For many employees, tax season is defined by the arrival of a single piece of paper: the Form W-2, Wage and Tax Statement. While the form is filled with numbered boxes and cryptic abbreviations, Box 1 is arguably the most significant figure on the document. Titled “Wages, tips, other compensation,” Box 1 represents the portion of your income that the federal government considers taxable.

Understanding what goes into Box 1—and more importantly, why it often doesn’t match your final paycheck of the year—is a cornerstone of personal finance literacy. This figure dictates your federal income tax bracket, influences your eligibility for various tax credits, and serves as the starting point for your Form 1040. In this guide, we will break down the mechanics of Box 1, the financial strategies that influence its calculation, and why it is the most critical number for your annual financial health.

The Anatomy of Box 1: Wages, Tips, and Other Compensation

At its most basic level, Box 1 reports the total taxable wages, tips, and other compensation you received from your employer during the calendar year. However, “total taxable” is a technical term that distinguishes this figure from your “gross pay.” Box 1 is the net result of your earnings minus specific tax-deferred or tax-exempt deductions.

What is Included in Box 1?

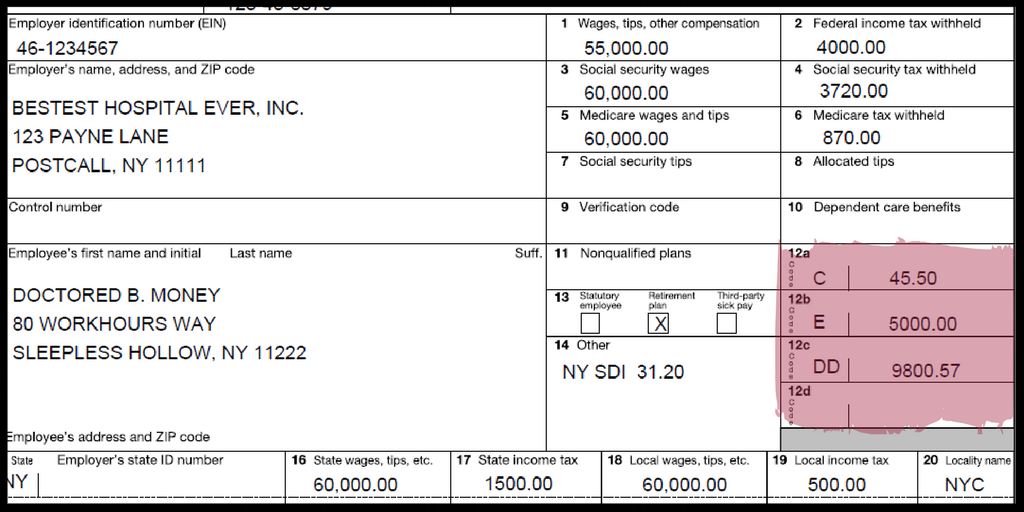

Box 1 isn’t just your base salary. It encompasses a wide variety of financial benefits provided by your employer. These include:

- Base Salary and Hourly Wages: The standard compensation for your labor.

- Bonuses and Commissions: Any performance-based pay or year-end bonuses.

- Taxable Fringe Benefits: This might include the value of a company car for personal use, certain group-term life insurance premiums (over $50,000 in coverage), or moving expense reimbursements that are no longer tax-exempt under current law.

- Tips: If you work in a service industry, any tips you reported to your employer are bundled into this total.

- Severance Pay: If you left a job during the year, any severance packages are included here.

The Role of “Other Compensation”

The “Other Compensation” portion of the label covers miscellaneous items that often surprise taxpayers. For example, if your employer pays for your gym membership or provides certain types of educational assistance that exceed the IRS tax-free limit, that value is added to Box 1. From a financial management perspective, it is vital to track these non-cash compensations throughout the year, as they increase your tax liability without increasing the liquid cash in your bank account.

The Great Discrepancy: Why Box 1 Differs from Gross Pay

One of the most frequent questions taxpayers ask financial advisors is: “Why is the amount in Box 1 lower than my total salary?” This discrepancy is usually the result of “pre-tax deductions.” For the savvy investor and disciplined saver, a lower Box 1 relative to gross pay is often a sign of healthy financial planning.

Retirement Contributions: The Primary Reducer

The most common reason Box 1 is lower than your gross earnings is your contribution to a traditional 401(k), 403(b), or similar employer-sponsored retirement plan. When you contribute to these accounts, the money is taken out of your paycheck before federal income taxes are calculated.

- Example: If you earned $80,000 but contributed $15,000 to a traditional 401(k), your Box 1 would show $65,000 (assuming no other adjustments). This effectively lowers your taxable income, potentially dropping you into a lower tax bracket.

Health and Welfare Benefits

Premiums paid for employer-sponsored health insurance, dental insurance, and vision insurance are typically “Section 125” cafeteria plan deductions. Because these are paid with pre-tax dollars, they are excluded from Box 1. Similarly, contributions to a Health Savings Account (HSA) or a Flexible Spending Account (FSA) through payroll deduction further reduce the figure in Box 1. These tools are essential for managing business and personal finance, as they allow you to pay for necessary medical or childcare expenses while simultaneously reducing your federal tax burden.

What is NOT Deducted?

It is important to note that while retirement and health contributions reduce Box 1, your Social Security and Medicare taxes do not. Furthermore, contributions to a Roth 401(k) do not reduce Box 1. Because Roth accounts are funded with after-tax dollars, that money remains included in your taxable wages for the current year, though it provides tax-free growth and withdrawals in the future.

Comparing Box 1 to Boxes 3 and 5

To truly understand your W-2, you must look at Box 1 in the context of Box 3 (Social Security wages) and Box 5 (Medicare wages). It is very common for these three boxes to show different amounts, and understanding why is key to verifying your employer’s accounting.

The Social Security Wage Base (Box 3)

Box 3 reports the portion of your wages subject to the Social Security tax. Unlike Box 1, Box 3 is capped by the Social Security wage base ($160,200 for 2023, and $168,600 for 2024). If you earn more than this limit, Box 3 will be lower than Box 1. However, for those earning below the limit, Box 3 is often higher than Box 1. This is because 401(k) contributions reduce your federal income tax (Box 1) but do not reduce your Social Security tax (Box 3).

Medicare Wages (Box 5)

Box 5 represents your Medicare wages. Unlike Social Security, there is no ceiling on Medicare taxes; you pay it on every dollar of earned income. Because of this, Box 5 is usually the most accurate representation of your “actual” gross pay before retirement contributions. If you see that Box 5 is significantly higher than Box 1, it is a clear indicator of how much of your income you successfully shielded from federal income tax through pre-tax benefits.

Identifying Potential Errors

If Box 1, 3, and 5 are all identical, but you know you contributed to a 401(k) or paid for health insurance through your employer, there may be a clerical error. Financial diligence requires reviewing these boxes against your final pay stub of the year to ensure you aren’t paying more in federal income tax than is legally required.

The Strategic Importance of Box 1 in Financial Planning

Box 1 is not just a historical record of what you earned; it is a tool for future financial strategy. Because this number is the basis for your Adjusted Gross Income (AGI), it influences almost every other part of your financial life.

Tax Bracket Management

The U.S. uses a progressive tax system. By understanding how deductions affect Box 1, you can engage in “bracket management.” If you find that your income is just a few thousand dollars into a higher tax bracket (e.g., the 24% bracket vs. the 22% bracket), increasing your 401(k) or HSA contributions can lower your Box 1 enough to keep the majority of your income taxed at the lower rate.

Eligibility for Credits and Deductions

Many federal tax benefits are phased out based on income levels. This includes the Child Tax Credit, the Student Loan Interest Deduction, and eligibility for contributing to a Roth IRA. Since Box 1 is the primary driver of your AGI, keeping this number low through smart pre-tax allocations can preserve your eligibility for these valuable financial offsets.

Loan Applications and Credit

When you apply for a mortgage or a business loan, lenders will often look at your W-2s. While a lower Box 1 is great for taxes, lenders are trained to look at the “add-backs” (like retirement contributions) to determine your true repayment capacity. However, having a clean, accurate Box 1 ensures that your debt-to-income ratios are calculated correctly based on your taxable reality.

Compliance, Corrections, and Common Mistakes

Errors in Box 1 can lead to significant issues with the IRS. As a taxpayer, you are responsible for the accuracy of your return, even if the error originated with your employer’s payroll department.

What if Box 1 is Wrong?

If you believe the amount in Box 1 is incorrect—perhaps a bonus was excluded or a pre-tax deduction was incorrectly treated as taxable—your first step is to contact your HR or payroll department. They must issue a Form W-2c (Corrected Wage and Tax Statement). Filing your taxes with an incorrect Box 1 can result in an underpayment penalty if the income was underreported, or a lost refund if it was overreported.

The Impact of Multiple Jobs

If you held multiple jobs during the year, you will receive a W-2 from each employer. Your total taxable income for the year will be the sum of Box 1 from all forms. It is a common financial pitfall to forget that while each employer might withhold taxes correctly for the income they paid you, the combined total might push you into a higher tax bracket. Monitoring the cumulative total of your Box 1 figures throughout the year allows you to adjust your withholdings (via Form W-4) to avoid a large surprise bill in April.

Conclusion

Box 1 of your W-2 is far more than just a number; it is a reflection of your annual earnings, your commitment to future savings, and your contribution to the national economy. By understanding the mechanics of “Wages, tips, and other compensation,” you move from being a passive recipient of tax forms to an active manager of your financial destiny. Whether you are looking to optimize your tax bracket or simply ensure that your employer has accounted for your benefits correctly, Box 1 is the definitive starting point for any serious discussion on personal finance and federal taxation.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.