the percentage” in a financial context means to gain clarity on your progress, your risks, and your opportunities. This guide explores the essential calculations every investor, entrepreneur, and saver must master to navigate the complexities of the modern economy.

The Foundation: Understanding Core Financial Percentages

Before diving into complex investment portfolios, one must master the basic mechanics of percentage calculations as they apply to daily money management. At its simplest, a percentage represents a fraction of 100, providing a standardized way to compare values of different scales.

The Basic Formula for Financial Comparison

To find the percentage of a specific financial figure, the formula is:

(Part / Whole) x 100 = Percentage

For example, if you save $500 out of a $4,000 monthly salary, you divide 500 by 4,000 to get 0.125. Multiplying by 100 gives you 12.5%. This simple calculation is the bedrock of budgeting. It allows you to move away from looking at “dollars spent” to “proportion of resources used,” which is a far more effective way to measure financial health across different income levels.

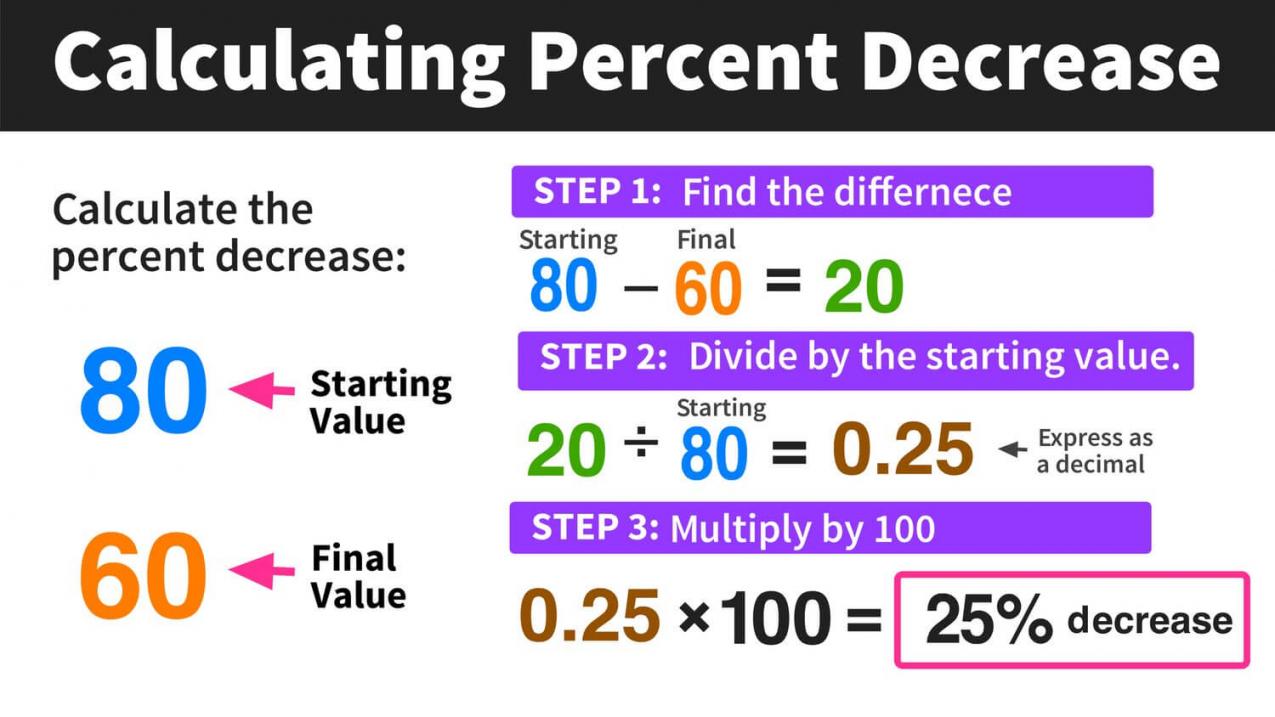

Calculating Percentage Increase and Decrease

In the markets, prices are rarely stagnant. Knowing how to calculate the percentage change is vital for tracking stock performance or inflation. The formula is:

[(New Value – Old Value) / Old Value] x 100 = Percentage Change

If a stock you purchased for $150 rises to $180, the increase is $30. Dividing $30 by the original $150 gives you 0.20, or a 20% gain. Conversely, understanding percentage decrease is crucial for risk management. A 50% loss on an investment requires a 100% gain just to break even—a mathematical reality that emphasizes the importance of protecting your downside.

Maximizing Your Returns: Percentages in Investing

For investors, percentages are the primary metric for performance. Raw dollar gains are deceptive because they do not account for the size of the initial outlay. A $1,000 profit is impressive on a $2,000 investment (50%), but negligible on a $1,000,000 investment (0.1%).

Calculating Return on Investment (ROI)

ROI is the gold standard for evaluating the efficiency of an investment. It is calculated by taking the net profit of the investment, dividing it by the cost of the investment, and multiplying by 100. This percentage allows you to compare disparate asset classes. By calculating the ROI, an investor can determine if a rental property yielding 8% annually is a better use of capital than a dividend-paying stock yielding 4%.

The Power of Compound Interest and the Rule of 72

Compound interest is often described as the eighth wonder of the world. It is the process where the percentage gain of one period is added to the principal, and the next period’s percentage gain is calculated based on that new, larger total.

To quickly estimate the impact of compound interest, savvy investors use the “Rule of 72.” By dividing 72 by your annual fixed percentage rate of return, you can determine roughly how many years it will take for your money to double. For instance, at a 6% return, your investment will double in approximately 12 years (72 / 6 = 12). Understanding this percentage-based shortcut is essential for long-term retirement planning and setting realistic financial goals.

Portfolio Allocation Percentages

Asset allocation is the practice of dividing an investment portfolio among different asset categories, such as stocks, bonds, and cash. Financial advisors often recommend a percentage-based approach, such as the “60/40” rule (60% stocks, 40% bonds). As the market fluctuates, these percentages will shift. “Rebalancing” a portfolio is the act of selling or buying assets to return to these original percentages, ensuring that your risk profile remains consistent with your financial objectives.

Managing Your Expenses: The Percentage-Based Budgeting Approach

Effective money management is less about how much you make and more about the percentages you keep. Using percentage-based budgeting allows your financial plan to scale automatically as your income rises or falls.

The 50/30/20 Rule

One of the most popular frameworks in personal finance is the 50/30/20 rule. This strategy suggests allocating your after-tax income into three percentage-based buckets:

- 50% to Needs: This includes essential costs like housing, groceries, utilities, and insurance.

- 30% to Wants: This covers discretionary spending, such as dining out, hobbies, and travel.

- 20% to Savings and Debt Repayment: This critical portion goes toward building an emergency fund, investing for retirement, or paying down high-interest debt.

By focusing on these percentages rather than fixed dollar amounts, you maintain a balanced lifestyle. If you receive a raise, the dollar amount in each category increases, but the proportion remains stable, preventing “lifestyle creep.”

Understanding Your Debt-to-Income Ratio (DTI)

When you apply for a mortgage or a car loan, lenders don’t just look at your salary; they look at your Debt-to-Income ratio. This is the percentage of your gross monthly income that goes toward paying debts. The formula is:

(Total Monthly Debt Payments / Gross Monthly Income) x 100 = DTI %

Lenders generally look for a DTI of 36% or less. If your DTI is too high, it signals to financial institutions that you are overleveraged. Knowing how to calculate this percentage yourself allows you to take corrective action—either by increasing income or paying down principal—before applying for major credit.

Business Finance: Margin vs. Markup

For entrepreneurs and business owners, the distinction between “margin” and “markup” is a frequent source of confusion, yet getting the percentage right is the difference between a profitable venture and bankruptcy.

Calculating Gross Profit Margin

Margin is calculated based on the selling price. It represents what percentage of each dollar of revenue is kept as profit after accounting for the Cost of Goods Sold (COGS).

Margin % = [(Revenue – COGS) / Revenue] x 100

If you sell a product for $100 and it costs $70 to produce, your profit is $30. Your margin is 30%. This percentage is vital because it tells you how much “room” you have to cover operating expenses like rent, marketing, and payroll.

Understanding Markup for Pricing Strategy

Markup, while related, is calculated based on the cost of the product. It represents how much you add to the cost to arrive at a selling price.

Markup % = [(Selling Price – COGS) / COGS] x 100

Using the same example (Cost $70, Sale $100), the markup is ($30 / $70) x 100, which equals approximately 42.9%. Business owners often make the mistake of wanting a 30% profit and applying a 30% markup, only to realize their actual margin is much lower (approx 23%). Understanding the math of these percentages ensures that pricing strategies are sustainable and profitable.

The Impact of Inflation and Real Returns

In finance, not all percentages are created equal. One of the most insidious threats to wealth is inflation—the percentage at which the general level of prices for goods and services rises.

Real vs. Nominal Returns

To understand the true growth of your money, you must distinguish between the “nominal” percentage return and the “real” percentage return. The nominal return is the percentage increase in your investment before adjusting for inflation. The real return is what remains after inflation is subtracted.

Real Return ≈ Nominal Return – Inflation Rate

If your savings account offers a 4% interest rate (nominal), but inflation is running at 5%, your “real” return is actually -1%. In this scenario, even though your balance is increasing in dollar terms, your purchasing power is decreasing. “Getting the percentage” in this context means looking beyond the surface-level numbers to understand the economic reality of your wealth.

Conclusion: The Strategic Value of the Percentage

Mastering the percentage is more than a mathematical necessity; it is a strategic advantage. Whether you are calculating the interest on a loan, the yield of a bond, or the efficiency of a business operation, the ability to derive and interpret these figures allows for objective decision-making.

In personal finance, percentages strip away the emotional weight of large numbers and provide a clear roadmap for budgeting and growth. In the world of investing, they provide a standardized metric for risk and reward. By consistently asking, “What is the percentage?” you move from being a passive observer of your finances to an active, informed manager of your economic future. Clarity in calculation leads to confidence in capital, and in the high-stakes world of money, confidence is the most valuable asset of all.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.