The intersection of labor policy and personal finance has recently been dominated by a singular, provocative proposal: the elimination of federal income taxes on tips. For millions of service industry workers—ranging from restaurant servers and bartenders to hair stylists and ride-share drivers—this shift represents a potential sea change in their annual take-home pay. However, as with any major shift in fiscal policy, the question of “when” is inextricably linked to the complexities of the legislative process, the federal budget, and the nuances of the Internal Revenue Code. Understanding the timeline and the mechanics of this proposal is essential for anyone whose livelihood depends on the generosity of customers and the precision of tax law.

The Policy Proposal: What “No Tax on Tips” Actually Means

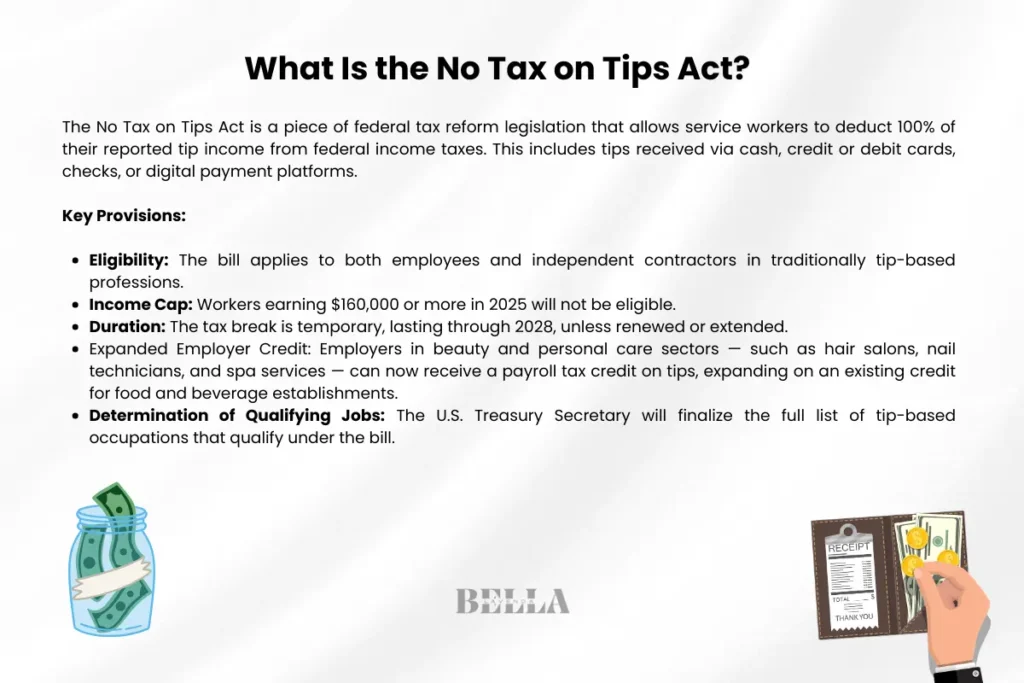

To understand when a “no tax on tips” policy might go into effect, one must first understand what exactly is being proposed. Currently, the IRS treats tips as taxable income, subject to federal income tax, Social Security, and Medicare taxes. The recent momentum to eliminate these taxes aims to provide immediate relief to low- and middle-income earners in the service sector.

The Current Taxation Landscape for Tipped Employees

Under current law, employees who receive more than $20 in tips in any given month are required to report those tips to their employer. These tips are then bundled with their hourly wages and taxed at the appropriate marginal rate. Furthermore, both the employer and the employee are responsible for their respective shares of FICA (Federal Insurance Contributions Act) taxes, which fund Social Security and Medicare. For many workers, these taxes can eat away significantly at the extra income earned through exceptional service, often placing a heavy administrative and financial burden on those who can least afford it.

How the New Proposal Aims to Change the Status Quo

The proposed “no tax on tips” framework generally seeks to exempt gratuities from federal income tax. Some versions of the proposal go further, suggesting an exemption from payroll taxes as well. The primary objective is to put more liquid cash directly into the pockets of service workers without requiring them to wait for a tax refund at the end of the year. From a financial perspective, this would effectively raise the “real” wage of tipped workers without requiring a direct increase in the minimum wage, which has historically been a more contentious legislative battle.

Legislative Timelines and the Path to Implementation

The timeline for when “no tax on tips” will go into effect is not determined by a single decree but by the rigorous machinery of the U.S. government. As of now, the proposal remains in the realm of legislative debate and campaign platforms, meaning implementation is not immediate.

The Role of the Executive Branch and Congress

For this proposal to become reality, it must be drafted into a formal bill, such as the “No Tax on Tips Act,” and pass through both the House of Representatives and the Senate. Because this involves a significant change to the tax code, it must navigate the House Ways and Means Committee and the Senate Finance Committee. The earliest such a bill could realistically be debated and passed would be during the first legislative session of a new or renewed administration. Historically, major tax overhauls—like the Tax Cuts and Jobs Act of 2017—take several months to move from a proposal to a signed law.

Key Milestones to Watch in the Coming Fiscal Years

If a bill were to be signed into law in early 2025, the implementation date would likely be tied to the start of a new tax year. In most scenarios, tax changes are not retroactive to the beginning of a calendar year unless specifically stated. Therefore, the most optimistic timeline for “no tax on tips” to go into effect would be January 1, 2025, or January 1, 2026. Financial analysts suggest that the IRS would also need a lead time of at least six months to update their forms, digital filing systems, and employer reporting guidelines to accommodate the new exemptions.

Financial Impact Analysis for the American Workforce

For the individual worker, the elimination of taxes on tips is more than a policy talking point; it is a fundamental shift in personal financial planning. The impact varies depending on the worker’s total income and the percentage of that income derived from gratuities.

Boosting Net Take-Home Pay for Service Workers

The most immediate benefit of this policy is the increase in net take-home pay. For a server earning $30,000 a year, where $15,000 of that comes from tips, the tax savings could range from $1,500 to $3,000 annually, depending on their tax bracket and filing status. In the context of personal finance, this “found money” can be redirected toward emergency funds, debt repayment, or long-term investments. For many in the service industry, who often lack access to employer-sponsored retirement plans, this extra cash flow could be the catalyst for starting an Individual Retirement Account (IRA).

Potential Shifts in Consumer Tipping Behavior

There is a psychological component to this financial shift that cannot be ignored. If consumers are aware that their tips are no longer taxed, it remains to be seen whether they will tip more or less. Some economists argue that customers might feel their tip “goes further” and thus maintain or increase their percentages. Others worry that if the policy is viewed as a significant “raise” for workers, the social pressure to tip high percentages may diminish. From a personal finance standpoint, workers should not necessarily count on increased tip volumes; rather, they should focus on the guaranteed retention of the tips they do receive.

Business Finance and Employer Obligations

The “no tax on tips” policy doesn’t just affect the employees; it has massive implications for business finance, particularly for small business owners in the hospitality and service sectors. Employers currently play a vital role in tracking, reporting, and withholding taxes on tips.

Changes to Payroll Processing and FICA Taxes

If tips are exempted from federal income tax but still subject to payroll taxes (Social Security and Medicare), the complexity for payroll departments increases. However, if the proposal eliminates payroll taxes on tips as well, business owners would see a direct reduction in their own tax liabilities, as they would no longer have to pay the employer’s share of FICA on those tips. This could free up capital for restaurant owners to reinvest in their facilities, expand their staff, or improve other benefits like health insurance.

Compliance and Reporting Standards in a Tax-Free Tipping Era

One of the major hurdles for the IRS in a “no tax on tips” environment is the risk of “reclassification.” If tips are tax-free but wages are taxed, there is a financial incentive for both employers and employees to shift as much compensation as possible into the “tip” category. To prevent this, any new law would likely require strict reporting standards and perhaps a cap on what qualifies as a “tax-free tip” relative to the hourly wage. Business owners would need to upgrade their financial tracking software to ensure that their records distinguish clearly between taxable wages and non-taxable gratuities to avoid costly audits.

Broader Economic Consequences and Long-Term Outlook

Looking at the “Money” aspect on a macro level, the elimination of tax on tips carries significant weight for the federal budget and the broader economy. Every tax exemption comes with a “price tag” in terms of lost federal revenue.

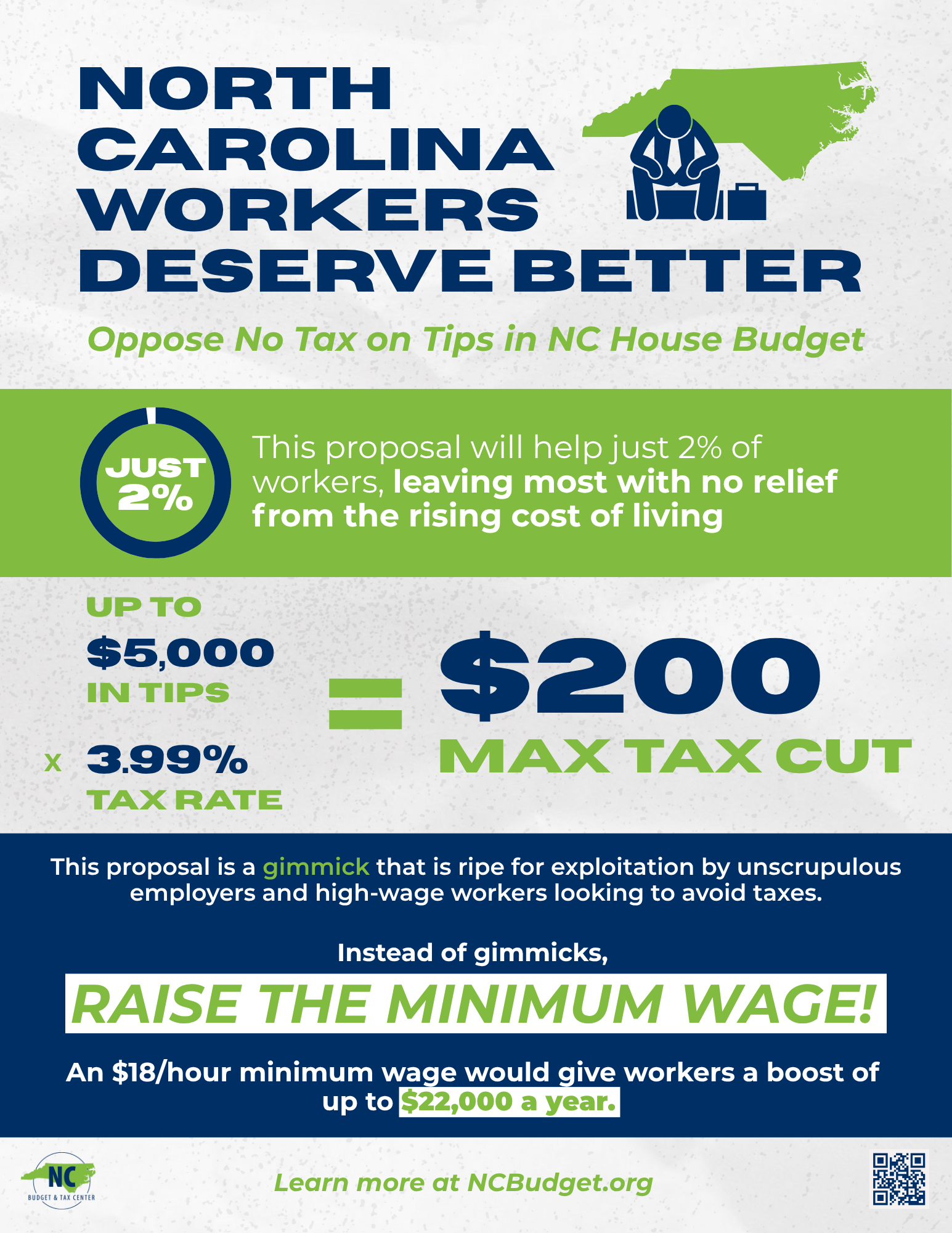

Federal Revenue Projections and the Deficit

The non-partisan Committee for a Responsible Federal Budget has estimated that eliminating federal income and payroll taxes on tips could reduce federal revenue by $150 billion to $250 billion over a decade. In an era of high national debt, this loss of revenue must be weighed against the economic stimulus provided by putting more money in the hands of consumers. From an investment perspective, increased consumer spending in the service sector could bolster the stocks of major restaurant groups and hospitality conglomerates, potentially offsetting some of the broader fiscal concerns.

Is This a Sustainable Model for the Future of Work?

Finally, we must consider whether this policy is a permanent solution or a temporary financial patch. As the “gig economy” continues to grow, more workers are finding themselves in positions where tips or “bonuses” make up a significant portion of their income. A tax-free tipping environment could accelerate the shift away from traditional salaried roles toward performance-based or service-based compensation. While this offers flexibility and the potential for higher earnings, it also places the onus of financial stability more squarely on the individual worker.

In conclusion, while the question of when “no tax on tips” will go into effect remains tied to the 2024 election and subsequent legislative cycles, the how is already being mapped out by financial experts and policy makers. For the worker, the focus should remain on maximizing current earnings and staying informed on tax law changes. For the business owner, the focus should be on preparing financial systems for a potential shift in reporting requirements. Regardless of the start date, the “no tax on tips” movement represents a significant evolution in how the American economy values and taxes service-based labor.

aViewFromTheCave is a participant in the Amazon Services LLC Associates Program, an affiliate advertising program designed to provide a means for sites to earn advertising fees by advertising and linking to Amazon.com. Amazon, the Amazon logo, AmazonSupply, and the AmazonSupply logo are trademarks of Amazon.com, Inc. or its affiliates. As an Amazon Associate we earn affiliate commissions from qualifying purchases.