In the world of digital assets, the ability to enter a position is only half of the equation. For the disciplined investor, the exit strategy is perhaps more critical. Whether you are rebalancing your portfolio, harvesting gains, or needing to liquidate assets for real-world expenses, understanding the nuances of withdrawing from Coinbase is a fundamental skill in personal finance management.

Coinbase has established itself as a primary gateway between traditional fiat systems and the decentralized economy. However, the process of moving value out of the ecosystem requires a keen understanding of settlement periods, fee structures, and security protocols. This guide provides a professional deep dive into the financial mechanics of withdrawing your capital effectively and securely.

The Mechanics of Liquidity: Preparing Your Portfolio for Withdrawal

Before initiating a withdrawal, an investor must understand the distinction between asset types and their respective liquidity paths. Your “Total Balance” on Coinbase is often different from your “Available Balance,” a distinction that frequently confuses those new to the platform’s financial ecosystem.

Understanding Fiat vs. Crypto Withdrawals

There are two primary ways to “withdraw” from Coinbase, each serving a different financial purpose. A crypto-to-fiat withdrawal involves selling your digital assets for a sovereign currency (like USD, EUR, or GBP) and transferring those funds to a traditional bank account. This is the path for those looking to realize gains in the traditional economy.

Conversely, a crypto-to-wallet withdrawal involves moving the digital asset itself to a private hardware wallet or another exchange. From a wealth management perspective, this is often done to increase security through self-custody or to utilize the assets in Decentralized Finance (DeFi) protocols. Knowing which path you are taking is the first step in determining your fee exposure and tax obligations.

Managing Settlement Times and Pending Transactions

One of the most common hurdles in personal finance management on Coinbase is the “available to withdraw” limit. When you purchase crypto using a bank account (ACH), the funds are often available for trading immediately, but they are not available for withdrawal until the underlying bank transfer has cleared.

This period typically lasts between 3 to 5 business days. For institutional or high-net-worth individual investors, this delay must be factored into any time-sensitive financial planning. If you anticipate needing liquidity by a specific date, the liquidation process should begin at least a week in advance to account for these traditional banking “hold” periods.

Executing the Transfer: A Step-by-Step Financial Protocol

Once your funds are settled and you have decided on your exit path, the execution must be handled with precision. Errors in the withdrawal process can lead to delayed access to capital or, in the case of crypto transfers, the permanent loss of assets.

Linking and Verifying Your Banking Channels

The efficiency of your withdrawal is largely dictated by the “plumbing” you have connected to your Coinbase account. For most users, an ACH (Automated Clearing House) connection is the standard. While ACH is cost-effective (often free), it is the slowest method.

For those requiring larger capital movements or faster speeds, a Federal Wire transfer is the preferred institutional method. While wires often carry a flat fee from both Coinbase and your receiving bank, they typically settle within one business day. Additionally, the integration of real-time payment systems like PayPal or Instant Card Withdrawals has provided a retail-friendly bridge for immediate liquidity, albeit usually at the cost of higher percentage-based fees.

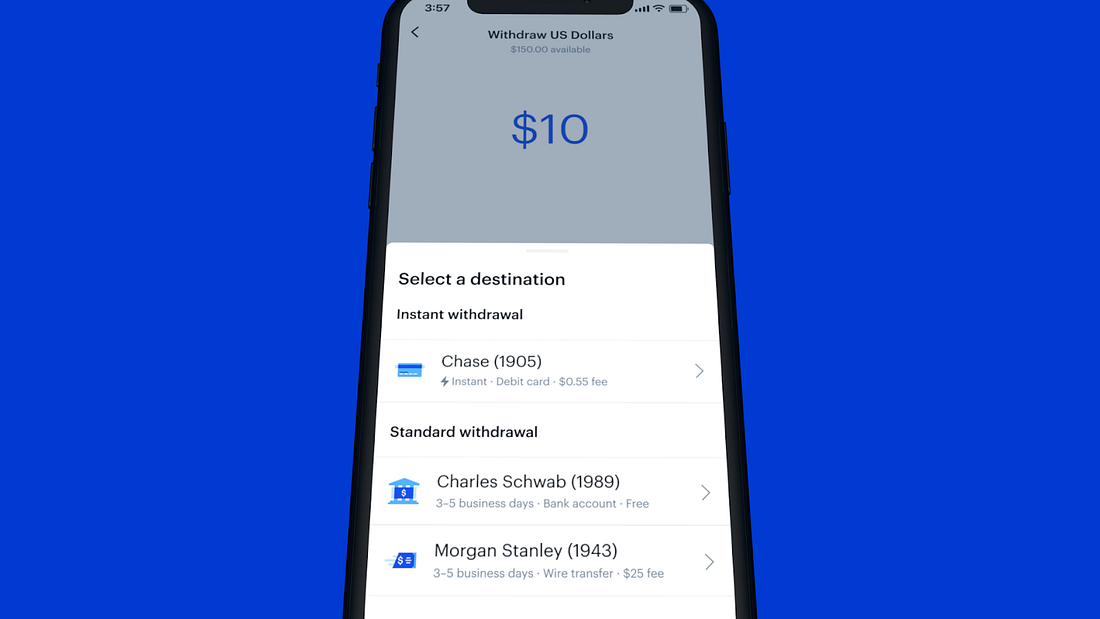

Navigating the Coinbase Interface for Optimal Speed

To begin the withdrawal, you first navigate to the “Assets” or “My Assets” section. If your wealth is currently held in a cryptocurrency like Bitcoin or Ethereum, you must first execute a “Sell” order to convert the asset into your local fiat currency (e.g., USD).

Once the asset is converted to fiat, you select the “Cash Out” option. At this stage, you will be prompted to choose your destination. A professional approach involves double-checking the destination account numbers. While Coinbase saves your linked accounts, it is a best practice in financial security to verify that the last four digits of the receiving account match your intended destination before confirming the “Cash Out” command.

Optimization and Cost Management: Navigating Fees and Limits

In the realm of investing, every basis point matters. High withdrawal fees can quietly erode your annual returns if not managed proactively. Coinbase utilizes a tiered fee structure that rewards higher-volume traders and those who utilize their more advanced tools.

Analyzing the Fee Structure of Different Withdrawal Methods

Withdrawal costs are not uniform. If you use a standard debit card for an “Instant Withdrawal,” you may be charged up to 1.5% of the transaction value (often with a minimum and maximum cap). For a $10,000 withdrawal, a 1.5% fee is $150—a significant cost for the sake of speed.

By contrast, standard ACH withdrawals to a linked bank account are typically free. For the patient investor, choosing the 1-3 day window of an ACH transfer over the instant gratification of a card withdrawal is a simple way to preserve capital. Furthermore, users should be aware of “network fees” (gas fees) when withdrawing crypto to an external wallet. These fees are paid to the blockchain miners, not Coinbase, and can fluctuate wildly based on network congestion.

Strategies to Minimize Slippage and Transaction Costs

For significant liquidations, “slippage” is a major concern. Slippage occurs when there is a difference between the expected price of a trade and the price at which the trade is executed. To minimize this, sophisticated investors avoid the simple “Convert” or “Sell” buttons on the main dashboard, which often use a spread-based pricing model that can be expensive.

Instead, utilizing “Coinbase Advanced” allows you to place “Limit Orders.” By setting a specific price at which you are willing to sell your crypto for fiat, you ensure that you aren’t overpaying via the spread. Once the limit order is filled, the fiat remains in your Coinbase cash balance, ready to be withdrawn via the most cost-effective channel (ACH).

Security and Compliance: Safeguarding Your Capital During Transit

Financial transit is the moment of highest vulnerability. Ensuring that your capital reaches its destination requires a combination of robust digital security and an understanding of the regulatory landscape.

Essential Security Layers for Large-Scale Transfers

Before moving significant sums, ensure your account security is updated. Professional investors should never rely on SMS-based Two-Factor Authentication (2FA), as it is vulnerable to SIM-swapping attacks. Instead, use hardware security keys (like YubiKey) or app-based authenticators (like Google Authenticator).

Additionally, Coinbase offers a “Whitelisting” or “Address Book” feature. This allows you to restrict withdrawals only to pre-approved addresses or bank accounts. While this adds a 48-hour delay to adding any new destination, it serves as a critical circuit breaker; if an unauthorized party gains access to your account, they would be unable to drain your funds to an outside address immediately, giving you time to freeze the account.

Tax Implications and Regulatory Record-Keeping

From a personal finance and tax perspective, a withdrawal is often a “taxable event.” In many jurisdictions, selling cryptocurrency for fiat currency triggers capital gains tax. It is a common mistake to think that taxes are only due when you move the money to a bank. In reality, the moment you sell the crypto for USD within the Coinbase app, the gain is realized.

Coinbase provides tax resource centers and generates Form 1099-MISC or 1099-B for eligible users, but these records are only as good as your personal bookkeeping. When withdrawing, it is wise to download your transaction history report immediately. This ensures you have a clear paper trail of your “cost basis” and “exit price,” which will be invaluable when tax season arrives. Managing your withdrawals with an eye toward future liabilities is the hallmark of a sophisticated investor.

By treating the withdrawal process not as a mere technical task, but as a strategic financial operation, you protect your margins and ensure the long-term viability of your investment portfolio. Success in the digital asset space is defined not just by the assets you accumulate, but by the capital you successfully preserve and transition back into your broader financial life.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.