Navigating the complexities of the Internal Revenue Service (IRS) can be a daunting task for even the most financially savvy individuals. While much of the public discourse surrounding taxes focuses on deductions, credits, and filing software, the final—and perhaps most critical—step is the actual delivery of funds. Knowing exactly where to send IRS payments is not merely a matter of administrative diligence; it is a vital component of personal and business financial management.

In an era defined by a mix of legacy paper systems and cutting-edge digital portals, the “where” and “how” of tax payments have evolved. An error in this stage can lead to misapplied funds, late penalties, and unnecessary interest accrual. This guide explores the diverse avenues for transmitting tax payments, categorized by method and necessity, ensuring your financial obligations are met with precision and security.

The Digital Frontier: Using Electronic Payment Portals

For the modern taxpayer, digital payment methods represent the gold standard of efficiency. The IRS has invested significantly in its digital infrastructure to move away from the bottlenecks associated with physical mail. Using electronic systems not only provides an immediate digital trail but also ensures that the funds reach the Treasury Department without the risks of mail theft or transit delays.

IRS Direct Pay for Individuals

IRS Direct Pay is the most popular tool for individual taxpayers. It allows you to pay your income tax directly from a checking or savings account without any additional fees. This system is particularly useful for those paying their annual 1040 balance or making quarterly estimated tax payments. When using Direct Pay, the “where” is a secure web interface that provides instant confirmation numbers. From a financial management perspective, this method is superior because it allows you to schedule payments up to 30 days in advance, helping you manage your cash flow effectively.

The Electronic Federal Tax Payment System (EFTPS)

While Direct Pay is designed for quick, one-off individual transactions, the Electronic Federal Tax Payment System (EFTPS) is the heavy hitter of the tax world. EFTPS is a free service provided by the U.S. Department of the Treasury that is primarily used by business entities and high-net-worth individuals with complex requirements. Unlike Direct Pay, EFTPS requires an initial enrollment process, which includes the mailing of a PIN. Once set up, it offers a robust platform for paying corporate taxes, payroll taxes, and large-scale estimated payments. For business owners, EFTPS is the professional choice for maintaining a rigorous audit trail.

Digital Wallets and Card Payments

The IRS now accepts payments via debit cards, credit cards, and digital wallets like PayPal or Click to Pay. These payments are processed through third-party service providers. While the “where” in this scenario is a secure third-party portal, it is important to consider the financial implications. These processors charge a convenience fee, often ranging from 1.82% to 1.98% for credit cards. From a strategic finance standpoint, this method is only advisable if the rewards or points earned on the credit card outweigh the processing fee, or if you are using the card as a short-term financing tool to avoid a more expensive IRS late-payment penalty.

The Traditional Route: Mailing Physical Checks and Money Orders

Despite the push toward digitization, a significant portion of the American public still prefers or requires the use of physical mail. Whether you are filing an amended return that requires a physical check or you simply prefer the tangibility of paper, knowing the correct destination is paramount. The IRS uses a distributed network of processing centers, and the address you use depends entirely on your geographical location and the specific form you are filing.

Determining the Correct Processing Center

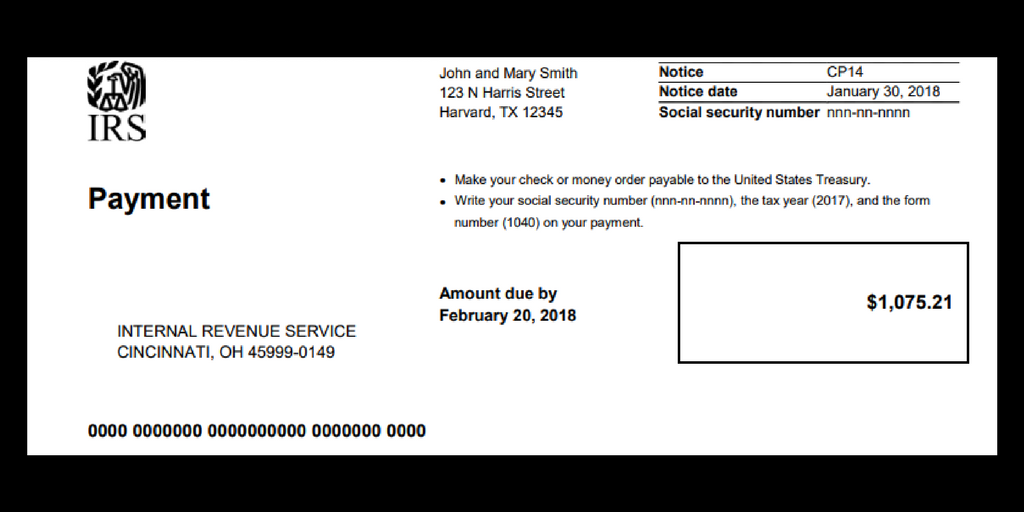

The IRS does not have one single “mailbox” for all payments. Instead, the country is divided into regions served by different centers, typically located in cities like Charlotte, Cincinnati, Hartford, Louisville, or San Francisco. To find the specific address, you must consult the instructions for your specific form (such as the 1040, 1040-ES, or 1040-V). If you are mailing a payment along with your tax return, the address will differ from a payment sent independently. Sending a check to the wrong regional center can delay processing by weeks, which could technically result in a late payment if the funds are not diverted in time.

The Critical Role of Form 1040-V

If you choose to mail a payment, you should never simply drop a check into an envelope. The IRS utilizes Form 1040-V, the Payment Voucher. This small, one-page document contains encoded information that helps the IRS scanners attribute your money to your specific Social Security Number (SSN) or Employer Identification Number (EIN). Financial advisors recommend always using the voucher provided by your tax software or the IRS website. Without this voucher, a check may sit in a “suspense account” while an agent manually attempts to identify the owner, a process that can lead to erroneous late notices.

Certified Mail and the “Timely Mailing” Rule

When sending large sums of money through the U.S. Postal Service, the “where” is only half of the equation; the “when” is the other. Under the Internal Revenue Code, the “timely mailing is timely filing/paying” rule applies. To protect your financial standing, always use USPS Certified Mail with a Return Receipt Requested. This provides legal proof of the date of mailing. If the IRS claims they never received your payment, your certified mail receipt is your primary defense against penalties. In the world of business finance, this receipt is as valuable as the funds themselves.

Specialized Payment Scenarios: Estimated Taxes and Business Obligations

Not all tax payments follow the standard April 15th deadline. For freelancers, small business owners, and investors, the “where” for payments changes based on the type of tax being settled. Managing these specialized streams is crucial for maintaining a healthy balance sheet and avoiding the dreaded underpayment penalty.

Quarterly Estimated Tax Payments (1040-ES)

For those who do not have taxes withheld from a paycheck, estimated tax payments are a quarterly reality. These payments are typically sent to a specific P.O. Box designated for 1040-ES forms. Because these occur four times a year, many taxpayers find it more efficient to transition these specific payments to the digital Direct Pay system mentioned earlier. However, if mailing, ensure you are using the specific voucher for the current tax year, as the addresses can change annually based on IRS processing capacity.

Employment and Business Tax Deposits

Businesses have a different set of rules. Federal Tax Deposits (FTDs), which include withheld income tax, Social Security, and Medicare taxes, generally must be made via electronic funds transfer. For most businesses, this means using EFTPS. Sending a physical check for payroll taxes is often not allowed and can result in significant “failure to deposit” penalties. In this niche, the “where” is almost exclusively a digital destination. Understanding this distinction is vital for corporate compliance and maintaining the brand’s financial integrity.

Installment Agreements and Payment Plans

If a taxpayer cannot pay their full balance at once, they may enter into an installment agreement. The destination for these payments may be different from standard tax payments. Often, these are set up as automated debits (Direct Debit Installment Agreements), which is the IRS’s preferred method. If paying by check under an agreement, the payments are usually sent to a specific address listed on your monthly installment notice. Keeping these payments separate from other tax liabilities is essential for accurate accounting.

Optimizing Your Financial Workflow: Best Practices for Tax Delivery

Knowing where to send IRS payments is a tactical skill, but integrating that knowledge into a broader financial strategy is what separates successful individuals from those constantly playing catch-up with the government.

Ensuring Accuracy to Avoid Penalties

The IRS is a massive bureaucracy, and the burden of proof for payment usually lies with the taxpayer. To optimize your financial workflow, ensure every check includes your SSN or EIN, the tax year, and the form number (e.g., “2023 Form 1040”). This redundancy ensures that even if a voucher is separated from a check, the funds can still be traced to your account. From a personal finance perspective, this reduces the risk of having to pay a tax professional to resolve “lost” payment issues later.

Timing Your Payments for Cash Flow Management

In finance, the “time value of money” is a core principle. While you never want to be late, there is no inherent financial benefit to paying the IRS months in advance if you could be earning interest on those funds in a high-yield savings account. By using digital scheduling tools, you can set your payment for the exact due date (April 15th or the quarterly deadlines), keeping the “float” in your own account for as long as possible while still ensuring the payment arrives exactly where and when it needs to.

Security and Fraud Prevention

Finally, the “where” of IRS payments is often a target for scammers. The IRS will never ask for payments via wire transfer, gift cards, or cryptocurrency. Legitimate destinations are always either a “.gov” website or a U.S. Treasury-designated P.O. Box. By strictly adhering to the official channels outlined in this guide, you protect your capital from fraudulent actors. Whether you are an individual managing a household budget or a CFO overseeing corporate tax strategy, the security of your transmission method is the final safeguard in your financial planning.

In conclusion, the question of where to send IRS payments has multiple answers depending on your preferred technology, your location, and your specific tax situation. By prioritizing electronic methods for speed and security, or using certified mail and vouchers for physical payments, you can navigate tax season with the confidence that your financial obligations are handled professionally and accurately. Proper tax logistics are not just about compliance—they are a fundamental pillar of sound financial health.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.