Deciding to close a bank account is a significant step in managing your personal finances. Whether you are moving toward a high-yield online savings account, switching to a local credit union, or simply consolidating your assets to simplify your financial life, closing an account with a major institution like Wells Fargo requires more than just withdrawing your cash and walking away.

In the modern financial ecosystem, your bank account serves as the central nervous system for your income, bills, and subscriptions. Severing this connection without a plan can lead to missed payments, overdraft fees, and unnecessary stress. This guide provides a professional, step-by-step roadmap to closing your Wells Fargo account while ensuring your financial health remains intact.

The Strategic Pre-Closing Checklist: Preparing Your Finances

Before you contact Wells Fargo to terminate your relationship, you must perform a thorough audit of your current financial activity. Closing an account prematurely is a common mistake that can lead to “zombie transactions”—charges that hit a closed account and force it back open, often triggering fees.

Auditing Automatic Payments and Direct Deposits

The first step in a successful transition is identifying every automated flow of money. Most consumers have dozens of “hidden” transactions linked to their Wells Fargo checking account. You should review at least three to six months of bank statements to identify:

- Direct Deposits: Contact your employer’s HR department to redirect your payroll. This often takes one to two pay cycles to take effect.

- Subscription Services: Streaming platforms, gym memberships, and software subscriptions usually pull directly from a debit card or via ACH.

- Utility and Bill Payments: Ensure your electricity, water, internet, and insurance providers have your new banking information.

Establishing Your New Financial Home

Never close your old account until your new one is fully operational. Open your new account at your chosen institution and fund it with enough capital to cover a month of expenses. By maintaining a “buffer” period where both accounts are active, you can monitor for any stray automated payments you might have missed during your audit.

Handling the Final Balance

While it is tempting to withdraw every cent immediately, it is often wiser to leave a small balance (around $50 to $100) until the very day you close the account. This prevents the account from falling below “minimum balance” requirements that might trigger a monthly service fee just as you are trying to leave. Once you are ready to speak with a representative, you can request the final balance via a cashier’s check or a wire transfer.

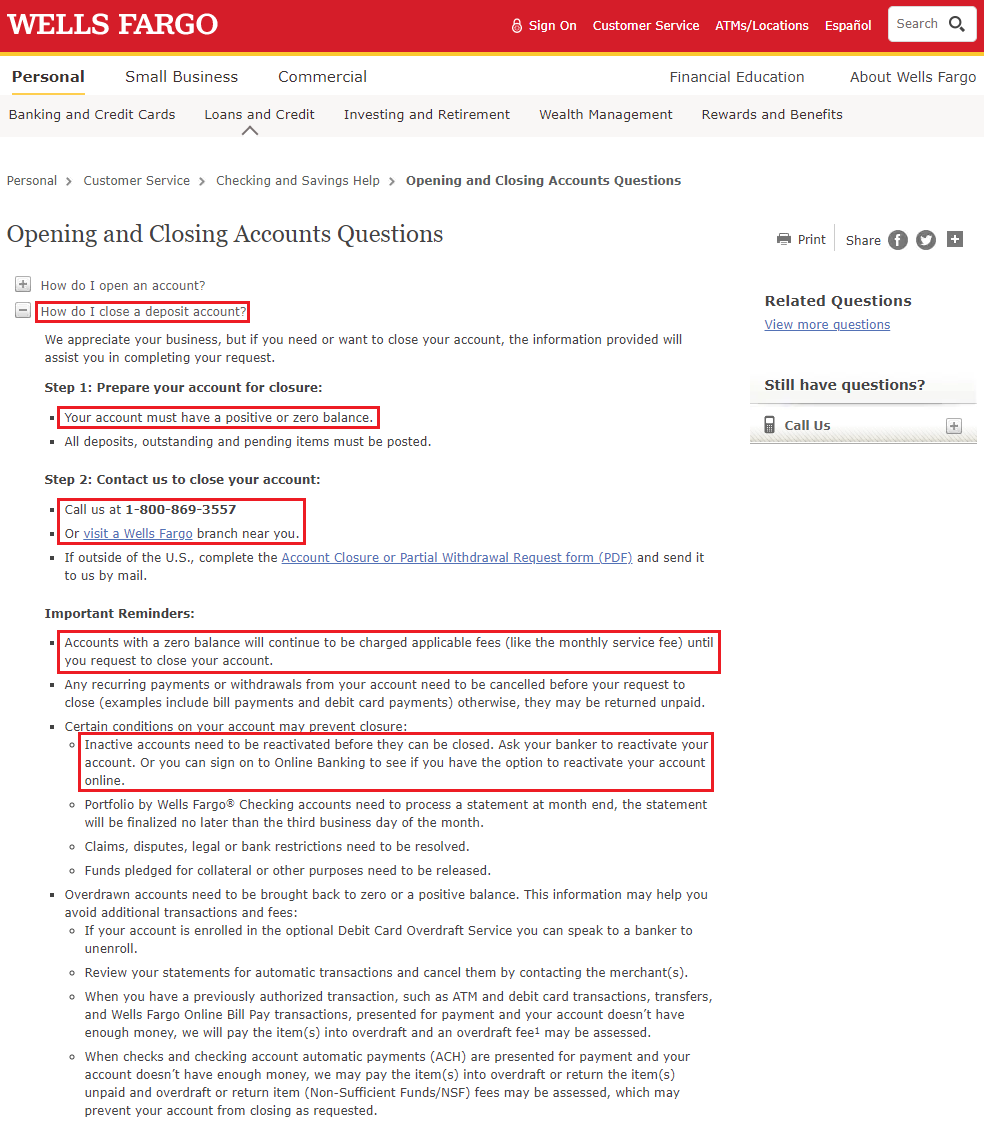

The Step-by-Step Process to Close Your Wells Fargo Account

Wells Fargo offers several channels for closing an account. The method you choose should depend on your preference for documentation and your proximity to a physical branch.

Method 1: Visiting a Local Branch (In-Person)

For many, the most effective way to close an account is to visit a Wells Fargo branch in person. This allows for immediate resolution and provides you with a physical paper trail.

- Bring Identification: You will need a government-issued ID (driver’s license or passport) and your account details.

- Speak with a Personal Banker: Request to close the account entirely. They may ask why you are leaving; you are not obligated to provide a detailed explanation, but citing “consolidating finances” is a standard, professional response.

- Request a Closing Statement: Before leaving, ensure you receive a document stating the account is closed with a $0.00 balance.

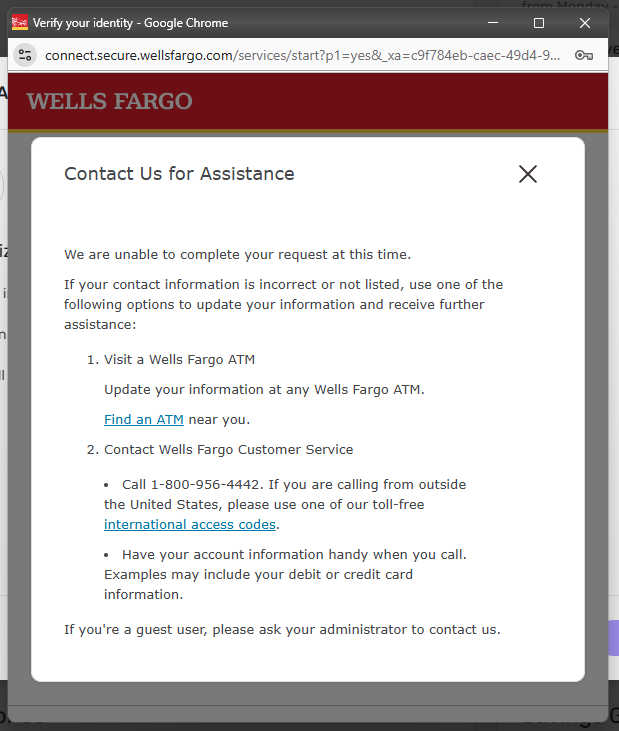

Method 2: Closing via Telephone

If you cannot visit a branch, you can close most personal checking or savings accounts over the phone.

- Call Customer Service: Dial Wells Fargo’s general banking line (1-800-869-3557).

- Verification: Be prepared to answer security questions to verify your identity.

- The Request: Clearly state that you wish to close the account. If there is a remaining balance, the representative will typically offer to mail a check to the address on file. Note that this may take 7–10 business days to arrive.

Method 3: Written Request (The Certified Mail Approach)

For those who prefer a formal record of their request, sending a letter is a valid option. This is particularly useful if you are currently abroad or if you want to ensure there is a legal record of your request.

- Write a letter including your name, account number, and a clear instruction to close the account.

- Include instructions on where to send the remaining balance.

- Crucial Step: Send the letter via Certified Mail with Return Receipt Requested. This provides proof that Wells Fargo received your request, which is vital if any fees are charged after the date of delivery.

Post-Closing Considerations: Protecting Your Credit and Records

Closing the account is not the final step. To maintain optimal financial security and organization, you must manage the “afterlife” of your account data.

Securing Your Financial History

Once an account is closed, your access to the Wells Fargo online banking portal will likely be terminated or severely restricted. Before you initiate the closure, download the last 24 months of bank statements and any tax documents (like 1099-INT forms for interest earned). You may need these for future loan applications, tax filings, or audits. Digital records are easier to store, but ensure they are kept in an encrypted or password-protected folder.

Monitoring for “Zombie” Accounts and Credit Impact

A “zombie account” occurs when a merchant attempts to charge a closed account, and the bank honors the payment, effectively reopening the account and putting you in a negative balance. Monitor your mail for any communication from Wells Fargo for 60 days following the closure.

Regarding your credit score: Closing a checking or savings account generally does not affect your credit score, as these are not credit lines. However, if an account is closed with a negative balance that goes unpaid, it can be reported to ChexSystems or debt collectors, which will severely damage your ability to open bank accounts in the future.

Managing Linked Credit Cards

If you have a Wells Fargo credit card linked to your checking account for “Overdraft Protection,” closing the checking account will break that link. Ensure you have set up a new payment method for your credit card to avoid late fees or missed payments on your debt obligations, as those do impact your credit score.

Financial Optimization: Where to Move Your Capital?

Choosing to leave a traditional “Big Four” bank like Wells Fargo often opens the door to better financial products. As you transition, consider where your money will work hardest for you.

High-Yield Savings Accounts (HYSA)

Traditional banks often offer interest rates as low as 0.01% on savings. In contrast, online-only banks often offer rates significantly higher. By moving your “emergency fund” or long-term savings to a high-yield account, you could earn hundreds of dollars more in interest annually. When selecting a new bank, prioritize those with no monthly maintenance fees and robust mobile apps.

The Benefits of Credit Unions

If you prefer a more community-focused approach to personal finance, a credit union may be the right choice. Credit unions are member-owned cooperatives. Because they are not-for-profit, they often return “profits” to members in the form of lower interest rates on loans and higher interest rates on deposits. For many, the personalized service of a credit union outweighs the national footprint of a major bank.

Consolidating for Simplicity

In the world of personal finance, “complexity is the enemy of execution.” If you find yourself managing five different bank accounts across four institutions, it may be time to consolidate. Keeping your primary checking and your emergency savings in one or two high-quality institutions makes it easier to track your net worth, monitor for fraud, and stay on top of your budget.

Conclusion: Taking Control of Your Financial Narrative

Closing a Wells Fargo account is more than a clerical task; it is a declaration of your intent to optimize your financial life. By following a structured approach—auditing your automated transactions, choosing the right closure method, and securing your historical data—you ensure a seamless transition that protects your assets and your reputation.

In today’s competitive financial landscape, you have the power to choose an institution that aligns with your values and financial goals. Whether you are seeking higher returns, lower fees, or better customer service, the process of moving your money is the first step toward a more intentional and prosperous financial future. Once the final statement arrives and the balance reads zero, you are free to deploy your capital where it serves you best.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.