In the contemporary real estate market, prospective homeowners often face a daunting dilemma: high prices for move-in-ready homes or affordable “fixer-uppers” that require cash the buyer simply doesn’t have. For many, the dream of homeownership is stalled by the reality of outdated kitchens, crumbling foundations, or inefficient HVAC systems. This is where the FHA 203(k) loan enters the conversation as a powerful financial tool.

Designed by the Federal Housing Administration (FHA), the 203(k) rehabilitation mortgage is a specialized government-backed loan that allows borrowers to purchase or refinance a property and include the cost of repairs and improvements in a single mortgage. Instead of juggling a primary mortgage and a separate high-interest construction loan or credit card debt, the FHA 203(k) provides a streamlined, affordable path to transforming a house into a home.

Understanding the FHA 203(k) Rehabilitation Mortgage

The FHA 203(k) loan is fundamentally different from a standard FHA 203(b) mortgage. While the latter is intended for homes in good condition, the 203(k) is specifically designed for properties that need significant work. It bridges the gap between the purchase price and the “after-repair value” (ARV) of the home.

The “One-Loan” Concept

The primary advantage of the 203(k) program is its simplicity in structure. When you buy a home that needs $50,000 in renovations, a traditional lender might only lend you the value of the home in its current state. You would then need to find an additional $50,000 elsewhere. The 203(k) loan combines these two into one monthly payment, one interest rate, and one closing process. This “one-loan” concept reduces closing costs and simplifies the financial management of the project.

The Role of the HUD Consultant

For larger projects, the FHA requires the involvement of a HUD Consultant. This is a professional who inspects the property, helps the borrower prepare the “Work Write-Up,” and ensures that the renovations meet FHA’s minimum property standards. From a financial perspective, the consultant acts as a safeguard, ensuring that the money is being spent on viable improvements that will actually increase the property’s value, thereby protecting the borrower’s investment.

Interest Rates and Escrow

Because the government backs these loans, interest rates are typically more competitive than those of personal loans or specialized construction financing. However, they are usually about 0.75% to 1% higher than a standard FHA loan. During the renovation period, the funds for repairs are held in a supervised escrow account and released to contractors in “draws” as specific milestones of the project are completed and inspected.

Limited vs. Standard: Which Loan Fits Your Project?

The FHA 203(k) program is divided into two distinct categories based on the scope of the work being performed: the Limited 203(k) and the Standard 203(k). Choosing the right one depends entirely on the scale of your renovation goals.

The Limited 203(k) (Formerly “Streamline”)

The Limited 203(k) is intended for minor remodeling and non-structural repairs. It is capped at a maximum of $35,000 in renovation costs. There is no minimum repair cost, making it ideal for homes that are mostly functional but need cosmetic upgrades.

- Permissible Projects: Kitchen remodeling, new flooring, roof replacement, painting, weatherization, and appliance upgrades.

- Restrictions: You cannot use this loan for structural changes (like moving a load-bearing wall), landscaping, or adding a room.

- Financial Advantage: It is faster to close and does not require a HUD Consultant, which saves on upfront fees.

The Standard 203(k)

The Standard 203(k) is the “heavy lifter” of the program. It is designed for properties that require major rehabilitation or structural changes. There is a minimum repair cost of $5,000, but the maximum is only limited by the FHA’s loan limits for the specific county.

- Permissible Projects: Structural alterations, room additions, foundation repair, complete gut-renovations, and even moving a house to a new location.

- The HUD Consultant Requirement: This loan requires a mandatory HUD Consultant to oversee the project from start to finish.

- Financial Advantage: It allows you to take a “unlivable” property—which most lenders wouldn’t touch—and turn it into a high-value asset, potentially building significant equity in a short period.

Qualifying for an FHA 203(k) Loan: Financial and Property Criteria

While the 203(k) loan offers great flexibility, it is still an FHA-insured product, meaning it comes with specific eligibility requirements regarding both the borrower’s finances and the property itself.

Borrower Requirements: Credit and Income

The FHA is known for being more lenient than conventional lenders, but there are still clear benchmarks:

- Credit Score: Most lenders require a minimum score of 580 to qualify for the 3.5% down payment. If your score is between 500 and 579, you may still qualify but will likely need a 10% down payment.

- Debt-to-Income (DTI) Ratio: Generally, your total monthly debt payments (including the new mortgage) should not exceed 43% to 45% of your gross monthly income, though some lenders allow higher ratios with compensating factors.

- Down Payment: The 3.5% down payment is calculated based on the purchase price plus the total renovation costs. This makes the entry point for homeownership much lower than many other renovation-focused financial products.

Property Eligibility

Not every building can be financed with a 203(k) loan. The property must be:

- Owner-Occupied: This loan is not for “fix-and-flip” investors who do not plan to live in the home. You must intend to use the property as your primary residence.

- Property Type: One-to-four unit dwellings, including condos (with some restrictions) and manufactured homes, are eligible.

- Aged Properties: The home must have been completed for at least one year before the loan application.

The Importance of Mortgage Insurance (MIP)

Like all FHA loans, the 203(k) requires an Upfront Mortgage Insurance Premium (UFMIP) and an annual Mortgage Insurance Premium (MIP). This is an added cost that borrowers must factor into their monthly budget. Since the loan amount includes renovation costs, the MIP will be slightly higher than it would be on a standard home purchase of the same price.

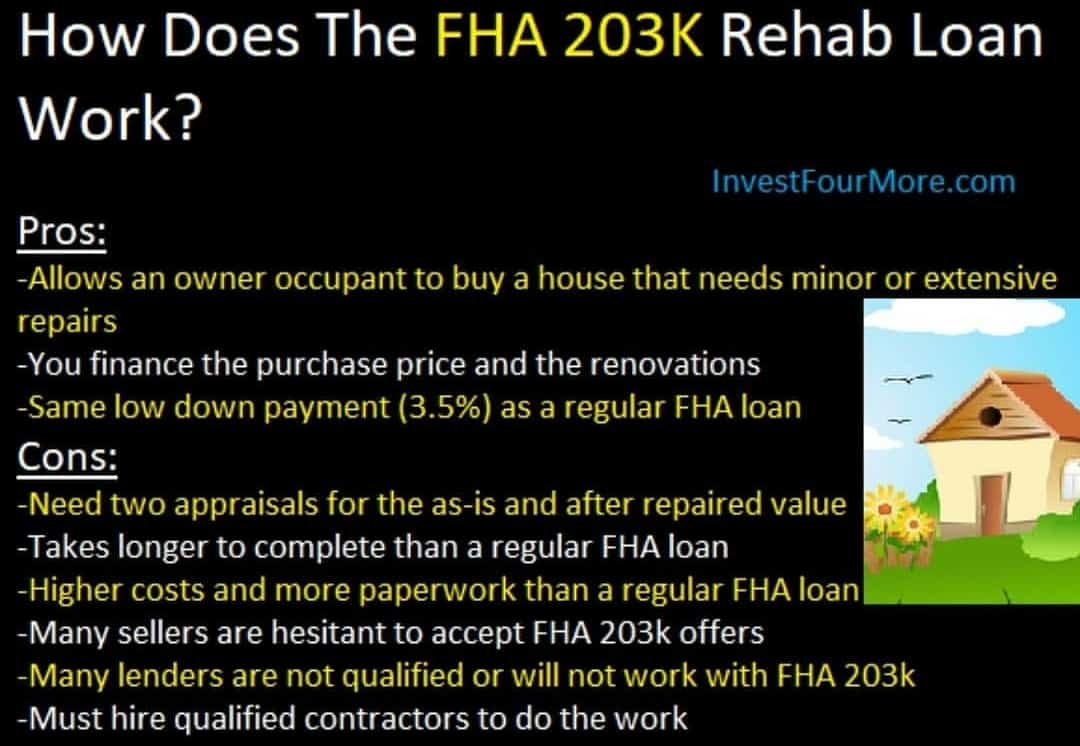

The Benefits and Drawbacks: Is It Worth the Effort?

Investing in an FHA 203(k) loan is a strategic financial move, but it is not without its complexities. Weighing the pros and cons is essential for any savvy personal finance manager.

The Pros: Equity and Customization

- Instant Equity: By purchasing a distressed property at a discount and renovating it, the “After-Repair Value” is often significantly higher than the total loan amount. This creates “forced appreciation” or instant equity.

- Customization: Instead of paying a premium for someone else’s design choices, you have the financial means to customize the home to your specific tastes and needs.

- Low Barrier to Entry: The low down payment and flexible credit requirements make this accessible to first-time homebuyers who are otherwise priced out of the move-in-ready market.

The Cons: Complexity and Cost

- Higher Interest Rates: You will pay a premium on your interest rate compared to a standard FHA or conventional loan.

- Strict Contractor Rules: You cannot do the work yourself (unless you are a professional contractor by trade). You must hire licensed, insured contractors, and the FHA must approve them. This can sometimes lead to higher labor costs.

- The Paperwork Burden: The application process is rigorous. You need detailed bids, architectural drawings (for standard loans), and multiple inspections. Closing usually takes longer—often 45 to 60 days compared to the standard 30.

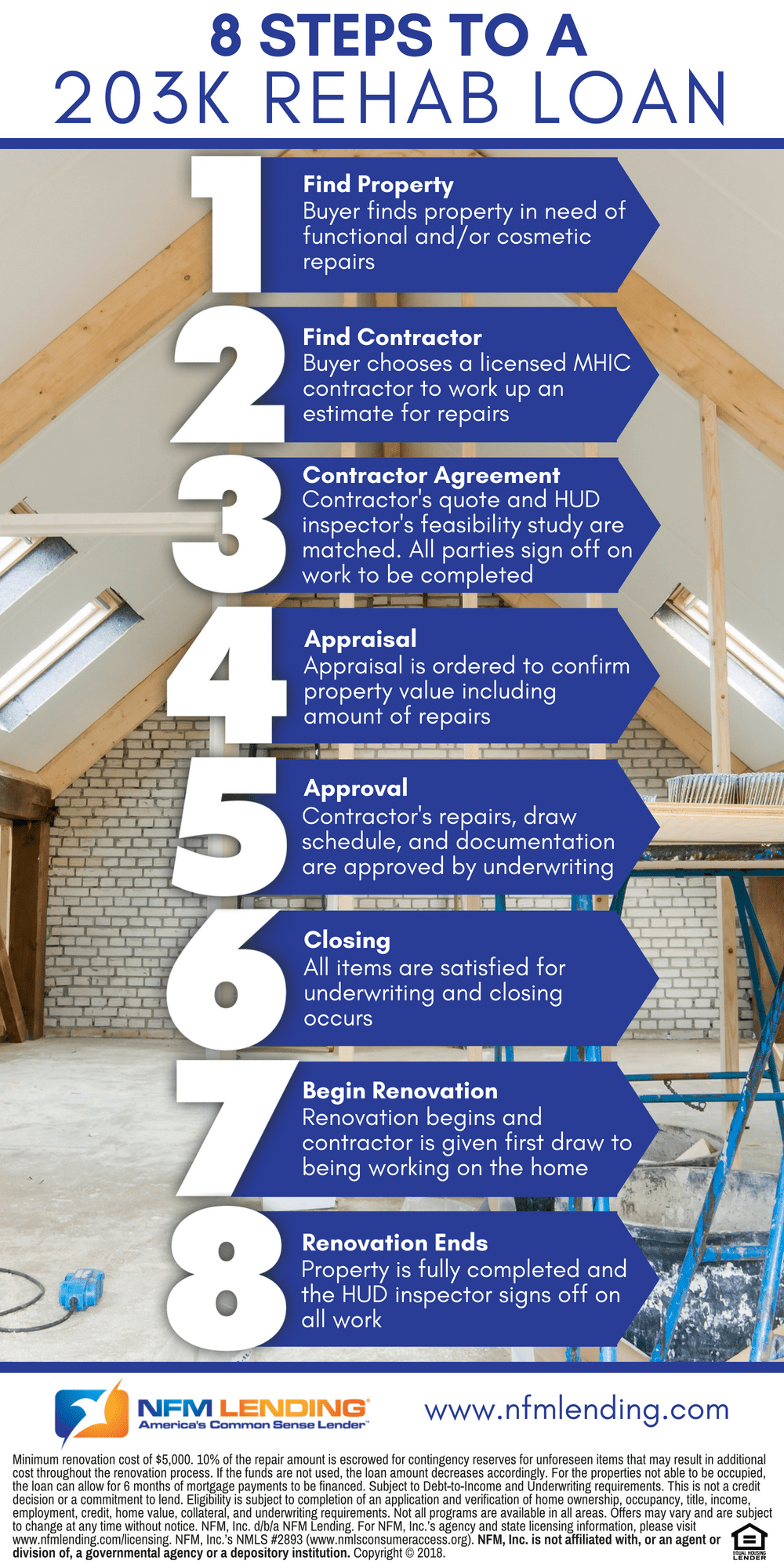

Navigating the 203(k) Process: From Approval to Completion

Successfully utilizing an FHA 203(k) loan requires a disciplined approach to project management and financial planning. The process follows a specific roadmap.

Step 1: Finding a 203(k) Approved Lender

Not all lenders offer 203(k) loans because they require more work from the bank’s back office. Your first step is finding a loan officer who specializes in this niche. They will pre-approve you for a total loan amount, which includes the purchase price and the renovation budget.

Step 2: Property Search and Feasibility

Once pre-approved, you search for a home. When you find a potential candidate, you must quickly estimate the repair costs. If you are pursuing a Standard 203(k), this is when you bring in your HUD Consultant to perform a feasibility study.

Step 3: Contractor Bids and Final Appraisal

After getting the house under contract, you must gather detailed bids from contractors. These bids are then sent to an appraiser. The appraiser doesn’t just look at what the house is worth today; they look at what it will be worth once the work described in the bids is finished. This “subject-to” appraisal is the backbone of the loan’s approval.

Step 4: Closing and the Renovation Phase

At closing, the seller is paid, and the remaining funds are placed into an escrow account. Work must begin within 30 days of closing and must be completed within six months. As the contractor finishes portions of the work, the lender sends an inspector out, and “draws” are released from the escrow account to pay the workers.

Step 5: Final Inspection and Closeout

Once the work is 100% complete, a final inspection ensures everything meets the original “Work Write-Up.” Any remaining funds in the contingency reserve (a 10-20% buffer required by the FHA) are applied toward the principal balance of the mortgage.

The FHA 203(k) loan remains one of the most effective ways for individuals to break into the real estate market while simultaneously building wealth. By understanding the nuances of the program, from the difference between Limited and Standard loans to the intricacies of the appraisal process, you can turn a financial challenge into a lucrative opportunity for homeownership.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.