Purchasing a vehicle is often the second-largest financial commitment most people make, trailing only the purchase of a home. Yet, many consumers approach the car-buying process backward. They walk onto a dealership lot, find a vehicle that fits their lifestyle, and then ask the salesperson, “How much will this cost me per month?” This “payment-first” mentality is a common trap that leads to long-term financial strain.

To maintain true financial health, the question shouldn’t be what the dealership can “get you into,” but rather, “How much car payment can I actually afford based on my unique financial ecosystem?” Determining this number requires a deep dive into your cash flow, your long-term wealth goals, and the total cost of ownership beyond the sticker price.

The Core Principles of Vehicle Budgeting

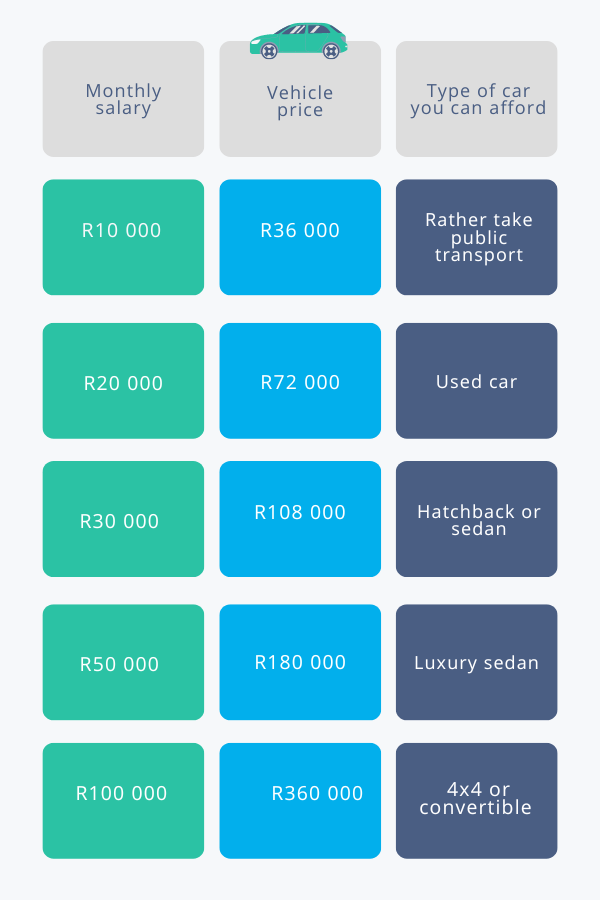

Before looking at specific models, you must establish a mathematical framework. Financial experts often rely on several “rules of thumb” to help individuals stay within their means. While these aren’t laws, they provide a safety net that prevents you from becoming “car poor.”

The 20/4/10 Rule

The 20/4/10 rule is widely considered the gold standard for vehicle financing. It breaks down as follows:

- 20% Down Payment: You should aim to put down at least 20% of the purchase price. This protects you from “negative equity”—the situation where you owe more on the loan than the car is worth—as soon as you drive off the lot.

- 4-Year Loan Term: While 72-month and 84-month loans are becoming common, a 48-month (4-year) term is the limit for healthy financing. Longer terms may lower the monthly payment, but they drastically increase the total interest paid and keep you in debt longer.

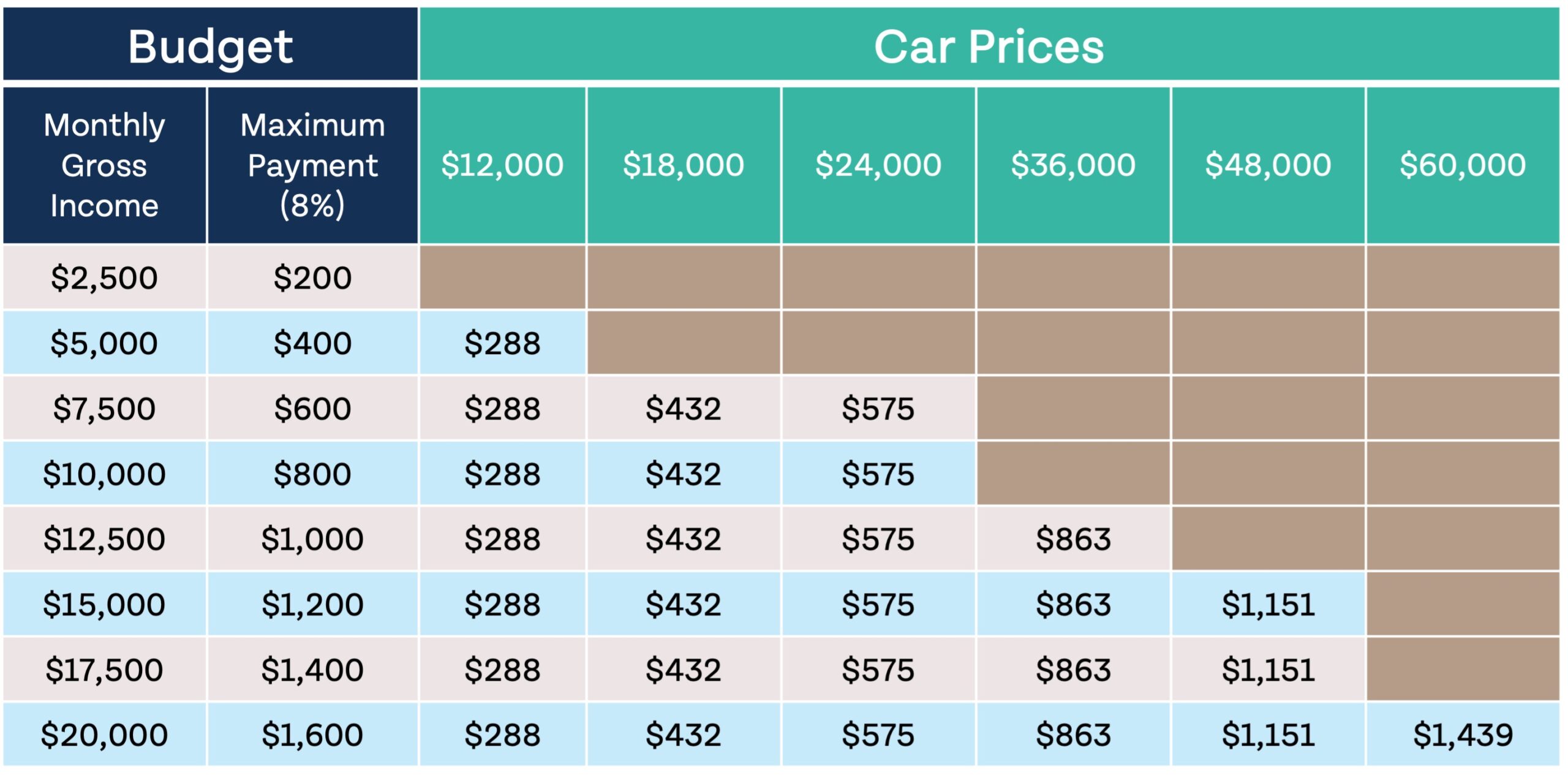

- 10% of Gross Income: Your total transportation costs—including the loan payment, insurance, and maintenance—should not exceed 10% of your gross monthly income.

Analyzing the Debt-to-Income (DTI) Ratio

Lenders look at your Debt-to-Income ratio to determine your creditworthiness, and you should too. Your DTI is the percentage of your gross monthly income that goes toward paying debts (rent/mortgage, student loans, credit cards, and car payments). Generally, your total DTI should stay below 36%. If a prospective car payment pushes your DTI toward 43% or higher, most financial planners would suggest you are overextending yourself, even if a lender is willing to approve the loan.

Understanding the Total Cost of Ownership (TCO)

The most frequent mistake in car budgeting is equating the “monthly payment” with the “monthly cost.” The loan installment is merely the entry fee. To understand what you can afford, you must account for the secondary costs that vary wildly depending on the vehicle type.

Insurance and Registration

The cost of insuring a vehicle is highly dependent on its safety rating, repair costs, and performance level. A luxury sedan might have the same monthly payment as a reliable SUV, but the insurance premiums on the luxury vehicle could be double. Before committing to a payment, call your insurance provider with a specific VIN or model to get a quote. Additionally, remember that annual registration fees and property taxes (in certain states) are based on the car’s value; these “hidden” annual costs should be amortized across your monthly budget.

Fuel, Maintenance, and Repairs

A “cheap” monthly payment on an older, high-end European car can quickly become a financial nightmare when maintenance is due. When calculating affordability, look up the “five-year cost to own” for the specific make and model. Consider the following:

- Fuel Efficiency: If you commute 30 miles a day, the difference between 20 MPG and 30 MPG can represent hundreds of dollars a month in fuel costs.

- Routine Maintenance: Factor in the cost of oil changes, tire rotations, and brake replacements.

- The “Out-of-Warranty” Buffer: If you are buying a used vehicle without a warranty, you should set aside an additional $50–$100 per month into a “sinking fund” specifically for unexpected repairs.

Depreciation: The Silent Budget Killer

While depreciation isn’t a monthly cash outflow, it is a significant financial cost. Most new cars lose 20% of their value in the first year and 60% within the first five years. If you buy an expensive car with a low down payment, depreciation can leave you “underwater” on your loan. This limits your financial flexibility because you cannot sell or trade the car without paying the lender the difference out of your own pocket.

Navigating the World of Auto Financing

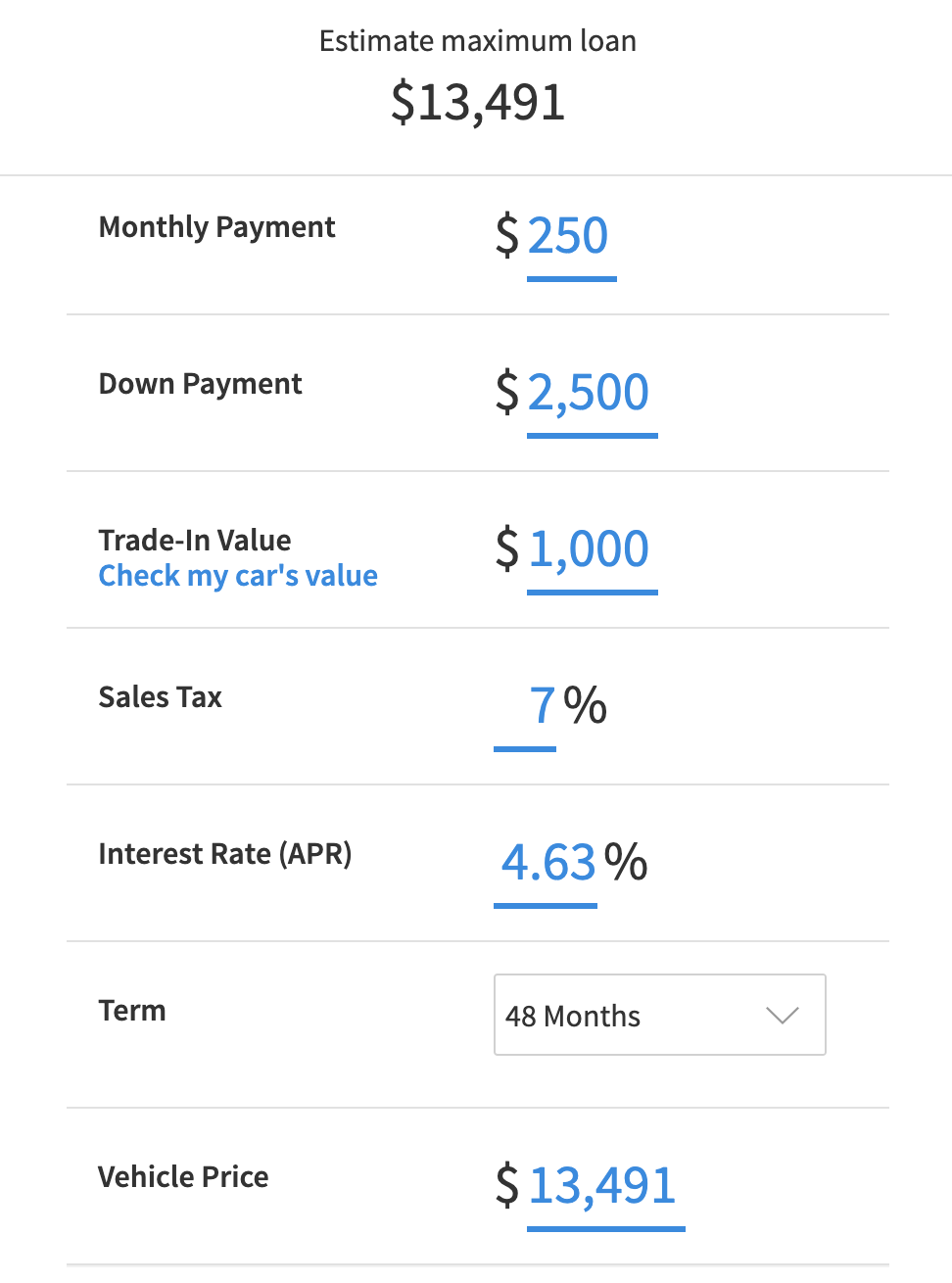

The “affordability” of a car is heavily dictated by the terms of the loan. Two people could buy the exact same car for the same price, but one might pay thousands more over the life of the loan due to poor financing choices.

The Impact of Credit Scores and Interest Rates

Your credit score is the most significant lever in determining your interest rate (APR). On a $30,000 loan, the difference between a 3% APR (for excellent credit) and a 12% APR (for subprime credit) can be over $100 per month and $6,000 in total interest. Before visiting a dealership, check your credit report and get pre-approved through a credit union or bank. This gives you a baseline for what you can afford and prevents the dealership from marking up the interest rate to increase their profit.

The Danger of Long-Term Loans

Dealerships often try to lower your monthly payment by extending the loan term to 72 or 84 months. While this makes a $50,000 truck “fit” into a $600-a-month budget, it is a dangerous financial move. Not only do you pay significantly more in interest, but you also risk being in debt for a vehicle that is no longer reliable or is worth a fraction of the remaining loan balance. If you cannot afford the payment on a 48-month or 60-month term, you simply cannot afford that specific car.

Leasing vs. Buying: A Financial Comparison

Leasing can be attractive because it offers lower monthly payments and the ability to drive a new car every few years. However, from a wealth-building perspective, leasing is generally the most expensive way to operate a vehicle. When you lease, you are essentially paying for the car’s depreciation during its most expensive years, and at the end of the term, you have zero equity. Buying a reliable vehicle and driving it for 10 years—well after the loan is paid off—is one of the most effective ways to free up cash for investing and long-term savings.

Practical Steps to Calculate Your Personal Number

Once you understand the rules and the hidden costs, it’s time to look at your actual bank statements and determine your “walk-away” number.

Auditing Your Current Cash Flow

Affordability is not just about what is left over at the end of the month; it is about your priorities. Perform a line-item audit of your spending. If you find that a $500 car payment would prevent you from contributing to your 401(k) or building an emergency fund, then you cannot afford that payment. Your car should serve your financial goals, not hinder them. A good rule of thumb is to ensure that after all expenses—including the new car payment—you still have a surplus of at least 10–15% of your income for savings and investments.

Building an Opportunity Cost Analysis

In the world of personal finance, every dollar spent on a depreciating asset like a car is a dollar that isn’t earning interest in the stock market or real estate. This is known as “opportunity cost.” For example, the difference between a $400 car payment and a $700 car payment is $300. If you were to take that $300 difference and invest it in a low-cost index fund with an average 7% annual return, you would have approximately $21,000 after five years. Over 30 years, that single decision could represent over $350,000 in retirement savings. Viewing a car payment through the lens of future wealth often provides the clarity needed to choose a more modest, affordable vehicle.

In conclusion, the amount of car payment you can afford is a personal calculation that goes far beyond the “monthly nut.” By following the 20/4/10 rule, accounting for the total cost of ownership, and understanding the long-term impact of financing and opportunity costs, you can make a purchase that provides both reliable transportation and financial peace of mind. Remember: the goal is to drive a car that fits your life, not to live a life that fits your car payment.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.