Navigating the landscape of personal finance requires a delicate balance between wealth accumulation and risk mitigation. While many individuals focus heavily on investment portfolios and savings accounts, one of the most critical components of a robust financial plan is often overlooked: car insurance. For the average person, a vehicle is one of their most significant assets, yet it is also a source of substantial potential liability.

Understanding the “Big Three” types of car insurance is not just a matter of legal compliance; it is a fundamental exercise in financial security. Choosing the right coverage ensures that a single moment of misfortune on the road does not lead to a lifetime of debt or the total loss of your net worth. In this guide, we will break down the three primary types of car insurance—Liability, Collision, and Comprehensive—through the lens of financial management, helping you determine how to structure your policy for maximum protection and efficiency.

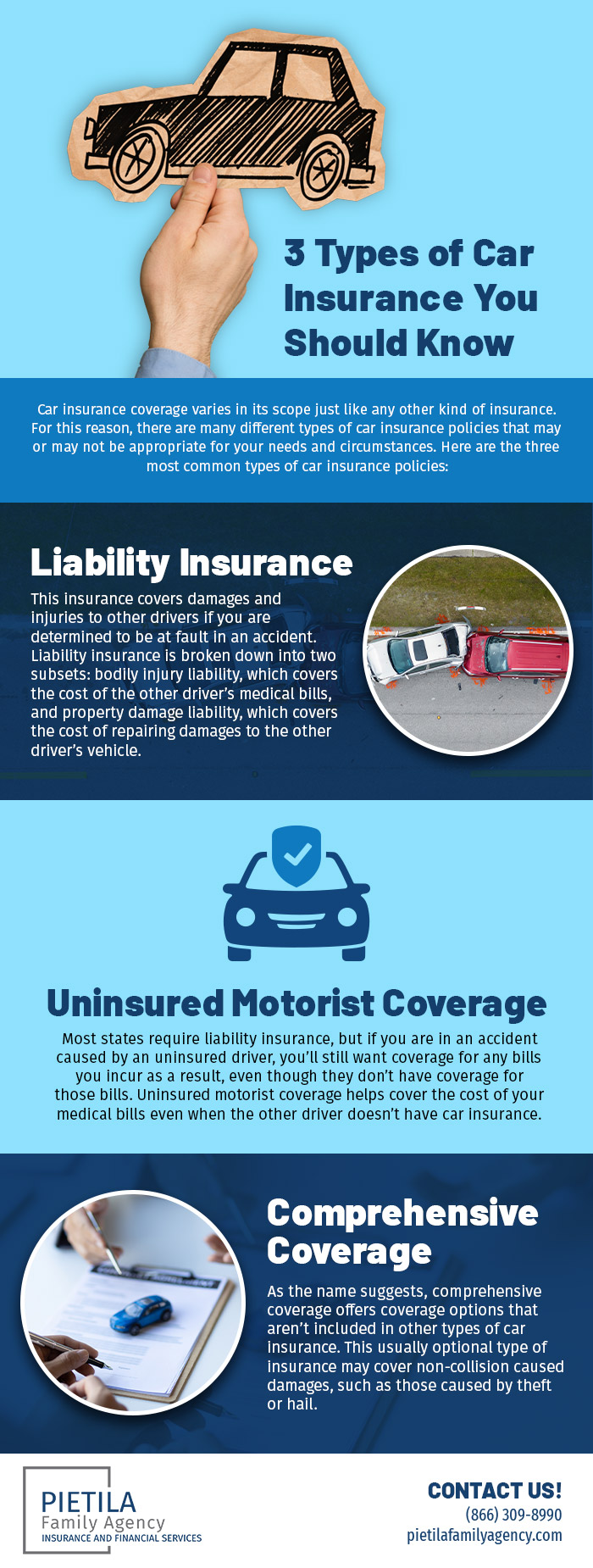

1. Liability Insurance: The Foundation of Personal Net Worth Protection

Liability insurance is the most basic and usually the only legally mandated type of car insurance. From a financial perspective, it serves as a shield for your assets. If you are found at fault in an accident, liability insurance pays for the other party’s expenses. Without it, your savings, home, and future wages could be seized to settle a judgment against you.

The Two Pillars of Liability Coverage

Liability coverage is divided into two distinct parts, both of which are essential for risk management:

- Bodily Injury Liability: This covers the medical expenses, lost wages, and legal fees associated with injuries to other people. In a litigious society, medical bills can easily reach six figures, making this coverage a vital safety net.

- Property Damage Liability: This pays for damage you cause to someone else’s property—usually their vehicle, but it can also include buildings, fences, or public infrastructure.

Determining Your Coverage Limits

Personal finance experts often advise against opting for the “state minimum” coverage. While minimums keep you legal, they are rarely sufficient to cover a serious accident. If you have a high net worth, you should carry liability limits that match or exceed your total assets. If your insurance limit is $50,000 but you cause $150,000 in damage, you are personally responsible for the $100,000 gap. Strategically increasing your liability limits is often one of the most cost-effective ways to buy financial peace of mind.

2. Collision and Comprehensive: Safeguarding Your Personal Assets

While Liability protects everyone else from you, Collision and Comprehensive coverage protect you from the world. In the world of finance, these are known as “first-party” coverages. They ensure that the capital you have invested in your vehicle is not wiped out by an accident, theft, or natural disaster.

Collision Insurance: Recovering from the Impact

Collision insurance pays to repair or replace your vehicle if it is damaged in an accident with another vehicle or an object (like a tree or a pole), regardless of who is at fault.

From an investment standpoint, Collision insurance is essential if you cannot afford to replace your vehicle out of pocket. For many, a car is the tool that enables them to reach their place of employment; losing that tool without the funds to replace it creates a cascading financial crisis. However, if your car is an older model with a low market value, the premiums for collision coverage might eventually exceed the potential payout, at which point a financial advisor might suggest “dropping” the coverage to save on monthly cash flow.

Comprehensive Insurance: Managing “Acts of God” and Theft

Comprehensive insurance covers almost everything that isn’t a collision. This includes theft, vandalism, fire, falling objects, and natural disasters like floods or hail.

In terms of financial strategy, Comprehensive coverage is often viewed as a low-cost way to mitigate high-impact risks. The likelihood of your car being stolen may be low, but the financial hit of losing a $30,000 asset overnight is high. By carrying comprehensive insurance, you transfer that risk to the insurance company for a relatively small annual fee.

3. The Financial Mechanics of Deductibles and Premiums

To master car insurance as a financial tool, one must understand the inverse relationship between premiums and deductibles. This is where your personal cash flow management meets your risk tolerance.

The Deductible as a Self-Insurance Tool

A deductible is the amount you pay out of pocket before your insurance kicks in. Choosing a higher deductible (e.g., $1,000 instead of $250) will significantly lower your monthly premium.

From a “Money” perspective, this is a form of self-insurance. If you have a healthy emergency fund, it is often financially savvy to opt for a higher deductible. You save money every month on premiums, and in the event of an accident, you have the liquid cash available to cover the deductible. Over a period of several years, the savings on premiums often far outweigh the cost of the occasional deductible payment.

Premiums and the Total Cost of Ownership

When budgeting for a new vehicle, many consumers only look at the monthly car payment. However, the insurance premium is a “soft cost” that can drastically alter the total cost of ownership. High-performance vehicles, cars with high theft rates, or cars with expensive specialized parts will command higher premiums for Collision and Comprehensive coverage. Always get an insurance quote before purchasing a vehicle to ensure the recurring cost fits within your monthly financial plan.

4. Specialized Add-Ons: Strategic Enhancements for Financial Security

Beyond the primary three types of insurance, there are several “riders” or additional coverages that can prevent specific financial pitfalls. Depending on your situation, these can be just as important as the core policy.

GAP Insurance: Protecting Against Negative Equity

If you finance a car with a small down payment, you may find yourself “underwater”—meaning you owe more on the loan than the car is worth. If the car is totaled, a standard Collision policy only pays the fair market value. GAP (Guaranteed Asset Protection) insurance covers the “gap” between the insurance payout and your remaining loan balance. This is a crucial tool for anyone who has financed a vehicle, preventing a situation where you are paying off a loan for a car you can no longer drive.

Uninsured and Underinsured Motorist Coverage

Statistically, a significant percentage of drivers on the road carry no insurance or insufficient insurance. If one of these drivers hits you, your Liability insurance won’t help you, and their lack of assets means you likely won’t recover funds through a lawsuit. Uninsured Motorist (UM) coverage acts as a safety net, paying for your medical bills and property damage when the at-fault party cannot. In the context of financial planning, this is an essential safeguard against the financial negligence of others.

5. Optimizing Your Policy for Long-Term Wealth

Car insurance should not be a “set it and forget it” expense. As your life changes, your financial needs and the value of your assets change, necessitating a review of your coverage.

Periodic Audits and Market Comparison

Insurance companies use complex algorithms to determine rates, and these change frequently. To optimize your personal finances, it is wise to shop your policy every 12 to 24 months. Furthermore, as your vehicle ages and its value depreciates, the cost-benefit analysis for carrying Collision and Comprehensive insurance shifts. Once the annual cost of the premium plus the deductible approaches the total value of the car, it is often more profitable to stop the coverage and redirect those funds into a dedicated “car replacement” savings account.

![]()

Leveraging Discounts and Loyalty

Most insurers offer discounts that can bolster your bottom line. These include bundling (combining auto and homeowners insurance), good driver discounts, and discounts for safety features. Additionally, some companies offer “vanishing deductibles” for years of accident-free driving. By actively managing these factors, you can reduce your fixed costs and increase the amount of capital available for investing and wealth building.

In conclusion, car insurance is a pillar of personal finance that serves as both a defensive shield and a strategic tool. By understanding the nuances of Liability, Collision, and Comprehensive coverage, and by aligning your deductibles and add-ons with your overall financial goals, you ensure that your journey toward financial independence is not derailed by the unpredictable nature of the road. Protect your assets, manage your risks, and treat your insurance policy as the vital financial document that it truly is.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.