For millions of Americans, the question “What is my Social Security payment?” is more than just a matter of curiosity—it is a fundamental pillar of retirement planning. Social Security was designed to provide a foundation of income for workers and their families upon retirement, disability, or death. However, the system is notoriously complex, governed by a labyrinth of formulas, age requirements, and legislative adjustments. To truly understand what your payment will be, you must look beyond the monthly check and understand the mechanics of how the Social Security Administration (SSA) evaluates your lifetime of work.

This guide explores the intricate details of Social Security payments, from the initial calculation of your earnings to the strategic decisions that can significantly increase your monthly take-home pay.

The Mechanics of the Calculation: How Your Benefit is Determined

Your Social Security payment is not a flat rate, nor is it based solely on your most recent salary. Instead, it is a reflection of your entire career’s earnings, adjusted for inflation. The SSA uses a specific multi-step process to arrive at your Primary Insurance Amount (PIA).

Average Indexed Monthly Earnings (AIME)

The first step in determining your payment is calculating your Average Indexed Monthly Earnings (AIME). The SSA looks at your highest 35 years of earnings. If you worked more than 35 years, they take the top 35. If you worked fewer, the remaining years are averaged as zeros, which can significantly lower your potential payment. These earnings are “indexed” to account for changes in average wages since the year the earnings were received, ensuring that your $20,000 salary from 1985 is weighted appropriately against today’s economic standards.

The Primary Insurance Amount (PIA) and “Bend Points”

Once your AIME is established, the SSA applies a formula to determine your Primary Insurance Amount. This formula is progressive, meaning it is designed to provide a higher percentage of replacement income for lower-wage earners than for higher-wage earners. This is achieved through “bend points”—fixed dollar amounts that change annually.

For example, the formula might take 90% of the first portion of your AIME, 32% of the middle portion, and 15% of the amount above the second bend point. This tiered structure ensures a social safety net while still rewarding those who contributed more into the system through payroll taxes.

The Impact of Full Retirement Age (FRA)

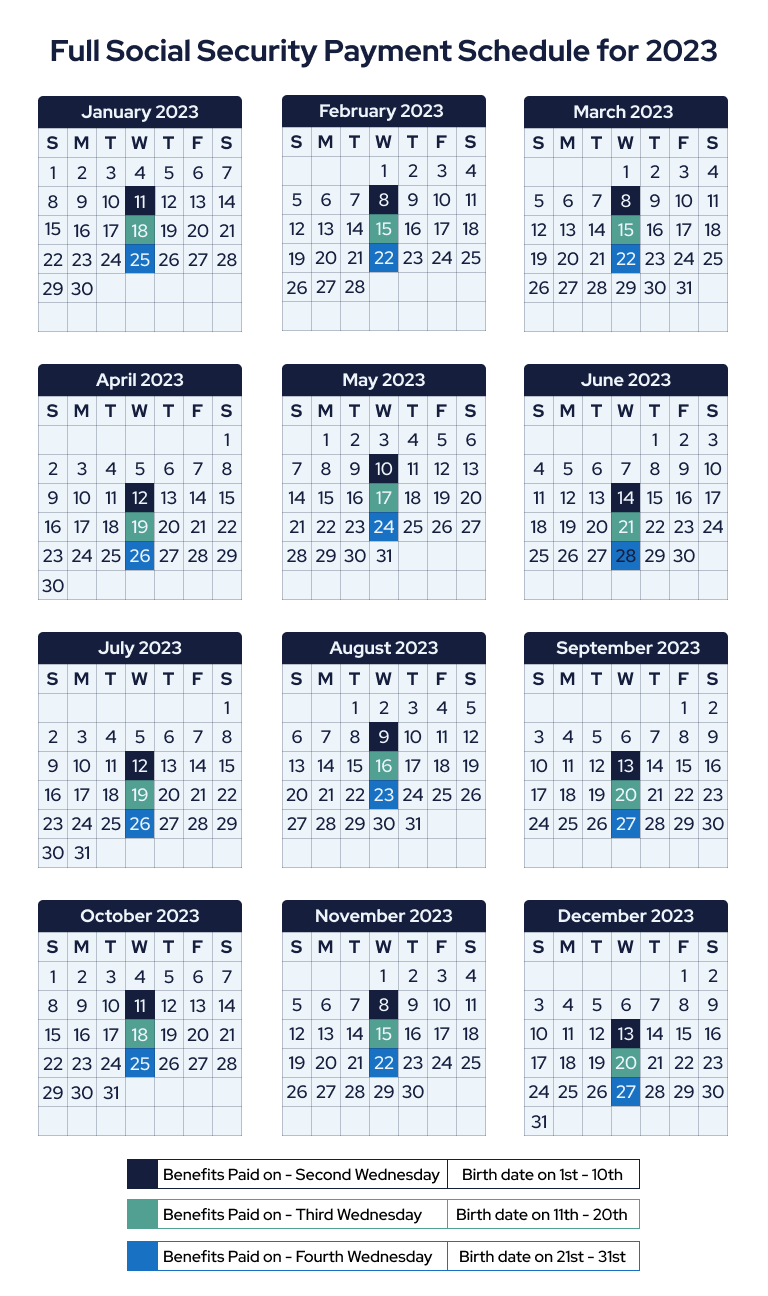

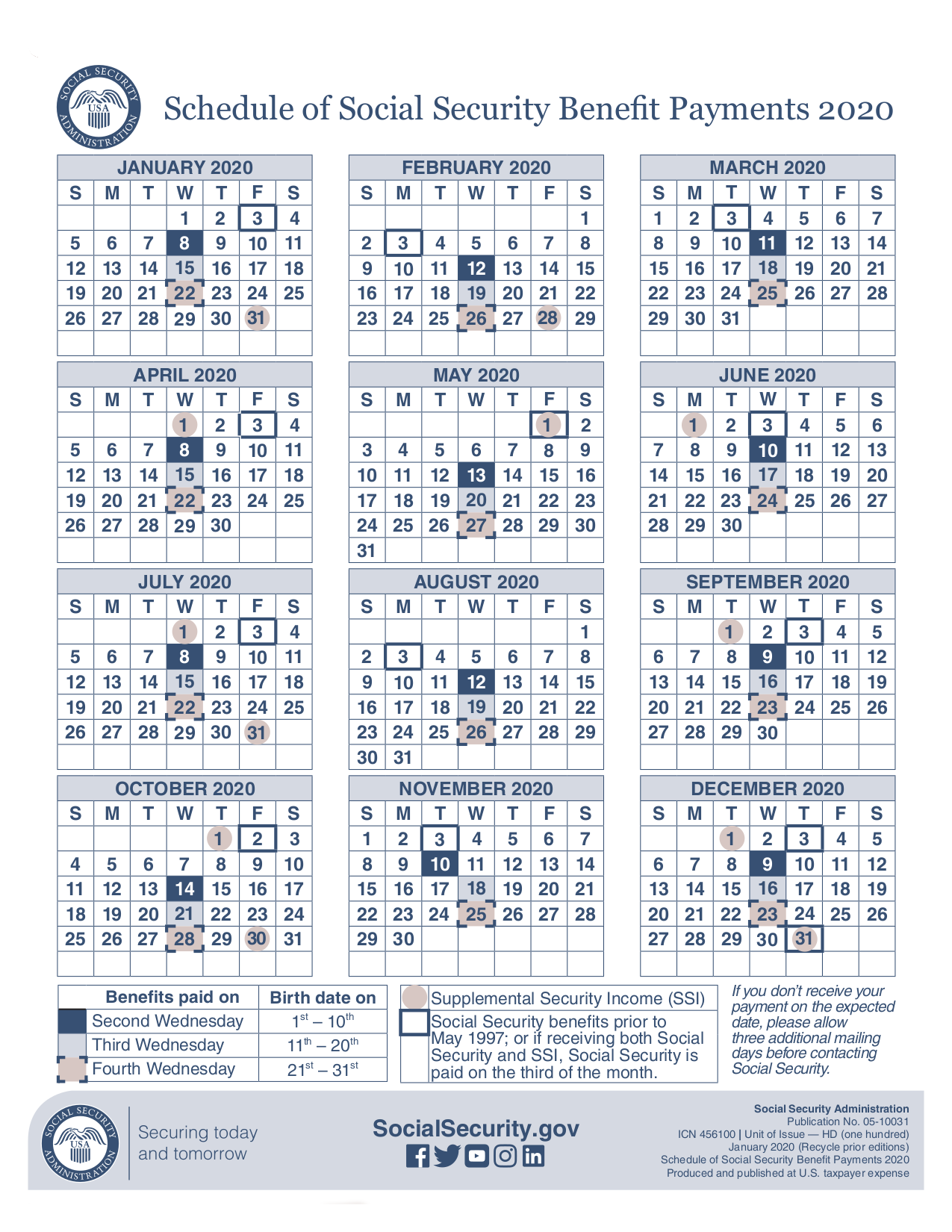

Your PIA is the amount you receive if you wait until your Full Retirement Age (FRA) to claim. For those born between 1943 and 1954, the FRA is 66. For those born in 1960 or later, it is 67. Claiming before your FRA results in a permanent reduction in your monthly payment, while waiting until after your FRA can lead to significant increases. Understanding your specific FRA is the baseline for any financial projection regarding your Social Security income.

Factors That Influence Your Monthly Check

While the base formula provides the starting point, several variables can fluctuate the actual amount that lands in your bank account. These factors range from personal choices regarding when to retire to external economic shifts.

Early vs. Delayed Claiming Strategies

One of the most significant factors in the “What is my payment?” equation is timing. You can begin receiving benefits as early as age 62, but doing so comes at a cost. If your FRA is 67 and you claim at 62, your monthly payment will be reduced by approximately 30%. Conversely, for every year you delay claiming beyond your FRA—up until age 70—your benefit increases by roughly 8% per year. This “delayed retirement credit” can result in a monthly payment that is 24% to 32% higher than it would have been at your FRA. From a personal finance perspective, delaying benefits is often one of the most effective ways to guarantee a higher “inflation-protected” income for life.

The “Top 35 Years” and Work History

Because the formula relies on your top 35 years of earnings, your work history plays a massive role. If you had several years of low earnings early in your career, working just a few more years at a higher salary later in life can “bump out” those low-earning years from the calculation. This is a common strategy for individuals looking to maximize their payments in the final decade of their career.

Cost-of-Living Adjustments (COLA)

To ensure that Social Security maintains its purchasing power, the SSA applies a Cost-of-Living Adjustment (COLA) almost every year. These adjustments are based on the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). When inflation rises, Social Security payments are increased to help beneficiaries keep up with the cost of goods and services. For retirees on a fixed income, COLA is a vital component of financial stability, protecting them against the eroding effects of a rising cost of living.

Different Types of Social Security Benefits

When asking “What is my Social Security payment?”, it is important to identify which specific benefit you are eligible for. The system covers more than just retirement; it acts as a comprehensive insurance program for various life stages and circumstances.

Retirement Benefits

This is the most common form of payment, available to workers who have earned at least 40 “credits” (usually equating to 10 years of work). These payments are intended to replace about 40% of an average worker’s pre-retirement income, though this percentage varies based on the earnings levels discussed earlier.

Social Security Disability Insurance (SSDI)

If you become unable to work due to a physical or mental disability that is expected to last at least a year or result in death, you may be eligible for SSDI. The payment amount for SSDI is generally calculated using the same PIA formula as retirement benefits, but it is based on your earnings up until the point the disability began.

Survivor and Spousal Benefits

Social Security provides a crucial safety net for families. Spouses of retired workers can receive up to 50% of the worker’s benefit amount, even if the spouse never worked themselves. Furthermore, survivor benefits allow widows, widowers, and dependent children to receive a portion of a deceased worker’s benefits. For a surviving spouse, this often means “stepping up” to the higher of the two checks the couple was receiving, which can be a critical factor in maintaining the survivor’s standard of living.

Navigating Taxes and Deductions

What you see on your SSA statement is your “gross” benefit. However, many retirees are surprised to find that their “net” payment is lower due to various deductions and tax obligations.

Combined Income and Federal Taxation

Depending on your total income, a portion of your Social Security benefits may be subject to federal income tax. The IRS uses “combined income” (your adjusted gross income + tax-exempt interest + half of your Social Security benefits) to determine this. If you are a single filer with a combined income between $25,000 and $34,000, you may pay taxes on up to 50% of your benefits. If your income exceeds $34,000, up to 85% of your benefits may be taxable. For married couples, these thresholds are $32,000 and $44,000, respectively.

Medicare Premium Deductions

For most retirees, the Part B Medicare premium is automatically deducted from their Social Security check. As healthcare costs rise, these premiums can take a larger bite out of the annual COLA increase. It is essential to factor in these deductions when calculating your actual spendable income in retirement.

Maximizing Your Benefit: Strategic Financial Planning

Understanding your payment is only the first step; the second is optimizing it. Effective financial planning requires a proactive approach to managing your Social Security expectations.

Working While Receiving Benefits

If you choose to work while receiving Social Security benefits before you reach your FRA, there is an “earnings test.” If you earn over a certain limit ($22,320 in 2024), the SSA will temporarily withhold $1 in benefits for every $2 you earn over that limit. Once you reach your FRA, these withholdings are recalculated and added back into your monthly payment, and the earnings limit disappears entirely. For those who enjoy working, it is often better to wait until FRA to claim to avoid these temporary reductions.

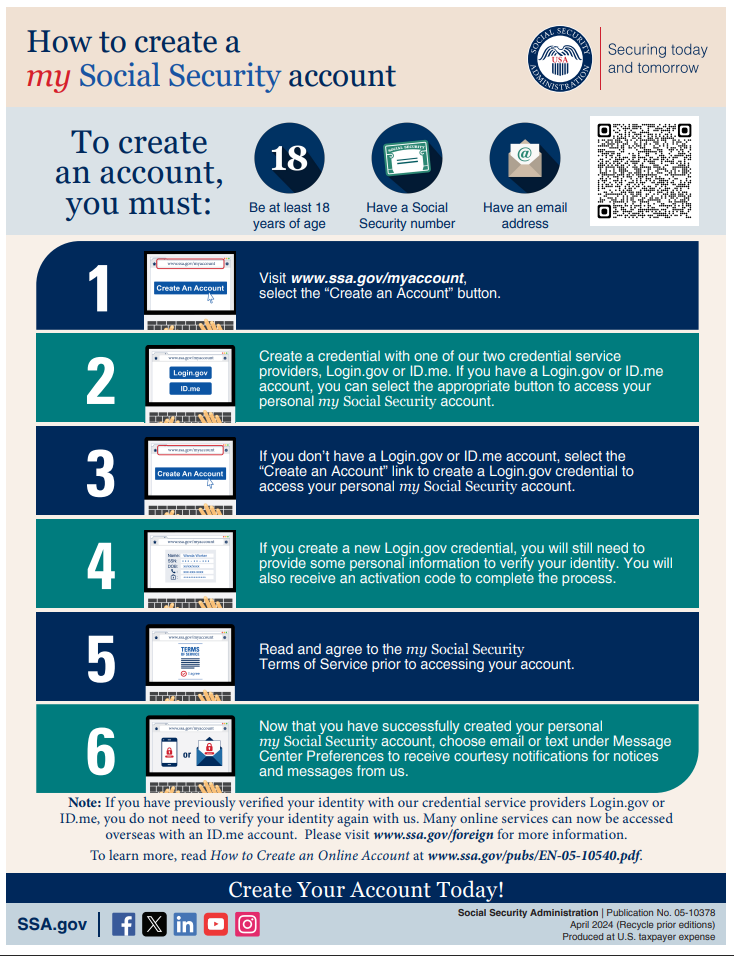

Utilizing the “my Social Security” Digital Tools

The most accurate way to answer “What is my Social Security payment?” is to create an account on the SSA’s official website. The “my Social Security” portal provides a personalized “Social Security Statement” that estimates your future benefits based on your actual earnings record. It allows you to model different retirement ages and see how your payments would change. Regularly reviewing this statement is crucial for catching errors in your earnings history, which, if left uncorrected, could permanently lower your monthly check.

Conclusion

Your Social Security payment is the result of decades of labor, and its value lies in its predictability and its protection against inflation. By understanding the AIME formula, the impact of claiming ages, and the tax implications of your total income, you can transform Social Security from a confusing government program into a powerful tool for financial independence. Whether you are 25 or 65, the decisions you make today regarding your career and your claiming strategy will echo throughout your retirement years, determining the level of comfort and security you enjoy in the future.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.